Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US satellite bus market current size stands at around USD ~ million, reflecting sustained procurement momentum across defense, civil, and commercial missions. Demand is supported by multi-orbit platform programs, modular bus architectures, and domestic manufacturing priorities. Supply chain localization, qualification cycles for radiation-tolerant components, and vertically integrated assembly lines continue to shape delivery cadence. Platform standardization is improving throughput, while customization remains critical for high-power payloads and resilient mission profiles.

Activity concentrates in established aerospace corridors with dense supplier networks, skilled labor pools, and proximity to launch and test infrastructure. Federal contracting hubs anchor demand through program offices and integration facilities, while commercial constellation operators cluster near manufacturing campuses and mission operations centers. Mature testing ecosystems, export compliance capabilities, and policy alignment with domestic sourcing reinforce regional leadership. Local incentives and streamlined permitting further support production scale-up and rapid iteration.

Market Segmentation

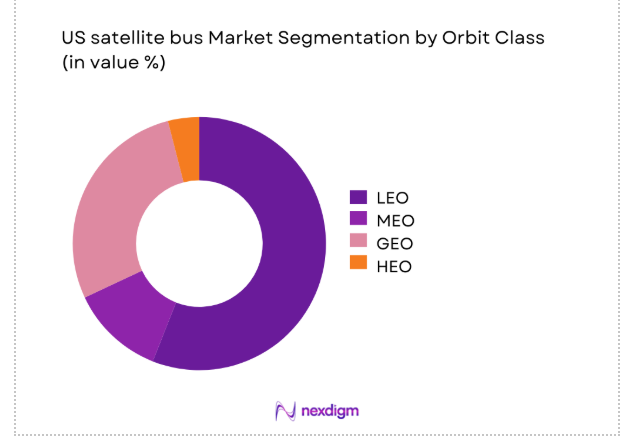

By Orbit Class

LEO platforms dominate deployments due to constellation architectures prioritizing low latency, rapid refresh cycles, and standardized production. Manufacturers have optimized assembly lines for frequent cadence, enabling faster qualification and integration of avionics, power systems, and thermal subsystems. MEO programs remain mission-specific, balancing coverage and lifecycle requirements for navigation and data relay. GEO buses retain importance for high-power communications and protected missions, requiring bespoke structures, propulsion redundancy, and long-life components. The mix reflects operational trade-offs across latency, coverage, radiation exposure, and servicing feasibility, with procurement favoring architectures that minimize lead times while preserving mission resilience and lifecycle reliability.

By Satellite Mass Class

Small satellite platforms lead volume-driven procurement as standardized buses support rapid constellation deployment and frequent technology refresh. Manufacturers emphasize modular frames, software-defined avionics, and scalable power architectures to compress timelines and enable batch production. Medium-class buses serve dual-use missions requiring higher payload mass and longer operational life, often integrating electric propulsion and enhanced thermal control. Large platforms remain critical for high-throughput communications and protected payloads, demanding bespoke structures, redundancy, and long-life components. The segmentation reflects lifecycle economics, integration complexity, and mission assurance priorities across civil, defense, and commercial programs seeking predictable delivery and maintainability.

Competitive Landscape

The competitive environment features vertically integrated manufacturers alongside agile platform specialists focused on modularity and production scalability. Differentiation centers on cadence reliability, qualification depth, supply chain control, and mission assurance credentials aligned with domestic compliance requirements.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Lockheed Martin | 1912 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Boeing Defense, Space & Security | 1916 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| L3Harris Technologies | 2019 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Maxar Technologies | 1969 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

US satellite bus Market Analysis

Growth Drivers

Proliferation of LEO constellations for broadband and ISR

Federal licensing actions in 2024 authorized 12 new non-geostationary deployments, accelerating platform orders for multi-orbit architectures. Launch cadence increased with 92 orbital insertions recorded across domestic providers during 2025, expanding integration throughput. Mission assurance requirements cite 3 redundancy layers across power and avionics for ISR payloads, raising bus complexity and unit configuration diversity. Manufacturing facilities expanded floor space by 180000 square feet in 2024 to accommodate parallel assembly lines. Workforce additions reached 1400 engineers across propulsion, structures, and thermal disciplines in 2025. Export compliance certifications cleared 7 production sites for secure integration, supporting sustained constellation deployment tempo.

Rising US defense spending on resilient space architectures

Defense program guidance in 2024 mandated proliferated architectures across 4 orbital regimes, increasing bus variants supporting cross-link networking and rapid reconstitution. Secure communications upgrades in 2025 specified 2 independent command paths per platform to enhance resilience. Ground segment modernization included 36 new mission terminals enabling higher tasking rates, driving demand for software-defined avionics. Test infrastructure added 5 thermal vacuum chambers nationwide during 2024, compressing qualification cycles. Security accreditation timelines shortened by 90 days through streamlined compliance workflows in 2025, enabling faster production ramp and fielding of resilient platforms aligned with operational requirements.

Challenges

Supply chain constraints in radiation-hardened electronics

Qualification bottlenecks persisted in 2024 as 14 component families faced extended lot acceptance testing due to radiation tolerance thresholds. Lead times for single-event upset screened processors reached 52 weeks in 2025, disrupting synchronized assembly schedules. Domestic foundry capacity allocated 3 fabrication lines to space-grade runs, limiting batch flexibility. Environmental screening throughput averaged 240 units per month across certified labs, below integration demand. Failure analysis backlogs rose to 210 cases in 2024, delaying corrective actions. Logistics constraints included 9 restricted materials subject to compliance reviews, extending inbound processing and inventory buffers for avionics and power management modules.

High non-recurring engineering costs for customized bus designs

Program offices in 2024 reported 18 bespoke interface requirements per mission, increasing configuration management complexity. Structural qualification campaigns required 220 unique load cases per platform variant in 2025, extending analysis cycles. Thermal modeling incorporated 6 orbital seasons per mission profile, increasing simulation runs and validation loops. Software baselines expanded to 24 configuration branches to support payload diversity, complicating verification. Configuration control boards processed 310 change requests during 2024, slowing production gating. Integration teams logged 480 rework hours per vehicle due to late-stage customization, constraining throughput and elevating schedule risk across multi-mission production lines.

Opportunities

Modular and scalable bus architectures for constellation deployment

Standardized frames adopted in 2024 supported 8 payload interface configurations, enabling rapid changeovers without structural redesign. Common avionics backplanes validated 16 peripheral modules in 2025, reducing qualification cycles across missions. Production takt time improved to 9 days per unit through modular kitting and pre-certified harness sets. Digital twins synchronized 1200 component parameters per platform, improving first-pass yield. Multi-orbit adaptability was proven across 4 environmental envelopes, enabling reuse across mission profiles. Quality metrics recorded 2 nonconformities per 100 assemblies in 2025, supporting scalable cadence for constellation-grade production without compromising mission assurance.

On-orbit servicing and refueling-compatible bus designs

Docking interface standards validated in 2024 across 5 mechanical profiles, enabling cross-platform servicing compatibility. Propellant management subsystems tested 3 transfer protocols in 2025, improving in-orbit refueling safety. Avionics upgrades supported 2 fault-tolerant rendezvous modes, expanding servicing mission envelopes. Structural hardpoints qualified for 12 capture loads, enabling tug-assisted repositioning. Ground simulations executed 48 servicing scenarios per mission class, improving readiness. Debris mitigation compliance included 25 deorbit planning parameters integrated into bus firmware, aligning designs with sustainability mandates and enabling life-extension missions that reduce replacement cycles.

Future Outlook

The market outlook through 2035 reflects sustained momentum from proliferated architectures, resilient mission design, and domestic manufacturing scale-up. Policy alignment, standardized platforms, and servicing-ready designs will reshape procurement preferences. Integration throughput and workforce depth remain decisive for cadence reliability. Ecosystem maturity and compliance readiness will determine supplier selection as mission complexity increases.

Major Players

- Lockheed Martin

- Northrop Grumman

- Boeing Defense, Space & Security

- L3Harris Technologies

- Maxar Technologies

- Ball Aerospace

- York Space Systems

- Terran Orbital

- Millennium Space Systems

- Sierra Space

- Rocket Lab

- Blue Origin

- Raytheon Technologies

- General Atomics

- Aerojet Rocketdyne

Key Target Audience

- Commercial satellite constellation operators

- Defense acquisition program offices

- Civil space agencies and mission directorates

- Prime system integrators

- Payload and subsystem suppliers

- Launch service providers

- Investments and venture capital firms

- Government and regulatory bodies with agency names

Research Methodology

Step 1: Identification of Key Variables

Platform classes, orbit regimes, propulsion architectures, qualification standards, and compliance requirements were mapped to mission profiles. Supplier capacity, integration cadence, and test infrastructure availability were defined as core variables. Risk vectors across electronics qualification and export compliance were included to bound operational feasibility.

Step 2: Market Analysis and Construction

Demand drivers were structured by mission class and procurement pathways. Production workflows were decomposed across structures, avionics, power, thermal, and propulsion to identify bottlenecks. Ecosystem linkages between suppliers, integrators, and testing facilities were modeled to reflect throughput constraints.

Step 3: Hypothesis Validation and Expert Consultation

Operational assumptions were stress-tested against manufacturing cadence, qualification cycles, and compliance workflows. Program-level process maps were validated through practitioner feedback. Sensitivities across modularity, servicing interfaces, and production scaling were iteratively refined.

Step 4: Research Synthesis and Final Output

Findings were consolidated into decision-oriented insights aligned with procurement, operations, and ecosystem readiness. Cross-functional dependencies were reconciled to ensure internal consistency. Implications for platform standardization and servicing readiness were translated into actionable strategic considerations.

- Executive Summary

- Research Methodology (Market Definitions and satellite bus platform classifications, OEM and integrator interviews across LEO/MEO/GEO programs, US government and commercial satellite procurement tracking, payload-agnostic bus cost and BOM modeling, supplier capacity and backlog assessment, program-level contract and launch manifest analysis)

- Definition and Scope

- Market evolution

- Usage and mission pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Proliferation of LEO constellations for broadband and ISR

Rising US defense spending on resilient space architectures

Commercial demand for high-throughput and low-latency satellites

Rapid miniaturization and standardized smallsat platforms

Increased cadence of launch services enabling faster refresh cycles

Growing private capital and venture funding in space manufacturing - Challenges

Supply chain constraints in radiation-hardened electronics

High non-recurring engineering costs for customized bus designs

Export controls and ITAR-related compliance burdens

Launch schedule volatility and manifest delays

Thermal and power management limits for high-density payloads

Workforce shortages in aerospace manufacturing and systems engineering - Opportunities

Modular and scalable bus architectures for constellation deployment

On-orbit servicing and refueling-compatible bus designs

Dual-use platforms for civil and defense missions

Vertical integration between bus OEMs and constellation operators

Domestic sourcing of critical components to reduce dependencies

Rapid prototyping and digital twin adoption for faster qualification - Trends

Shift toward standardized smallsat and ESPA-class buses

Adoption of electric propulsion for station-keeping and orbit raising

Increased use of software-defined avionics and autonomy

Radiation-tolerant COTS components in LEO missions

Mass production lines for constellation-grade buses

Design for in-orbit upgradeability and servicing interfaces - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Shipment Volume, 2020–2025

- By Active Systems, 2020–2025

- By Average Selling Price, 2020–2025

- By Orbit Class (in Value %)

LEO

MEO

GEO

HEO - By Satellite Mass Class (in Value %)

Nano and Pico satellites

Micro satellites

Small satellites

Medium satellites

Large satellites - By Mission Application (in Value %)

Earth observation and remote sensing

Communications and broadband

Navigation and timing

Scientific and exploration

Technology demonstration and in-orbit servicing - By End User Type (in Value %)

Commercial operators

Civil government agencies

Defense and intelligence organizations

Academic and research institutions - By Propulsion Type (in Value %)

Chemical propulsion

Electric propulsion

Hybrid propulsion

Non-propulsive platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product portfolio breadth, orbit-class coverage, production scalability, unit cost competitiveness, heritage flight experience, vertical integration level, customization flexibility, delivery lead times)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Lockheed Martin

Northrop Grumman

Boeing Defense, Space & Security

L3Harris Technologies

Blue Origin

Maxar Technologies

Ball Aerospace

York Space Systems

Terran Orbital

Millennium Space Systems

Sierra Space

Rocket Lab

Aerojet Rocketdyne

Raytheon Technologies

General Atomics

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Shipment Volume, 2026–2035

- By Active Systems, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now