Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Solar EPC Market is expected to see significant growth in the upcoming years, with a market size projected to be valued at USD ~ billion. This growth is driven by the rising demand for renewable energy solutions, the UK’s commitment to net-zero emissions, and the expansion of solar energy capacity across various sectors. Increased government incentives and declining costs of solar technology are also boosting market development. The market is further propelled by an increase in private sector investments and a growing adoption of solar energy systems.

Dominant cities and regions contributing to the market include London, Birmingham, and Manchester, driven by their high population densities, economic activities, and government-backed renewable energy initiatives. These areas are home to a variety of industrial and residential projects, making them prime locations for solar energy adoption. The dominance of these cities is supported by both local government policies and the presence of established solar energy infrastructure, promoting widespread implementation of solar EPC services.

Market Segmentation

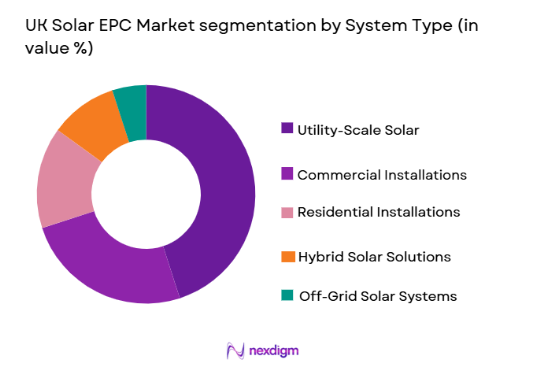

By System Type

The UK Solar EPC market is segmented by system type into utility-scale solar, commercial solar installations, residential solar installations, hybrid solar solutions, and off-grid solar systems. Recently, utility-scale solar has dominated the market share due to its higher energy production potential and the government’s focus on large-scale renewable energy projects. The expansion of solar farms and the availability of funding from both government and private sectors are factors contributing to the dominance of this sub-segment. Utility-scale systems offer an efficient solution to the UK’s energy demands, providing cleaner power and contributing to renewable energy targets. These systems also benefit from advancements in solar panel technology and energy storage systems, enabling more efficient energy management and grid integration.

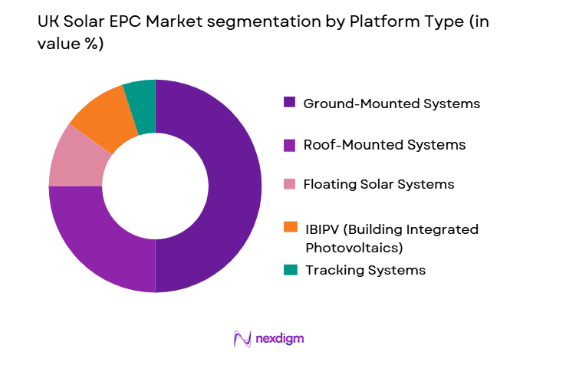

By Platform Type

The UK Solar EPC market is segmented by platform type into ground-mounted systems, roof-mounted systems, floating solar systems, BIPV (Building Integrated Photovoltaics), and tracking systems. Recently, ground-mounted systems have dominated the market share due to their scalability and high efficiency in generating energy. These systems are easier to install on large plots of land, and they benefit from economies of scale. The government’s support for utility-scale projects has led to a surge in ground-mounted installations, which have become essential for meeting renewable energy targets. Additionally, their lower maintenance costs and ability to be installed in remote locations make them a preferred option for large-scale solar power generation.

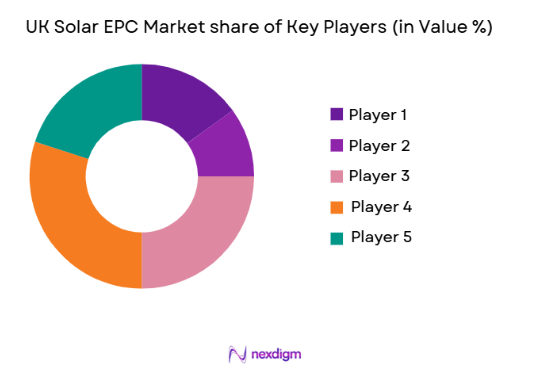

Competitive Landscape

The UK Solar EPC market is highly competitive, with several key players dominating the landscape. The market is characterized by strong consolidation, with both large multinational companies and smaller regional players vying for market share. The influence of major players, such as First Solar and SunPower, is evident, as they lead in technology innovation and large-scale project execution. Additionally, regional firms that specialize in residential and commercial installations are also gaining ground due to their ability to adapt quickly to local demands. The UK government’s commitment to renewable energy further consolidates the position of leading players, while smaller firms focus on niche markets and service diversification.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| First Solar | 1999 | USA | ~ | ~ | ~ | ~ | ~ |

| SunPower Corporation | 1985 | USA | ~ | ~ | ~ | ~ | ~ |

| Trina Solar | 1997 | China | ~ | ~ | ~ | ~ | ~ |

| JinkoSolar | 2006 | China | ~ | ~ | ~ | ~ | ~ |

| Canadian Solar | 2001 | Canada | ~ | ~ | ~ | ~ | ~ |

UK Solar EPC Market Analysis

Growth Drivers

Government Incentives and Policies:

Government incentives and policies play a major role in driving the growth of the UK Solar EPC market. The UK’s commitment to reducing carbon emissions by 2030 has spurred investments in renewable energy technologies, particularly solar power. Various incentives such as tax rebates, feed-in tariffs, and renewable energy grants have made it financially viable for businesses and homeowners to invest in solar power. Additionally, government-backed programs aimed at enhancing the infrastructure for renewable energy solutions have further boosted market growth. The UK’s ambitious energy goals are set to continue driving demand for solar EPC services, which will help increase adoption across residential, commercial, and utility sectors. Government support in the form of subsidies for large-scale solar projects is ensuring that solar technology becomes more affordable for end-users, making it an attractive investment option. Furthermore, the UK’s commitment to meeting its Net Zero targets by 2050 provides long-term stability for the market.

Technological Advancements in Solar Energy:

The continuous advancements in solar panel technology are another key growth driver in the UK Solar EPC market. Over the past few years, there has been a significant reduction in the cost of solar panels due to improvements in manufacturing processes and materials. New innovations, such as bifacial solar panels and high-efficiency inverters, have made solar systems more efficient, with a higher return on investment. These technological breakthroughs have made solar energy more attractive to a broader range of consumers, including residential, commercial, and industrial sectors. Furthermore, developments in energy storage solutions have significantly enhanced the reliability of solar power, especially in off-grid and hybrid systems. As these technologies become more mainstream, they are expected to further reduce the barriers to adoption and drive market growth in the long term.

Market Challenges

High Initial Capital Investment:

A major challenge hindering the growth of the UK Solar EPC market is the high initial capital investment required for the installation of solar systems. Although the cost of solar panels has decreased over time, the overall expense of installing solar systems, particularly for utility-scale projects, remains significant. Many businesses and residential customers still face financial barriers, especially in the face of economic uncertainty. While financing options such as loans and leasing are available, these still pose a challenge for some end-users. In addition, the installation of large-scale solar farms often requires considerable land acquisition costs, which further complicates the market dynamics. High upfront costs also deter some businesses from transitioning to renewable energy, which impacts the market’s growth potential. The reliance on government subsidies has also made the market sensitive to any changes in policy, which could potentially disrupt growth.

Regulatory Barriers and Grid Integration:

Regulatory barriers and grid integration issues pose significant challenges to the UK Solar EPC market. While the UK government has made strides in supporting renewable energy, complex regulations regarding grid connection and the approval of solar projects can delay installations. The integration of solar energy into the national grid requires sophisticated infrastructure, and grid stability remains a concern when incorporating intermittent renewable energy sources like solar. Despite advancements in smart grid technologies, grid integration remains a challenge that could potentially limit the scalability of solar energy in the country. Furthermore, the lengthy permitting processes and complex environmental assessments required for large-scale projects can result in delays, driving up costs and reducing the market’s efficiency.

Opportunities

Expansion of Solar Energy in Rural Areas:

An important opportunity for the UK Solar EPC market lies in the expansion of solar energy solutions in rural areas. Many rural regions in the UK are currently underserved in terms of renewable energy infrastructure, presenting a growing demand for solar installations. These areas are ideal for large-scale solar farms, as they often have vast, unutilized land available for development. With the increasing push for energy independence and sustainability, rural areas are becoming prime locations for the installation of solar energy systems. Furthermore, government incentives to support renewable energy adoption in these regions have led to increased interest from both private and public stakeholders. Rural expansion also aligns with the UK’s efforts to decentralize energy production and reduce the strain on urban grids, making it an attractive market opportunity.

Solar + Storage Integration for Commercial Sectors:

The integration of solar energy with energy storage solutions is creating significant opportunities within the commercial sector. Businesses are increasingly seeking ways to reduce their energy bills and reliance on the grid by adopting solar systems coupled with energy storage. This integration allows companies to store excess energy produced during the day and use it during peak demand periods, further enhancing the economic viability of solar energy. As energy storage technologies improve and costs continue to decline, more commercial entities are expected to invest in solar-plus-storage systems. This trend is supported by government policies that promote energy independence and renewable energy integration. The growing demand for energy-efficient solutions in commercial buildings is likely to drive the market forward, especially in sectors such as retail, hospitality, and manufacturing.

Future Outlook

The UK Solar EPC market is expected to continue growing in the next five years, driven by advancements in solar technology, government policies, and an increasing demand for renewable energy. The market is likely to witness significant growth in both residential and commercial solar installations, as well as the development of large-scale solar farms. Technological advancements in solar panels and storage solutions will improve the efficiency and cost-effectiveness of solar energy, making it more accessible to a broader range of consumers. Furthermore, regulatory support for renewable energy is expected to remain strong, with the UK government setting ambitious energy targets. The continued drive for decarbonization and energy independence will contribute to the sustained growth of the solar EPC market, making it a key player in the country’s energy transition.

Major Players

- First Solar

- SunPower Corporation

- Trina Solar

- JinkoSolar

- Canadian Solar

- LONGi Green Energy

- Sharp Corporation

- Belectric

- SMA Solar Technology

- Risen Energy

- Q CELLS

- Enel Green Power

- Hanwha Q CELLS

- Yingli Solar

- REC Group

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy producers

- Private utility companies

- Industrial developers

- Corporate sustainability officers

- Real estate developers

- Energy technology innovators

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the core variables influencing the solar EPC market, including technological advancements, government policies, and economic factors.

Step 2: Market Analysis and Construction

In this phase, the market structure, size, and growth factors are thoroughly analyzed using both qualitative and quantitative data sources to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

The next step involves validating the hypotheses generated in the previous phase by consulting with industry experts, stakeholders, and market leaders to ensure accuracy and reliability.

Step 4: Research Synthesis and Final Output

The final step combines all gathered data, insights, and expert opinions to produce the final report, ensuring it accurately reflects the market’s current state and future trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Support for Renewable Energy

Advancements in Solar Panel Efficiency

Increasing Energy Demand and Sustainability Initiatives

Declining Cost of Solar Technologies

Rising Corporate Social Responsibility (CSR) Adoption - Market Challenges

High Initial Capital Investment

Regulatory Hurdles and Certification Processes

Grid Integration and Intermittency Issues

Land Availability for Large-Scale Projects

Supply Chain Disruptions - Market Opportunities

Integration of Storage Solutions with Solar Systems

Rising Adoption of Solar for Residential Applications

Expansion of Solar Projects in Rural Areas - Trends

Growth in BIPV (Building Integrated Photovoltaics)

Advances in Solar Tracking Technologies

Increased Focus on Solar Energy Storage

Rise of Solar Microgrids

Shift Towards Hybrid Solar Solutions - Government Regulations & Defense Policy

Renewable Energy Targets and Incentives

Tax Breaks and Subsidies for Solar Projects

Regulatory Framework for Solar Grid Integration - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility-Scale Solar Projects

Commercial Solar Installations

Residential Solar Installations

Hybrid Solar Solutions

Off-Grid Solar Systems - By Platform Type (In Value%)

Ground-Mounted Systems

Roof-Mounted Systems

Floating Solar Systems

BIPV (Building Integrated Photovoltaics)

Tracking Systems - By Fitment Type (In Value%)

On-Grid Solutions

Off-Grid Solutions

Hybrid Solutions

Flexible Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Residential Sector

Commercial Sector

Industrial Sector

Utility Sector

Government and Public Sector - By Procurement Channel (In Value%)

Direct Procurement

Public Tenders

Private Sector Procurement

Third-Party Distributors

Online Bidding Platforms - By Material / Technology (In Value%)

Monocrystalline Panels

Polycrystalline Panels

Thin Film Panels

Solar Inverters

Storage Solutions

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material/Technology, Market Value, Installed Units, Average System Price, System Complexity Tier)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

First Solar

SMA Solar Technology

Belectric

SolarEdge Technologies

SunPower Corporation

Trina Solar

JinkoSolar

LONGi Green Energy

Canadian Solar

Risen Energy

GCL-Poly Energy

Sharp Corporation

Enel Green Power

First Solar

Sungrow Power Supply

- Residential Sector’s Shift Towards Sustainability

- Increasing Corporate Adoption of Solar Solutions

- Government’s Role in Expanding Solar Projects

- Utility Sector’s Investment in Solar Energy

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now