Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US satellite attitude and orbit control system market current size stands at around USD ~ million, reflecting steady procurement of precision control subsystems across commercial, civil, and defense missions. Demand is shaped by mission-critical reliability requirements, flight heritage preferences, and integration with diverse satellite buses. Program cadence is supported by recurring constellation replenishment and technology demonstration missions, while procurement cycles emphasize qualification depth, radiation tolerance, and lifecycle support. Supplier pipelines align with domestic sourcing priorities and programmatic continuity across multiyear mission portfolios.

The market shows strong concentration across established aerospace clusters in California, Colorado, Texas, and Florida, supported by dense integrator ecosystems, testing infrastructure, and proximity to launch services. Demand concentrates around mission control centers and spacecraft manufacturing hubs with mature supplier networks. Policy emphasis on space domain awareness and national security missions reinforces sustained procurement. State-level incentives, workforce depth, and co-location with propulsion, avionics, and payload suppliers accelerate integration timelines and ecosystem maturity across these regional clusters.

Market Segmentation

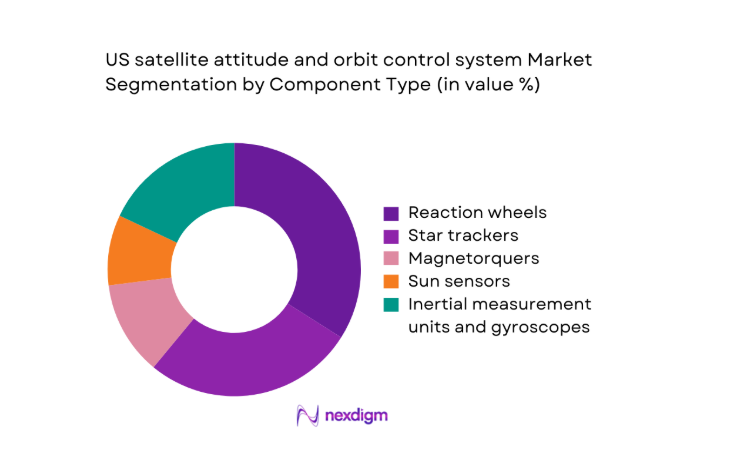

By Component Type

Demand concentration is highest for precision sensors and actuators that directly influence pointing accuracy and stability across imaging and communications payloads. Reaction wheels and star trackers dominate mission-critical configurations due to reliability requirements and flight heritage preferences, while magnetorquers and sun sensors support detumbling and coarse pointing for small platforms. Integration trends favor modular component stacks to simplify qualification across satellite buses. Thrusters increasingly complement attitude control in agile missions, reflecting tighter coupling between guidance software and hardware. Procurement emphasizes radiation tolerance, redundancy options, and compatibility with standardized avionics interfaces to reduce integration risk.

By Orbit Regime

Low Earth orbit dominates deployments due to high launch cadence and constellation replenishment cycles, driving volume demand for compact, power-efficient control subsystems. Medium Earth orbit supports navigation missions requiring sustained pointing stability and thermal resilience. Geostationary orbit emphasizes long-life reliability and redundancy, shaping procurement toward proven architectures. Cislunar and deep space missions drive demand for advanced control algorithms, higher radiation tolerance, and fault management capabilities. Orbit-specific environmental exposure shapes component selection, qualification depth, and redundancy strategies, influencing procurement cycles and supplier qualification pathways across mission classes.

Competitive Landscape

Competition is shaped by flight heritage, qualification depth, and integration support across diverse satellite buses. Buyers prioritize reliability, delivery certainty, and technical support for mission assurance. Supplier differentiation centers on component performance, radiation tolerance, software compatibility, and production scalability to meet constellation schedules.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Blue Canyon Technologies | 2008 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Honeywell Aerospace | 1906 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Ball Aerospace | 1956 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| L3Harris Technologies | 2019 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

US satellite attitude and orbit control system Market Analysis

Growth Drivers

Rising LEO constellation deployments for broadband and EO

Launch cadence accelerated with 184 missions conducted across domestic spaceports during 2024 and 2025, increasing annual spacecraft integration throughput. Satellite manufacturing lines expanded floor space by 42 facilities nationwide, improving parallel assembly rates. Mission manifests show 96 distinct broadband and imaging payload programs entering integration between 2024 and 2025, elevating demand for compact control subsystems with rapid qualification. Federal licensing approvals reached 2,841 spacecraft authorizations across 2024 and 2025, sustaining deployment momentum. Ground segment expansion added 318 gateway antennas, tightening pointing accuracy requirements for crosslink stability. Workforce certifications for spacecraft assembly increased by 1,740 technicians, supporting higher production tempo and consistent subsystem integration across programs.

Increased national security and space domain awareness missions

National security launch allocations increased to 14 missions across 2024 and 2025, expanding deployment of surveillance and resilient communications platforms requiring high pointing stability. Defense program line items funded 27 new spacecraft development efforts during 2024 and 2025, elevating demand for fault-tolerant control architectures. Space domain awareness operations expanded tracking coverage to 47 additional sensors nationwide, raising requirements for precise attitude control to support high-resolution sensing payloads. Secure command-and-control terminals increased by 132 sites, tightening link budgets and control precision needs. Mission assurance protocols mandated 2 redundant control chains for critical platforms, raising subsystem integration depth. Qualification cycles extended across 180 environmental test campaigns, reinforcing reliability-driven procurement patterns.

Challenges

Radiation tolerance and reliability constraints in space environments

On-orbit anomaly reports logged 214 control subsystem faults across 2024 and 2025, with 61 linked to radiation-induced single-event effects. Solar activity cycles recorded 2 significant geomagnetic storm periods during the timeframe, increasing component stress exposure. Test facilities conducted 389 radiation campaigns to validate component hardening, extending qualification timelines. Failure investigations required 78 corrective action programs, delaying integration schedules. Thermal vacuum chambers operated at 92 utilization days annually, constraining test throughput. Redundancy mandates added 2 parallel control paths for critical missions, increasing integration complexity. Component redesign cycles averaged 14 months following anomaly resolution, stretching development schedules and elevating engineering resource loads across programs.

Export control and ITAR compliance limiting supplier choices

Licensing reviews processed 1,126 technical assistance agreements across 2024 and 2025, extending procurement lead times. Compliance audits increased to 63 inspections annually, diverting engineering resources from development. Program schedules absorbed 41 documented export review delays, affecting subsystem delivery sequencing. Cross-border component sourcing required 118 jurisdiction determinations, narrowing supplier pools. Secure data environments expanded to 29 facilities to meet compliance requirements, raising operational overhead. Training certifications for export compliance reached 3,402 personnel, reflecting administrative burden. Contractual amendments addressing jurisdiction constraints totaled 96 actions, complicating integration planning and limiting rapid substitution of qualified components for time-sensitive missions.

Opportunities

Adoption of AI-enabled guidance, navigation, and control software

Flight software updates incorporating onboard autonomy were validated across 24 demonstration missions during 2024 and 2025, improving disturbance rejection performance. Onboard compute capability expanded to 128 TOPS across selected platforms, enabling real-time control optimization. Fault detection libraries logged 6,412 anomaly classifications during ground simulations, reducing operator intervention cycles. Closed-loop control tuning reduced slew stabilization windows by 38 seconds per maneuver in test campaigns. Digital twin environments expanded across 17 integration centers, accelerating validation cycles. Secure uplink update mechanisms were certified across 9 mission profiles, enabling iterative control logic enhancements. Workforce training for autonomy modules reached 812 engineers, building deployment readiness across integrator teams.

Demand for agile and high-torque AOCS in ISR missions

ISR mission profiles expanded across 31 new spacecraft programs during 2024 and 2025, requiring rapid retargeting and high-torque actuation. Slew rate requirements tightened to 12 degrees per second for time-sensitive imaging, driving actuator performance thresholds. On-orbit tasking windows increased to 9 daily passes per platform, compressing stabilization timelines. Sensor payload mass increased by 18 kilograms on average, raising torque demands for attitude stabilization. Ground tasking queues processed 4,260 retargeting commands monthly, necessitating responsive control loops. Multi-target tracking scenarios increased by 22 mission sets, reinforcing demand for precision pointing and rapid maneuvering under constrained power budgets.

Future Outlook

The outlook through 2035 reflects sustained deployment of small satellite constellations alongside more complex national security missions. Advances in onboard autonomy, tighter integration with propulsion, and modular control architectures will shape procurement strategies. Domestic supply chain strengthening and qualification depth will remain decisive. Cislunar missions and proximity operations will further elevate performance expectations and reliability requirements.

Major Players

- Blue Canyon Technologies

- Honeywell Aerospace

- Ball Aerospace

- Northrop Grumman

- Lockheed Martin Space

- L3Harris Technologies

- Moog Inc.

- AAC Clyde Space

- Rocket Lab Space Systems

- York Space Systems

- Kearfott Corporation

- BAE Systems

- Collins Aerospace

- Sierra Space

- Airbus U.S. Space & Defense

Key Target Audience

- Commercial satellite operators

- Defense acquisition organizations

- National security space program offices

- Government and regulatory bodies with agency names

- Launch service providers

- Satellite bus manufacturers and integrators

- Space insurance and risk underwriting firms

- Investments and venture capital firms

Research Methodology

Step 1: Identification of Key Variables

Program pipelines, mission profiles, component qualification depth, and integration constraints were mapped to define demand drivers and technical thresholds. Regulatory compliance requirements, domestic sourcing preferences, and test infrastructure availability were identified as structural variables influencing procurement pathways.

Step 2: Market Analysis and Construction

Mission cadence, licensing throughput, manufacturing capacity indicators, and integration center utilization were analyzed to construct demand scenarios. Technology readiness levels, qualification cycles, and supply chain resilience indicators were incorporated to frame capability constraints and adoption timelines.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through structured consultations with systems engineers, program managers, and mission assurance leads. Test campaign outputs, anomaly logs, and qualification records were reviewed to triangulate performance thresholds and reliability expectations.

Step 4: Research Synthesis and Final Output

Insights were synthesized into coherent market narratives aligned to mission pathways, regulatory constraints, and technology evolution. Scenario framing emphasized deployment tempo, qualification bottlenecks, and adoption readiness for advanced control architectures.

- Executive Summary

- Research Methodology (Market Definitions and AOCS subsystem boundaries, Primary interviews with US satellite OEMs and integrators, Analysis of DoD and NASA program budgets and solicitations, Review of FCC filings and spacecraft licensing data, Teardown and bill of materials analysis of AOCS components, Satellite launch and on-orbit fleet tracking, Pricing triangulation from supplier quotes and contract awards)

- Definition and Scope

- Market evolution

- Mission and application pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory and export control environment

- Growth Drivers

Rising LEO constellation deployments for broadband and EO

Increased national security and space domain awareness missions

Miniaturization and COTS adoption for small satellites

Higher pointing accuracy requirements for high-resolution payloads

Increased launch cadence and rideshare availability

Growth in on-orbit servicing and proximity operations - Challenges

Radiation tolerance and reliability constraints in space environments

Export control and ITAR compliance limiting supplier choices

Supply chain fragility for precision electromechanical components

Thermal management and vibration issues in compact platforms

Qualification and testing costs for space-rated AOCS hardware

Integration complexity across heterogeneous satellite buses - Opportunities

Adoption of AI-enabled guidance, navigation, and control software

Demand for agile and high-torque AOCS in ISR missions

Growth of lunar and cislunar missions requiring advanced control

In-orbit servicing, docking, and formation flying systems

Dual-use components for commercial and defense programs

Domestic sourcing incentives and reshoring of critical components - Trends

Shift toward modular, software-defined AOCS architectures

Proliferation of micro reaction wheels for smallsat constellations

Integration of electric propulsion for combined attitude and orbit control

Use of high-precision star trackers for SAR and optical payloads

Increased use of redundancy and fault-tolerant designs

Standardization of interfaces across satellite bus platforms - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Shipment Volume, 2020–2025

- By Active Systems, 2020–2025

- By Average Selling Price, 2020–2025

- By Component Type (in Value %)

Reaction wheels

Control moment gyros

Magnetorquers

Star trackers

Inertial measurement units and gyroscopes

Sun sensors

Thrusters for attitude control - By Satellite Class (in Value %)

Nanosatellites and CubeSats

Microsatellites

Minisatellites

Large satellites and spacecraft - By Orbit Regime (in Value %)

Low Earth orbit

Medium Earth orbit

Geostationary orbit

Cislunar and deep space - By Mission Application (in Value %)

Earth observation and remote sensing

Communications and broadband

Navigation and PNT

Technology demonstration

Science and exploration

National security and defense - By End User Sector (in Value %)

Commercial operators

Civil government and space agencies

Defense and intelligence

Academic and research institutions

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product performance and pointing accuracy, Radiation tolerance and reliability, Mass and power efficiency, Customization and integration support, Qualification heritage and flight heritage, Production scalability and lead times, Pricing and contract flexibility, After-sales and on-orbit support)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Blue Canyon Technologies

Honeywell Aerospace

Ball Aerospace

Northrop Grumman

Lockheed Martin Space

L3Harris Technologies

Moog Inc.

AAC Clyde Space

Rocket Lab Space Systems

York Space Systems

Kearfott Corporation

BAE Systems

Collins Aerospace

Sierra Space

Airbus U.S. Space & Defense

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service and in-orbit support expectations

- By Value, 2026–2035

- By Shipment Volume, 2026–2035

- By Active Systems, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now