Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK Online Insurance Market forms part of the broader UK insurance industry that generated approximately USD ~ billion in gross written premiums, according to data published by the Association of British Insurers. A significant proportion of personal lines premiums are distributed through digital channels, driven by high internet penetration, widespread use of price comparison websites, strong fintech adoption, and consumer preference for direct-to-consumer policy purchase and claims management platforms.

London remains the primary insurance hub due to its concentration of major insurers, reinsurers, and Lloyd’s market participants, while Manchester and Birmingham support regional underwriting and digital operations. The UK benefits from advanced financial infrastructure, strong regulatory oversight by the Financial Conduct Authority, and mature comparison website ecosystems. Nationwide digital adoption and embedded insurance partnerships further strengthen online distribution and automated underwriting expansion.

Market Segmentation

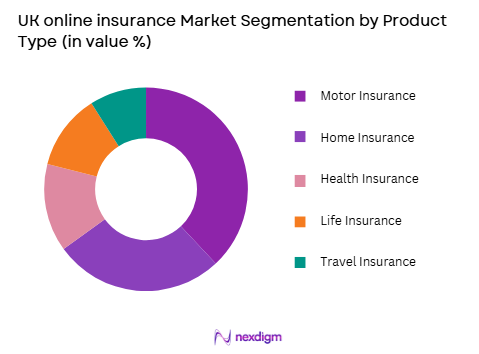

By Product Type

UK Online Insurance Market market is segmented by product type into Motor Insurance, Home Insurance, Health Insurance, Life Insurance, and Travel Insurance. Recently, Motor Insurance has a dominant market share due to factors such as mandatory coverage requirements, high vehicle ownership density, extensive use of price comparison websites, strong direct-to-consumer advertising, and streamlined digital underwriting processes supported by telematics integration and automated claims platforms.

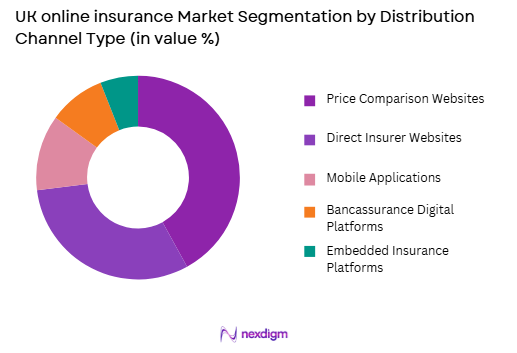

By Distribution Channel

UK Online Insurance Market market is segmented by distribution type into Price Comparison Websites, Direct Insurer Websites, Mobile Applications, Bancassurance Digital Platforms, and Embedded Insurance Platforms. Recently, Price Comparison Websites have a dominant market share due to factors such as consumer demand for transparent pricing, competitive multi-insurer quotes, simplified purchasing interfaces, strong brand recognition of aggregator platforms, and integrated payment gateways that streamline policy issuance and renewal processes.

Competitive Landscape

The UK Online Insurance Market is characterized by strong competition between established insurers expanding digital capabilities and insurtech firms operating fully online. Market consolidation has increased through acquisitions of digital startups by legacy carriers. Leading firms leverage brand trust, underwriting capacity, telematics integration, and advanced analytics to strengthen online distribution. Aggregator platforms also exert significant influence by directing high volumes of traffic and shaping pricing competition.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Digital Premium Share |

| Aviva | 2000 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Direct Line Group | 1985 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Admiral Group | 1993 | Cardiff, UK | ~ | ~ | ~ | ~ | ~ |

| AXA UK | 1985 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Hastings Direct | 1997 | East Sussex, UK | ~ | ~ | ~ | ~ | ~ |

UK Online Insurance Market Analysis

Growth Drivers

High Digital Penetration and Consumer Reliance on Price Comparison Ecosystems

The widespread adoption of broadband and smartphone usage across the United Kingdom has significantly accelerated digital insurance purchasing behavior, particularly within personal lines segments such as motor and home insurance. Consumers increasingly rely on price comparison websites to access multiple insurer quotes in a single interface, driving transparency and competitive pricing. This ecosystem reduces distribution friction and shortens policy decision cycles. Insurers benefit from targeted online marketing campaigns and data analytics that refine customer acquisition strategies. Automated underwriting systems allow instant quote generation and policy issuance. Telematics-based pricing models enhance risk-based segmentation in motor insurance. Integrated digital claims platforms improve settlement efficiency and customer satisfaction. Regulatory frameworks encourage fair pricing practices and consumer transparency. Recurring renewal cycles reinforce digital platform engagement. These structural digital adoption trends provide a sustained growth foundation for online insurance distribution.

Integration of Advanced Analytics, Telematics, and Automated Claims Processing

The UK insurance industry has increasingly deployed advanced analytics and artificial intelligence to optimize underwriting accuracy and operational efficiency across online channels. Telematics devices and mobile tracking applications enable usage-based motor insurance models aligned with real-time driving behavior. Predictive modeling tools enhance fraud detection and loss forecasting capabilities. Automated claims platforms reduce processing time and administrative overhead. Data-driven personalization improves cross-selling and customer retention. Cloud-based infrastructure supports scalable policy management systems. Digital identity verification accelerates onboarding and compliance procedures. Insurtech collaborations accelerate product innovation and modular policy design. Real-time data integration enhances actuarial precision and premium competitiveness. These technological advancements collectively strengthen efficiency, reduce cost ratios, and expand digital premium volumes within the UK Online Insurance Market.

Market Challenges

Regulatory Pricing Reforms and Margin Compression

The UK Online Insurance Market faces structural pressure from regulatory reforms implemented by the Financial Conduct Authority that restrict differential pricing between new and renewing customers. These reforms reduce insurers’ ability to offer discounted introductory premiums while increasing renewal pricing, compressing margins in competitive segments. Price comparison websites intensify downward pricing pressure by promoting lowest-cost options. Customer loyalty remains low in commoditized motor insurance categories. Rising claims costs linked to inflation and vehicle repair expenses impact underwriting profitability. Insurers must recalibrate pricing algorithms to align with regulatory compliance. Operational costs increase as firms enhance transparency reporting and customer communication. Competitive advertising expenditure further narrows profit margins. Consolidation among insurers may intensify under sustained pricing pressure. These regulatory and competitive factors create ongoing profitability challenges.

Cybersecurity Risks and Data Protection Compliance Complexity

The digital nature of the UK Online Insurance Market increases exposure to cyber threats targeting sensitive personal and financial data. Insurers must maintain robust encryption, authentication, and intrusion detection systems to safeguard policyholder information. Compliance with UK data protection regulations requires strict data governance practices. Breach incidents can result in significant reputational damage and regulatory penalties. Integration of third-party aggregator platforms increases interconnected system vulnerabilities. Continuous technological upgrades are required to mitigate emerging cyber risks. Fraudulent online claims require advanced monitoring algorithms. Customer trust is directly influenced by perceived data security standards. Cyber insurance demand may rise as digital dependency expands. These cybersecurity challenges necessitate sustained capital investment and operational vigilance.

Opportunities

Expansion of Embedded Insurance within Digital Retail and Mobility Platforms

The integration of insurance products into digital purchasing journeys across e-commerce, travel booking, and mobility platforms presents a significant growth opportunity within the UK Online Insurance Market. Embedded insurance allows consumers to purchase coverage seamlessly at the point of transaction. Strategic partnerships with online retailers and ride-sharing services broaden distribution channels. API-based underwriting enables real-time premium calculation during checkout processes. Micro-duration policies provide flexible coverage tailored to specific events. Reduced acquisition costs enhance profitability. Personalized policy recommendations increase conversion rates. Subscription-style insurance bundles align with recurring digital services. Automated claims processing within partner ecosystems improves customer experience. This embedded distribution model expands reach beyond traditional insurance channels.

Growth of Usage-Based and On-Demand Insurance Models

Increasing consumer demand for flexible and customized coverage structures supports expansion of usage-based insurance offerings across the UK market. Pay-as-you-drive motor policies leverage telematics data to align premiums with driving behavior. On-demand travel and gadget insurance can be activated through mobile applications for defined periods. Gig economy workers benefit from flexible short-term coverage options. Real-time policy activation enhances customer control and transparency. Data analytics enable dynamic risk pricing adjustments. Digital payment integration simplifies premium collection. Younger demographics demonstrate strong adoption of app-based insurance management. Modular product structures increase cross-selling potential. This evolution toward flexible, technology-enabled coverage models supports long-term digital growth within the UK Online Insurance Market.

Future Outlook

Over the next five years, the UK Online Insurance Market is expected to expand through continued digital adoption, embedded insurance integration, and enhanced analytics-driven underwriting systems. Regulatory clarity on pricing practices will shape competitive strategies. Telematics and automated claims technologies are likely to gain further prominence. Growth in flexible and usage-based insurance models will continue to redefine distribution dynamics and customer engagement across personal lines segments.

Major Players

- Aviva

- Direct Line Group

- Admiral Group

- AXA UK

- Hastings Direct

- LV=

- Zurich UK

- Allianz UK

- RSA Insurance

- Bupa UK

- Vitality Health

- esure

- Churchill Insurance

- Ageas UK

- Hiscox

Key Target Audience

- Insurance carriers

- Insurtech platforms

- Digital insurance brokers

- Reinsurance companies

- Institutional investors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aggregator platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables including gross written premiums, digital distribution channels, product segmentation, and regulatory frameworks were identified through Association of British Insurers publications and insurer financial disclosures. Technology adoption metrics and consumer behavior trends were integrated into the analysis.

Step 2: Market Analysis and Construction

Market construction was based on official premium data and digital channel penetration insights. Segmentation was developed by mapping product categories and online distribution models within the UK insurance ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultations with underwriting professionals, actuarial analysts, and regulatory experts. Cross-verification ensured alignment with public financial statements and supervisory guidance.

Step 4: Research Synthesis and Final Output

Quantitative findings and qualitative insights were consolidated into a structured analytical framework. Final outputs were reviewed for factual consistency, regulatory accuracy, and logical coherence prior to publication.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

High Internet and Smartphone Penetration

Rising Demand for Instant Quotes and Digital Claims Processing

Growth of Insurtech Innovation and Venture Funding - Market Challenges

Strict Regulatory Compliance under FCA Guidelines

Data Privacy and Cybersecurity Risks

Intense Price Competition on Comparison Platforms - Market Opportunities

Expansion of Usage Based and Telematics Insurance

AI Driven Underwriting and Fraud Detection

Partnerships with Fintech and E Commerce Platforms - Trends

Increased Adoption of Telematics and Pay As You Drive Models

Growth of Fully Digital First Insurance Providers - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Motor Insurance

Online Home Insurance

Online Life Insurance

Online Travel Insurance

Cyber and Specialty Digital Insurance - By Platform Type (In Value%)

Direct Insurer Websites

Mobile Insurance Applications

Price Comparison Websites

Broker Led Digital Platforms

Embedded Insurance Platforms - By Fitment Type (In Value%)

Direct to Consumer Online Policies

Broker Assisted Online Sales

API Integrated Distribution

White Label Digital Insurance Solutions - By End User Segment (In Value%)

Individual Consumers

Small and Medium Enterprises

Large Corporate Clients

Gig Economy and Self Employed Workers

- Market Share Analysis

- Cross Comparison Parameters (Premium Pricing Structure, Claims Settlement Efficiency, Digital Onboarding Process, Coverage Customization Options, Data Security Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Aviva plc

Legal and General Group

Prudential plc

Admiral Group

Direct Line Group

AXA UK

Zurich Insurance Group UK

LV General Insurance

Hastings Group

Saga plc

Ageas UK

esure Group

Vitality Life

Marshmallow Insurance

Zego

- Rising Preference for Self Service Policy Management

- Demand for Transparent Pricing and Easy Policy Switching

- SME Adoption of Digital Commercial Insurance

- Growing Interest in Flexible Coverage among Freelancers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now