Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The US Satellite Manufacturing Market, based on a recent historical assessment, is projected to reach USD ~ billion in value. This growth is driven by the increasing demand for communication satellites, advancements in satellite technology, and the rising adoption of satellite-based services. The market is expected to expand further due to government investments in space infrastructure, alongside the private sector’s growing interest in satellite-based applications for telecommunication, earth observation, and defense. The growth is also fueled by demand for miniaturized satellites and low-cost solutions, making satellite manufacturing more accessible.

The US market is dominated by major hubs such as California, Texas, and Colorado. These regions have a strong presence of satellite manufacturing companies, favorable policies, and access to launch sites. California, in particular, has established itself as the leading state due to its innovation-driven ecosystem, including a significant number of aerospace companies, research institutions, and government agencies like NASA. Texas and Colorado also contribute to the market’s growth through partnerships with defense contractors and a robust infrastructure for space technology development.

Market Segmentation

By Product Type

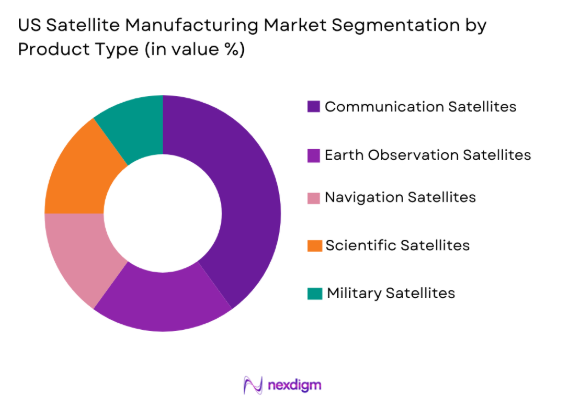

The US Satellite Manufacturing market is segmented by product type into communication satellites, earth observation satellites, navigation satellites, scientific satellites, and military satellites. Recently, communication satellites have dominated the market share due to high demand from telecommunications and internet service providers for global connectivity. This segment’s growth is attributed to technological advancements in satellite communication systems and the rising need for reliable broadband services in remote areas. Furthermore, government and private sector collaborations have bolstered the development and deployment of communication satellites.

By Platform Type

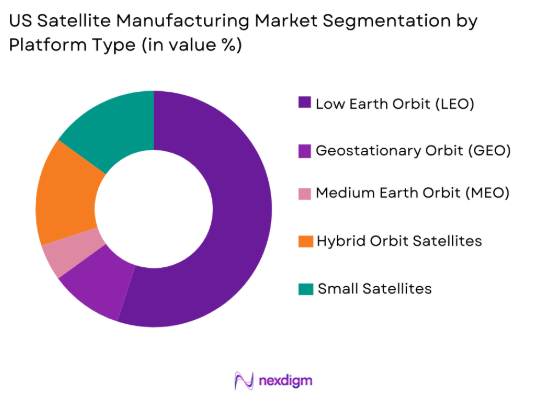

The US Satellite Manufacturing market is segmented by platform type into low earth orbit (LEO) satellites, geostationary orbit (GEO) satellites, medium earth orbit (MEO) satellites, hybrid orbit satellites, and small satellites. The LEO satellite segment currently holds a dominant market share, driven by the increasing demand for small satellite constellations offering global internet coverage and real-time data. LEO satellites are more cost-effective and flexible for deployment, making them a popular choice for both commercial and government space missions. Their ability to provide low-latency communication further strengthens their dominance in the market.

Competitive Landscape

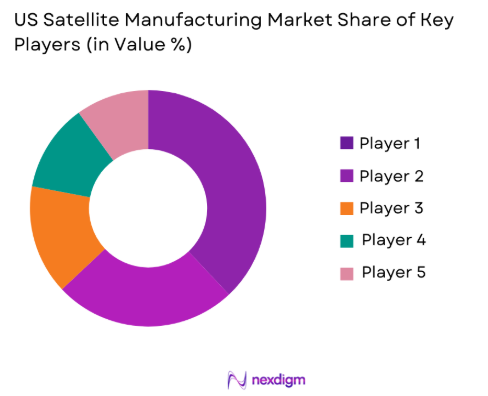

The competitive landscape of the US Satellite Manufacturing market is marked by strong consolidation, with key players leading the way in satellite development, manufacturing, and deployment. Major companies such as SpaceX, Boeing, and Lockheed Martin are at the forefront, driving innovation in satellite technologies and services. The market is seeing increasing collaborations and mergers, as smaller firms seek to leverage the expertise and resources of larger players to scale operations. Government funding and defense contracts also significantly influence market dynamics, driving competitiveness and technological advancements.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| SpaceX | 2002 | Hawthorne, CA | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, IL | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, MD | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church, VA | ~ | ~ | ~ | ~ | ~ |

| Maxar Technologies | 1969 | Westminster, CO | ~ | ~ | ~ | ~ | ~ |

US Satellite Manufacturing Market Analysis

Growth Drivers

Government Investments in Space Infrastructure

The US government plays a pivotal role in driving the satellite manufacturing market, with substantial investments in space infrastructure. Key agencies such as NASA, the Department of Defense, and the National Reconnaissance Office (NRO) are consistently funding satellite manufacturing projects that serve both defense and civilian purposes. These investments support long-term contracts and contribute to the development of cutting-edge satellite technology. In addition, the growing demand for satellite-based services such as global internet, weather monitoring, and defense applications, along with government initiatives like space exploration programs, significantly boosts market growth. The federal funding and long-term satellite contracts help manufacturers scale their operations, improve their technological capabilities, and reduce production costs, fostering innovation and expanding market opportunities. As government spending on space exploration and satellite technology increases, satellite manufacturers can expect sustained demand and further market expansion.

Technological Advancements in Satellite Systems

Technological innovations in satellite design and manufacturing are driving the growth of the US satellite manufacturing market. The continuous development of advanced satellite systems, including miniaturized, high-performance satellites, and the integration of new technologies like artificial intelligence, machine learning, and advanced propulsion systems, have transformed satellite manufacturing. Satellite miniaturization has made it possible to manufacture cost-effective and highly efficient satellites for a wide range of applications, from communication to Earth observation and military uses. The growing demand for small satellite constellations, which offer affordable, scalable solutions for global communications, is expected to propel market expansion. Furthermore, innovations in propulsion systems, solar energy panels, and communication technologies are enhancing satellite capabilities, enabling manufacturers to provide solutions that meet the growing needs of the telecommunications, defense, and space industries. These technological advancements are crucial in fostering both short-term and long-term market growth.

Market Challenges

High Manufacturing Costs

One of the most significant challenges facing the US satellite manufacturing market is the high cost of manufacturing satellites. The costs involved in designing and producing satellites are substantial, as advanced technologies, high-quality materials, and specialized manufacturing processes are required. Satellites, especially those used for communication and defense purposes, must meet stringent performance, durability, and reliability standards, which drives costs. Additionally, the complexity of satellite integration and the high costs associated with rocket launches further contribute to the overall expense of satellite manufacturing. As the demand for high-tech and specialized satellites continues to rise, manufacturers face increasing pressure to optimize production processes and reduce costs without compromising quality. While technological advancements have helped lower some costs, the capital-intensive nature of satellite manufacturing remains a key challenge that manufacturers must navigate.

Space Debris and Environmental Impact

As the number of satellites launched into orbit increases, space debris has become a growing concern for satellite manufacturers. The increasing volume of satellites in orbit raises the risk of collisions and the creation of more debris, which can damage both operational satellites and space stations. Space debris mitigation and safe satellite disposal have become critical challenges for satellite manufacturers, as they are now required to design satellites with end-of-life disposal plans, such as deorbiting mechanisms to ensure safe removal from orbit. The regulatory pressures surrounding space debris management are increasing, and satellite manufacturers are expected to adopt technologies that mitigate the risk of creating additional debris. Furthermore, environmental concerns over the emissions from rocket launches and the overall environmental impact of satellite production and operation are also becoming increasingly important. These environmental challenges require the industry to innovate and adopt more sustainable practices.

Opportunities

Growth of Small Satellites and Constellations

The US satellite manufacturing market has witnessed significant growth in the small satellite segment, which is expected to continue expanding in the coming years. Small satellites offer a cost-effective solution for both commercial and government applications, enabling faster deployment and scalability. The development of small satellite constellations, such as SpaceX’s Starlink, is one of the most notable trends in the industry. These constellations are designed to provide global internet coverage, real-time Earth observation, and other data services. The increasing demand for satellite internet services, especially in underserved and remote areas, is driving the growth of small satellites. Additionally, small satellites are easier and cheaper to launch, which makes them an attractive option for companies looking to deploy space infrastructure quickly and affordably. With advancements in miniaturization technology and the ability to launch large constellations of small satellites efficiently, the market for small satellites is poised for further growth.

Private Sector Collaboration with Government

The ongoing collaboration between private satellite manufacturers and government agencies presents significant opportunities for the US satellite manufacturing market. Government entities like NASA, the Department of Defense, and the National Oceanic and Atmospheric Administration (NOAA) often enter into public-private partnerships with satellite manufacturers to develop and deploy satellite systems for national defense, space exploration, and Earth monitoring purposes. These partnerships provide satellite manufacturers with access to government funding and long-term contracts, which are crucial for market expansion. Private companies, including SpaceX, Blue Origin, and other players, are increasingly involved in satellite manufacturing for both commercial and government projects, contributing to the market’s growth. This collaboration allows satellite manufacturers to leverage government support, improve technological capabilities, and tap into new market segments such as space exploration, communications, and environmental monitoring. As the demand for advanced satellite systems rises, continued public-private partnerships will further stimulate market development.

Opportunities

Growing Demand for Earth Observation Data

The demand for Earth observation data is expanding as businesses, governments, and research institutions seek real-time insights for various applications, including environmental monitoring, disaster management, and agricultural optimization. Satellite-based Earth observation systems play a critical role in providing high-resolution imagery and data that can be used for monitoring climate change, weather patterns, urban development, and natural disasters. The increasing use of satellites for geospatial analytics, mapping, and other data-driven applications is expected to propel the growth of Earth observation satellites. This demand is particularly strong in sectors such as agriculture, forestry, and environmental monitoring, where satellite data offers a unique and efficient solution for tracking large-scale trends and making informed decisions. The growth of data analytics and the need for precise monitoring are providing satellite manufacturers with ample opportunities to expand their Earth observation satellite offerings.

Private Sector Innovation and Investment

Another opportunity lies in the growing interest and investment from private companies in satellite manufacturing. Venture capital and private sector investment in space-based technologies have surged, leading to increased innovation and competition among manufacturers. Companies like SpaceX, Rocket Lab, and Planet Labs are exploring new ways to reduce satellite production costs, improve satellite performance, and increase accessibility to space. The increasing involvement of private companies in satellite manufacturing is expected to drive innovation in both satellite technology and launch systems, making space more accessible and affordable. As commercial players look to capitalize on the opportunities in space communications, Earth observation, and defense applications, the market will see a rise in new and innovative satellite solutions that meet the evolving demands of various industries. The rapid pace of technological development and private sector involvement presents significant opportunities for growth in the satellite manufacturing industry.

Future Outlook

Over the next five years, the US Satellite Manufacturing Market is expected to continue its growth trajectory, driven by advances in satellite technology and increasing demand for satellite-based services. This growth will be supported by significant government funding for space infrastructure, including national defense and space exploration projects. Additionally, innovations in small satellite constellations, space communication technologies, and satellite miniaturization will open new market avenues. The US government’s commitment to space exploration and international collaborations will also propel the market forward. Technological developments such as reusable rockets and AI-driven satellite management systems will improve efficiency and reduce costs, further driving market expansion.

Major Players

- SpaceX

- Boeing

- Lockheed Martin

- Northrop Grumman

- Maxar Technologies

- SES S.A.

- Airbus Defence and Space

- Ball Aerospace

- Arianespace

- Rocket Lab

- Planet Labs

- OneWeb

- Inmarsat

- Iridium Communications

- SL (Space Systems/Loral)

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Military organizations and contractors

- Satellite communications service providers

- Satellite technology developers

- Aerospace manufacturers

- Space exploration agencies

- Private sector technology companies

Research Methodology

Step 1: Identification of Key Variables

Key variables were identified based on industry trends, historical data, and expert insights to define the market scope and parameters.

Step 2: Market Analysis and Construction

A comprehensive market analysis was conducted, incorporating data from primary and secondary sources to build a robust market framework.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were validated through expert consultations and feedback from key stakeholders to ensure the accuracy and relevance of the findings.

Step 4: Research Synthesis and Final Output

The final report synthesized all gathered data, findings, and insights to provide actionable conclusions and market recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Demand for Communication Satellites

Technological Advancements in Miniaturization

Increasing Government Investment in Space Exploration

Expanding Commercial Space Opportunities

Enhanced Global Connectivity Needs - Market Challenges

High Capital Investment in Satellite Manufacturing

Technological Barriers to Satellite Integration

Regulatory Hurdles in Space Operations

Environmental Risks in Satellite Deployment

Cybersecurity Concerns in Satellite Communication - Market Opportunities

Emerging Markets for Satellite Internet Services

Increasing Demand for Earth Observation Data

Partnerships between Government and Private Sector - Trends

Miniaturization of Satellite Systems

Increased Demand for Low-Cost Satellites

Adoption of Autonomous Satellite Operations

Integration of AI for Satellite Management

Sustainability Trends in Satellite Manufacturing - Government Regulations & Defense Policy

Space Debris Mitigation Regulations

Government Funding Programs for Space Innovation

National Security and Satellite Protection Policies

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Communication Satellites

Earth Observation Satellites

Navigation Satellites

Scientific Satellites

Military Satellites - By Platform Type (In Value%)

Low Earth Orbit (LEO) Satellites

Geostationary Orbit (GEO) Satellites

Medium Earth Orbit (MEO) Satellites

Hybrid Orbit Satellites

Small Satellites - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Government Agencies

Telecommunication Operators

Military Forces

Private Space Companies

Commercial Enterprises - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Carbon Fiber Composites

Solar Panels

Propulsion Systems

Satellite Communication Systems

Onboard Computing Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Material / Technology, Market Value, Installed Units, Average System Price)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

SpaceX

Lockheed Martin

Northrop Grumman

Boeing

Blue Origin

Airbus Defence and Space

Maxar Technologies

SES S.A.

Thales Alenia Space

Ball Aerospace

Arianespace

Rocket Lab

Planet Labs

OneWeb

Inmarsat

- Government Agencies’ Role in Satellite Procurement

- Military Forces’ Increased Dependence on Space Assets

- Telecommunication Operators’ Expansion of Satellite Networks

- Private Space Companies’ Emerging Market Growth

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now