Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US military rotorcraft market, based on a recent historical assessment, is projected to reach USD ~ billion, driven by consistent investments in modernizing military fleets. A significant part of this growth comes from the increasing demand for versatile, multi-role rotorcraft, critical for various defense operations, including transport, surveillance, and combat. Additionally, technological advancements in rotorcraft design, propulsion systems, and avionics play a central role in driving the market, ensuring enhanced performance and operational efficiency.

The market remains predominantly driven by the US, where military rotorcraft demand is fueled by high defense spending and strategic military needs across various regions. Cities like Washington, D.C., and military bases across the country continue to lead the market due to their central roles in defense operations and technology development. This dominance is supported by a robust defense procurement process and extensive governmental funding aimed at maintaining technological superiority in military aviation.

Market Segmentation

By Product Type

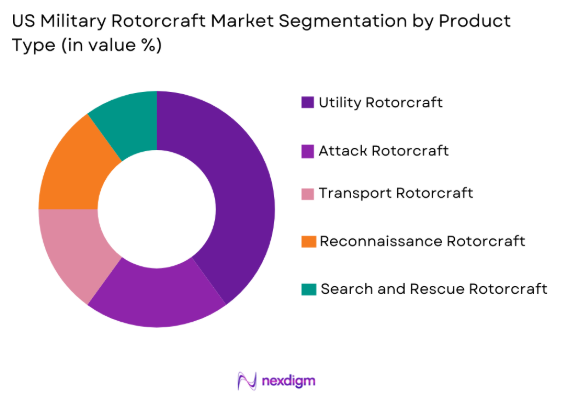

The US military rotorcraft market is segmented by product type into utility, attack, transport, reconnaissance, and search and rescue rotorcraft. Recently, transport rotorcraft had a dominant market share due to factors such as the increasing need for versatile, heavy-lift helicopters capable of performing multiple roles in diverse operational environments. This segment benefits the military’s focus on enhancing logistical capabilities, especially in regions with challenging terrain and harsh conditions. Additionally, transport rotorcraft is essential in amphibious operations, quick troop deployment, and humanitarian assistance, which further reinforces their dominance.

By Platform Type

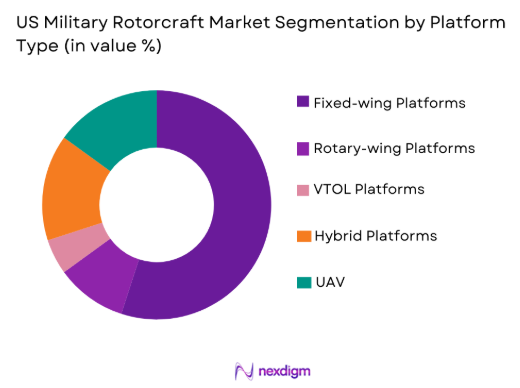

The US military rotorcraft market is segmented by platform type into fixed-wing platforms, rotary-wing platforms, vertical take-off and landing (VTOL) platforms, hybrid platforms, and unmanned aerial vehicles (UAV). Recently, rotary-wing platforms have a dominant market share due to the growing need for highly maneuverable aircraft capable of operating in confined spaces and providing quick-response capabilities in dynamic environments. These platforms are particularly favored in military operations that require versatility, such as close air support, tactical operations, and evacuation missions.

Competitive Landscape

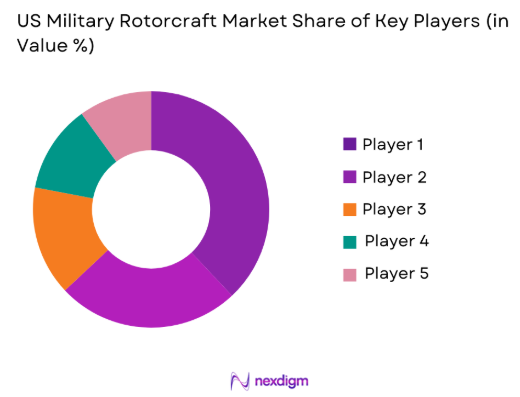

The US military rotorcraft market is characterized by a highly competitive landscape with major players contributing to market consolidation through acquisitions and technology integration. The competition is particularly fierce among OEMs and defense contractors that innovate in rotorcraft designs and systems to meet the evolving needs of the military. Companies are constantly vying for defense contracts and engaging in strategic partnerships to ensure the development of next-generation rotorcraft. Players like Sikorsky Aircraft, Boeing, and Bell Helicopter dominate the industry with their innovative designs and extensive operational experience in military applications.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Product Portfolio |

| Lockheed Martin | 1995 | Bethesda, MD | ~ | ~ | ~ | ~ | ~ |

| Sikorsky Aircraft | 1923 | Stratford, CT | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, IL | ~ | ~ | ~ | ~ | ~ |

| Bell Helicopter | 1935 | Fort Worth, TX | ~ | ~ | ~ | ~ | ~ |

| Airbus Helicopters | 1992 | Marignane, France | ~ | ~ | ~ | ~ | ~ |

US Military Rotorcraft Market Analysis

Growth Drivers

Increasing Demand for Multi-role Rotorcraft

The US military is emphasizing the acquisition of multi-role rotorcraft that can perform a wide range of missions, including troop transport, logistics, surveillance, and reconnaissance. This demand is driven by the increasing complexity of modern warfare, where versatility and adaptability are critical for operational success. Rotorcraft that can operate in a variety of environments, such as mountainous, desert, and urban terrains, are becoming essential assets for the military. These platforms are particularly valuable in special operations and rapid response missions, which require flexibility and quick adaptation to evolving battlefield conditions. Additionally, rotorcraft play a crucial role in humanitarian and disaster relief operations, where their ability to reach remote areas and deliver aid is indispensable. The demand for multi-role rotorcraft is thus expected to continue rising, with various defense contracts supporting the growth of this segment.

Technological Advancements in Rotorcraft Design

The integration of advanced technologies in rotorcraft design is another key growth driver in the market. Innovations in propulsion systems, avionics, and materials science are significantly improving rotorcraft performance, reliability, and operational efficiency. For example, the development of hybrid-electric propulsion systems and the use of composite materials are reducing the weight of rotorcraft, leading to improved fuel efficiency and greater payload capacity. Furthermore, advancements in autopilot and autonomous flight systems are increasing rotorcraft safety and mission efficiency, particularly in complex combat environments. The US military’s focus on modernization and technological superiority is driving demand for next-generation rotorcraft equipped with state-of-the-art systems. These technological advancements are expected to enhance rotorcraft capabilities, making them more effective in multi-domain operations, thereby fueling market growth.

Market Challenges

High Development and Procurement Costs

One of the primary challenges facing the US military rotorcraft market is the high cost associated with developing and procuring advanced rotorcraft systems. The development of next-generation rotorcraft requires significant investments in research, testing, and certification processes, which can strain defense budgets. Additionally, the procurement costs for these aircraft are often substantial, especially for specialized military platforms equipped with cutting-edge technologies. Budgetary constraints and the need to allocate funds across various defense programs can limit the ability of the military to acquire the required number of rotorcraft. This challenge is particularly acute for the procurement of advanced rotorcraft platforms, which involve long development cycles and high manufacturing costs. These financial hurdles are a significant obstacle to the growth of the market, as they restrict the ability of defense agencies to modernize their fleets as quickly as needed.

Regulatory and Certification Hurdles

The US military rotorcraft market is also challenged by the complex regulatory and certification requirements that govern the design, production, and deployment of military rotorcraft. The Federal Aviation Administration (FAA) and other regulatory bodies impose strict guidelines on rotorcraft safety, environmental impact, and airworthiness, which can delay the development and approval of new platforms. These regulatory hurdles are compounded by the need for military rotorcraft to meet specific defense standards, which vary depending on the operational role and environment in which the aircraft will be deployed. Compliance with these regulations requires additional testing, modification, and certification processes, leading to increased time and costs for manufacturers. Moreover, the evolving nature of regulatory frameworks poses ongoing challenges for rotorcraft manufacturers, who must adapt to new standards and ensure their products meet all necessary criteria for military operations.

Opportunities

Emerging Demand for Autonomous Rotorcraft

The integration of autonomous technologies in rotorcraft presents a significant opportunity for the US military rotorcraft market. Autonomous rotorcraft, capable of operating without human intervention or with minimal pilot oversight, offer numerous advantages in terms of operational efficiency, safety, and cost savings. These systems are particularly valuable in high-risk environments, such as combat zones or areas with challenging terrain, where they can perform missions with reduced risk to human life. Autonomous rotorcraft can also operate in environments where human pilots may face physical limitations, such as extreme weather conditions or prolonged flight durations. The military is increasingly investing in unmanned and autonomous rotorcraft to enhance reconnaissance capabilities, surveillance operations, and logistics support. The development of these technologies is expected to revolutionize the rotorcraft market, opening new avenues for innovation and growth.

Integration of Hybrid Propulsion Systems

The growing demand for environmentally sustainable and fuel-efficient rotorcraft presents an opportunity for the integration of hybrid propulsion systems in military rotorcraft. Hybrid systems, which combine conventional turbine engines with electric propulsion, offer significant advantages in terms of reduced fuel consumption and lower emissions. These systems can extend the operational range of rotorcraft while also reducing their dependence on fossil fuels. Additionally, hybrid systems can provide greater flexibility in mission planning, allowing rotorcraft to operate in both urban and remote environments with reduced environmental impact. The US military’s focus on sustainability and energy efficiency is driving interest in hybrid propulsion technologies for rotorcraft. As these technologies mature, they are expected to become an integral part of the next generation of military rotorcraft, providing a competitive edge in both operational performance and environmental responsibility.

Future Outlook

The future outlook for the US military rotorcraft market over the next five years shows promising growth driven by advancements in rotorcraft technology, increased defense spending, and the growing demand for versatile, multi-role aircraft. Technological developments, such as autonomous flight systems, hybrid propulsion, and advanced avionics, are expected to enhance rotorcraft performance and mission capabilities. Regulatory support and government funding will continue to bolster the market, while the increasing complexity of modern warfare will drive the need for highly adaptable rotorcraft capable of meeting a variety of operational requirements. Additionally, the rising geopolitical tensions and focus on military modernization will ensure sustained demand for rotorcraft across various defense sectors.

Major Players

- Lockheed Martin

- Sikorsky Aircraft

- Boeing

- Bell Helicopter

- Airbus Helicopters

- Northrop Grumman

- Leonardo

- Thales Group

- Textron Aviation

- Raytheon Technologies

- General Electric

- Honeywell Aerospace

- L3 Technologies

- Rockwell Collins

- Saab Group

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense contractors

- Aerospace manufacturers

- Military forces

- Security and defense agencies

- Aviation technology developers

- Rotorcraft maintenance service providers

Research Methodology

Step 1: Identification of Key Variables

The research identifies critical variables, including market drivers, technological trends, regulatory frameworks, and key players that influence market dynamics.

Step 2: Market Analysis and Construction

An in-depth analysis is conducted using primary and secondary data, focusing on market size, growth trends, segmentation, and competition.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert consultations, including interviews with industry professionals and stakeholders in defense and aviation sectors.

Step 4: Research Synthesis and Final Output

The research is synthesized into a final output, presenting key findings, conclusions, and recommendations based on the analyzed data.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Defense Spending in the US

Rising Demand for Versatile and Multi-role Rotorcraft

Technological Advancements in Rotorcraft Systems

Geopolitical Tensions Driving Military Modernization

Integration of Commercial Technologies into Defense Systems - Market Challenges

High Development and Procurement Costs

Regulatory Compliance and Certification Barriers

Technological Integration and Interoperability Issues

Maintenance and Lifecycle Management Costs

Environmental and Sustainability Concerns - Market Opportunities

Emerging Demand for Autonomous Rotorcraft

Expansion of Public-Private Partnerships for Rotorcraft Innovation

Adoption of AI and Machine Learning for Rotorcraft Optimization - Trends

Increasing Use of Advanced Rotorcraft Technologies

Integration of Autonomous Flight Systems in Military Operations

Shift Toward Multi-role and Modular Rotorcraft Designs

Surge in Cybersecurity Investments for Rotorcraft Systems

Focus on Green and Sustainable Rotorcraft Technologies - Government Regulations & Defense Policy

National Defense Authorization Act (NDAA) for Rotorcraft

FAA Certification and Safety Standards for Military Rotorcraft

Incentives for Advanced Rotorcraft Development under Defense Innovation Programs

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility Rotorcraft

Attack Rotorcraft

Transport Rotorcraft

Reconnaissance Rotorcraft

Search and Rescue Rotorcraft - By Platform Type (In Value%)

Fixed Wing Platforms

Rotary Wing Platforms

Vertical Take-Off and Landing (VTOL) Platforms

Hybrid Platforms

Unmanned Aerial Vehicles (UAV) - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions

Modular Solutions - By End User Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (In Value%)

Carbon Fiber Composites

Advanced Turbine Engines

Hybrid Propulsion Systems

Autonomous Control Systems

Enhanced Avionics Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Material / Technology, Pricing Strategy, Technology Integration, Regulatory Compliance, Innovation Rate)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Lockheed Martin

Sikorsky Aircraft

Boeing

Bell Helicopter

Northrop Grumman

Airbus Helicopters

Textron Aviation

General Electric

Honeywell Aerospace

Raytheon Technologies

Leonardo

Thales Group

SAAB Group

L3 Technologies

Rockwell Collins

- Military Forces’ Increasing Demand for Versatile Aircraft

- Defense Contractors’ Drive for Innovation and Cost-efficiency

- Government Agencies’ Role in Procuring Advanced Systems

- Private Sector’s Growing Role in Rotorcraft Technology and Cybersecurity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now