Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK wealth management market oversees approximately USD ~ trillion in assets under management, according to the Investment Association and the Office for National Statistics, expressed in USD equivalent terms. The market is driven by high household financial wealth, growing defined contribution pension assets, rising intergenerational transfers, and demand for discretionary portfolio management, tax-efficient investments, and holistic financial planning services across affluent and high-net-worth client segments.

London remains the dominant wealth management hub due to its concentration of private banks, global asset managers, and advanced financial infrastructure, while Edinburgh plays a central role in institutional asset administration and fund servicing. The United Kingdom benefits from a stable regulatory framework under the Financial Conduct Authority, deep capital markets, and international client inflows, reinforcing its position as a global cross-border wealth advisory center supported by sophisticated custody and digital investment platforms.

Market Segmentation

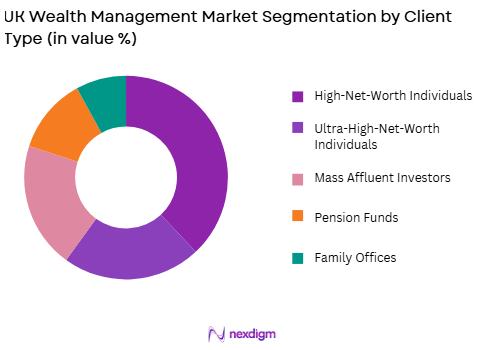

By Client Type

UK Wealth Management market is segmented by client type into High-Net-Worth Individuals, Ultra-High-Net-Worth Individuals, Mass Affluent Investors, Pension Funds, and Family Offices. Recently, High-Net-Worth Individuals has a dominant market share due to strong demand for discretionary portfolio management, estate planning, and tax advisory services, supported by growing private wealth accumulation and business ownership exits. This segment benefits from diversified investment portfolios, advisory-led engagement models, and structured succession planning requirements, making it the core revenue generator for private banks and integrated wealth platforms.

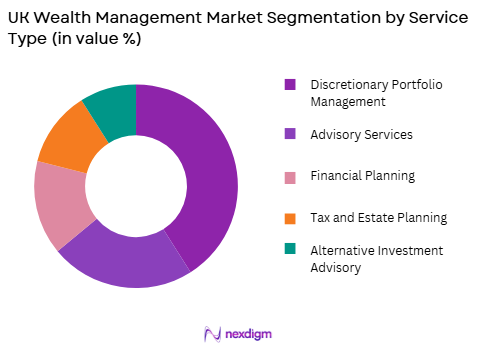

By Service Type

UK Wealth Management market is segmented by service type into Discretionary Portfolio Management, Advisory Services, Financial Planning, Tax and Estate Planning, and Alternative Investment Advisory. Recently, Discretionary Portfolio Management has a dominant market share due to rising client preference for professionally managed, actively monitored investment strategies amid market volatility and regulatory complexity. Institutional-grade asset allocation frameworks, model portfolio solutions, and access to global equities and private markets enhance its appeal, while regulatory suitability standards reinforce demand for structured discretionary mandates.

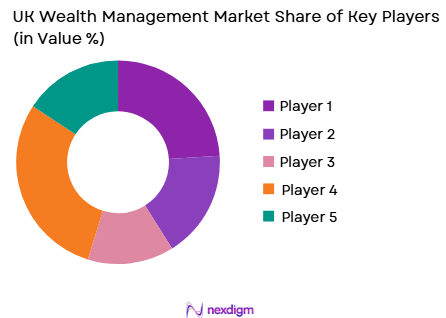

Competitive Landscape

The UK wealth management market is moderately consolidated, with a mix of global private banks, domestic asset managers, and independent wealth boutiques competing for affluent and high-net-worth clients. Large institutions benefit from scale, integrated banking capabilities, and international distribution networks, while specialized firms differentiate through tailored advisory, alternative investments, and digital engagement platforms. Strategic acquisitions and platform consolidation have strengthened market concentration, particularly among firms expanding discretionary mandates and retirement-focused wealth solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Assets Under Management (USD) |

| St. James’s Place | 1991 | Cirencester, UK | ~ | ~ | ~ | ~ | ~ |

| Schroders | 1804 | London, UK | ~ | ~ | ~ | ~ | ~ |

| HSBC Global Private Banking | 1865 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Barclays Private Bank | 1690 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Quilter | 2018 | London, UK | ~ | ~ | ~ | ~ | ~ |

UK Wealth Management Market Analysis

Growth Drivers

Intergenerational Wealth Transfer and Retirement Asset Expansion

The accelerating transfer of wealth between generations is reshaping the UK wealth management market by increasing the need for structured estate planning, tax optimization, and multi-generational advisory frameworks that preserve capital across families. A significant portion of private wealth is held by aging demographics, creating sustained advisory demand as beneficiaries seek professional guidance on portfolio restructuring, philanthropic structuring, and long-term income planning. Expanding defined contribution pension schemes have further increased managed assets, compelling individuals to seek discretionary and advisory services to optimize retirement income streams. The complexity of pension drawdown strategies and lifetime allowance considerations encourages deeper engagement with certified wealth planners. Growing longevity and healthcare costs reinforce the importance of sustainable withdrawal strategies supported by diversified portfolios. Wealth managers are developing integrated retirement propositions combining investment management, insurance solutions, and trust services. Rising entrepreneurial liquidity events from private equity exits and business sales contribute additional investable capital entering advisory pipelines. These cumulative structural factors support long-term asset inflows into professionally managed wealth solutions across the United Kingdom.

Digital Advisory Platforms and Personalized Investment Solutions

Technological advancement has transformed client acquisition, portfolio management, and engagement models across the UK wealth management ecosystem. Digital onboarding, automated suitability assessments, and hybrid advisory models reduce operational friction while maintaining regulatory compliance under Financial Conduct Authority standards. Advanced analytics and artificial intelligence tools enable portfolio customization aligned with risk tolerance, tax positioning, and liquidity preferences. Clients increasingly expect seamless digital dashboards providing real-time visibility into multi-asset portfolios, enhancing transparency and engagement. Integration of alternative assets such as private equity and infrastructure into model portfolios is facilitated by improved data processing capabilities. Open banking frameworks enable holistic financial profiling, supporting cross-product advisory strategies. Cost efficiencies generated through platform automation allow firms to serve broader mass affluent segments profitably. Competition from fintech-enabled robo-advisors has accelerated digital investment in established institutions. These digital enhancements collectively strengthen client retention and expand addressable markets within the UK wealth management sector.

Market Challenges

Regulatory Compliance Complexity and Cost Pressures

The UK wealth management market operates under stringent oversight by the Financial Conduct Authority, imposing rigorous suitability, transparency, and reporting requirements that elevate operational complexity. Regulatory frameworks governing MiFID II obligations, anti-money laundering protocols, and consumer duty standards require continuous system upgrades and compliance monitoring. These obligations increase fixed costs, particularly for mid-sized and independent wealth managers with limited economies of scale. Heightened disclosure rules affect fee structures, pushing firms toward transparent pricing models that may compress margins. Ongoing supervisory reviews demand robust documentation and governance controls, requiring specialized compliance talent. Cross-border advisory for international clients introduces additional jurisdictional reporting burdens. Technological adaptation to meet regulatory reporting standards involves significant capital investment in compliance infrastructure. Smaller advisory boutiques face consolidation pressure due to rising administrative expenses. This evolving regulatory environment constrains profitability while demanding higher service quality and accountability across the industry.

Market Volatility and Fee Compression Dynamics

Persistent market fluctuations across global equity and bond markets create performance uncertainty that directly affects client sentiment and asset-based revenue streams in the UK wealth management market. Revenue models heavily reliant on assets under management are sensitive to valuation declines, potentially reducing fee income during downturns. Low-cost passive investment vehicles and exchange-traded funds intensify competitive pressure on traditional active managers. Clients increasingly scrutinize fee structures, comparing discretionary mandates against lower-cost digital alternatives. Margin compression challenges firms to differentiate through advisory depth, alternative asset access, and holistic financial planning services. Economic uncertainty influences investor risk appetite, affecting allocation to higher-yield or private market instruments. Sustained inflationary pressures may alter asset allocation strategies and income expectations. Competition from international private banks and digital wealth platforms increases pricing transparency. These factors collectively challenge revenue stability and require strategic cost management and value-driven client engagement.

Opportunities

Expansion of Sustainable and ESG-Oriented Investment Mandates

Growing investor interest in environmental, social, and governance considerations presents a structural opportunity for UK wealth management firms to design differentiated portfolio solutions aligned with sustainability objectives. Institutional and private clients increasingly demand transparency regarding carbon exposure, stewardship practices, and responsible investment screening. Regulatory frameworks encouraging climate disclosure reinforce integration of ESG metrics into portfolio construction processes. Development of thematic funds focused on renewable energy, infrastructure transition, and social impact enables wealth managers to capture capital flows directed toward sustainable assets. Enhanced data analytics improve measurement of ESG performance and risk mitigation outcomes. Wealth managers can integrate sustainability advisory into broader financial planning discussions, strengthening client relationships. Corporate clients and family offices seek alignment between investment strategies and philanthropic objectives. Expansion of green bonds and sustainable private equity creates diversified allocation pathways. This structural shift supports asset growth and brand differentiation within competitive advisory markets.

Growth of Cross-Border Wealth and International Client Servicing

The United Kingdom’s established financial infrastructure and global connectivity create significant opportunities to attract and manage cross-border wealth from international clients seeking stable advisory jurisdictions. London’s legal and financial services ecosystem provides sophisticated trust structures and international tax planning expertise. Global mobility among high-net-worth individuals drives demand for multi-currency portfolio management and jurisdictional diversification. Wealth managers can leverage international custody networks to deliver integrated banking and investment services. Political and economic diversification strategies encourage overseas investors to allocate assets within UK-managed portfolios. Digital advisory capabilities enable seamless engagement with clients residing outside the country. Partnerships with global private banks expand referral pipelines and offshore advisory mandates. Expansion of alternative investment platforms enhances cross-border appeal. These dynamics position UK wealth managers to capture incremental inflows from internationally diversified high-value clients.

Future Outlook

The UK wealth management market is expected to experience steady expansion over the next five years, supported by sustained private wealth accumulation, pension asset growth, and rising demand for discretionary mandates. Technological innovation will deepen through artificial intelligence-driven advisory tools and digital client engagement platforms. Regulatory emphasis on transparency and consumer duty is likely to enhance trust and governance standards. Demand for sustainable investments and cross-border diversification will continue shaping portfolio construction strategies across affluent and high-net-worth segments.

Major Players

- St. James’s Place

- Schroders

- HSBC Global Private Banking

- Barclays Private Bank

- Quilter

- Brewin Dolphin

- Rathbones Group

- Evelyn Partners

- Investec Wealth & Investment

- Charles Stanley

- Cazenove Capital

- Close Brothers Asset Management

- Standard Life Wealth

- JM Finn

- Brooks Macdonald

Key Target Audience

- High-Net-Worth Individuals

- Ultra-High-Net-Worth Individuals

- Family Offices

- Pension Fund Administrators

- Insurance Companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- International Private Banking Clients

Research Methodology

Step 1: Identification of Key Variables

Core variables including assets under management, client segmentation, service mix, fee structures, and regulatory frameworks were identified through secondary research. Macroeconomic indicators and pension asset data were mapped to wealth accumulation trends.

Step 2: Market Analysis and Construction

A bottom-up approach was used to assess institutional and retail asset pools. Company financial disclosures and industry association reports were synthesized to construct the overall market framework.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with industry professionals, portfolio managers, and compliance specialists. Insights were refined to ensure alignment with prevailing regulatory and market dynamics.

Step 4: Research Synthesis and Final Output

Quantitative data and qualitative insights were consolidated into a structured analytical framework. The final output integrates segmentation, competitive benchmarking, and forward-looking evaluation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Household Financial Assets and Investment Participation

Increasing Demand for Retirement and Pension Planning

Expansion of Digital and Hybrid Advisory Platforms - Market Challenges

Regulatory Compliance under FCA and MiFID II

Market Volatility Affecting Portfolio Performance

Fee Compression and Competitive Pricing Pressure - Market Opportunities

Growth of ESG and Sustainable Investment Mandates

Integration of Artificial Intelligence in Portfolio Management

Cross Border Advisory for International Investors - Trends

Shift Toward Passive and ETF Based Investment Strategies

Adoption of Digital Client Reporting and Analytics Tools - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory and Financial Planning Services

Robo Advisory Solutions

Alternative Investment Advisory

Estate and Tax Planning Services - By Platform Type (In Value%)

Private Banking Platforms

Independent Financial Advisors

Broker Dealer Networks

Digital Wealth Platforms

Hybrid Advisory Models - By Fitment Type (In Value%)

Fee Based Advisory Model

Commission Based Model

Hybrid Fee Structure

Subscription Based Wealth Services - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Mass Affluent Investors

Family Offices and Trusts

- Market Share Analysis

- Cross Comparison Parameters (Assets Under Management, Fee Structure Model, Minimum Investment Threshold, Digital Advisory Capability, Product Diversification Range)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

St James Place Wealth Management

Schroders Personal Wealth

Rathbones Group

Brewin Dolphin

HSBC Private Banking UK

Barclays Private Bank

Lloyds Bank Private Banking

Coutts and Co

UBS Wealth Management UK

J P Morgan Private Bank UK

Charles Stanley Group

Investec Wealth and Investment

Quilter plc

Evelyn Partners

Canaccord Genuity Wealth Management

- Growing Preference for Personalized and Goal Based Investment Strategies

- Rising Allocation toward Alternative and Private Market Assets

- Demand for Transparent Fee Structures and Reporting

- Succession and Estate Planning Needs among Aging Investors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now