Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agricultural Engine & Powertrain Market reached approximately USD ~ billion based on a recent historical assessment derived from agricultural machinery production value and engine shipment data reported by the Association of Equipment Manufacturers and U.S. Census machinery manufacturing statistics. Demand is driven by large-scale mechanized farming requiring high-horsepower tractors and harvesters, replacement cycles of aging machinery fleets, and increasing integration of advanced transmissions and emission-compliant diesel engines across agricultural equipment platforms.

Major activity clusters are concentrated in Midwest manufacturing states including Iowa, Illinois, Wisconsin, and Nebraska due to strong agricultural machinery production ecosystems and proximity to commercial farming regions. Cities such as Waterloo, Moline, Peoria, and Fargo host major engine and powertrain engineering and assembly facilities. These regions benefit from established component supply chains, skilled manufacturing workforce, and OEM headquarters presence, enabling continuous innovation and localized production of agricultural powertrain systems.

Market Segmentation

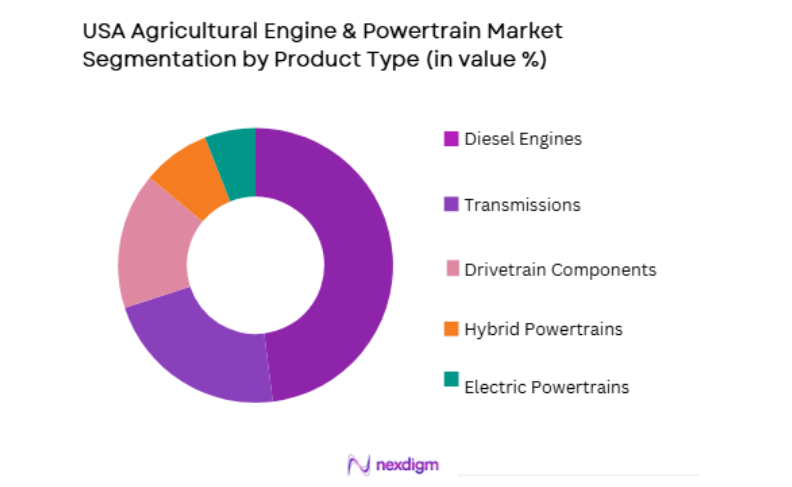

By Product Type

USA Agricultural Engine & Powertrain Market is segmented by product type into diesel engines, hybrid powertrains, electric powertrains, transmissions, and drivetrain components. Recently, diesel engines has a dominant market share due to factors such as high torque requirements in tractors and harvesters, proven reliability in heavy-duty agricultural operations, and widespread compatibility across existing machinery fleets. High-horsepower diesel engines remain essential for large-scale farming equipment operating under demanding field conditions, sustaining strong replacement and OEM integration demand despite emerging electrification trends.

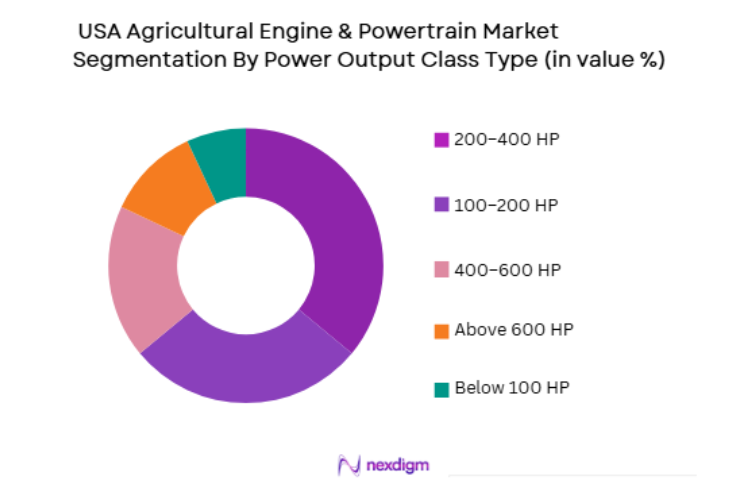

By Power Output Class

USA Agricultural Engine & Powertrain Market is segmented by power output class into below 100 HP, 100–200 HP, 200–400 HP, 400–600 HP, and above 600 HP. Recently, 200–400 HP has a dominant market share due to factors such as widespread use in row-crop tractors and mid-size combine harvesters across commercial farming operations. This power range provides optimal balance between field capability, fuel efficiency, and equipment cost, making it the most common specification for tractors performing planting, tillage, and hauling tasks across U.S. agricultural regions.

Competitive Landscape

The USA Agricultural Engine & Powertrain Market is moderately consolidated with dominance of major agricultural machinery OEMs and specialized engine manufacturers supplying integrated powertrain systems. Large OEMs design proprietary engines and transmissions optimized for their equipment platforms, while independent suppliers provide components and subsystems. Competitive positioning is shaped by emission compliance capability, fuel efficiency performance, and integration with advanced tractor and harvester driveline architectures.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Emission Compliance Capability |

| John Deere Power Systems | 1918 | USA | ~ | ~ | ~ | ~ | ~ |

| Cummins | 1919 | USA | ~ | ~ | ~ | ~ | ~ |

| AGCO Power | 1942 | Finland | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial Powertrain | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| Caterpillar Industrial Engines | 1925 | USA | ~ | ~ | ~ | ~ | ~ |

USA Agricultural Engine & Powertrain Market Analysis

Growth Drivers

Expansion of High-Horsepower Agricultural Machinery and Mechanization Intensity

USA Agricultural Engine & Powertrain Market growth is strongly driven by increasing adoption of high-horsepower tractors and harvesters required for large-scale commercial farming operations across the Midwest and Plains regions. Farm consolidation trends have increased average farm size, encouraging use of larger equipment capable of covering extensive acreage efficiently. High-horsepower machinery requires advanced engines and transmissions delivering higher torque and power density. Replacement demand from aging tractor and combine fleets sustains continuous engine and powertrain integration. Modern agricultural operations rely on mechanization to compensate for labor shortages and maintain productivity. Larger implements and wide headers increase load requirements on powertrains. OEMs continuously develop more powerful and fuel-efficient engines to meet performance expectations. Commercial farming profitability supports capital investment in high-capacity machinery. Export demand for U.S.-manufactured agricultural equipment also drives powertrain production. These structural factors collectively sustain demand growth for agricultural engines and powertrain systems across the United States.

Emission Regulations and Fuel Efficiency Improvements in Agricultural Engines

USA Agricultural Engine & Powertrain Market expansion is driven by stringent emission standards requiring modernization of diesel engines and adoption of advanced combustion and aftertreatment technologies in agricultural machinery. Tier 4 emission regulations mandate significant reductions in particulate and nitrogen oxide emissions from off-road engines used in tractors and harvesters. Compliance requires electronic fuel injection, turbocharging, and exhaust aftertreatment systems integrated into powertrains. Farmers replacing older equipment adopt emission-compliant engines with improved fuel efficiency and reliability. OEMs invest heavily in engine technology innovation to meet regulatory requirements. Modern engines deliver higher efficiency and lower operating cost per acre. Environmental compliance also aligns with sustainability goals in agriculture. Engine upgrades often accompany transmission and drivetrain improvements. Regulatory-driven modernization therefore acts as a major driver for agricultural engine and powertrain replacement and innovation.

Market Challenges

High Development Cost and Technological Complexity of Advanced Powertrain Systems

USA Agricultural Engine & Powertrain Market faces significant challenges from the high research, development, and manufacturing cost associated with advanced agricultural engines and transmissions required for modern machinery. Tier 4 emission compliance and fuel efficiency improvements demand sophisticated engineering and precision manufacturing. Powertrain integration with electronic controls and hydraulic systems increases complexity. Development cycles are long and capital-intensive. OEMs must balance performance, durability, and cost. Smaller manufacturers face barriers to entry due to technology investment requirements. Farmers ultimately bear higher equipment cost resulting from advanced powertrains. High complexity also increases maintenance and repair requirements. These factors raise lifecycle cost of agricultural machinery. Powertrain technology cost therefore constrains affordability and adoption across farm segments.

Transition Uncertainty Toward Electrification and Alternative Powertrain Technologies

USA Agricultural Engine & Powertrain Market faces structural uncertainty related to gradual transition toward electric and hybrid agricultural machinery powertrains. Electrification promises lower emissions and reduced operating cost but remains technically challenging for high-horsepower agricultural applications requiring sustained torque and long operating hours. Battery energy density limitations restrict feasibility of fully electric large tractors and harvesters. Farmers and OEMs face uncertainty regarding long-term powertrain technology pathways. Investment in diesel engine technology remains necessary despite electrification trends. Hybrid systems add complexity and cost without full replacement of diesel capability. Charging infrastructure for electric agricultural machinery is limited in rural regions. Transition uncertainty complicates R&D investment and product planning. This technological transition risk therefore challenges long-term strategy in the agricultural engine and powertrain sector.

Opportunities

Electrification and Hybridization of Agricultural Machinery Powertrains

USA Agricultural Engine & Powertrain Market presents strong opportunity in gradual electrification and hybridization of agricultural powertrain systems aimed at improving fuel efficiency, reducing emissions, and enabling automation-ready machinery platforms. Hybrid diesel-electric drivetrains can optimize power delivery and reduce fuel consumption in tractors and harvesters. Electric auxiliary drives support implements and hydraulic systems more efficiently than mechanical linkages. Electrified powertrains enable precise torque control beneficial for autonomous machinery. Government decarbonization initiatives encourage development of low-emission agricultural equipment. OEMs invest in electric tractor prototypes and hybrid combine systems. Electrification also reduces maintenance complexity in certain subsystems. Battery technology improvements will expand feasible power range. Electrification integration therefore represents a major future growth opportunity for agricultural powertrain innovation.

Integration of Smart Powertrain Controls and Digital Performance Optimization

USA Agricultural Engine & Powertrain Market holds significant opportunity in integration of digital control systems and sensor-driven optimization technologies into engines and transmissions used in agricultural machinery. Smart powertrain control units optimize fuel injection, torque delivery, and load management based on real-time operating conditions. Integration with telematics and farm management platforms enables predictive maintenance and performance monitoring. Data-driven engine management improves fuel efficiency and durability. Powertrain optimization supports precision agriculture operations requiring consistent machine performance. OEMs develop software-driven driveline systems integrated with automation features. Farmers benefit from lower operating cost and reduced downtime. Digitalization enhances value proposition of modern powertrains. Smart powertrain integration therefore expands technological differentiation and market opportunity in agricultural engines and driveline systems.

Future Outlook

The USA Agricultural Engine & Powertrain Market is expected to grow steadily over the next five years driven by demand for high-horsepower machinery, emission-compliant engine upgrades, and gradual electrification integration. Smart digital powertrain controls and hybrid driveline technologies will enhance efficiency and automation readiness. Replacement of aging machinery fleets will sustain baseline demand. Continued mechanization intensity in large-scale farming will support long-term powertrain innovation and production.

Major Players

- John Deere Power Systems

- Cummins

- AGCO Power

- CNH Industrial Powertrain

- Caterpillar Industrial Engines

- FPT Industrial

- Deutz Corporation

- Kubota Engine America

- Yanmar America

- Volvo Penta

- Kohler Engines

- Dana Incorporated

- ZF Off-Highway Solutions

- Bosch Rexroth

- Danfoss Power Solutions

Key Target Audience

- Agricultural equipment manufacturers

- Engine and powertrain component suppliers

- Farm machinery OEM integrators

- Agricultural machinery dealers

- Commercial farming enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment technology developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including engine power class distribution, machinery production volumes, emission compliance requirements, and replacement cycles were identified using agricultural machinery manufacturing data and engine shipment statistics.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping engine and powertrain integration across tractors, combines, and agricultural machinery platforms operating in major U.S. farming regions.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding powertrain demand drivers, emission impact, and electrification transition were validated through consultation with engine manufacturers and agricultural machinery engineers.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, and growth dynamics for the agricultural engine and powertrain sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Demand for high efficiency and high horsepower farm machinery

Emission compliance and engine performance regulations

Electrification and hybridization of agricultural equipment - Market Challenges

High development cost for advanced powertrain technologies

Integration complexity across diverse equipment platforms

Reliability requirements under harsh agricultural conditions - Market Opportunities

Adoption of electric and hybrid agricultural drivetrains

Autonomous equipment powertrain optimization

Localization of advanced powertrain component manufacturing - Trends

Shift toward higher torque and fuel efficient diesel engines

Integration of electronic control and smart power management

Growth of electrified auxiliary and traction systems - Government regulations

EPA emission standards for non road agricultural engines

Fuel efficiency and emission compliance requirements

Incentives for low emission and alternative powertrains - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diesel Agricultural Engines

Hybrid Powertrain Systems

Electric Agricultural Powertrains

Hydrostatic Transmissions

Mechanical Drivetrain Systems - By Platform Type (In Value%)

Tractor Powertrains

Combine Harvester Powertrains

Sprayer Powertrains

Forage Harvester Powertrains

Autonomous Equipment Powertrains - By Fitment Type (In Value%)

OEM Integrated Powertrains

Modular Engine Platforms

High Efficiency Emission Compliant Systems

Electrified Assist Powertrains

Heavy Duty High Torque Systems - By End User Segment (In Value%)

Agricultural Machinery OEMs

Aftermarket Powertrain Integrators

Large Commercial Farms

- Market Share Analysis

- Cross Comparison Parameters (Engine Horsepower Range, Peak Torque Density, Emission Compliance Tier, Fuel Efficiency Performance, Hybrid and Electrification Capability, Transmission Type Integration, Power to Weight Ratio, Thermal Efficiency, Electronic Control Architecture, Durability and Lifecycle Cost, OEM Platform Compatibility, Aftermarket Support Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cummins

John Deere Power Systems

AGCO Power

CNH Industrial FPT

Caterpillar Industrial Engines

Deutz Corporation

Kubota Engine America

Yanmar America

Perkins Engines

Dana Incorporated

ZF Off Highway Solutions

Bosch Rexroth

Eaton Corporation

Allison Transmission

Schaeffler Group

- OEMs demanding high efficiency emission compliant engines

- Large farms requiring high horsepower and durability

- Fleet operators prioritizing fuel efficiency and uptime

- Autonomous equipment developers integrating electric drives

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now