Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agricultural Sensors GPS & Control Systems Market reached approximately USD ~ billion based on a recent historical assessment derived from precision agriculture technology shipments and GNSS guidance system integration values reported by the Association of Equipment Manufacturers and USDA digital agriculture adoption studies. Demand is driven by widespread adoption of precision farming, GPS-guided machinery, automated steering, and sensor-based crop and soil monitoring technologies that improve input efficiency, productivity, and operational accuracy across large-scale commercial farming systems.

Major activity clusters are concentrated in Midwest and precision agriculture technology regions including Iowa, Illinois, Minnesota, North Dakota, and California due to high mechanization intensity and advanced precision farming adoption. Cities such as Moline, Fargo, Ames, and Sunnyvale host leading agricultural technology development centers and OEM engineering facilities. These regions benefit from agritech innovation ecosystems, research institutions, and large commercial farms accelerating deployment of GPS guidance, sensors, and automated control systems in agricultural machinery.

Market Segmentation

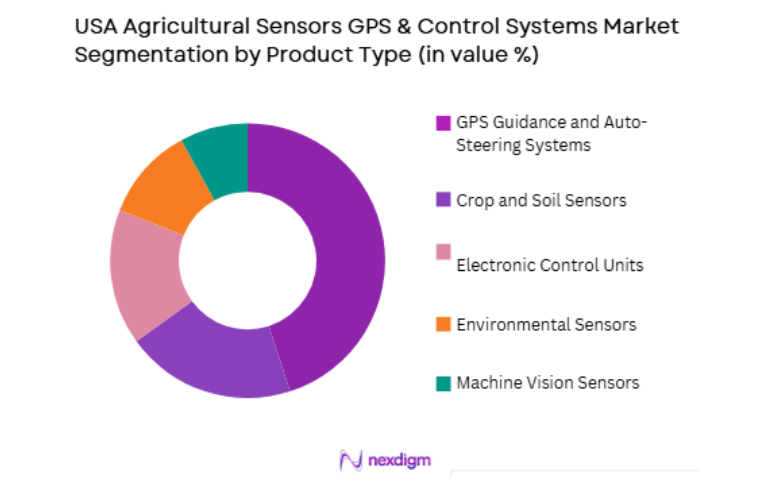

By Product Type

USA Agricultural Sensors GPS & Control Systems Market is segmented by product type into GPS guidance and auto-steering systems, crop and soil sensors, machine vision sensors, environmental sensors, and electronic control units. Recently, GPS guidance and auto-steering systems has a dominant market share due to factors such as near-universal installation in modern tractors and combines, direct productivity impact, and compatibility with precision agriculture practices across large commercial farms. These systems enable accurate field navigation, reduce overlap in planting and spraying operations, and improve fuel and input efficiency, making them foundational technologies in modern agricultural machinery fleets.

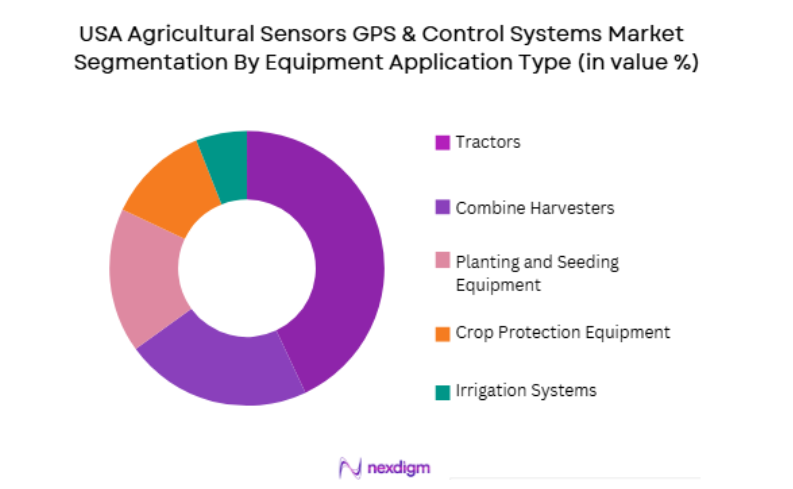

By Equipment Application

USA Agricultural Sensors GPS & Control Systems Market is segmented by equipment application into tractors, combine harvesters, planting and seeding equipment, crop protection equipment, and irrigation systems. Recently, tractors has a dominant market share due to factors such as largest installed base, continuous field operation across seasons, and central role as primary precision agriculture platforms. Tractors integrate GPS guidance, auto-steering, and implement control systems supporting multiple operations including tillage, planting, and spraying, resulting in the highest adoption and value of sensors and control systems across agricultural machinery categories.

Competitive Landscape

The USA Agricultural Sensors GPS & Control Systems Market is moderately consolidated with strong influence from precision agriculture technology providers and agricultural machinery OEMs integrating sensors and guidance systems into equipment platforms. Major players leverage GNSS positioning expertise, digital agriculture platforms, and OEM partnerships to maintain competitive positioning. Technology integration with farm management software and automation systems differentiates market leaders, while aftermarket retrofitting solutions expand deployment across existing machinery fleets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | GNSS Accuracy Capability |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| Trimble | 1978 | USA | ~ | ~ | ~ | ~ | ~ |

| Raven Industries | 1956 | USA | ~ | ~ | ~ | ~ | ~ |

| Topcon Agriculture | 1932 | Japan | ~ | ~ | ~ | ~ | ~ |

| Hexagon Agriculture | 1992 | Sweden | ~ | ~ | ~ | ~ | ~ |

USA Agricultural Sensors GPS & Control Systems Market Analysis

Growth Drivers

Precision Agriculture Adoption and Data-Driven Farm Management Expansion

USA Agricultural Sensors GPS & Control Systems Market growth is strongly driven by widespread adoption of precision agriculture technologies across large commercial farming operations seeking to optimize productivity, input efficiency, and crop yield consistency. Farmers increasingly deploy GPS guidance, crop sensors, and automated control systems to collect high-resolution field data enabling variable-rate planting, fertilization, and spraying decisions. Precision technologies reduce input waste and operational overlap, directly improving economic returns and sustainability outcomes. Integration of sensors and controllers into tractors, planters, and harvesters enables automated machine functions aligned with digital agronomy platforms. Farm management software relies on sensor-generated data streams for decision support and performance analytics. Commercial grain and specialty crop producers adopt precision systems to manage large acreage efficiently under labor constraints. Continuous data collection across crop cycles improves predictive agronomy and risk management. OEM integration of sensors into equipment platforms accelerates adoption among farmers purchasing new machinery. Government conservation and sustainability initiatives encourage precision input management technologies.

Automation and Autonomous Agricultural Machinery Development

USA Agricultural Sensors GPS & Control Systems Market expansion is significantly driven by increasing automation and autonomy integration in agricultural machinery designed to reduce operator workload and improve operational efficiency. Modern tractors, sprayers, and combines incorporate auto-steering, implement control, and machine vision sensors enabling semi-autonomous operation across large fields. Sensor fusion technologies combining GNSS, cameras, lidar, and environmental sensing enable autonomous navigation and task execution. Labor shortages in agriculture accelerate demand for automation capable of sustaining productivity with fewer operators. Autonomous equipment requires extensive sensor arrays and control systems for navigation, crop detection, and machine performance optimization. OEM investment in autonomous agriculture platforms drives demand for advanced sensing technologies. Automation also enhances safety and operational consistency in large-scale farming operations. Integration with digital connectivity platforms allows remote monitoring and control of equipment fleets. Precision automation reduces operator fatigue and operational variability.

Market Challenges

High Integration Cost and Technology Complexity in Precision Systems

USA Agricultural Sensors GPS & Control Systems Market faces significant barriers from high acquisition and integration cost of advanced sensor and GNSS control technologies required for precision agriculture and automation systems. Precision guidance, imaging sensors, and electronic control modules add substantial cost to farm equipment purchases, limiting adoption among smaller or cost-sensitive farms. Retrofitting existing machinery with sensors and controllers often requires complex installation and calibration. Farmers may face compatibility issues across mixed equipment brands and generations. Software integration and data interoperability challenges increase implementation complexity. Training requirements for operators and technicians raise operational cost and learning barriers. Rapid technology evolution risks obsolescence of installed systems.

Data Connectivity Limitations and Interoperability Challenges in Farm Systems

USA Agricultural Sensors GPS & Control Systems Market development is constrained by inconsistent rural connectivity infrastructure and lack of standardized data interoperability across agricultural equipment and software platforms. Precision agriculture systems depend on reliable GNSS correction signals, cloud connectivity, and data transfer between machines and farm management systems. Connectivity gaps in remote farming regions limit real-time data utilization and remote monitoring capability. Proprietary data formats across OEM platforms restrict cross-brand compatibility. Farmers operating mixed equipment fleets face integration challenges. Data ownership concerns affect willingness to share agronomic data across platforms. Interoperability limitations reduce full value realization from sensor data. Software fragmentation complicates digital agriculture adoption.

Opportunities

Expansion of Autonomous and Robotics-Based Agricultural Systems

USA Agricultural Sensors GPS & Control Systems Market presents major opportunity through rapid development of autonomous tractors, robotic harvesters, and sensor-driven agricultural robots requiring advanced GNSS positioning and sensing architectures. Autonomous field robots for planting, weeding, and harvesting rely heavily on machine vision, lidar, and environmental sensors. Robotics integration expands sensor demand beyond traditional machinery platforms. Autonomous fleets require coordination and sensor fusion systems. Agricultural robotics startups and OEMs are investing heavily in sensing technologies. Commercial farms seeking labor-independent operations adopt robotic solutions. Sensor miniaturization and AI-based perception improve robotics capability. Regulatory acceptance of autonomous agricultural machines supports commercialization.

Integration of AI Analytics and Digital Twin Farming Platforms

USA Agricultural Sensors GPS & Control Systems Market holds strong opportunity in integration of sensor data streams with artificial intelligence analytics and digital twin farm modeling platforms enabling predictive agronomy and equipment optimization. Sensor networks generate continuous environmental, crop, and machine performance data that AI systems analyze for yield prediction and operational recommendations. Digital twin farm models simulate field conditions and machinery operations for planning optimization. Integration enhances value of sensor investments beyond data collection. AI-driven agronomy improves decision accuracy and resource efficiency. Equipment manufacturers incorporate analytics into precision platforms. Farms adopting AI-enabled management increase sensor deployment density.

Future Outlook

The USA Agricultural Sensors GPS & Control Systems Market is expected to grow steadily over the next five years driven by precision agriculture expansion, automation in farm machinery, and integration of AI-based analytics. Autonomous agricultural equipment will increase sensor density and control system complexity. Digital farm platforms and connectivity improvements will enhance data utilization. Sustainability-driven input optimization will further accelerate adoption across commercial farming regions.

Major Players

- Trimble Inc.

- Deere & Company Precision Agriculture Division

- AGCO Corporation Precision Planting

- Raven Industries

- Topcon Positioning Systems

- Hemisphere GNSS

- Hexagon Agriculture

- CNH Industrial Precision Technology

- John Deere Intelligent Solutions Group

- Bosch Rexroth Agricultural Electronics

- Danfoss Power Solutions

- Valarm

- Red Hen Systems

- UAV-IQ

- Microchip Technology

Key Target Audience

- Agricultural machinery manufacturers

- Precision farming solution providers

- Commercial farming enterprises

- Agricultural technology integrators

- Farm equipment OEMs

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural data analytics providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including precision agriculture adoption rates, GNSS guidance deployment, sensor integration levels, and automation penetration were identified using agricultural technology adoption studies and industry shipment data.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping sensor and control system integration across tractors, planters, sprayers, and harvesters used in major U.S. farming regions.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, technology cost barriers, and interoperability challenges were validated through consultation with precision agriculture experts and equipment manufacturers.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, and growth dynamics for the agricultural sensors, GPS, and control systems sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of precision agriculture and automated field operations

Integration of autonomous and smart agricultural machinery

Demand for input optimization and yield monitoring - Market Challenges

High cost of advanced sensor and control technologies

Interoperability issues across equipment platforms

Connectivity and data integration limitations in rural areas - Market Opportunities

Adoption of AI enabled sensing and control platforms

Growth of autonomous and robotics farming systems

Cloud based farm data and decision support integration - Trends

Shift toward multi sensor integrated precision systems

Real time GPS guidance and variable rate application

Edge computing and on machine control processing - Government regulations

Agricultural data privacy and ownership policies

Precision agriculture innovation support programs

Wireless communication and GPS spectrum regulations - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPS Guidance and Auto Steering Systems

Variable Rate Control Systems

Machine Vision and Imaging Sensors

Soil and Crop Monitoring Sensors

Telematics and Fleet Control Systems - By Platform Type (In Value%)

Tractor Integrated Control Systems

Combine Harvester Guidance Systems

Sprayer Precision Control Systems

Autonomous Agricultural Platforms

Standalone Field Sensor Networks - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Retrofit Kits

Precision Agriculture Modules

Autonomous Ready Configurations

Cloud Connected Control Systems - By End User Segment (In Value%)

Large Commercial Farms

Corporate Agribusiness Enterprises

Precision Agriculture Service Providers

Agricultural Cooperatives

- Market Share Analysis

- Cross Comparison Parameters (GPS Accuracy Level, Sensor Type Portfolio, Precision Control Capability, Automation Integration Level, Data Platform Compatibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere Precision Ag

Trimble Agriculture

AGCO Precision Planting

CNH Industrial Raven

Topcon Agriculture

Hexagon Agriculture

Deere Blue River Technology

Climate LLC

Taranis

Sentera

Ag Leader Technology

Lindsay FieldNET

Valmont Industries

CropX Technologies

Bosch Smart Agriculture

- Large farms adopting integrated GPS and control systems

- Agribusiness enterprises investing in automation platforms

- Precision service providers deploying retrofit kits

- Research farms piloting advanced sensing technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now