Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the United States third‑party logistics (3PL) market was valued at approximately USD ~ billion according to an established industry research source, reflecting sustained spending on outsourced logistics services including transportation management, warehousing, and integrated supply chain solutions. This market size is driven by the rapid expansion of e‑commerce, increasing complexity of supply chains, and a growing corporate focus on cost efficiency through logistics outsourcing, as businesses seek to leverage scalable third‑party networks and technology‑enabled solutions to optimize operations.

The United States is home to several dominant logistics hubs that shape the 3PL landscape due to their infrastructure, connectivity, and access to major trade lanes. Key metropolitan regions such as Los Angeles, Chicago, and Atlanta serve as critical nodes for freight distribution, linked to major ports, rail networks, and interstate highways that facilitate efficient movement of goods across the country. These cities attract 3PL providers due to high volumes of inbound and outbound freight, diverse industrial activity, and proximity to consumer markets, enabling providers to deliver faster service and integrate multimodal logistics strategies to meet demand.

Market Segmentation

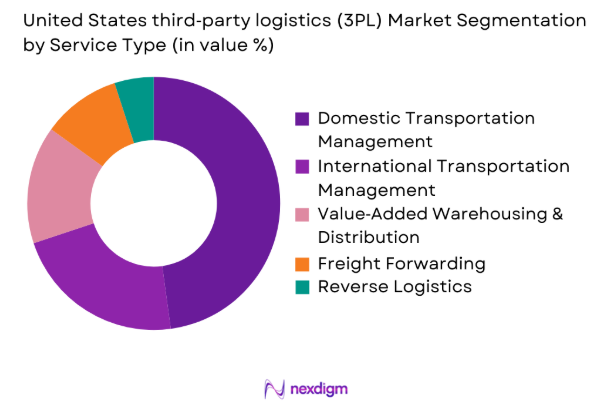

By Service Type

The United States 3PL market is segmented by service type into Domestic Transportation Management, International Transportation Management, Value‑Added Warehousing & Distribution, Freight Forwarding, and Reverse Logistics. Recently, Domestic Transportation Management has a dominant market share due to its central role in managing inland freight movements, freight brokerage, and last‑mile delivery coordination, which remain critical for e‑commerce and retail supply chains. Its dominance is supported by robust infrastructure, widespread carrier networks, and advanced transportation management systems that improve route efficiency and cost control for shippers handling high volumes of domestic freight.

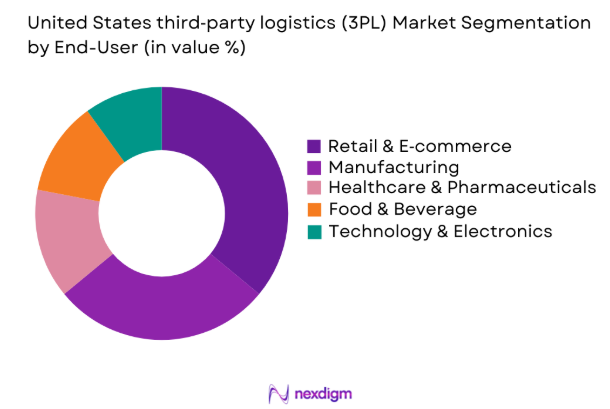

By End‑User Segment

The United States 3PL market is segmented by end users into Retail & E‑commerce, Manufacturing, Healthcare & Pharmaceuticals, Food & Beverage, and Technology & Electronics. Recently, Retail & E‑commerce has a dominant market share due to ongoing demand for fast fulfillment, inventory management, and scalable logistics solutions that support omnichannel sales. E‑commerce growth requires rapid order processing and last‑mile delivery capabilities, which 3PL providers facilitate through extensive distribution networks, automated fulfillment centers, and technology platforms tailored to consumer expectations and inventory visibility requirements.

Competitive Landscape

The United States 3PL market features a competitive environment with several global and regional players driving consolidation through technology investment and expanded service portfolios. Major providers leverage digital freight platforms, data analytics, and integrated supply chain solutions to differentiate offerings and meet diverse customer requirements across sectors. Competition also stems from firms focusing on specialized segments such as cold chain logistics, last‑mile delivery, and international freight forwarding, leading to strategic partnerships, mergers, and acquisitions that strengthen network reach and service breadth.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Specialized Capability |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| C.H. Robinson | 1905 | USA | ~ | ~ | ~ | ~ | ~ |

| XPO Logistics | 2011 | USA | ~ | ~ | ~ | ~ | ~ |

| FedEx Logistics | 1985 | USA | ~ | ~ | ~ | ~ | ~ |

| UPS Supply Chain Solutions | 1907 | USA | ~ | ~ | ~ | ~ | ~ |

United States third‑party logistics (3PL) Market Analysis

Growth Drivers

Supply Chain Digitalization and E‑commerce Integration

The rapid acceleration of supply chain digitalization and e‑commerce integration has transformed the United States third‑party logistics market, driving investment in transportation and warehouse management systems, real‑time visibility, and predictive analytics. 3PL providers leverage cloud platforms, machine learning, and automated distribution centers to optimize routing, inventory, and capacity, reducing costs and improving agility. Growing e‑commerce demand for fast, scalable order management, last‑mile delivery, and returns processing has spurred robotics, digital freight matching, and seamless platform integration. These technologies enable transparency, just‑in‑time inventory, and omnichannel fulfillment while fostering collaboration, performance monitoring, and long-term client relationships, making digitalization a central growth driver in the US 3PL industry.

Infrastructure Expansion and Network Optimization

Infrastructure expansion and network optimization are key growth drivers for the United States third‑party logistics market, as providers invest in distribution centers, cross‑dock facilities, and transportation corridors to support high-volume freight and reduce transit times. Investments in automated warehouses, temperature‑controlled facilities, and multimodal networks enable efficient handling of diverse cargo, from perishables to electronics, while optimizing labor and capacity. Network strategies combine road, rail, air, and ocean freight to lower costs, improve sustainability, and support near‑shoring trends. These developments enhance connectivity between ports, manufacturing zones, and consumer markets, attracting shippers across sectors and enabling 3PL providers to deliver scalable, reliable, and cost-effective logistics solutions.

Market Challenges

Labor Shortages and Workforce Skill Gaps

The United States third‑party logistics market faces major challenges from labor shortages and skill gaps, limiting operational scalability across warehousing, transportation planning, and technology functions. A shortage of skilled workers to manage advanced equipment and automated systems forces 3PL providers to invest heavily in training or rely on costly staffing agencies, raising operating expenses. Limited qualified drivers exacerbate capacity constraints, increasing freight rates and delivery delays. Automation partially offsets workforce pressures but requires specialized technicians, intensifying competition and wage costs. Aging demographics reduce experienced personnel, while regulatory compliance demands add complexity. Collectively, these workforce constraints hinder efficiency, expansion, and innovation, pressuring 3PL providers to adapt strategically.

Regulatory Compliance and Cost Pressures

Regulatory compliance and rising cost pressures present major challenges for the United States third‑party logistics market, as firms must navigate federal, state, and local regulations covering transportation safety, emissions, labor practices, and hazardous materials. Compliance increases administrative and operational costs, requiring investments in training, monitoring systems, and fleet upgrades. Varying state mandates on weight limits, tolls, and labor classification complicate network optimization, while regulatory uncertainty around data privacy and trade agreements can delay technology adoption. Additional cost pressures include fuel, real estate, and insurance. These factors strain profitability, limit investment in innovation, and challenge 3PL providers’ ability to maintain competitive, value‑added services in a dynamic market.

Opportunities

Advanced Automation and AI‑Enabled Logistics

The adoption of advanced automation and AI-enabled logistics offers the United States third-party logistics market a significant opportunity to enhance efficiency and service quality by reducing manual tasks, optimizing routing, forecasting demand, and improving inventory placement. Technologies such as autonomous guided vehicles, robotic picking, and automated storage accelerate order processing, improve accuracy, and increase safety. AI-powered interfaces and IoT integration enable real-time tracking, proactive bottleneck management, and improved client communication. Digital twin simulations support scenario planning and resilience. These innovations allow 3PL providers to offer premium, data-driven services, optimize energy use, support sustainability goals, and expand market share while meeting growing shipper expectations.

Integration of Sustainable and Green Logistics Services

The emphasis on sustainability and green logistics offers significant opportunities for United States third‑party logistics providers to differentiate services and attract environmentally conscious clients. Shippers seek partners who reduce carbon footprints, optimize energy use, and support carbon‑neutral deliveries, modal shifts, and electric vehicle integration. Investments in alternative fuel vehicles, energy‑efficient warehouses, and carbon accounting help clients meet emissions targets and ESG objectives. Sustainable practices also include packaging optimization and reverse logistics to minimize waste. Certifications and transparent reporting enhance brand reputation, while partnerships with clean energy suppliers and intermodal carriers improve efficiency. Integrating sustainability enables 3PL providers to access new market segments and gain competitive advantage.

Future Outlook

Over the coming five years, the United States third‑party logistics market is expected to sustain growth driven by continued e‑commerce expansion, adoption of advanced digital and automation technologies, and strategic investments in infrastructure and network optimization. Demand for real‑time visibility, predictive analytics, and integrated supply chain services will accelerate as shippers prioritize flexibility and resilience in their logistics operations. Regulatory focus on emissions and safety standards, coupled with consumer expectations for faster delivery and transparent tracking, will encourage 3PL providers to innovate and differentiate through green logistics and AI‑enabled solutions. Public and private investments in transportation corridors and distribution hubs will further enhance connectivity across key markets, supporting domestic and international freight flows.

Major Players

- DHL Supply Chain

- C.H. Robinson

- XPO Logistics

- FedEx Logistics

- UPS Supply Chain Solutions

- Ryder System

- CEVA Logistics

- J.B. Hunt Transport Services

- Kuehne + Nagel

- DB Schenker Logistics

- Americold Logistics

- Expeditors International of Washington

- Penske Logistics

- DSV

Key Target Audience

- Manufacturing firms supply chain executives

- Retail and e‑commerce operations directors

- Healthcare and pharmaceuticals logistics managers

- Food and beverage distribution planners

- Technology and electronics logistics strategists

- Investments and venture capitalist firms

- Government and regulatory bodies

- Large fleet and transportation procurement heads

Research Methodology

Step 1: Identification of Key Variables

We identified market drivers, segmentation axes, historical revenue benchmarks, and competitive factors to frame the research scope and data requirements.

Step 2: Market Analysis and Construction

We compiled verified market size figures, segmented the market by service and end‑user types, and analyzed demand indicators and structural trends.

Step 3: Hypothesis Validation and Expert Consultation

We cross‑referenced findings with industry reports, trade publications, and expert commentary to validate hypotheses and ensure data integrity.

Step 4: Research Synthesis and Final Output

We synthesized insights into a cohesive narrative, ensuring alignment with verified statistics, structural requirements, and editorial accuracy.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce and Omnichannel Retail

Advancements in Digital Supply Chain Technologies

Increasing Outsourcing of Logistics Operations - Market Challenges

Rising Operational Costs and Labor Constraints

Regulatory Compliance and Safety Standards

Integration Complexity Across Multi-modal Networks - Market Opportunities

Adoption of AI and IoT in 3PL Operations

Expansion in Cold Chain and Specialized Logistics

Strategic Partnerships with Technology Providers - Trends

Automation in Warehousing and Distribution

Real-time Tracking and Data Analytics Integration

Sustainability Initiatives and Green Logistics - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Contract Logistics

Freight Forwarding Services

Warehouse Management Solutions

Transportation Management Systems

Integrated Supply Chain Services - By Platform Type (In Value%)

Road Transport Platforms

Air Freight Platforms

Rail Freight Platforms

Maritime Logistics Platforms

Integrated Digital Platforms - By Fitment Type (In Value%)

On-premise Logistics Solutions

Cloud-enabled 3PL Platforms

Hybrid Operational Models

Automated Warehousing Solutions

End-to-End Managed Services - By End User Segment (In Value%)

Retail and E-commerce Firms

Manufacturing and Industrial Companies

Pharmaceutical and Healthcare Providers

Food and Beverage Companies

Technology and Electronics Firms - By Procurement Channel (In Value%)

Direct Contracts with 3PL Providers

Government and Municipal Contracts

Third-party Logistics Brokers

Online Logistics Marketplaces

Industry Consortiums and Partnerships

- Market Share Analysis

- Cross Comparison Parameters (Service Type, Platform Type, End User Segment, Fitment Type, Procurement Channel, Geographic Coverage, Technology Integration, Sustainability Practices, Automation Level, Network Density, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

Kuehne + Nagel

DB Schenker

XPO Logistics

CEVA Logistics

UPS Supply Chain Solutions

FedEx Logistics

Ryder System

C.H. Robinson

Geodis

J.B. Hunt Transport Services

Expeditors International

Penske Logistics

Americold Logistics

Kerry Logistics

- Retailers Increasing Dependence on Third-party Logistics

- Manufacturers Leveraging 3PL for Distribution Efficiency

- Healthcare Sector Expanding Specialized Logistics Needs

- E-commerce Firms Driving Urban Fulfillment Innovations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now