Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US Aerospace and Defense market is valued at approximately USD ~ billion, driven by ongoing investments in military modernization, technological advancements, and expanding defense budgets. The market is primarily fueled by the continuous development of advanced military systems, aerospace technology, and space exploration. Increased defense spending from both government and private sector players is a key factor propelling market growth. With heightened geopolitical tensions and the integration of artificial intelligence, robotics, and cybersecurity in defense solutions, this sector is experiencing significant innovation.

The US remains a dominant player in the global aerospace and defense sector due to its robust infrastructure, technological leadership, and strategic investments in defense. Major defense contractors and agencies in cities such as Washington, D.C., Los Angeles, and Seattle contribute to the market’s leadership position. The United States’ military and space programs have set benchmarks in defense innovation, including advancements in aircraft, satellite systems, and unmanned technologies. Strategic initiatives and a strong regulatory framework further consolidate the country’s position as a key global player in this space.

Market Segmentation

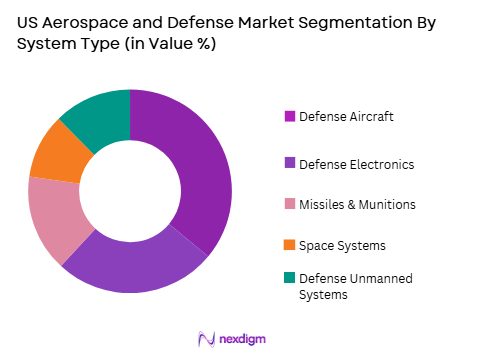

By System Type

The US Aerospace and Defense market is segmented by system type into defense aircraft, defense electronics, missiles & munitions, space systems, and defense unmanned systems. Recently, the defense aircraft sub-segment has dominated the market share due to the growing demand for advanced combat aircraft and military transport systems. Factors such as technological innovation, defense budget allocations, and government policies that focus on military modernization are driving the increasing need for defense aircraft. Additionally, the rise in international tensions and the need for national security have led to an escalation in aircraft development and procurement.

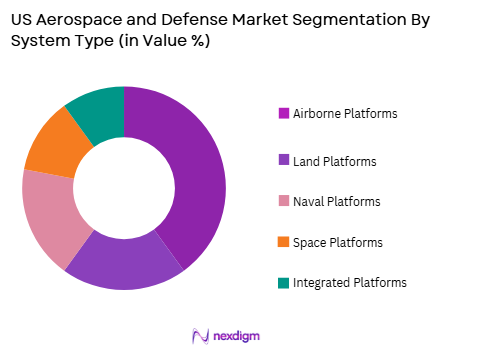

By Platform Type

The market is segmented by platform type into airborne platforms, land platforms, naval platforms, space platforms, and integrated platforms. Airborne platforms have the largest market share, owing to the increasing demand for both combat and surveillance aircraft. The integration of next-gen technologies like unmanned aerial systems (UAS) and advancements in stealth technology contribute to the dominance of airborne platforms. Additionally, the United States’ strategic focus on enhancing air superiority and the growth of aerospace defense spending in both military and commercial sectors play a key role in this segment’s prominence.

Competitive Landscape

The competitive landscape of the US Aerospace and Defense market is marked by consolidation, with key players dominating the industry. Major companies continue to invest heavily in research and development to stay ahead in technological advancements, including AI, cyber defense, and aerospace systems. These players leverage strategic partnerships, acquisitions, and government contracts to enhance their market share. With major players leading in various segments like defense systems, aerospace manufacturing, and satellite technologies, the market remains competitive and innovation-driven.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Market-Specific Parameter |

| Lockheed Martin | 1912 | Bethesda, MD | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, IL | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church, VA | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 1922 | Waltham, MA | ~ | ~ | ~ | ~ | ~ |

| General Dynamics | 1952 | Falls Church, VA | ~ | ~ | ~ | ~ | ~ |

US Aerospace and Defense Market Analysis

Growth Drivers

Technological Advancements in Aerospace Systems

Technological advancements in aerospace systems are driving market growth. The continuous development of state-of-the-art aircraft, drones, and defense electronics allows the US to maintain military superiority. Innovation in propulsion, communication systems, and surveillance technologies enhances the efficiency and capabilities of defense systems. In particular, the integration of artificial intelligence (AI) and machine learning (ML) into aircraft, unmanned aerial vehicles (UAVs), and cybersecurity solutions has revolutionized operational effectiveness. Additionally, innovations like autonomous weapons systems are pushing the boundaries of modern warfare, presenting significant growth opportunities within the aerospace and defense sector. Furthermore, advancements in space technologies, including satellite systems and defense capabilities, are expanding the US’s strategic advantage in global security. The continued demand for both manned and unmanned platforms ensures that technological breakthroughs in these areas remain critical for sustaining the growth trajectory in this market.

Government Investment in National Security

The US government’s increasing investment in national security is a significant growth driver for the aerospace and defense market. With rising global security concerns and the evolution of warfare technologies, the US government is allocating substantial funds to develop next-generation defense systems. These investments are essential in ensuring military readiness, enhancing technological capabilities, and reinforcing national defense infrastructure. Federal budgets continue to prioritize defense spending, facilitating the advancement of military projects, including the development of new aircraft, missile defense systems, and space programs. Furthermore, federal contracts for defense manufacturers are expected to increase as the country focuses on fortifying its defense systems against potential threats. The integration of new technologies and military modernization programs continues to be the primary focus of these investments, ensuring the US remains a global leader in defense capabilities.

Market Challenges

High Capital Expenditure in Aerospace Projects

One of the main challenges in the US Aerospace and Defense market is the high capital expenditure required for aerospace projects. Developing cutting-edge aircraft, defense systems, and space technologies involves significant financial commitments. These investments often result in long development cycles and require immense R&D efforts, which can strain both private and public finances. Furthermore, the complexity and size of such projects necessitate substantial manufacturing and testing costs, which further increases the overall capital expenditure. The challenge is compounded by delays in project timelines and budget overruns, which can disrupt the financial viability of such projects. Government spending, while robust, is still subject to fiscal policies, political decision-making, and economic fluctuations that can impact the budget allocations for critical aerospace and defense programs. Additionally, the requirement for continuous updates to aging military equipment and technologies further drives up costs, posing a challenge for companies and governments seeking to maintain a modern, competitive defense force.

Regulatory and Compliance Barriers

Regulatory and compliance barriers pose another significant challenge for the US Aerospace and Defense market. Defense contractors and aerospace manufacturers must adhere to a stringent set of regulations that govern procurement, technology development, export controls, and cybersecurity standards. Compliance with these rules is mandatory for all players in the market, often requiring substantial investment in legal, administrative, and operational processes. The US government’s strict export control regulations on defense-related technologies, including the International Traffic in Arms Regulations (ITAR), limit market expansion opportunities for US firms, especially in foreign markets. Additionally, as aerospace and defense technologies evolve, regulatory frameworks must adapt quickly to emerging technologies like autonomous systems, cyber-defense tools, and artificial intelligence. Delays in updating regulations to keep pace with technological advances can hinder the growth and adoption of innovative solutions. Moreover, non-compliance with these regulations can lead to severe penalties, damaging companies’ reputations and financial standing.

Opportunities

Expansion in Artificial Intelligence-Driven Defense Solutions

One of the key opportunities in the US Aerospace and Defense market lies in the expansion of artificial intelligence (AI)-driven defense solutions. As AI and machine learning continue to evolve, they present unprecedented opportunities for enhancing defense systems. AI technologies are already being integrated into military platforms, from autonomous drones and unmanned ground vehicles to surveillance and reconnaissance systems. These solutions are able to analyze vast amounts of data in real time, offering improved decision-making capabilities, predictive maintenance, and enhanced operational efficiency. In addition to improving defense systems, AI-driven technologies are also expected to revolutionize cybersecurity and defense intelligence systems, enabling quicker responses to emerging threats. The US government’s strong support for AI research and defense technology development, along with the rise of private sector involvement in AI, positions the market for continued growth in this area. The demand for AI-powered defense technologies is expected to increase as geopolitical tensions rise, providing ample opportunities for companies to develop innovative solutions that meet national security requirements.

Partnerships with Private Tech Firms for Enhanced Cybersecurity

Partnerships between defense contractors and private tech firms focused on enhancing cybersecurity present a valuable market opportunity. With the increasing number of cyberattacks and rising concerns about national security, the demand for cybersecurity solutions is growing rapidly. Collaboration between private tech firms and defense contractors is essential for developing advanced cybersecurity systems to protect sensitive military and defense infrastructure. These partnerships enable the integration of cutting-edge technologies, such as AI, blockchain, and data encryption, into defense systems, improving the resilience of national security. As cyber warfare becomes an ever-growing concern, governments and defense agencies are seeking stronger cybersecurity measures, opening new revenue streams for companies in the aerospace and defense market. Furthermore, these partnerships help address the shortage of skilled cybersecurity professionals in the defense sector, offering companies the opportunity to enhance their market position.

Future Outlook

The future outlook for the US Aerospace and Defense market over the next five years shows promising growth, driven by technological advancements, government support, and increasing demand for enhanced defense systems. Investment in next-gen technologies such as autonomous systems, AI, and cybersecurity will continue to shape the market. Additionally, the US government’s commitment to defense spending and national security will provide a steady stream of projects and contracts for defense contractors. As international threats evolve, the US is likely to expand its aerospace and defense capabilities, with a focus on air, space, and cyber defense. Technological innovation, including advancements in space exploration and military aircraft, will be a key factor in driving market growth.

Major Players

- Lockheed Martin

- Northrop Grumman

- Boeing

- Raytheon Technologies

- General Dynamics

- BAE Systems

- L3 Harris Technologies

- Leonardo

- Thales Group

- Harris Corporation

- Elbit Systems

- Rheinmetall AG

- BAE Systems

- Sikorsky Aircraft

- General Electric

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Defense contractors

- Aerospace system integrators

- Military forces

- Defense technology providers

- Space exploration companies

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key market variables such as technological trends, governmental policies, and consumer preferences that will shape market dynamics.

Step 2: Market Analysis and Construction

This step involves gathering data on market size, segments, and growth patterns through primary and secondary research.

Step 3: Hypothesis Validation and Expert Consultation

Engaging with industry experts and validating the findings with the latest market data helps ensure accuracy and relevance.

Step 4: Research Synthesis and Final Output

The final output synthesizes all collected data into a comprehensive market report, ensuring clarity and actionable insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Investment in National Security

Technological Advancements in Aerospace Systems

Rising Geopolitical Tensions - Market Challenges

High Capital Expenditure in Aerospce Projects

Regulatory and Compliance Barriers

Technological Integration and Interoperability Issues - Market Opportunities

Growth in Autonomous and Unmanned Systems

Partnerships with Private Tech Firms for Enhanced Defense Solutions

Expansion in Space Exploration and Commercialization - Trends

Rise in Use of AI and Automation in Defense Systems

Increased Focus on Cybersecurity for Aerospace Platforms

Development of Next-gen Fighter Aircrafts and Missiles - Government regulations

Export Control and Compliance Policies

Cybersecurity Regulations for Aerospace Systems

Government Funding and Grants for Defense Technologies - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Defense Aircraft

Defense Electronics

Missiles & Munitions

Space Systems

Defense Unmanned Systems - By Platform Type (In Value%)

Airborne Platforms

Land Platforms

Naval Platforms

Space Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Military Forces

Government Agencies

Defense Contractors

Commercial Aviation

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Market Share, Technological Advancements, Regulatory Compliance, Geopolitical Influence, Investment Levels)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Lockheed Martin

Northrop Grumman

Boeing

Raytheon Technologies

General Dynamics

BAE Systems

L3 Harris Technologies

Leonardo

Thales Group

Saab Group

Harris Corporation

Elbit Systems

Rheinmetall AG

BAE Systems

Sikorsky Aircraft

- Military Forces’ Increasing Demand for Advanced Systems

- Government Agencies’ Role in Regulating and Procuring Aerospace Technologies

- Defense Contractors’ Shift Towards Innovation

- Private Sector’s Growing Interest in Space Exploration

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now