Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK warehousing market is valued at approximately USD ~ billion, according to combined analysis from the UK Office for National Statistics and logistics infrastructure reports published by Statista and Savills. The market is driven by expanding e-commerce fulfillment networks, increasing outsourcing of logistics operations to third party providers, and growing demand for automated distribution infrastructure. Retail supply chains require large scale storage and distribution facilities to support national delivery networks, while manufacturing industries depend on strategically located warehouses for inventory management and just in time production supply chains.

Major logistics and warehousing activity are concentrated around cities such as London, Birmingham, Manchester, and Leeds due to strong transport connectivity and proximity to major consumer markets. These metropolitan logistics corridors benefit from advanced motorway networks, international airports, and major seaports that support the nationwide freight movement. Industrial clusters and distribution parks across the Midlands and Southeast England provide efficient access to national road networks, enabling rapid distribution to urban population centers while supporting the operational requirements of retailers, manufacturers, and third-party logistics providers.

Market Segmentation

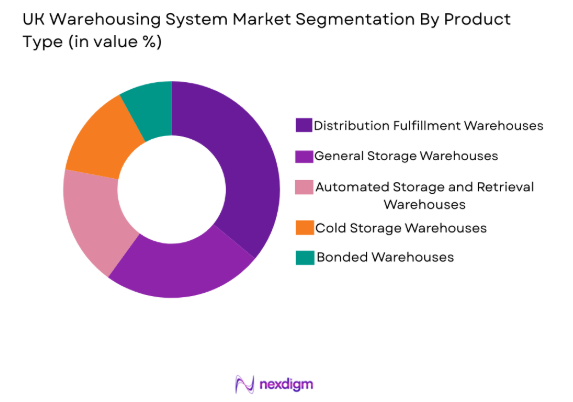

By Product Type

The UK Warehousing market is segmented by product type into general storage warehouses, automated storage and retrieval warehouses, cold storage warehouses, bonded warehouses, and distribution of fulfillment warehouses. Recently, distribution fulfillment warehouses had a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rapid expansion of online retail has increased demand for large fulfillment centers capable of processing thousands of orders daily. Retail companies require strategically located distribution hubs close to major consumer regions to enable rapid order processing and last mile delivery efficiency. Large scale e commerce companies also invest in technologically advanced fulfillment facilities equipped with robotics and warehouse management software, strengthening the dominance of distribution fulfillment infrastructure across national logistics networks.

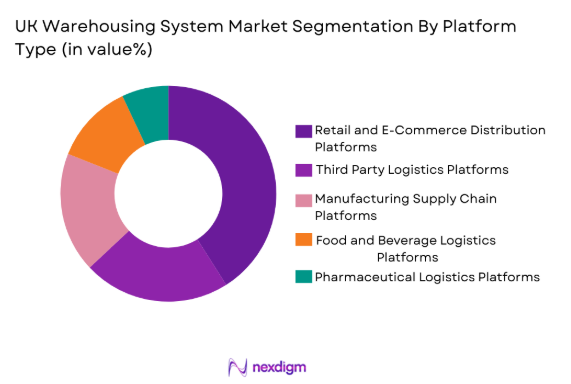

By Platform Type

UK Warehousing market is segmented by platform type into retail and e commerce distribution platforms, manufacturing supply chain platforms, third party logistics platforms, pharmaceutical logistics platforms, and food and beverage logistics platforms. Recently, retail and e commerce distribution platforms has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Online retail platforms process extremely high daily order volumes requiring advanced fulfillment centers and large distribution warehouses located near urban markets. Retailers invest heavily in logistics automation, inventory management technologies, and high capacity distribution networks to maintain fast delivery services. The growth of omnichannel retail models further strengthens the importance of integrated warehousing infrastructure supporting both online and physical retail supply chains.

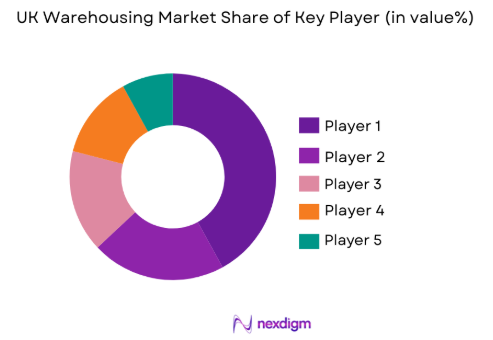

Competitive Landscape

The UK warehousing market shows moderate consolidation with large logistics infrastructure developers and global third party logistics providers controlling significant portions of distribution capacity. International logistics companies compete alongside domestic warehouse operators to support retail supply chains, manufacturing logistics, and pharmaceutical distribution networks. Major players invest heavily in automated warehouse systems, digital inventory management technologies, and strategically located logistics parks near transportation corridors. Strong partnerships between retailers, manufacturers, and logistics providers shape competitive positioning within the national warehousing ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| Prologis | 1983 | San Francisco | ~ | ~ | ~ | ~ | ~ |

| Segro | 1920 | London | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| Wincanton | 1925 | Chippenham | ~ | ~ | ~ | ~ | ~ |

| GXO Logistics | 2021 | Connecticut | ~ | ~ | ~ | ~ | ~ |

UK Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce Fulfillment and Digital Retail Logistics Networks

Rapid expansion of digital retail platforms significantly strengthens demand for large scale warehousing infrastructure across the UK logistics ecosystem. Online marketplaces and retail websites process millions of daily transactions that require efficient inventory storage and order fulfillment operations across national distribution networks. Retailers therefore invest heavily in automated fulfillment centers and strategically located regional warehouses capable of managing high order volumes while maintaining fast delivery timelines. Advanced warehouse robotics, automated sorting equipment, and digital inventory tracking technologies enable logistics operators to improve productivity while reducing manual handling requirements. Large retailers increasingly rely on integrated warehouse management systems capable of coordinating inventory movement across multiple distribution facilities. Third party logistics providers expand fulfillment infrastructure to support smaller online retailers that outsource logistics operations to specialized service providers. Strong consumer demand for fast home delivery services further increases the need for efficient warehousing and distribution capacity. As online retail continues expanding across the national economy, large scale fulfillment warehouses remain critical logistics infrastructure supporting digital commerce growth and supply chain efficiency.

Adoption of Automated Warehouse Technologies and Robotics Systems

Automation technologies significantly strengthen operational efficiency across modern warehousing facilities throughout the UK logistics sector. Companies increasingly deploy automated storage and retrieval systems, robotic picking technologies, and intelligent warehouse management software capable of managing large inventory volumes with minimal human intervention. These technologies improve order processing speed, reduce operational errors, and enhance workplace safety by minimizing manual lifting and repetitive labor tasks. Logistics operators benefit from improved inventory accuracy and optimized storage density through advanced digital warehouse management platforms integrated with robotics equipment. Automation systems also support rapid order fulfillment for retailers requiring same day or next day delivery capabilities. Large distribution centers integrate artificial intelligence driven demand forecasting systems that allocate storage space and processing capacity according to changing shipment patterns. Warehouse automation allows logistics companies to manage increasing parcel volumes while maintaining consistent operational performance. As labor shortages and operational costs continue influencing logistics operations, investment in warehouse automation technologies continues expanding across the UK logistics infrastructure landscape.

Market Challenges

High Industrial Land Costs and Limited Logistics Space Availability

Industrial land scarcity and rapidly increasing property costs present significant challenges for warehousing infrastructure development across the UK logistics sector. Major metropolitan regions experience strong competition for industrial land due to rising demand from logistics companies, manufacturing industries, and commercial property developers seeking strategically located facilities near consumer markets. Urban areas such as London and the Southeast face particularly limited land availability, which restricts development of large distribution warehouses required for national supply chain operations. Developers therefore encounter complex land acquisition processes and higher construction costs when planning new logistics facilities. Increasing property values also raise warehouse rental costs for logistics operators and retailers requiring large scale distribution space. These cost pressures can limit expansion plans for logistics companies attempting to increase storage capacity to support growing e commerce demand. Infrastructure constraints further complicate development of large logistics parks requiring access to highways, rail networks, and freight corridors. As a result, industrial land shortages remain a major structural challenge affecting long term expansion of the warehousing sector.

Labor Shortages and Workforce Retention Challenges in Logistics Operations

Workforce availability remains a critical operational challenge affecting warehouse productivity and logistics service delivery across the UK supply chain sector. Warehousing operations require a large workforce responsible for inventory handling, packaging, equipment operation, and logistics coordination tasks within distribution facilities. However logistics companies increasingly face difficulty recruiting and retaining skilled workers capable of operating advanced warehouse technologies and maintaining efficient operational workflows. Demographic shifts, competition from other industries, and physically demanding working conditions contribute to labor shortages within the logistics workforce. Companies often experience higher employee turnover rates that increase recruitment and training costs for warehouse operators. Workforce shortages can also reduce operational efficiency within large distribution centers responsible for processing thousands of daily shipments. Logistics operators therefore invest in automation technologies and employee training programs designed to reduce reliance on manual labor while improving worker productivity. Despite technological advancements, maintaining a stable logistics workforce remains a continuing operational challenge affecting warehouse operations nationwide.

Opportunities

Development of Urban Micro Fulfillment Centers for Last Mile Logistics

Increasing consumer demand for rapid delivery services creates significant opportunities for development of urban micro fulfillment centers located close to metropolitan population clusters. These smaller distribution facilities enable retailers and logistics providers to store high demand inventory near customers, allowing faster order processing and delivery across dense urban environments. Micro fulfillment centers support same day and next day delivery services that modern online consumers increasingly expect from retailers and logistics companies. Retailers invest in automated micro warehouses equipped with robotics systems capable of processing online grocery orders and consumer goods shipments within compact facilities. Urban logistics infrastructure therefore becomes an essential component supporting efficient last mile distribution networks across major cities. Real estate developers and logistics companies collaborate to convert underutilized commercial spaces into technologically advanced micro fulfillment facilities supporting rapid order fulfillment operations. Growing consumer expectations for faster delivery services continue strengthening demand for distributed urban logistics infrastructure across the UK retail supply chain landscape.

Expansion of Sustainable and Energy Efficient Warehousing Infrastructure

Environmental sustainability initiatives create major opportunities for development of energy efficient warehousing facilities across the UK logistics sector. Logistics companies increasingly adopt green building standards and renewable energy technologies to reduce environmental impact while improving operational efficiency. Modern warehouse facilities integrate solar energy systems, advanced insulation technologies, and energy efficient lighting infrastructure that reduce long term operating costs while supporting corporate sustainability objectives. Government environmental policies encouraging carbon reduction across industrial sectors also support development of sustainable logistics infrastructure. Companies investing in environmentally responsible warehouses strengthen their competitive positioning within supply chains increasingly focused on sustainability performance. Logistics operators also implement electric vehicle charging infrastructure within warehouse facilities to support electrified delivery fleets used for last mile transportation. Sustainable warehouse development therefore represents a major investment opportunity for logistics developers, retailers, and industrial property investors seeking environmentally responsible logistics infrastructure supporting future supply chain operations.

Future Outlook

The UK warehousing market is expected to experience steady expansion driven by continued growth in e commerce logistics, supply chain outsourcing, and industrial distribution infrastructure development. Increasing investment in warehouse automation technologies and robotics systems will transform operational efficiency across large distribution centers. Government infrastructure initiatives supporting logistics connectivity and industrial development are likely to strengthen national supply chain capacity. Demand from retail, manufacturing, and pharmaceutical industries will continue driving investment in strategically located warehousing facilities.

Major Players

- Prologis

- Segro

- DHL Supply Chain

- GXO Logistics

- Wincanton

- Clipper Logistics

- DB Schenker

- Kuehne + Nagel

- CEVA Logistics

- XPO Logistics

- Lineage Logistics

- Maersk Contract Logistics

- Great Bear Distribution

- Yusen Logistics

- Eddie Stobart Logistics

Key Target Audience

- Retail and e commerce companies

- Third partylogistics providers

- Manufacturing and industrial companies

- Food and beverage supply chain operators

- Pharmaceutical distribution companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Industry data related to warehousing infrastructure, logistics capacity, and distribution networks is identified through multiple public and private data sources. Key performance indicators such as warehouse capacity, logistics demand drivers, and infrastructure investment trends are selected for further evaluation.

Step 2: Market Analysis and Construction

The market structure is constructed using macroeconomic indicators, logistics infrastructure development patterns, and industrial real estate data. Supply chain activity across retail, manufacturing, and logistics sectors is analyzed to determine demand for warehousing infrastructure.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists, logistics professionals, and infrastructure analysts validate research assumptions through expert consultation. Insights from supply chain operators and logistics developers help refine market segmentation and infrastructure demand analysis.

Step 4: Research Synthesis and Final Output

All research inputs are integrated to construct a comprehensive analysis of the warehousing market. Quantitative and qualitative findings are synthesized to produce final insights covering infrastructure development, logistics demand drivers, and competitive landscape dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Expansion of E Commerce Fulfillment and Online Retail Logistics

Increasing Supply Chain Outsourcing to Third Party Logistics Providers

Growth of Automated Warehousing Technologies and Robotics Integration - Market Challenges

High Land and Infrastructure Costs in Major Logistics Corridors

Labor Shortages and Increasing Warehouse Workforce Costs

Complex Regulatory and Zoning Approvals for Logistics Infrastructure - Market Opportunities

Development of Urban Micro Fulfillment Centers for Last Mile Delivery

Investment in Sustainable and Energy Efficient Warehousing Infrastructure

Expansion of Temperature Controlled Warehousing for Pharmaceutical Logistics - Trends

Adoption of Robotics and Warehouse Automation Technologies

Growth of Green Warehousing and Carbon Neutral Logistics Facilities - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

General Storage Warehouses

Automated Storage and Retrieval Warehouses

Cold Storage Warehouses

Bonded Warehouses

Distribution Fulfillment Warehouses - By Platform Type (In Value%)

Retail and E Commerce Distribution Platforms

Manufacturing Supply Chain Warehousing Platforms

Third Party Logistics Warehousing Platforms

Pharmaceutical and Healthcare Distribution Platforms

Food and Beverage Logistics Platforms - By Fitment Type (In Value%)

Dedicated Warehousing Facilities

Shared Multi Client Warehousing

Automated Smart Warehousing

On Demand Flexible Warehousing - By End User Segment (In Value%)

Retail and E Commerce Companies

Manufacturing and Industrial Enterprises

Logistics and Third Party Distribution Providers

- Market Share Analysis

- Cross Comparison Parameters (Warehouse Capacity, Automation Level, Storage Technology, End User Industries Served, Geographic Distribution Network, Temperature Control Capability, Value Added Logistics Services)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Prologis

Segro

DHL Supply Chain UK

Wincanton

Clipper Logistics

Eddie Stobart Logistics

Kuehne + Nagel UK

DB Schenker UK

Ceva Logistics UK

Yusen Logistics UK

Lineage Logistics UK

XPO Logistics UK

Maersk Contract Logistics UK

GXO Logistics UK

Great Bear Distribution

- Retail and E Commerce Companies Increasing Demand for Fulfillment Infrastructure

- Manufacturers Expanding Inventory Storage to Improve Supply Chain Resilience

- Third Party Logistics Providers Investing in Multi Client Distribution Facilities

- Pharmaceutical and Food Companies Requiring Specialized Temperature Controlled Warehousing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now