Download PDF

Download PDFMarket Overview

The US commercial aircraft cabin interior market current size stands at around USD ~ million, reflecting sustained demand for certified seating systems, galleys, lavatories, monuments, bins, and connected cabin hardware across new aircraft deliveries and refurbishment programs. Capital deployment across interior platforms remains steady, with investments in lightweight materials, modular monuments, and digital cabin management. Spending is shaped by long certification cycles, multi-year supplier contracts, and airline refresh strategies tied to fleet renewal and service differentiation initiatives.

Demand concentration is strongest around aerospace manufacturing and MRO hubs in Washington state, California, Kansas, Oklahoma, Texas, and Florida, supported by dense supplier clusters, engineering talent, and certification pathways. Airline operational bases in Atlanta, Dallas–Fort Worth, Chicago, Denver, Phoenix, and Los Angeles anchor retrofit activity through proximity to maintenance capacity. The ecosystem benefits from mature Tier-1 integration, specialized interiors workshops, and policy environments emphasizing airworthiness compliance, safety certification, and domestic manufacturing resilience.

Market Segmentation

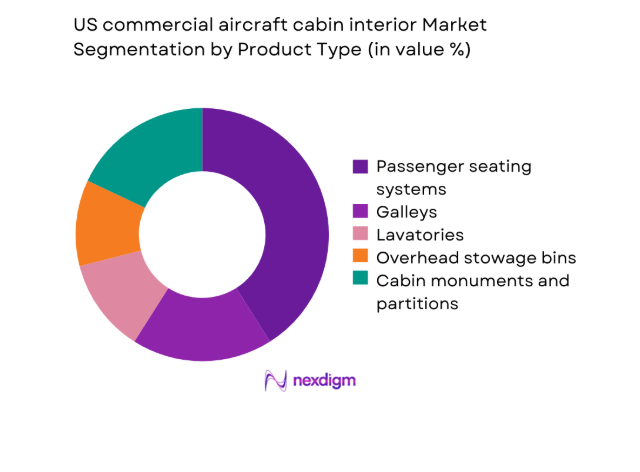

By Product Type

Passenger seating systems dominate procurement because they drive cabin density, comfort differentiation, and weight optimization across narrow-body fleets. Slimline architectures, integrated power, and modular cushions enable rapid refresh cycles aligned to heavy checks, while galleys and lavatories follow as secondary spend driven by hygiene upgrades and accessibility mandates. Overhead bins and monuments are increasingly specified in lightweight composites to offset densification penalties. IFEC hardware and cabin lighting see cyclical demand tied to connectivity upgrades and brand refresh programs. The dominance of seating reflects airline focus on yield management, faster linefit integration, and scalable retrofit kits certified across aircraft families, compressing downtime and installation complexity.

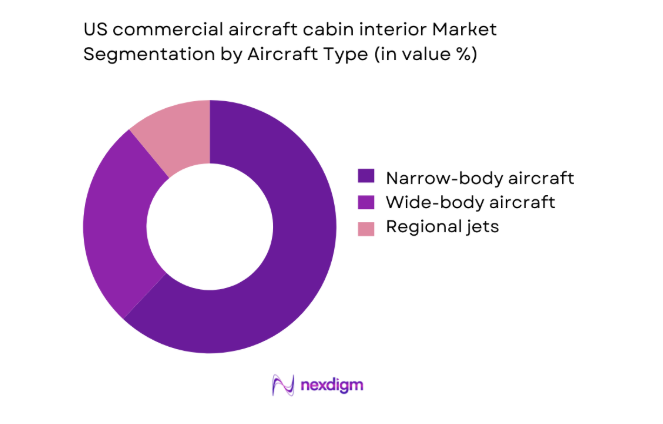

By Aircraft Type

Narrow-body aircraft account for the majority of interior demand due to high utilization rates, dense route networks, and faster refurbishment cycles. Cabin densification and premium-economy retrofits on single-aisle fleets create recurring replacement volumes for seats, bins, and monuments, while wide-body programs emphasize premium cabins, galleys, and connectivity upgrades aligned to long-haul differentiation. Regional jets contribute targeted demand for lightweight seating and compact monuments optimized for turn-time efficiency. The segmentation is reinforced by standardized interior kits across narrow-body families, enabling airlines to streamline spares, certification, and installation workflows while scaling retrofit cadence across multiple bases.

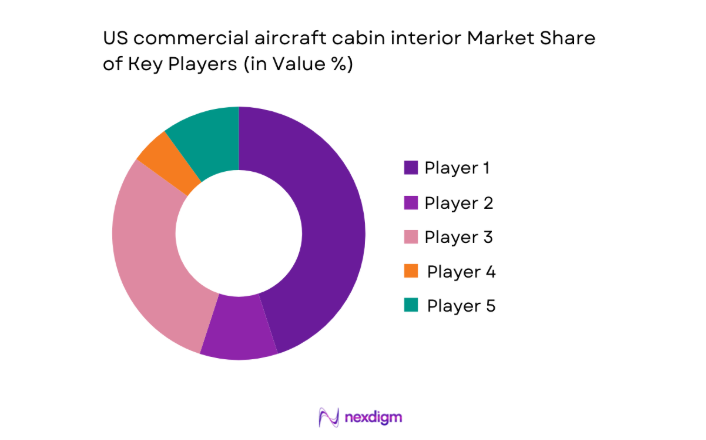

Competitive Landscape

The competitive environment is shaped by certification depth, linefit relationships, and aftermarket installation capability across major MRO bases. Differentiation centers on modularity, lead-time reliability, and integration with digital cabin systems, while long qualification cycles favor incumbents with established STC portfolios and airline-approved kits.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Safran Seats USA | 2014 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Collins Aerospace Interiors | 2018 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Adient Aerospace | 2016 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Recaro Aircraft Seating | 1972 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Jamco America | 2009 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

US commercial aircraft cabin interior Market Analysis

Growth Drivers

Rising narrow-body fleet deliveries and cabin densification programs

Airline narrow-body utilization remains elevated, with average daily aircraft cycles recorded at 6 to 8 across major domestic networks during 2024 and 2025, increasing wear on seating, bins, and monuments. Federal aviation data shows single-aisle movements exceeded 22 in several hub airports in 2024, accelerating refurbishment cadence. Manufacturing indicators reported 3 consecutive quarters of backlog expansion across certified interior components during 2023 and 2024, while maintenance bases expanded bay capacity by 2 to accommodate faster turn times. Aircraft delivery schedules in 2024 added 482 narrow-body units to active fleets, intensifying linefit demand. Densification kits standardization reduced installation hours from 420 to 360 per shipset across multiple MROs.

Adoption of lightweight composite interiors to reduce fuel burn

Airlines prioritize mass reduction to stabilize operating efficiency under volatile fuel markets, with fleet programs targeting 150 to 280 kilograms per narrow-body shipset reduction achieved through composite bins, slimline seats, and thermoplastic monuments during 2023 to 2025. Certification filings recorded 74 supplemental approvals for lightweight interior modifications in 2024, reflecting rapid uptake. Federal efficiency metrics indicate average block fuel per departure declined from 3,980 to 3,760 kilograms on comparable sectors following interior retrofits. Manufacturing output indices for aerospace composites rose 11 points across 2024, while MRO adoption of pre-certified lightweight kits shortened induction windows from 14 to 11 days, enabling faster return to service and higher aircraft availability across dense domestic networks.

Challenges

Long FAA certification timelines for new interior components

Certification lead times constrain innovation cycles, with type design approvals for seating and monuments extending from 9 months in 2022 to 14 months in 2024 due to conformity backlogs. Regulatory filings for interiors experienced 1,420 application reviews across 2023 and 2024, exceeding inspector capacity by 210 positions nationally. Engineering change orders increased to 3 per program on average, driven by flammability and dynamic load testing iterations. MRO induction slots were delayed by 6 to 10 weeks awaiting approvals, reducing aircraft availability during peak schedules. Compliance documentation volumes rose from 1,200 to 1,760 pages per certification package, increasing program management overhead and elongating time-to-install across fleet-wide retrofit campaigns.

Supply chain disruptions and long lead times for certified materials

Interior-grade foams, laminates, and composite panels experienced procurement lead times rising from 18 to 34 weeks between 2022 and 2024 due to constrained supplier capacity and specialty resin shortages. Logistics throughput at major ports showed container dwell times of 6 to 9 days during 2024, disrupting kit synchronization for linefit deliveries. Tier-2 machining queues extended from 21 to 38 days for certified brackets, while quality escape rates rose to 2.4 per 1,000 components in 2025, increasing rework cycles. Workforce vacancy rates across certified upholstery lines averaged 12 in 2024, slowing throughput. These constraints forced MROs to stagger inductions, elongating retrofit schedules and raising operational complexity.

Opportunities

Fleet-wide cabin retrofits for connectivity and seat upgrades

Connectivity penetration expanded across domestic fleets, with 9 of 10 major operators mandating seat power and antenna upgrades across narrow-body programs during 2024 and 2025. Installation campaigns averaged 120 aircraft per carrier annually, supported by standardized kits that reduced downtime from 6 to 4 days per aircraft. Passenger device usage metrics from airport authorities recorded 1.8 connected devices per traveler in 2024, reinforcing demand for power-enabled seating. Certification throughput improved with 52 approvals for bundled retrofit packages in 2025, enabling scale deployment. Maintenance capacity additions of 4 new hangar bays across major hubs supported accelerated rollouts, creating sustained demand for integrated seating, monuments, and IFEC hardware installations.

Sustainable materials and recyclable cabin components adoption

Environmental compliance pressures accelerated adoption of recyclable thermoplastics and low-VOC laminates across interiors programs, with 38 new material qualifications recorded in 2024 and 2025. Waste audits at major MROs indicated interior scrap volumes of 420 tons annually, creating incentives for closed-loop material recovery. Manufacturing energy intensity indices for thermoplastics declined 14 points between 2023 and 2025, improving lifecycle performance. Airline sustainability frameworks mandate 25 percent recycled content targets for non-structural cabin components in new programs, catalyzing supplier reformulation. Regulatory guidance updates expanded acceptance of recycled polymers in flammability testing, shortening validation cycles and opening pathways for scaled deployment across narrow-body and regional jet fleets.

Future Outlook

The market outlook reflects sustained retrofit cycles aligned to fleet renewal, connectivity standardization, and premium cabin differentiation across domestic networks. Certification throughput is expected to normalize as inspector capacity expands, enabling faster adoption of lightweight and sustainable interiors. Narrow-body programs will anchor volume growth, while modular monuments and bundled retrofit kits improve installation velocity. Policy emphasis on domestic manufacturing resilience and safety compliance will continue to shape supplier strategies through the forecast period.

Major Players

- Safran Seats USA

- Collins Aerospace Interiors

- Adient Aerospace

- Recaro Aircraft Seating

- Jamco America

- Diehl Aviation

- Thompson Aero Seating

- Haeco Cabin Solutions

- Astronics Corporation

- Aviointeriors

- Acro Aircraft Seating

- Aim Altitude

- Lufthansa Technik

- FACC Cabin Interiors

- Expliseat

Key Target Audience

- Airline fleet planning and engineering departments

- Aircraft OEM interiors integration teams

- MRO operators and certified repair stations

- Cabin design and certification engineering firms

- Aircraft lessors and asset management firms

- Investments and venture capital firms

- Government and regulatory bodies with agency names such as the Federal Aviation Administration

- Airport authorities and infrastructure operators

Research Methodology

Step 1: Identification of Key Variables

Key variables were mapped across interior product categories, certification pathways, installation capacity, and airline refresh cycles. Operational metrics included induction throughput, approval lead times, and component reliability indicators. Ecosystem variables covered supplier tiering, material qualification depth, and MRO bay availability.

Step 2: Market Analysis and Construction

The market construct integrated linefit and retrofit workflows across narrow-body, wide-body, and regional fleets. Demand drivers were aligned with utilization intensity, maintenance cycles, and connectivity mandates. Structural constraints were modeled using certification queues, material lead times, and labor availability across certified interiors lines.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on densification, lightweighting, and sustainability adoption were validated through structured consultations with airline engineering teams, MRO program managers, and certification specialists. Operational benchmarks were stress-tested against maintenance capacity data and regulatory throughput to confirm feasibility and timing.

Step 4: Research Synthesis and Final Output

Insights were synthesized into actionable frameworks linking fleet programs, certification readiness, and supply chain resilience. Scenario narratives were constructed around retrofit cadence, modular kit adoption, and sustainable material qualification. Outputs were standardized for comparability across aircraft types and installation channels.

- Executive Summary

- Research Methodology (Market Definitions and cabin interior scope delineation, OEM and Tier-1 shipment tracking for seats, galleys, lavatories and monuments, Airline fleet retrofit and linefit procurement surveys, FAA certification filings and STC approvals analysis, MRO installation capacity mapping and labor rate benchmarking, Supplier contract pricing and backlog triangulation, Import-export and customs data analysis for cabin components)

- Definition and Scope

- Market evolution

- Usage and refurbishment pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising narrow-body fleet deliveries and cabin densification programs

Airline premiumization strategies to enhance passenger experience

Post-pandemic cabin refresh cycles and deferred retrofit recovery

Adoption of lightweight composite interiors to reduce fuel burn

IFEC and connectivity upgrades to meet passenger expectations

Brand differentiation through customized cabin design - Challenges

Long FAA certification timelines for new interior components

Supply chain disruptions and long lead times for certified materials

High capital intensity and tooling costs for Tier-1 suppliers

Aircraft grounding and delivery delays impacting linefit demand

Labor shortages at MROs delaying retrofit schedules

Price pressure from airlines amid tight operating margins - Opportunities

Fleet-wide cabin retrofits for connectivity and seat upgrades

Sustainable materials and recyclable cabin components adoption

Growth in premium economy seat installations

Aftermarket demand from aging narrow-body fleets

Modular monuments enabling faster reconfiguration

Partnerships with airlines for co-designed cabin concepts - Trends

Lightweight seating architectures and slimline seats

Touchless lavatories and antimicrobial surface adoption

Increased personalization and mood lighting integration

Standardization of cabin monuments across fleet families

Digital cabin management systems integration

Shorter refresh cycles for high-traffic aircraft - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Product Type (in Value %)

Passenger seating systems

Galleys

Lavatories

Overhead stowage bins

Cabin monuments and partitions

In-flight entertainment and connectivity hardware

Cabin lighting and PSU - By Aircraft Type (in Value %)

Narrow-body aircraft

Wide-body aircraft

Regional jets - By Fitment Type (in Value %)

Linefit installations

Retrofit and refurbishment - By Cabin Class (in Value %)

Economy class

Premium economy

Business class

First class - By Material and Finish (in Value %)

Composites and thermoplastics

Aluminum alloys

Textiles and foams

Leather and synthetic upholstery

Decor laminates and surface finishes - By Sales Channel (in Value %)

OEM direct contracts

Aftermarket and MRO channels

Distributor-led sales

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product portfolio breadth, certification depth and STC portfolio, installed base across US fleets, delivery lead times, customization and design capability, pricing competitiveness, aftermarket service network, sustainability and materials roadmap)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarketing

- Detailed Profiles of Major Companies

Safran Seats USA

Collins Aerospace Interiors

Adient Aerospace

Recaro Aircraft Seating

Zodiac Aerospace (Safran Cabin)

Jamco America

Diehl Aviation

Thompson Aero Seating

Haeco Cabin Solutions

B/E Aerospace (Collins Aerospace)

Astronics Corporation

Aviointeriors

Acro Aircraft Seating

Aim Altitude

Lufthansa Technik

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now