Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Recent logistics industry assessments indicate that the UK last mile delivery market generated approximately USD ~ billion in annual revenue according to logistics activity reports from the Office for National Statistics and parcel market insights from Ofcom. Market expansion is strongly driven by the rapid growth of digital commerce platforms, increasing consumer demand for rapid parcel deliveries, and widespread adoption of automated sorting and route optimization technologies across national logistics networks serving millions of daily online retail transactions.

Major urban regions such as London, Manchester, Birmingham, and Leeds dominate logistics demand due to dense population centers, extensive e commerce retail activity, and well developed transportation infrastructure supporting rapid parcel distribution. London remains the largest logistics hub because of high consumer purchasing activity and the concentration of national distribution centers. Northern logistics corridors across the Midlands and Greater Manchester also experience strong demand as fulfillment centers support nationwide parcel distribution networks.

Market Segmentation

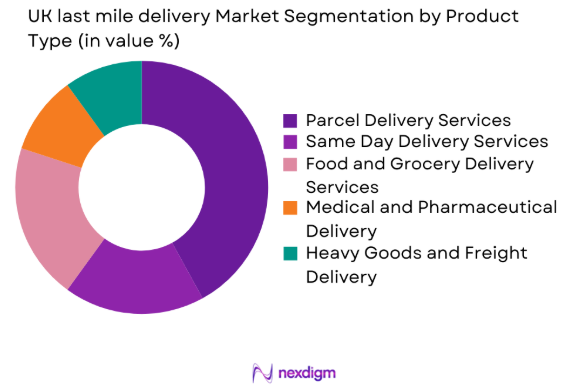

By Product Type

UK Last-Mile Delivery market is segmented by product type into parcel delivery services, same day delivery services, food and grocery delivery services, medical and pharmaceutical delivery, and heavy goods delivery. Recently, parcel delivery services have a dominant market share due to strong growth in online retail shipments across consumer electronics, clothing, household goods, and packaged consumer products. Major logistics providers operate large automated parcel sorting facilities capable of processing thousands of shipments daily, enabling efficient nationwide delivery networks connecting fulfillment centers with residential customers.

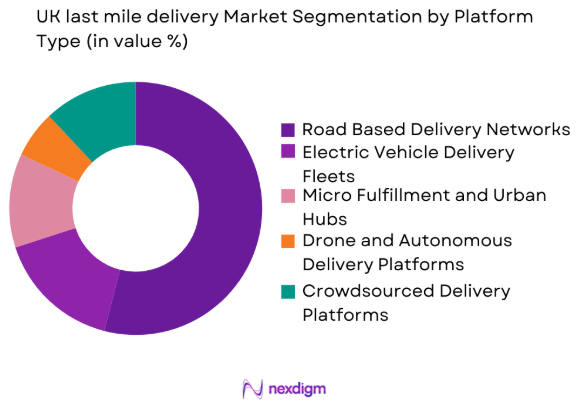

By Platform Type

UK Last-Mile Delivery market is segmented by platform type into road based delivery networks, electric vehicle delivery fleets, micro fulfillment hubs, drone and autonomous delivery platforms, and crowdsourced delivery platforms. Recently, road based delivery networks dominate market share because traditional van based courier operations remain the most widely deployed infrastructure for parcel distribution. Major logistics providers maintain extensive vehicle fleets and regional depots enabling efficient national parcel transportation across urban and suburban delivery networks.

Competitive Landscape

The UK last mile delivery market is moderately consolidated with several large logistics providers controlling national parcel distribution networks supported by advanced warehousing and sorting infrastructure. Companies compete through delivery speed, geographic coverage, fleet efficiency, and technology adoption. Large players invest heavily in automated parcel hubs, digital tracking systems, and electric vehicle fleets to strengthen operational efficiency and environmental compliance across urban delivery networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| Royal Mail Group | 1516 | London | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| Amazon Logistics | 2014 | Seattle | ~ | ~ | ~ | ~ | ~ |

| DPDgroup | 1977 | Paris | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta | ~ | ~ | ~ | ~ | ~ |

UK last mile delivery Market Analysis

Growth Drivers

Expansion of E Commerce Retail Logistics Networks

Rapid expansion of online retail platforms across the United Kingdom significantly increases demand for efficient last mile delivery services transporting parcels from fulfillment centers to residential consumers. Digital marketplaces process high transaction volumes requiring advanced logistics infrastructure capable of managing large shipment flows and rapid delivery schedules. Retail companies increasingly depend on specialized courier providers operating automated sorting facilities and nationwide vehicle fleets to improve operational efficiency. Growth of mobile commerce and digital payments further expands online purchasing across electronics, clothing, groceries, and household goods. Logistics providers invest in route optimization software, robotics enabled parcel sorting systems, and predictive analytics. Urban fulfillment hubs near large population centers also improve delivery speed and distribution efficiency.

Rising Consumer Demand for Same Day and Time Definite Delivery Services

Changing consumer purchasing behavior significantly increases demand for extremely fast parcel delivery services across urban regions throughout the United Kingdom. Online shoppers increasingly expect same day or next day delivery options when purchasing goods through digital marketplaces, which forces logistics providers to redesign delivery operations and distribution networks to meet strict timelines. Retailers collaborate with courier providers capable of offering time specific delivery windows that enhance customer satisfaction and brand loyalty. Logistics companies deploy route optimization software, real time tracking systems, and predictive demand analytics to coordinate deliveries efficiently across metropolitan areas. Expansion of urban micro fulfillment centers allows inventory storage closer to consumers, reducing delivery times. Food and grocery delivery platforms also intensify demand for rapid logistics services.

Market Challenges

Urban Traffic Congestion and Delivery Inefficiencies

Increasing urban population density across major cities such as London, Birmingham, and Manchester creates severe traffic congestion that significantly affects the operational efficiency of last mile delivery services across metropolitan logistics networks. Delivery vehicles frequently face delays caused by heavy traffic conditions, restricted road access, and limited loading zones which extend delivery timelines and reduce daily parcel handling capacity. Municipal transportation policies including congestion pricing and restricted vehicle zones further limit vehicle movement within central city districts. Logistics providers therefore redesign distribution networks using micro fulfillment hubs and alternative delivery methods including bicycle couriers and electric cargo vehicles suited for dense urban environments. High parcel volumes from digital commerce platforms further intensify congestion near major distribution hubs.

Rising Operational Costs Across Logistics Infrastructure and Delivery Fleets

Operating last mile logistics networks requires substantial investment in transportation fleets, warehouse infrastructure, workforce management, and digital logistics platforms supporting large scale parcel distribution. Rising fuel prices, vehicle maintenance costs, labor wages, and warehouse rentals increase operational expenses for courier providers across the United Kingdom. Logistics companies also invest in automation technologies such as robotics enabled parcel sorting, digital tracking systems, and route optimization software to improve efficiency. Environmental regulations encouraging transition to electric delivery fleets further raise capital expenditure due to vehicle costs and charging infrastructure requirements. Competitive pricing pressures and workforce shortages also increase operational costs, requiring continuous optimization of logistics operations.

Opportunities

Expansion of Electric Vehicle Based Urban Delivery Networks

Increasing environmental sustainability policies across the United Kingdom create strong opportunities for logistics providers to adopt electric vehicle delivery fleets that reduce emissions and improve operational efficiency. Urban governments implement stricter emission standards and low emission transport zones encouraging the use of electric vans, cargo bicycles, and other sustainable delivery solutions within city centers. Electric fleets offer benefits such as lower energy costs, reduced maintenance expenses, and improved environmental compliance compared with diesel vehicles. Retail companies increasingly prefer logistics partners that support sustainable supply chains. Expanding charging infrastructure and government incentives including subsidies and tax benefits further accelerate adoption of electric delivery fleets across urban logistics networks.

Development of Urban Micro Fulfillment Centers Supporting Rapid Delivery Services

Retailers and logistics providers increasingly invest in compact urban fulfillment centers that store high demand inventory closer to consumers in densely populated metropolitan areas. These micro fulfillment facilities allow companies to process online orders quickly and dispatch deliveries within very short timeframes supporting same day and rapid delivery services. Automated warehouses integrate robotics based inventory systems and advanced sorting technologies to process large order volumes efficiently. Logistics providers connect these centers with electric delivery fleets and bicycle couriers for short distance urban transportation. Businesses benefit from reduced transportation distances lower delivery costs and faster order processing. Expanding consumer demand for rapid deliveries continues strengthening the importance of micro fulfillment infrastructure across urban logistics networks.

Future Outlook

The UK last mile delivery market is expected to experience sustained expansion driven by continued growth in digital commerce and rapid delivery expectations among consumers. Technological innovations including automation, artificial intelligence route optimization, and electric vehicle logistics fleets will reshape distribution networks. Government environmental policies will accelerate adoption of sustainable transportation technologies. Expansion of micro fulfillment infrastructure and advanced parcel sorting facilities will further strengthen delivery efficiency and logistics capacity across national retail supply chains.

Major Players

- Royal Mail Group

- DHL Supply Chain

- UPS

- FedEx

- Amazon Logistics

- Evri

- DPDgroup

- Yodel

- Stuart Delivery

- Deliveroo

- Uber Eats Logistics

- Just Eat Takeaway Logistics

- Whistl

- DX Group

- Gophr

Key Target Audience

- Logistics and transportation companies

- E commerce retailers

- Courier and parcel service providers

- Supply chain technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail distribution companies

- Urban infrastructure planners

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the UK last mile delivery market were identified through analysis of logistics activity reports, government transportation statistics, and retail distribution data. Demand drivers such as digital commerce expansion, parcel shipment volumes, and urban logistics infrastructure were evaluated to determine key industry trends.

Step 2: Market Analysis and Construction

Market sizing involved combining logistics industry revenue data, parcel shipment volumes, and courier service performance indicators to construct a comprehensive market framework. Multiple data sources including government transport reports and logistics industry publications were used to validate sector scale.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses regarding delivery infrastructure development, technology adoption, and logistics investment trends were validated through consultations with supply chain experts, transportation analysts, and logistics sector specialists with operational experience.

Step 4: Research Synthesis and Final Output

All validated insights were integrated into a structured market framework combining qualitative analysis and quantitative logistics indicators. The final output synthesizes sector trends, operational dynamics, and competitive strategies influencing the UK last mile delivery ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E Commerce Fulfillment Networks

Rapid Growth of Same Day and Instant Delivery Services

Urban Logistics Infrastructure Investments - Market Challenges

Urban Traffic Congestion and Delivery Inefficiencies

High Operational Costs in Last Mile Logistics

Labor Shortages in Courier and Delivery Operations - Market Opportunities

Adoption of Electric Vehicle Delivery Fleets

Development of Micro Fulfillment Centers

Integration of Autonomous Delivery Technologies - Trends

Growth of Urban Micro Fulfillment Networks

Increasing Use of Delivery Route Optimization Software

Expansion of Gig Economy Courier Platforms - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Same Day Delivery Services

Food and Grocery Delivery Services

Medical and Pharmaceutical Delivery

Heavy Goods and Freight Delivery - By Platform Type (In Value%)

Road Based Delivery Networks

Electric Vehicle Delivery Fleets

Micro Fulfillment and Urban Hubs

Drone and Autonomous Delivery Platforms

Crowdsourced Delivery Platforms - By Fitment Type (In Value%)

Dedicated Logistics Networks

Retailer Integrated Delivery Systems

Third Party Logistics Partnerships

Platform Based Delivery Integration

Hybrid Fulfillment Delivery Systems - By End User Segment (In Value%)

E Commerce Retailers

Grocery and Food Delivery Platforms

Healthcare and Pharmaceutical Companies

Consumer Electronics Retailers

Industrial and Commercial Distributors - By Procurement Channel (In Value%)

Direct Retailer Logistics Contracts

Third Party Logistics Providers

Digital Marketplace Delivery Platforms

Courier and Parcel Service Agreements

Integrated Omnichannel Logistics Contracts

- Market Share Analysis

- Cross Comparison Parameters (Delivery Speed Capability, Fleet Technology Adoption, Geographic Coverage, Automation Integration, Retail Partnership Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Royal Mail Group

DPD group

DHL Supply Chain

Amazon Logistics

UPS

Evri

FedEx

Yodel

Just Eat Takeaway Logistics

Deliveroo

Uber Eats Logistics

Stuart Delivery

Gophr

DX Group

Whistl

- Rising demand from digital commerce retailers for rapid parcel distribution

- Growth of grocery delivery platforms requiring hyperlocal logistics infrastructure

- Healthcare providers adopting temperature controlled last mile distribution

- Electronics retailers expanding direct to consumer delivery networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now