Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US civil aviation flight training and simulation market is valued at approximately USD ~ billion, driven by increasing demand for aviation safety and pilot training programs. This market growth is propelled by advancements in simulation technology, including virtual reality and AI integration. The demand for cost-effective and scalable solutions is also pushing market expansion, as airlines and training centers look for ways to enhance pilot skills while minimizing operational costs.

The US remains a dominant force in the civil aviation flight training and simulation sector due to its extensive airline networks and regulatory support. Key cities such as Dallas, Atlanta, and Chicago are central to market growth due to their proximity to major aviation hubs and the presence of leading flight schools and training centers. These cities foster strong relationships between airlines, training organizations, and technology providers, ensuring a steady demand for simulation of equipment and services.

Market Segmentation

By Product Type

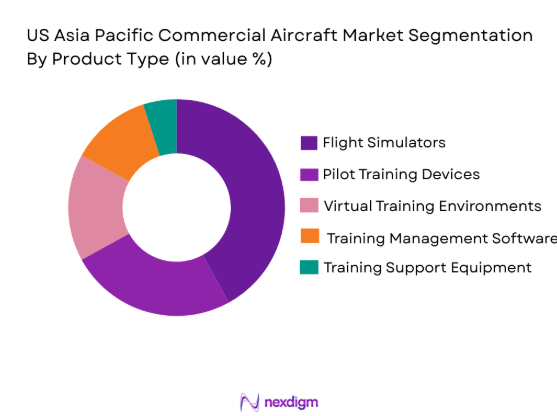

The US civil aviation flight training and simulation market is segmented by product type into flight simulators, pilot training devices, virtual training environments, training management software, and training support equipment. Recently, flight simulators have held a dominant market share due to their effectiveness in replicating various flight conditions and scenarios, making them indispensable in modern pilot training. The rising need for realistic, cost-efficient, and versatile training tools has made flight simulators the preferred choice in both commercial and military aviation training programs.

By Platform Type

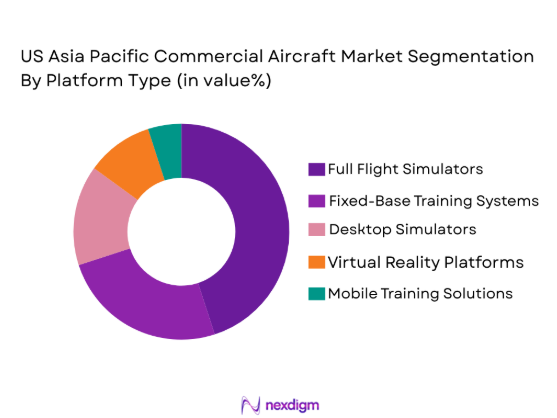

The US civil aviation flight training and simulation market is segmented by platform type into fixed-base training systems, full flight simulators, desktop simulators, virtual reality platforms, and mobile training solutions. Recently, full flight simulators have dominated the market share due to their ability to provide the most realistic and immersive training experience. These platforms replicate real-world flight conditions with high accuracy, which is crucial for pilot training in both commercial and military aviation sectors. The demand for full flight simulators is further driven by their ability to handle complex flight scenarios and emergency situations, providing pilots with the necessary skills for safe operations. Their widespread adoption by major airlines and flight training institutions reflects their importance in modern pilot education programs, contributing significantly to market growth.

Competitive Landscape

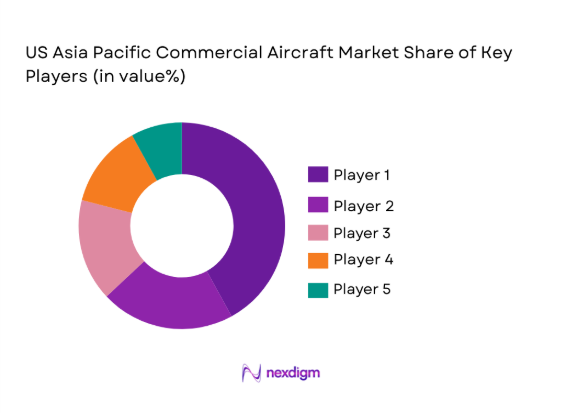

The competitive landscape of the US civil aviation flight training and simulation market is marked by significant consolidation, with major players dominating the market through technological advancements and strategic partnerships. These players focus on enhancing simulation capabilities, integrating emerging technologies like AI, and expanding global market reach. Leading companies are involved in mergers and acquisitions to improve product offerings and maintain a competitive edge in an increasingly crowded market.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| CAE Inc. | 1947 | Montreal, Canada | ~ | ~ | ~ | ~ | ~ |

| L3Harris Technologies | 2019 | Melbourne, USA | ~ | ~ | ~ | ~ | ~ |

| FlightSafety International | 1951 | Wichita, USA | ~ | ~ | ~ | ~ | ~ |

| Rockwell Collins | 1933 | Cedar Rapids, USA | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

US Civil Aviation Flight Training and Simulation Market Analysis

Growth Drivers

Rising Demand for Pilot Training

The US civil aviation flight training and simulation market is experiencing significant growth due to the increasing need for skilled pilots across both commercial airlines and military aviation sectors. With the rising global demand for air travel, airlines are expanding their fleets, which, in turn, requires more pilots. The need for effective training systems has led to the widespread adoption of simulation technology. Flight simulators allow for realistic training scenarios that enhance pilot skills and provide hands-on experience in emergency situations without the associated risks or costs of live flights. Simulators are highly beneficial in reducing training costs, minimizing risks, and improving training efficiency, which makes them a top choice for flight schools and commercial aviation companies. Furthermore, the ability to train pilots across various aircraft types without needing physical aircraft has significantly increased the adoption of simulators. This rising demand for qualified pilots, especially in the context of expanding global aviation fleets, is expected to continue driving market growth. Additionally, regulatory requirements and government support for aviation training programs contribute to further market expansion, as strict safety and training regulations ensure that only qualified pilots are allowed to operate commercial aircraft.

Technological Advancements in Simulation

Technological advancements in simulation systems are also fueling the growth of the US civil aviation flight training and simulation market. Innovations in virtual reality (VR), augmented reality (AR), and artificial intelligence (AI) are transforming how flight simulators work, making them more immersive and realistic. These advancements allow for better training experiences by replicating complex flight conditions and environments. VR and AR integration enhances the realism of flight simulators, enabling pilots to train for a wide range of scenarios, including extreme weather conditions and emergency situations, without leaving the ground. AI-powered simulators can adapt to a pilot’s individual training needs and progress, offering personalized training experiences. The push toward more sophisticated, customizable, and cost-effective simulation systems has made it a highly attractive solution for both commercial and military aviation sectors. These technological advancements also support the shift toward cloud-based and modular training platforms, allowing aviation companies to deliver scalable and flexible training solutions to pilots across different regions. With these advancements, the market is poised to benefit from increased demand as aviation companies seek to improve their training processes while optimizing operational costs.

Market Challenges

High Initial Investment

One of the significant challenges facing the US civil aviation flight training and simulation market is the high initial investment required to procure and maintain flight simulators. The upfront cost of purchasing advanced simulation systems can be prohibitively expensive for smaller flight schools and regional airlines, particularly those looking to incorporate the latest technologies, such as VR or AI-powered systems. This high cost barrier can limit the adoption of flight simulators by certain sectors, especially small-to-medium-sized enterprises that may not have the financial resources to invest in these advanced technologies. Furthermore, the maintenance and operational costs associated with flight simulators can add to the financial burden. For example, simulator systems require regular calibration, software updates, and maintenance, all of which incur ongoing expenses. This makes it difficult for smaller companies to remain competitive with larger players that can afford to make significant investments in their simulation infrastructure. In addition to the high financial costs, the complexity of training personnel to operate and maintain these systems adds another layer of challenge. Despite the technological benefits, many smaller firms may find it more cost-effective to rely on traditional training methods, thus slowing the adoption rate of simulation systems in certain areas.

Regulatory Barriers

Regulatory challenges also pose significant barriers to the growth of the US civil aviation flight training and simulation market. Flight training and simulation systems are subject to stringent regulations from government agencies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA). These regulations ensure that flight simulators meet specific safety standards, performance benchmarks, and operational requirements. Compliance with these regulations can be time-consuming and costly, especially when new technologies, such as virtual and augmented reality, are incorporated into training systems. Additionally, frequent updates to regulations may require simulator manufacturers and training organizations to make costly modifications to existing systems. The process of certifying new simulation systems can be lengthy and complex, potentially delaying the introduction of innovative technologies to the market. Furthermore, the regulatory landscape can vary from country to country, complicating the ability of manufacturers and training providers to enter international markets without facing additional certification challenges. Regulatory compliance requirements also drive up the cost of acquiring and operating simulators, making it even more difficult for smaller training organizations to participate in the market.

Opportunities

Growth of Virtual and Augmented Reality in Training Systems

The increasing integration of virtual reality (VR) and augmented reality (AR) technologies into flight training systems presents a significant opportunity for growth in the US civil aviation flight training and simulation market. VR and AR technologies offer a high level of immersion, making flight simulations more realistic and enabling trainees to experience various flight scenarios that would be difficult or costly to replicate in the real world. These immersive technologies provide the opportunity for training on specific situations such as emergency landings, system failures, or bad weather conditions, which can be simulated without the risks associated with live training. Additionally, VR and AR systems can reduce training costs by allowing trainees to practice in a controlled, virtual environment without requiring the use of expensive physical aircraft or full-motion simulators. The growing demand for these technologies in the aviation sector is also being driven by the increasing affordability and accessibility of VR and AR hardware, along with the development of more sophisticated simulation software. As the technology matures, more aviation companies and flight schools are likely to adopt these innovative training solutions, increasing the demand for advanced simulation platforms. As such, VR and AR adoption offers a significant growth opportunity for companies in the simulation market, enabling them to capture a larger share of the training solutions market.

Partnerships with Aviation Universities and Corporations

Another key opportunity for the US civil aviation flight training and simulation market is the increasing number of partnerships between flight simulator providers, aviation universities, and corporate organizations. These partnerships allow simulation companies to expand their reach and offer tailored training solutions to a broader range of customers. Aviation universities and corporate flight departments are actively seeking high-quality training programs that can meet the needs of aspiring pilots and aviation professionals. By partnering with these institutions, simulation providers can develop customized training programs that address the specific needs of students and professionals. These collaborations also present opportunities for simulation companies to participate in cutting-edge research and development, further improving their product offerings. Additionally, partnerships with airlines and training providers can help establish long-term relationships and secure recurring business opportunities for simulation providers. As the aviation industry continues to evolve, these partnerships will be essential in ensuring that flight training programs are equipped with the latest simulation technology to meet the growing demand for skilled pilots. By tapping into these strategic partnerships, flight training and simulation providers can significantly expand their market share and position themselves for future growth.

Future Outlook

Over the next five years, the US civil aviation flight training and simulation market is expected to continue its steady growth, driven by technological advancements, regulatory support, and the increasing demand for skilled pilots. The adoption of virtual and augmented reality technologies, along with AI-powered simulators, is likely to enhance training capabilities and reduce operational costs for airlines and training institutions. Additionally, increasing government investments in aviation safety and training programs will provide further opportunities for growth. The market is poised for expansion as both commercial and military sectors seek more advanced, scalable, and cost-effective training solutions.

Major Players

- CAE Inc.

- L3Harris Technologies

- FlightSafety International

- Rockwell Collins

- Boeing

- Alsim Simulation

- AeroStar Training Services

- TRU Simulation + Training

- Aviation Performance Solutions

- Frasca International

- Lufthansa Aviation Training

- Airbus

- Saab

- ZedaSoft

- Airbus DS

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Airlines and aviation companies

- Flight training schools

- Simulation equipment manufacturers

- Military and defense agencies

- Corporate flight departments

- Aviation technology providers

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying the critical factors influencing the market, including market size, growth drivers, challenges, and key trends.

Step 2: Market Analysis and Construction

A detailed analysis is conducted to examine the market dynamics, segmentations, and potential areas for growth.

Step 3: Hypothesis Validation and Expert Consultation

The initial hypotheses are validated through interviews with industry experts and stakeholders to ensure accuracy.

Step 4: Research Synthesis and Final Output

The collected data is synthesized into a comprehensive report, including all relevant findings, insights, and projections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Demand for Qualified Pilots

Technological Advancements in Flight Simulators

Government Investments in Aviation Safety and Training

Increased Demand for Cost-Effective Training Solutions

Growing Airline Fleet Expansion - Market Challenges

High Initial Investment in Flight Simulators

Regulatory Compliance and Certification Barriers

Technological Integration Challenges

Lack of Skilled Trainers for Advanced Simulations

High Maintenance and Operational Costs of Training Equipment - Market Opportunities

Growth of Virtual and Augmented Reality in Training Systems

Emerging Demand for Customized Pilot Training Solutions

Partnerships with Aviation Universities and Corporations - Trends

Integration of Artificial Intelligence in Training Systems

Shift Towards Cloud-based Flight Training Solutions

Growing Adoption of Hybrid and Modular Training Platforms

Advancements in Immersive Virtual Reality for Pilot Training

Increased Focus on Cybersecurity in Flight Training Systems - Government Regulations & Defense Policy

FAA Training Requirements and Certification

Compliance with International Aviation Safety Standards

Government Funding for Aviation Training Research and Development

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Flight Simulators

Pilot Training Devices

Virtual Training Environments

Training Management Software

Training Support Equipment - By Platform Type (In Value%)

Fixed-Base Training Systems

Full Flight Simulators

Desktop Simulators

Virtual Reality Platforms

Mobile Training Solutions - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Commercial Airlines

Flight Schools

Government and Military

Corporate Flight Departments

Training Service Providers - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Simulated Hardware

Training Software

Virtual Reality Technologies

Augmented Reality Systems

Artificial Intelligence Systems

- Market structure and competitive positioning

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

CAE Inc.

L3Harris Technologies

FlightSafety International

Rockwell Collins

Boeing

Alsim Simulation

AeroStar Training Services

TRU Simulation + Training

Aviation Performance Solutions

Frasca International

Lufthansa Aviation Training

Airbus

Saab

ZedaSoft

Airbus DS

- Commercial Airlines’ Increasing Demand for Simulators

- Flight Schools’ Investment in Affordable Training Solutions

- Government and Military Adoption of Advanced Simulation Technologies

- Training Service Providers’ Shift Towards Integrated Systems

Forecast Market Value, 2026-2035

Forecast Installed Units, 2026-2035

Price Forecast by System Tier, 2026-2035

Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now