Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Military Aviation Market has seen significant growth driven by ongoing investments in advanced aircraft, defense technologies, and increased demand for security services. The market size, based on recent historical assessments, is valued in the range of USD ~ billion, propelled by government defense budgets, strategic defense alliances, and the need for enhanced national security capabilities.

The dominance of the UK military aviation sector is largely centered around key cities such as London, Bristol, and Stevenage. These locations are home to major defense contractors and research facilities, fostering innovation and technological advancements. The country’s established infrastructure, proximity to international defense allies, and robust regulatory framework further enhance its position as a leader in military aviation development.

Market Segmentation

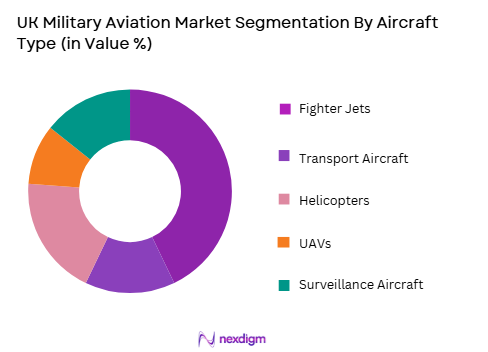

By Aircraft Type

The UK military aviation market is segmented by aircraft type into fighter jets, transport aircraft, helicopters, unmanned aerial vehicles (UAVs), and surveillance aircraft. Recently, fighter jets have a dominant market share due to factors such as increasing demand for advanced defense systems, ongoing modernization programs, and strategic defense needs. The UK’s commitment to enhancing its air superiority capabilities, as well as its partnerships with NATO allies, significantly contribute to the growing reliance on high-performance fighter jets, which are integral to national defense operations.

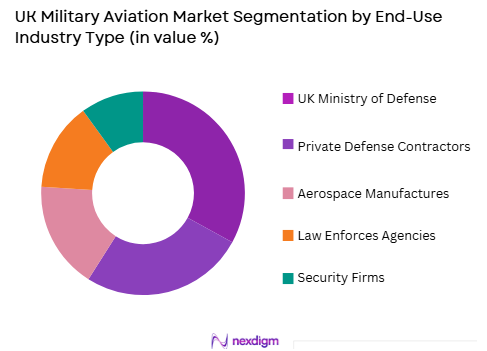

By End-User

The market is segmented by end-user into the UK Ministry of Defence (MOD), private defense contractors, aerospace manufacturers, law enforcement agencies, and security firms. The UK Ministry of Defence has a dominant market share due to its substantial defense budget and increasing investment in modernizing military aviation assets. The MOD’s involvement in strategic defense planning, procurement of advanced military aircraft, and funding for military aviation projects underscores its significant influence on the market’s growth trajectory.

Competitive Landscape

The UK Military Aviation Market is highly competitive with a mix of established players and new entrants offering advanced defense solutions. The market is characterized by consolidation, where key players continue to expand their technological capabilities and partnerships to maintain a strategic advantage. Companies are also focusing on research and development to meet the ever-evolving demands of modern warfare. The influence of major players like BAE Systems, Leonardo, and Rolls-Royce plays a pivotal role in driving innovation within the market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Military Aviation Focus |

| BAE Systems | 1999 | Farnborough | ~ | ~ | ~ | ~ | ~ |

| Leonardo | 1948 | London | ~ | ~ | ~ | ~ | ~ |

| Rolls-Royce | 1906 | Derby | ~ | ~ | ~ | ~ | ~ |

| Airbus | 1970 | Toulouse | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda | ~ | ~ | ~ | ~ | ~ |

UK Military Aviation Market Analysis

Growth Drivers

Increased Government Spending on Defense

The UK’s military aviation market is primarily driven by the substantial government investment in defense. The UK government has committed to upgrading its military infrastructure, bolstering its defense capabilities, and enhancing the UK’s air superiority through advanced aviation technology. As part of its defense strategy, the government has focused on the procurement of high-tech aircraft and defense systems, including stealth fighters and UAVs, to ensure national security. This focus on strengthening air defense infrastructure results in a consistent increase in market demand for military aviation equipment. Furthermore, rising geopolitical tensions globally necessitate continued investment in the defense sector. The government’s commitment to defense expenditure, as seen in the Integrated Review and Defence Command Paper, ensures the steady flow of contracts for aviation technology providers and supports growth in the military aviation market.

Technological Advancements in Aircraft Systems

Another key driver of growth in the UK Military Aviation Market is the continuous advancement of aircraft systems. The UK is investing heavily in developing and integrating next-generation aircraft technologies, including autonomous systems, advanced avionics, and AI-powered aircraft management systems. Innovations such as the Tempest fighter jet, which is expected to be a cornerstone of the UK’s defense strategy, highlight the trend towards highly capable, technologically sophisticated aviation solutions. The development and integration of these technologies enable the military to stay ahead of evolving threats and enhance the capabilities of both manned and unmanned aerial platforms. As defense forces seek greater operational efficiency, the demand for cutting-edge technologies in the aviation sector is expected to grow substantially.

Market Challenges

High Capital Investment Requirements

One of the major challenges facing the UK Military Aviation Market is the significant capital investment required to maintain and develop advanced aircraft systems. The procurement of state-of-the-art fighter jets, UAVs, and surveillance systems entails high upfront costs, which may pose a challenge to maintaining consistent growth in the market. Additionally, the ongoing need for upgrades to existing aircraft fleets further adds to the financial burden on defense budgets. This is particularly challenging for smaller defense contractors and companies looking to enter the market. High initial capital expenditure also results in long development cycles and delayed returns on investment, making it harder for companies to compete with industry giants who have deeper financial resources and established infrastructure. Despite government spending, the sector faces budgetary constraints and prioritization of defense projects, which can delay new acquisitions and technological advancements.

Regulatory and Compliance Hurdles

The regulatory landscape for military aviation is complex, with multiple layers of government oversight, international defense agreements, and export control regulations. The UK’s exit from the European Union has added a layer of complexity to the regulation of military aviation exports, particularly to European Union member states. Export licensing and the compliance with defense procurement regulations also create hurdles for businesses, especially when trying to navigate various defense contracting procedures and standards. Furthermore, the approval process for new aircraft designs and technologies is lengthy, involving several rounds of testing, certification, and scrutiny, which can impede the pace at which new innovations are brought to market. These regulatory challenges not only affect the efficiency of the market but also raise the costs of bringing new products to fruition.

Opportunities

Emerging Demand for UAVs and Autonomous Aircraft

The UK Military Aviation Market is witnessing a rising demand for unmanned aerial vehicles (UAVs) and autonomous aircraft systems. UAVs are increasingly seen as a valuable tool for reconnaissance, surveillance, and combat operations. Their ability to operate without risking human lives makes them an attractive investment for military forces looking to enhance their operational capabilities in both peacetime and combat scenarios. The UK has already invested in UAV technologies and is expected to continue expanding its use in military operations. The development of autonomous aircraft systems, which are capable of operating independently, is another area where significant growth opportunities exist. These systems are poised to revolutionize aerial defense strategies and provide the UK military with more versatile, efficient, and cost-effective solutions.

Integration of AI and Advanced Data Analytics in Aircraft Systems

The integration of artificial intelligence (AI) and advanced data analytics into military aviation systems presents another key opportunity for market growth. AI is being used to enhance aircraft performance, optimize maintenance schedules, and improve overall system reliability. Advanced data analytics enable the military to assess vast amounts of data collected from various aircraft systems, providing real-time insights into operational performance and identifying areas for improvement. AI-powered systems can also play a role in improving pilot training, autonomous operations, and decision-making in combat environments. As the UK military continues to embrace AI technologies, there will be increased demand for systems that incorporate these advancements, creating opportunities for companies specializing in AI-driven aviation technologies.

Future Outlook

The UK Military Aviation Market is expected to continue its growth trajectory over the next five years, with an emphasis on modernization, technological innovation, and bolstered defense capabilities. Key trends include the increased adoption of UAVs, autonomous systems, and AI-powered technologies. Furthermore, the UK government’s commitment to defense spending, coupled with increasing global security concerns, will drive continued demand for military aviation solutions. Technological developments, including next-generation fighter jets and advanced surveillance systems, will play a critical role in shaping the market’s future growth.

Major Players

- BAE Systems

- Leonardo

- Rolls-Royce

- Airbus

- Lockheed Martin

- Northrop Grumman

- General Dynamics

- Thales Group

- Saab AB

- Boeing

- Raytheon Technologies

- MBDA

- L3 Technologies

- Elbit Systems

- Harris Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense contractors

- Aerospace manufacturers

- Military forces

- Security agencies

- Aerospace technology firms

- Aviation supply chain companies

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key market variables that impact the UK military aviation industry, including government spending, technological advancements, and geopolitical influences.

Step 2: Market Analysis and Construction

In this step, detailed market analysis is conducted to create a market model, integrating data from both primary and secondary sources, such as government reports, defense contracts, and industry insights.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are conducted with industry professionals and stakeholders to

validate assumptions, ensure accuracy, and refine the market model based on real-time insights.

Step 4: Research Synthesis and Final Output

The final output synthesizes all research findings, producing a comprehensive market report that highlights key insights, trends, and actionable strategies for industry players.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising National Security Concerns

Increased Defense Budget Allocations

Technological Advancements in Aircraft Design - Market Challenges

High Development and Maintenance Costs

Regulatory and Certification Barriers

Cybersecurity Vulnerabilities - Market Opportunities

Emerging Demand for Autonomous Aircraft Systems

Private Sector Partnerships for Defense Solutions

Growth in Space-Based Military Platforms - Trends

Integration of Artificial Intelligence in Aviation Systems

Increased Investment in UAV Technologies

Rise in Hybrid and Electric Military Aircraft - Government regulations

Defense Export Controls

Aviation Safety Standards

Environmental Regulations for Aircraft Emissions - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Airborne Early Warning Systems

Combat Aircraft

Surveillance Systems

Helicopter Systems

UAVs - By Platform Type (In Value%)

Land Platforms

Airborne Platforms

Naval Platforms

Space Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End-user Segment, Fitment Type, Technology Integration, Market Geography, Regulatory Compliance, Product Lifecycle, Pricing Strategy)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BAE Systems

Leonardo

Rolls-Royce

Thales Group

Airbus

Lockheed Martin

Northrop Grumman

General Dynamics

Rheinmetall AG

Saab Group

L3 Technologies

Raytheon Technologies

Harris Corporation

Boeing

Sikorsky Aircraft

- Military Forces’ Increasing Demand for Digital Systems

- Government Agencies’ Role in Regulating and Procuring Defense Systems

- Defense Contractors’ Shift Towards Innovation and Integration

- Private Sector’s Growing Interest in Cybersecurity Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now