Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US Satellite Manufacturing and Launch Systems market is valued at approximately USD ~ billion based on a recent historical assessment, supported by consolidated data from national space agencies and industry foundations. Demand is driven by expanding commercial satellite constellations, defense space modernization programs, and increasing launch cadence requirements. Government procurement of resilient space architectures and private sector investment in reusable launch vehicles are accelerating production volumes, while vertically integrated providers are reducing costs and improving deployment responsiveness across civil, military, and commercial missions nationwide.

Dominance within this market is concentrated in established aerospace hubs including California, Colorado, Alabama, and Florida, supported by dense supplier ecosystems and specialized launch infrastructure. California leads through integrated satellite design and private launch innovation clusters, while Florida anchors orbital launch operations due to coastal spaceports and federal facilities. Colorado hosts mission operations and component manufacturing networks, and Alabama supports propulsion engineering. These regions benefit from sustained federal contracts, skilled aerospace labor pools, advanced research institutions, and proximity to defense customers and launch ranges.

Market Segmentation

By Product Type

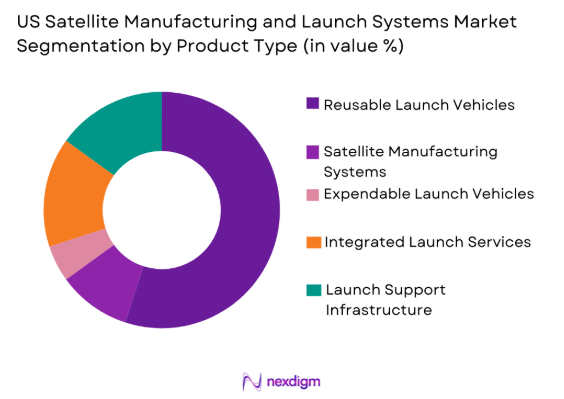

US Satellite Manufacturing and Launch Systems market is segmented by product type into satellite manufacturing systems, reusable launch vehicles, expendable launch vehicles, integrated launch services, and launch support infrastructure. Recently, reusable launch vehicles has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Reusable launch vehicles dominate because operators seek lower cost per launch and higher cadence capabilities. Government missions prioritize rapid reflight capability to ensure resilient orbital access. Commercial constellation deployments require frequent launches, favoring reusable architectures. Established providers have demonstrated reliability through repeated recoveries and reflights. Launch service contracts increasingly specify partial or full reusability requirements. Manufacturing investments are shifting toward reusable booster production lines. Supply chains are optimized around refurbishment cycles rather than single use hardware. Insurance premiums decline with proven reusable flight records. Market perception associates reusability with technological leadership and operational efficiency.

By Platform Type

US Satellite Manufacturing and Launch Systems market is segmented by platform type into low Earth orbit platforms, geostationary orbit platforms, medium Earth orbit platforms, deep space platforms, and responsive launch platforms. Recently, low Earth orbit platforms has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Low Earth orbit platforms dominate due to massive broadband constellation deployment requirements. Earth observation and analytics services rely primarily on low altitude satellites. Defense surveillance architectures increasingly shift toward proliferated low Earth orbit layers. Launch providers optimize vehicles for smaller payloads targeting low Earth trajectories. Manufacturing lines standardize satellite buses for low Earth constellations. Investors favor scalable constellation business models centered on low Earth orbit. Insurance and mission risk profiles are lower compared with higher orbits. Regulatory approvals are streamlined for low Earth deployments. Market momentum reinforces continued concentration in low Earth platform manufacturing and launches.

Competitive Landscape

The US Satellite Manufacturing and Launch Systems market is moderately consolidated, led by vertically integrated aerospace primes and disruptive commercial launch entrants. Major firms control end to end capabilities spanning satellite design, propulsion, launch vehicles, and mission services, creating high entry barriers. Long term government contracts reinforce incumbent dominance, while private capital has enabled emerging launch providers to scale manufacturing and flight cadence. Competitive differentiation centers on reusability maturity, payload integration flexibility, and assured launch availability across civil, defense, and commercial missions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Launch Reusability Capability |

| SpaceX | 2002 | Hawthorne USA | ~ | ~ | ~ | ~ | ~ |

| United Launch Alliance | 2006 | Centennial USA | ~ | ~ | ~ | ~ | ~ |

| Blue Origin | 2000 | Kent USA | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church USA | ~ | ~ | ~ | ~ | ~ |

| Rocket Lab USA | 2006 | Long Beach USA | ~ | ~ | ~ | ~ | ~ |

US Satellite Manufacturing and Launch Systems Market Analysis

Growth Drivers

Commercial Satellite Constellation Expansion

Commercial Satellite Constellation Expansion is transforming the US Satellite Manufacturing and Launch Systems market by driving unprecedented production and launch cadence requirements across broadband, Earth observation, and connectivity services. Operators are deploying hundreds of satellites annually to build global coverage networks. Manufacturing facilities are shifting toward mass production lines rather than bespoke spacecraft assembly. Launch providers are adapting vehicles for frequent constellation deployment missions. Investors are prioritizing scalable constellation business models with recurring service revenues. Government agencies are procuring commercial constellation capacity to augment national infrastructure. Supply chains are expanding to support standardized satellite components. Launch integration timelines are shortening to meet deployment schedules. This constellation driven demand ensures sustained growth across both satellite manufacturing and launch segments.

Defense Space Resilience and Proliferation Programs

Defense Space Resilience and Proliferation Programs are accelerating demand for distributed satellite architectures and responsive launch capability across the US Satellite Manufacturing and Launch Systems market. National security agencies are transitioning from limited high value satellites toward proliferated constellations. This shift requires increased manufacturing throughput and diversified launch providers. Responsive launch initiatives mandate rapid deployment readiness from domestic launch sites. Procurement frameworks emphasize assured access to space and redundancy. Satellite designs prioritize modularity and rapid replacement capability. Government funding supports domestic supply chain expansion and propulsion innovation. Launch vehicle development programs receive sustained defense investment. Industrial base modernization initiatives expand manufacturing capacity nationwide. These defense priorities significantly reinforce market growth across manufacturing and launch services.

Market Challenges

High Capital Intensity of Launch Vehicle Development

High Capital Intensity of Launch Vehicle Development constrains expansion within the US Satellite Manufacturing and Launch Systems market by requiring multibillion dollar investments before revenue realization. Launch vehicle research, testing, and certification cycles extend over many years. Manufacturing infrastructure for propulsion and structures demands specialized facilities. Failure risks during early flights create financial uncertainty. Insurance costs remain elevated for new launch systems. Smaller entrants struggle to secure sustained funding through development phases. Supply chain qualification adds additional cost and schedule burdens. Government certification requirements impose extensive testing obligations. Investors demand long term returns that delay profitability timelines. These capital barriers limit competitive entry and slow innovation diffusion across the market.

Regulatory and Range Infrastructure Constraints

Regulatory and Range Infrastructure Constraints hinder operational scalability in the US Satellite Manufacturing and Launch Systems market by limiting launch frequency and facility access. Launch approvals involve complex federal licensing and environmental assessments. Range scheduling conflicts occur due to shared military and civil operations. Coastal launch sites face geographic and safety restrictions. Expansion of new spaceports encounters permitting and community opposition challenges. Launch windows are constrained by orbital mechanics and airspace closures. Satellite export control regulations complicate international collaborations. Compliance requirements increase administrative costs for manufacturers. Infrastructure congestion delays mission schedules and constellation deployment timelines. These regulatory and infrastructure limitations restrict market efficiency and capacity utilization.

Opportunities

Responsive Launch Services for Defense and Commercial Customers

Responsive Launch Services for Defense and Commercial Customers represent a major opportunity in the US Satellite Manufacturing and Launch Systems market as users demand rapid orbital deployment capability. Defense agencies require quick replacement of compromised satellites. Commercial operators need flexible launch schedules for constellation maintenance. Dedicated small launch vehicles enable on demand mission readiness. Government funding programs incentivize responsive launch infrastructure development. New mobile and inland launch concepts expand geographic flexibility. Integration timelines are shortening through modular payload interfaces. Responsive launch differentiates providers beyond price competition. Market demand favors providers offering guaranteed rapid deployment capability. This opportunity expands both launch service revenue and satellite manufacturing throughput.

Advanced Manufacturing and Reusable Propulsion Integration

Advanced Manufacturing and Reusable Propulsion Integration offers substantial growth potential in the US Satellite Manufacturing and Launch Systems market by reducing production costs and increasing launch vehicle reliability. Additive manufacturing enables complex propulsion components with fewer parts. Automated composite fabrication accelerates rocket structure production. Reusable engine architectures extend operational lifetimes across missions. Digital engineering shortens design and testing cycles. Manufacturing scalability supports higher launch cadence targets. Cost efficiencies improve competitiveness of domestic launch providers. Government innovation funding accelerates advanced manufacturing adoption. Industrial partnerships expand material and propulsion technology capabilities. Integration of these technologies strengthens long term market competitiveness and profitability.

Future Outlook

The US Satellite Manufacturing and Launch Systems market is expected to expand steadily over the next five years as commercial constellations scale and defense space programs intensify. Reusable launch technologies will mature further, lowering launch costs and increasing cadence. Government initiatives supporting domestic launch infrastructure and resilient space architectures will sustain demand. Advanced manufacturing and modular satellite production will accelerate throughput. Responsive launch capability and proliferated low orbit deployments will remain central growth drivers.

Major Players

- SpaceX

- United Launch Alliance

- Blue Origin

- Northrop Grumman

- Boeing Defense Space and Security

- Lockheed Martin Space

- Rocket Lab USA

- Relativity Space

- Firefly Aerospace

- Astra Space

- Sierra Space

- L3Harris Technologies

- Maxar Space Systems

- York Space Systems

- Terran Orbital

Key Target Audience

- Satellite manufacturers

- Launch service providers

- Defense space agencies

- Commercial satellite operators

- Aerospace component suppliers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Space infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The research began by identifying variables including launch cadence, satellite production capacity, constellation demand, defense procurement, and propulsion technology adoption. Data sources included government budgets, aerospace manufacturing statistics, and launch registries. Variables were validated across multiple industry datasets to ensure consistency. This stage established the structural framework for market sizing and segmentation.

Step 2: Market Analysis and Construction

Quantitative modeling integrated satellite production volumes, launch frequency, and pricing benchmarks across segments. Historical manufacturing output and launch records were analyzed to construct baseline market values. Segment shares were derived from mission distribution and contract allocations. The market structure was assembled through triangulation of supply chain, procurement, and operational datasets.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultation with aerospace engineers, launch operators, and procurement specialists. Assumptions regarding reusability adoption and constellation growth were tested against industry feedback. Discrepancies were reconciled using updated mission and budget data. Expert validation ensured realism and alignment with operational market dynamics.

Step 4: Research Synthesis and Final Output

All validated datasets and analytical outputs were synthesized into a coherent market model and narrative. Segmentation, competitive landscape, and growth factors were aligned with quantitative evidence. Consistency checks ensured segment totals and shares were accurate. The final report integrates validated data, expert insights, and structured analysis to present actionable market intelligence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of commercial satellite broadband constellations

Rising defense space resilience and launch readiness programs

Growth in responsive and smallsat launch demand

Increasing private investment in reusable launch technologies

Acceleration of civil space exploration missions - Market Challenges

High capital intensity of launch vehicle development

Supply chain constraints in propulsion and avionics components

Regulatory and export control compliance complexity

Launch infrastructure bottlenecks and range congestion

Technological risks in reusable system reliability - Market Opportunities

Proliferation of mega constellation deployment programs

Growth in dedicated small satellite launch services

Integration of additive manufacturing in launch production - Trends

Shift toward reusable and partially reusable launch architectures

Miniaturization and standardization of satellite bus platforms

Growth of commercial rideshare launch missions

Automation in satellite assembly and testing

Vertical integration across satellite and launch providers - Government Regulations & Defense Policy

National security space launch certification frameworks

Export control and ITAR compliance evolution

Government funding for domestic launch capability expansion

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Small Satellite Manufacturing Systems

Medium and Large Satellite Platforms

Reusable Launch Vehicle Systems

Expendable Launch Vehicle Systems

Integrated Satellite and Launch Solutions - By Platform Type (In Value%)

Low Earth Orbit Deployment Platforms

Medium Earth Orbit Deployment Platforms

Geostationary Orbit Deployment Platforms

Deep Space and Exploration Platforms

Responsive OnDemand Launch Platforms - By Fitment Type (In Value%)

Commercial Off the Shelf Configurations

Mission Specific Custom Integration

Modular Satellite Bus Integration

Dedicated Launch Integration Packages

Hosted Payload Integration - By End User Segment (In Value%)

Commercial Satellite Operators

Defense and National Security Agencies

Civil Space Agencies and Research Institutions

Earth Observation and Analytics Firms

Satellite Broadband and Communications Providers - By Procurement Channel (In Value%)

Direct Government Contracts

Commercial Launch Service Agreements

Public Private Partnership Programs

Defense Acquisition Frameworks

Multi Launch Service Contracts - By Material / Technology (in Value %)

Advanced Composite Satellite Structures

Additive Manufactured Rocket Components

Cryogenic Propulsion Systems

Electric and Hybrid Satellite Propulsion

Autonomous Guidance and Avionics Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Launch Vehicle Class, Satellite Mass Capability, Orbit Delivery Range, Reusability Level, Manufacturing Integration, Launch Cadence, Mission Assurance, Cost per Launch, Vertical Integration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

SpaceX

United Launch Alliance

Blue Origin

Northrop Grumman

Boeing Defense Space and Security

Lockheed Martin Space

Rocket Lab USA

Relativity Space

Firefly Aerospace

Astra Space

Sierra Space

L3Harris Technologies

Maxar Space Systems

York Space Systems

Terran Orbital

- Defense agencies prioritizing assured access to space

- Commercial operators scaling constellation deployment rates

- Civil agencies increasing science and exploration missions

- News pace startups adopting integrated satellite launch models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now