Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agricultural Equipment Market reached approximately USD ~ billion based on a recent historical assessment derived from farm machinery shipment values and production statistics reported by the Association of Equipment Manufacturers and U.S. Census Bureau machinery manufacturing data. Demand is driven by large-scale mechanized farming, replacement cycles in extensive tractor and harvester fleets, and adoption of high-capacity and precision-enabled machinery to improve productivity, efficiency, and labor optimization across commercial crop production systems.

Major activity clusters are concentrated in Midwest manufacturing and farming states including Iowa, Illinois, Wisconsin, Nebraska, and Kansas due to strong agricultural output and equipment manufacturing ecosystems. Cities such as Moline, Waterloo, Fargo, and Hesston host major agricultural machinery OEM headquarters and production facilities. These regions benefit from integrated supply chains, advanced engineering centers, and proximity to large commercial farms, supporting continuous innovation and high equipment utilization across U.S. agricultural operations.

Market Segmentation

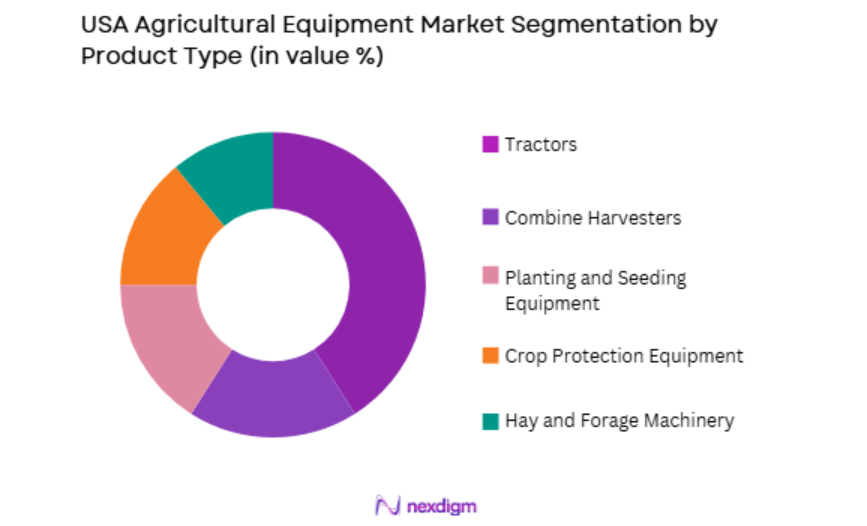

By Product Type

USA Agricultural Equipment Market is segmented by product type into tractors, combine harvesters, planting and seeding equipment, crop protection equipment, and hay and forage machinery. Recently, tractors has a dominant market share due to factors such as central role in all field operations, extensive installed base, and continuous replacement demand across diverse farming systems. Tractors serve as primary power units for tillage, planting, transport, and implement operations across both crop and livestock farms, ensuring sustained demand and integration with modern precision agriculture technologies across commercial farming regions.

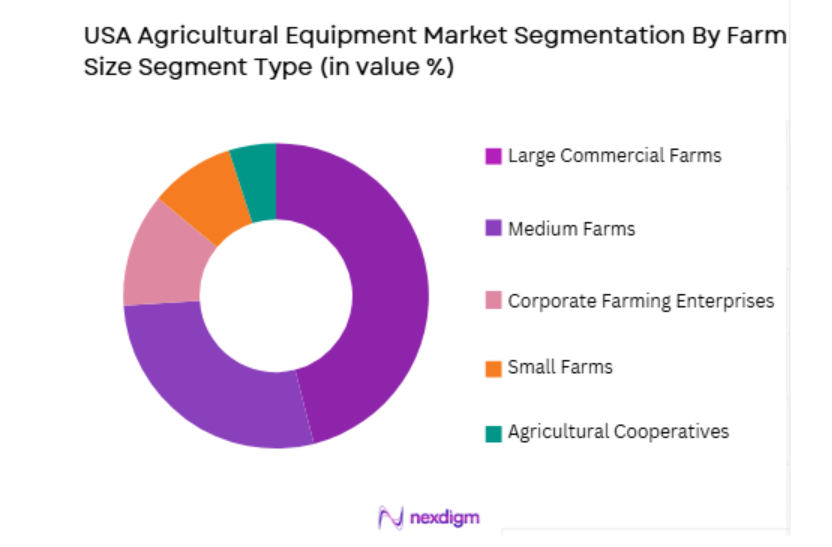

By Farm Size Segment

USA Agricultural Equipment Market is segmented by farm size segment into small farms, medium farms, large commercial farms, corporate farming enterprises, and agricultural cooperatives. Recently, large commercial farms has a dominant market share due to factors such as extensive acreage, high mechanization intensity, and capital capacity for purchasing advanced machinery fleets. These farms operate high-horsepower tractors and large harvesting equipment to manage large-scale crop production efficiently, driving higher equipment value purchases compared with smaller farms that rely more on used or shared machinery.

Competitive Landscape

The USA Agricultural Equipment Market is highly consolidated with dominance of a few global agricultural machinery manufacturers possessing extensive dealer networks, advanced technology integration, and strong brand loyalty across commercial farming regions. Major OEMs control most equipment sales through integrated manufacturing and distribution ecosystems, while specialized manufacturers focus on niche machinery segments. Competitive positioning is shaped by horsepower capability, precision agriculture integration, and aftersales service infrastructure supporting large-scale farm operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Precision Integration Level |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

USA Agricultural Equipment Market Analysis

Growth Drivers

Large-Scale Commercial Farming Expansion and Mechanization Intensity

USA Agricultural Equipment Market growth is strongly driven by expansion and consolidation of large-scale commercial farming operations across major crop-producing regions that require high-capacity mechanized equipment fleets to manage extensive acreage efficiently. Farm consolidation has increased average farm size, encouraging adoption of high-horsepower tractors, large combines, and wide implements capable of covering large fields quickly. Mechanization intensity rises as farms seek productivity improvements and labor cost reduction. Replacement demand from aging machinery fleets sustains equipment sales. Commercial farms prioritize equipment uptime and throughput, supporting investment in advanced machinery. Precision agriculture integration further enhances productivity gains. Strong grain and specialty crop production profitability supports capital spending. Equipment financing programs facilitate purchases. Export-oriented agriculture requires modern machinery. These structural factors collectively sustain long-term demand for agricultural equipment across the United States.

Precision Agriculture and Automation Integration in Farm Machinery

USA Agricultural Equipment Market expansion is driven by rapid adoption of precision agriculture technologies and automation systems integrated into tractors, planters, sprayers, and harvesters used by commercial farms. GPS guidance, variable-rate application, and yield monitoring enable data-driven crop management and improved input efficiency. Automation features reduce operator workload and improve operational consistency. Digital farm management platforms rely on sensor-enabled machinery. Precision equipment improves productivity and sustainability metrics. Farmers adopt technology-equipped machinery to remain competitive. OEM innovation accelerates integration of sensors and control systems. Autonomous-ready equipment platforms expand functionality. Data-driven agriculture supports long-term equipment upgrades. Precision and automation integration therefore acts as a major driver of agricultural machinery demand in the U.S.

Market Challenges

High Capital Cost and Cyclical Demand Linked to Farm Income

USA Agricultural Equipment Market faces major challenges from high acquisition cost of modern agricultural machinery and strong dependence on farm income cycles driven by commodity price volatility. Large tractors and harvesters represent substantial capital investments. Farmers delay purchases during low commodity price periods. Equipment sales correlate with agricultural profitability cycles. Financing cost fluctuations affect purchasing capacity. Used equipment markets compete with new sales. Long machinery lifespans extend replacement cycles. Economic uncertainty reduces capital spending. Price sensitivity persists despite productivity benefits. Cyclical demand therefore constrains consistent growth in agricultural equipment sales.

Labor Shortages and Operational Complexity in Advanced Machinery Use

USA Agricultural Equipment Market faces challenges from agricultural labor shortages and increasing operational complexity of technologically advanced machinery requiring skilled operators and maintenance capability. Modern equipment integrates digital controls, automation, and precision systems. Skilled labor is required for operation and servicing. Rural labor availability is declining. Training requirements increase adoption barriers. Maintenance complexity raises ownership cost. Smaller farms lack technical expertise. Equipment downtime risk affects productivity. Technology adoption gap persists across regions. Operational complexity therefore limits uniform adoption of advanced agricultural machinery.

Opportunities

Autonomous and Electrified Agricultural Machinery Development

USA Agricultural Equipment Market presents strong opportunity through development of autonomous tractors, robotic implements, and electrified machinery platforms aimed at improving productivity, reducing labor dependence, and lowering emissions. Autonomous equipment can operate continuously with minimal human input. Electrified drivetrains improve energy efficiency and enable precise control. OEMs invest heavily in robotics and electric platforms. Large farms adopt early automation technologies. Sustainability initiatives support low-emission equipment. Electrification reduces operating cost in certain applications. Autonomous fleets increase machinery utilization. Technology leadership enhances OEM competitiveness. Autonomous and electric machinery therefore represents major long-term growth opportunity in agricultural equipment.

Digital Agriculture Ecosystem Integration and Data-Driven Equipment Services

USA Agricultural Equipment Market holds significant opportunity in integration of machinery with digital agriculture ecosystems enabling data-driven farm management, predictive maintenance, and service-based equipment models. Connected machinery generates operational and agronomic data streams. OEM platforms analyze data to optimize performance and maintenance. Digital services create recurring revenue beyond equipment sales. Farmers benefit from reduced downtime and improved productivity. Fleet management improves efficiency in large farms. Data-driven agronomy enhances crop yield. Integration strengthens customer loyalty. Digital ecosystem integration therefore expands value proposition of agricultural machinery and creates new growth pathways.

Future Outlook

The USA Agricultural Equipment Market is expected to grow steadily over the next five years driven by large-scale farm consolidation, precision agriculture adoption, and automation integration. Replacement demand from aging machinery fleets will sustain baseline sales. Autonomous and electrified machinery technologies will drive innovation. Digital agriculture platforms will enhance equipment value and services. Continued mechanization intensity across commercial farming regions will support long-term market expansion.

Major Players

- John Deere

- CNH Industrial

- AGCO

- Kubota

- CLAAS

- New Holland Agriculture

- Case IH

- Fendt

- Massey Ferguson

- Gleaner

- Versatile

- SAME Deutz-Fahr

- Kuhn Group

- Horsch

- Great Plains Manufacturing

Key Target Audience

- Agricultural equipment manufacturers

- Commercial farming enterprises

- Agricultural machinery dealers and distributors

- Farm equipment financing institutions

- Precision agriculture technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural machinery rental and leasing companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including machinery fleet size, mechanization intensity, replacement cycles, and technology integration levels were identified using agricultural machinery production data and farm mechanization statistics.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping equipment sales and installed base across major U.S. farming regions and farm size segments.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding demand drivers, technology adoption, and replacement behavior were validated through consultation with equipment dealers, manufacturers, and farm operators.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured analysis covering market size, segmentation, and growth dynamics for the agricultural equipment sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Large scale commercial farming and farm consolidation

Technological advancement in precision and autonomous equipment

Replacement demand from aging machinery fleets - Market Challenges

High equipment acquisition and ownership cost

Cyclical demand linked to commodity price volatility

Labor shortages affecting farm mechanization investment - Market Opportunities

Adoption of autonomous and electric agricultural machinery

Growth of equipment leasing and service based models

Integration of digital agriculture and data platforms - Trends

Shift toward high horsepower and high capacity machinery

Precision agriculture and automation integration

Telematics and fleet management adoption - Government regulations

Emission standards for non road agricultural equipment

Farm subsidy and financing support programs

Safety and operator certification requirements - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors

Combine Harvesters

Planting and Seeding Equipment

Crop Protection Equipment

Tillage and Soil Preparation Equipment - By Platform Type (In Value%)

Wheeled Equipment

Tracked Equipment

Self Propelled Machinery

Mounted Implements

Trailed Implements - By Fitment Type (In Value%)

Open Station Equipment

Cab Enclosed Equipment

Precision Agriculture Enabled Systems

Autonomous Ready Equipment

High Capacity Commercial Equipment - By End User Segment (In Value%)

Large Commercial Farms

Corporate Agribusiness Enterprises

Custom Farming Service Providers

- Market Share Analysis

- Cross Comparison Parameters (Equipment Portfolio Breadth, Horsepower Range, Precision Technology Integration, Automation Capability, Dealer and Service Network Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere

CNH Industrial

AGCO Corporation

Kubota North America

Claas of America

Case IH

New Holland Agriculture

Massey Ferguson

Fendt

Versatile

Great Plains Manufacturing

Kinze Manufacturing

Horsch America

AG Leader Technology

Lindsay Corporation

- Large farms driving demand for high capacity equipment

- Corporate agribusiness investing in precision machinery

- Custom service providers expanding equipment fleets

- Cooperatives optimizing shared equipment utilization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now