Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agricultural Combine Harvester Market reached approximately USD ~ billion based on a recent historical assessment derived from farm machinery shipment values and manufacturer sales disclosures reported by the Association of Equipment Manufacturers and USDA farm mechanization statistics. Demand is driven by replacement cycles in a large installed combine fleet, expansion of large-scale grain farming, and adoption of high-capacity harvesters equipped with precision yield monitoring and automation technologies to improve harvesting efficiency and reduce labor dependence.

Major activity clusters are concentrated in Midwest grain belt states including Iowa, Illinois, Nebraska, Kansas, and Minnesota due to extensive corn and soybean production and large commercial farm structures requiring high-capacity harvesting machinery. Cities such as Moline, Fargo, Hesston, and Grand Island host major combine manufacturing and engineering facilities. These regions benefit from strong dealer networks, export logistics, and advanced agronomic research institutions supporting rapid technology adoption in commercial grain harvesting operations.

Market Segmentation

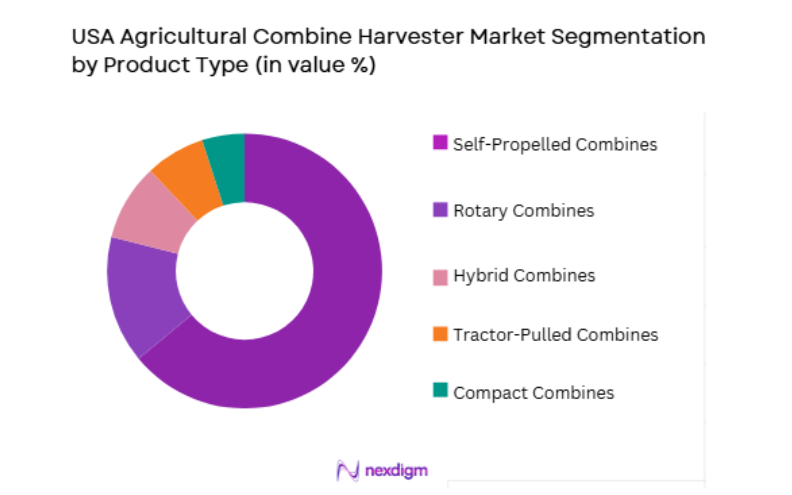

By Product Type

USA Agricultural Combine Harvester Market is segmented by product type into self-propelled combines, tractor-pulled combines, rotary combines, hybrid combines, and compact combines. Recently, self-propelled combines has a dominant market share due to factors such as superior harvesting capacity, integrated grain handling systems, and suitability for large-scale mechanized grain farming across the Midwest. Commercial farms prioritize high-throughput self-propelled machines capable of covering extensive acreage efficiently, while tractor-pulled and compact models are limited to niche or smaller-scale operations.

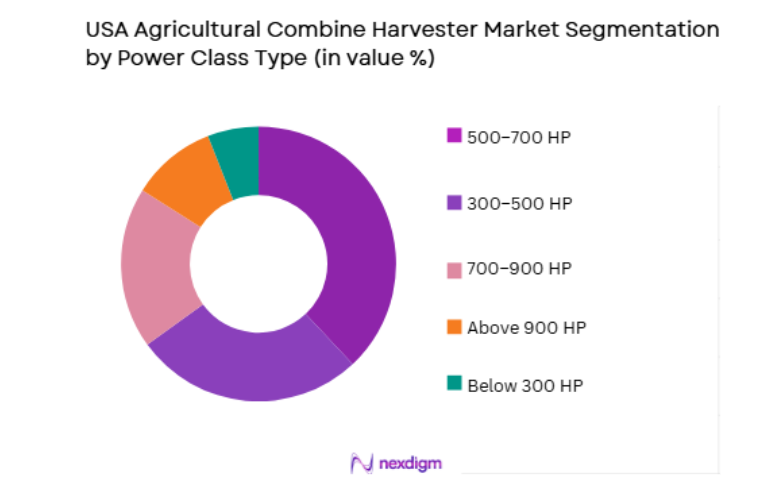

By Power Class

USA Agricultural Combine Harvester Market is segmented by power class into below 300 HP, 300–500 HP, 500–700 HP, 700–900 HP, and above 900 HP. Recently, 500–700 HP has a dominant market share due to factors such as optimal balance between harvesting capacity, fuel efficiency, and compatibility with large header widths commonly used in commercial corn and soybean operations. This power range supports high productivity without excessive acquisition cost or transport constraints, making it preferred by large grain producers upgrading from older mid-power combines.

Competitive Landscape

The USA Agricultural Combine Harvester Market is highly consolidated with dominance of a few global agricultural machinery manufacturers possessing strong brand loyalty, advanced harvesting technology, and extensive dealer service networks. Major OEMs control most sales through integrated distribution and financing programs, while smaller players focus on specialty or niche combine segments. Competitive advantage is driven by automation capability, header compatibility, and precision agriculture integration across commercial grain farming operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Automation Capability |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kubota | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

USA Agricultural Combine Harvester Market Analysis

Growth Drivers

Expansion of Large-Scale Commercial Grain Farming and Harvesting Efficiency Requirements

USA Agricultural Combine Harvester Market growth is strongly driven by the dominance of large-scale commercial grain farms across the Midwest and Plains regions that require high-capacity harvesting machinery capable of covering extensive acreage within short harvest windows. Corn and soybean production systems depend on timely harvesting to minimize yield loss and weather exposure, encouraging investment in advanced self-propelled combines with wide headers and high grain tank capacity. Farm consolidation trends have increased average farm size, raising demand for larger and more powerful combines that improve operational productivity. Labor shortages in agricultural operations further incentivize mechanization upgrades toward machines with automation and operator-assist features. Modern combines equipped with yield monitoring, auto-steering, and crop sensing technologies enable data-driven harvesting and precision farm management. Commercial farms prioritize equipment uptime and throughput, supporting replacement cycles for aging combines. Technological improvements in threshing and separation systems increase grain recovery efficiency, enhancing economic return on investment. Strong grain export demand supports farm profitability and capital spending on harvesting equipment. Financing programs offered by OEMs facilitate acquisition of high-value combines. These structural factors collectively sustain long-term demand for high-capacity combine harvesters across the United States.

Precision Agriculture Integration and Automation in Harvesting Operations

USA Agricultural Combine Harvester Market expansion is driven by rapid integration of precision agriculture technologies and automation systems into combine harvesters used by commercial crop producers. Yield mapping, moisture sensing, and GPS-guided harvesting enable farmers to collect field-level productivity data essential for precision agronomy planning. Autonomous and semi-autonomous harvesting features reduce operator workload and improve harvesting consistency across large fields. Combines integrated with farm management software support real-time monitoring of yield and machine performance, enhancing decision-making efficiency. Automation technologies such as auto-adjusting threshing settings optimize grain separation across varying crop conditions, improving output quality. Data connectivity allows fleet coordination and logistics optimization during harvest operations. Adoption of smart harvesting aligns with broader digital agriculture transformation across U.S. grain farming. Precision harvesting reduces grain loss and fuel consumption, improving operational economics. Technology-driven equipment differentiation encourages replacement demand for advanced combines. Integration with digital agronomy ecosystems therefore acts as a major growth driver in the combine harvester market.

Market Challenges

High Acquisition Cost and Capital Intensity of Modern Combine Harvesters

USA Agricultural Combine Harvester Market faces significant challenges from the extremely high purchase cost of modern self-propelled combines equipped with advanced harvesting and automation technologies. New high-capacity combines represent one of the largest capital investments in grain farming operations, often exceeding affordability thresholds for medium-scale farms. Rising machinery prices driven by technology integration and input cost inflation increase financial burden on farmers. Interest rate fluctuations affect financing cost for equipment purchases. Long replacement cycles due to high capital value reduce annual sales volume stability. Farmers extend usage of older combines to manage debt exposure during commodity price downturns. Used equipment markets compete with new sales, limiting OEM growth. High acquisition cost also discourages adoption of latest technology upgrades. Capital intensity therefore constrains consistent combine replacement demand across farm segments.

Volatility in Agricultural Commodity Prices and Farm Income Cycles

USA Agricultural Combine Harvester Market demand is closely tied to farm profitability, which fluctuates with global grain prices and input cost dynamics affecting farmer purchasing capacity. Periods of low commodity prices reduce farm cash flow and delay machinery investment decisions. Combine purchases are often deferred during unfavorable market conditions. Income variability increases reliance on used equipment or leasing rather than new combine acquisition. Export demand shifts and trade policies influence grain prices and farm revenue expectations. Weather-related yield variability further affects income stability. OEM sales cycles therefore correlate with agricultural economic cycles. Financing institutions tighten credit during downturns, reducing equipment loan availability. Market demand volatility therefore represents a structural challenge for combine manufacturers.

Opportunities

Autonomous Harvesting and Fully Automated Combine Development

USA Agricultural Combine Harvester Market presents strong opportunity through development and commercialization of fully autonomous combine harvesters capable of operating with minimal human intervention across large grain fields. Advances in machine vision, AI-based crop sensing, and autonomous navigation enable combines to harvest efficiently without continuous operator input. Autonomous harvesting reduces labor constraints and improves operational continuity during peak harvest periods. Fleet-based autonomous combines can coordinate harvesting logistics and grain transport operations. OEM investment in autonomy platforms aligns with broader agricultural robotics transformation. Autonomous capability increases equipment productivity and utilization rates. Early adoption by large commercial farms will drive market expansion. Regulatory acceptance of autonomous agricultural machinery supports commercialization. Autonomous harvesting therefore represents a major long-term growth opportunity.

Data-Driven Harvest Optimization and Digital Agriculture Ecosystem Integration

USA Agricultural Combine Harvester Market holds significant opportunity in integration of combines with digital agriculture ecosystems that leverage harvest data for agronomic optimization and farm management decision-making. Yield maps generated during harvest provide critical insights for variable-rate planting and fertilization strategies. Combines connected to cloud-based platforms enable real-time performance analytics and predictive maintenance. Data interoperability across tractors, planters, and combines supports full-season precision agriculture planning. Harvest data analytics improves crop management and profitability forecasting. OEM digital services create recurring revenue streams beyond equipment sales. Farms adopting data-driven management prioritize advanced combine technology. Integration with digital agronomy platforms strengthens customer retention. Data-enabled harvesting therefore expands value proposition of combine equipment beyond mechanical harvesting functions.

Future Outlook

The USA Agricultural Combine Harvester Market is expected to grow steadily over the next five years driven by precision agriculture adoption, automation technologies, and consolidation of large-scale grain farming operations. Replacement demand from aging combine fleets will sustain baseline sales. Autonomous harvesting development and digital farm integration will drive technology upgrades. Strong grain production and export demand will support capital investment in high-capacity harvesting machinery across major agricultural regions.

Major Players

- John Deere

- CNH Industrial

- AGCO

- CLAAS

- Kubota

- New Holland Agriculture

- Case IH

- Fendt

- Massey Ferguson

- Gleaner

- Versatile

- SAME Deutz-Fahr

- Yanmar Agricultural Equipment

- Lovol Heavy Industry

- Zoomlion Agriculture

Key Target Audience

- Agricultural equipment manufacturers

- Commercial grain farming enterprises

- Agricultural machinery dealers and distributors

- Farm machinery financing institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- Precision agriculture technology providers

- Agricultural machinery rental and leasing companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including combine fleet size, harvesting acreage, replacement cycles, and technology adoption levels were identified using USDA farm mechanization statistics and industry shipment data. Automation capability and precision integration were defined as core segmentation factors.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping combine sales value with installed fleet and harvesting demand across major grain regions. Power class and product type distribution were derived from manufacturer data and agricultural production patterns.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding combine demand drivers, replacement behavior, and technology adoption were validated through consultation with agricultural equipment dealers, agronomists, and grain producers. Findings were cross-checked with industry association reports.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, and growth dynamics. Consistency checks ensured alignment with grain production trends and mechanization practices to produce the final outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising farm consolidation and large scale grain production

Technological advancements in harvesting automation and precision

Replacement demand from aging combine fleets - Market Challenges

High acquisition and maintenance cost of combines

Seasonal utilization limiting return on investment

Dependence on commodity price cycles affecting purchases - Market Opportunities

Adoption of autonomous and smart harvesting systems

Growth in custom harvesting service providers

Integration of data driven yield monitoring technologies - Trends

Shift toward high horsepower and high capacity combines

Precision harvesting and real time analytics integration

Tracked combine adoption for soil compaction reduction - Government regulations

Emission standards for agricultural machinery engines

Farm equipment financing and subsidy programs

Safety and operator certification requirements - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Combines

Rotary Combines

Hybrid Combines

High Capacity Combines

Compact Combines - By Platform Type (In Value%)

Wheeled Combines

Tracked Combines

Articulated Combines

Hillside Combines

Autonomous Ready Combines - By Fitment Type (In Value%)

Grain Harvesting Combines

Corn and Maize Combines

Soybean Combines

Multi Crop Combines

Specialty Crop Combines - By End User Segment (In Value%)

Large Commercial Grain Farms

Corporate Farming Enterprises

Custom Harvesting Contractors

- Market Share Analysis

- Cross Comparison Parameters (Harvesting Capacity, Engine Horsepower, Grain Tank Capacity, Header Width Compatibility, Precision Harvesting Technology Integration, Automation and Autonomy Level, Fuel Efficiency, Throughput Efficiency, Residue Management Capability, Dealer and Service Network Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere

Case IH

New Holland Agriculture

Claas

AGCO Massey Ferguson

AGCO Fendt

Kubota

Sampo Rosenlew

Gleaner

Versatile

Preet Agro

Mahindra USA Agri

Yanmar America

Deutz Fahr America

Bourgault Industries

- Large commercial farms driving high capacity combine demand

- Custom harvesters expanding fleet size and technology adoption

- Corporate farms investing in precision harvesting systems

- Cooperatives optimizing shared combine utilization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now