Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agricultural Tractor market demonstrates a substantial installed and transactional base, with total market size valued at approximately USD ~ billion based on a recent historical assessment from industry shipment and retail sales consolidation reported by the Association of Equipment Manufacturers and USDA economic data. Market expansion is driven by sustained replacement cycles, high mechanization intensity across row-crop agriculture, rising precision agriculture adoption, and demand for high-horsepower tractors in large-scale commercial farming operations, particularly across grain and oilseed production belts.

Dominant regions within the USA Agricultural Tractor market include the Midwest, Great Plains, and California’s Central Valley due to concentration of large mechanized farms, high-value crop cultivation, and advanced agricultural infrastructure. States such as Iowa, Illinois, Nebraska, Texas, and California lead equipment demand because of extensive cultivated acreage, commercial-scale agribusiness operations, strong dealership networks, and access to financing and technology services supporting equipment modernization and fleet renewal among professional farming enterprises.

Market Segmentation

By Product Type

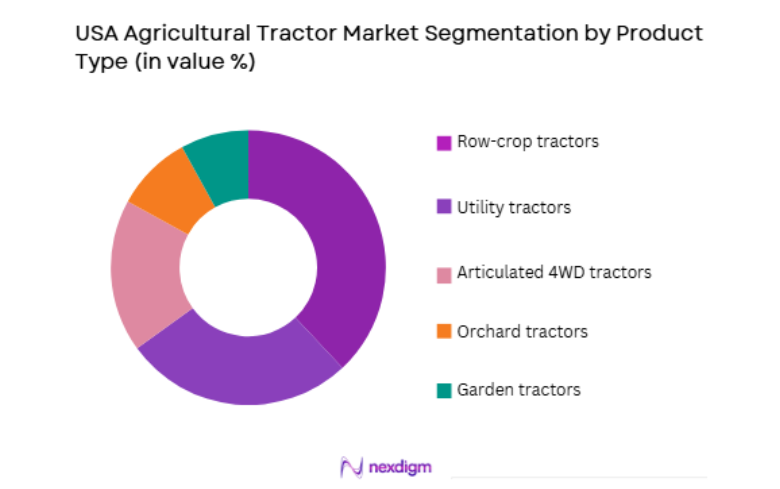

USA Agricultural Tractor market is segmented by product type into utility tractors, row-crop tractors, orchard tractors, garden tractors, and articulated four-wheel-drive tractors. Recently, row-crop tractors have a dominant market share due to factors such as extensive acreage cultivation patterns across corn and soybean belts, strong brand presence from major OEMs in high-horsepower segments, compatibility with precision planting and tillage implements, and infrastructure availability supporting large-scale mechanized row agriculture. Professional farming enterprises prioritize row-crop tractors for versatility across planting, spraying, hauling, and harvesting support operations, while financing programs and dealership service ecosystems further reinforce procurement preference for this segment across commercial producers.

By Horsepower Range

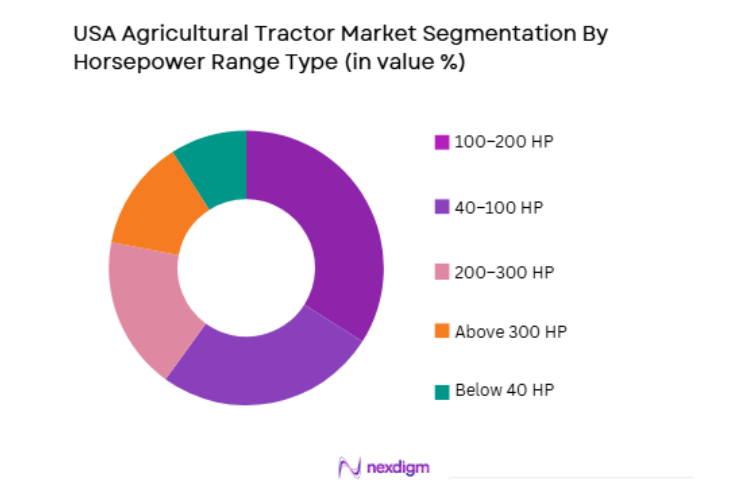

USA Agricultural Tractor market is segmented by horsepower range into below 40 HP, 40–100 HP, 100–200 HP, 200–300 HP, and above 300 HP. Recently, 100–200 HP tractors have a dominant market share due to factors such as balanced capability for mid- to large-scale farming operations, compatibility with diverse implements across planting, mowing, and hauling tasks, and strong availability across dealer inventories nationwide. This horsepower range suits the operational scale of a large proportion of commercial farms, offering optimal fuel efficiency, maneuverability, and cost-to-productivity ratio. Financing accessibility and OEM model proliferation further reinforce adoption across mixed-crop and livestock enterprises seeking versatile mechanization platforms.

Competitive Landscape

The USA Agricultural Tractor market exhibits a highly consolidated competitive structure dominated by a small number of multinational OEMs with extensive dealer networks, manufacturing localization, and strong brand loyalty among commercial farmers. Leading players maintain technological differentiation through precision agriculture integration, autonomous capability development, and high-horsepower engineering. Competitive intensity centers on product innovation, financing solutions, aftermarket service ecosystems, and digital farm management platforms, with major companies leveraging scale and distribution reach to sustain market leadership.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Scale |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK/Netherlands | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota Corporation | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| CLAAS Group | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

USA Agricultural Tractor Market Analysis

Growth Drivers

Large-Scale Commercial Farming Mechanization Intensity

The USA Agricultural Tractor market experiences sustained expansion due to the structural prevalence of large commercial farming operations requiring high-capacity mechanized equipment fleets, which drives continuous tractor procurement cycles across planting, tillage, and hauling applications. Farm consolidation trends increase average farm size, raising demand for higher horsepower tractors capable of covering extensive acreage efficiently within narrow seasonal windows. Mechanization intensity also rises because labor availability constraints push producers toward capital-intensive equipment solutions that improve operational reliability and timeliness. Large grain and oilseed producers prioritize advanced tractors to maintain productivity per worker and reduce operational risk during planting and harvesting peaks. Equipment replacement cycles remain active because professional operators retire tractors based on utilization hours rather than age, sustaining baseline market demand. Financing availability through agricultural credit institutions further enables capital equipment acquisition among commercial producers. OEM dealer ecosystems provide service, parts, and technology support that reinforce equipment lifecycle management and fleet renewal. Precision agriculture compatibility requirements also encourage adoption of newer tractor platforms with integrated digital control architectures.

Precision Agriculture and Digital Farm Integration Adoption

The USA Agricultural Tractor market benefits from widespread integration of digital agriculture technologies that rely on advanced tractor platforms as operational hubs for field automation, guidance, and data collection. Precision planting, variable-rate application, and satellite-guided operations require tractors equipped with electronic control units, telematics, and implement communication systems. Farmers adopt connected tractors to optimize input utilization, improve yield consistency, and document field operations for compliance and agronomic decision support. OEMs embed sensors, connectivity modules, and automated steering capabilities that transform tractors into digital farm management nodes. Data-driven agriculture increases equipment productivity per acre, encouraging investment in technologically advanced tractor models. Digital compatibility also supports integration with farm management software and cloud analytics platforms used by agribusinesses. Autonomous and semi-autonomous operation features further expand tractor functionality in repetitive field tasks. Equipment manufacturers and technology providers collaborate to enhance interoperability across implements and software ecosystems.

Market Challenges

High Capital Acquisition and Ownership Costs for Advanced Tractors

The USA Agricultural Tractor market faces structural constraints due to the significant capital expenditure required to acquire modern high-horsepower and technology-enabled tractors, which can strain farm balance sheets and limit adoption among smaller operations. Advanced tractors incorporate precision guidance, connectivity, and emissions-compliant powertrains that increase purchase price and lifecycle maintenance costs. Financing burdens are amplified during periods of commodity price volatility that reduce farm income stability and borrowing capacity. Ownership costs extend beyond acquisition to include fuel, service contracts, software subscriptions, and replacement parts. Smaller and mid-scale farms often defer purchases or rely on used equipment markets due to cost barriers. Capital intensity also raises investment risk perception among producers uncertain about technology obsolescence timelines. Dealer financing programs partially mitigate cost barriers but do not fully offset high upfront expenditure. Equipment depreciation and resale value uncertainty further influence procurement decisions. These financial pressures constrain broader market penetration of advanced tractors despite technological benefits.

Supply Chain Volatility and Component Availability Constraints

The USA Agricultural Tractor market encounters operational disruption risks stemming from global supply chain volatility affecting availability of critical components such as semiconductors, hydraulic systems, castings, and electronic modules used in modern tractors. Manufacturing delays or shortages can extend equipment lead times, delaying delivery to farmers during critical agricultural seasons. OEM production planning becomes complex when component sourcing fluctuates due to geopolitical, logistical, or raw material constraints. Dealers may face inventory imbalances that limit customer choice and reduce sales conversion. Component cost inflation can also raise final tractor prices, exacerbating affordability challenges for buyers. Technologically advanced tractors are particularly vulnerable because of higher electronic and sensor content. Supply uncertainty can discourage farmers from committing to purchases if delivery timing is unclear. OEMs attempt to localize sourcing and diversify suppliers, but transition periods still affect production continuity.

Opportunities

Autonomous and Semi-Autonomous Tractor Deployment in Large Farms

The USA Agricultural Tractor market has significant expansion potential through deployment of autonomous and semi-autonomous tractor systems capable of operating with minimal human supervision across large commercial farms. Labor scarcity and rising wage pressures motivate producers to adopt automated machinery that maintains productivity without continuous operator presence. Autonomous tractors enable extended operating hours, precise repeatability in field operations, and reduced operator fatigue, enhancing efficiency across planting and tillage tasks. Integration with precision agriculture platforms allows automated tractors to execute variable-rate and guidance-based operations accurately. Large farms with extensive acreage offer optimal environments for autonomous deployment due to scale efficiencies and predictable field layouts. OEM investment in robotics, sensors, and artificial intelligence accelerates commercialization readiness. Early adopters among technologically progressive producers demonstrate operational benefits that influence broader market acceptance. Regulatory frameworks for autonomous agricultural equipment are evolving favorably, supporting adoption pathways.

Electrification and Alternative Powertrain Development for Sustainable Farming

The USA Agricultural Tractor market presents growth opportunities through development of electric and hybrid tractor platforms aligned with sustainability goals and emission reduction requirements in agriculture. Electrified tractors offer lower operating emissions, reduced noise, and potentially lower lifecycle maintenance compared with conventional diesel equipment. Specialty crop farms and operations near urban interfaces show strong interest in low-emission machinery. Advances in battery energy density and charging infrastructure support feasibility of electric tractors in specific duty cycles. Hybrid powertrains can improve fuel efficiency and torque delivery in heavy-load applications. Government incentives and environmental programs encourage adoption of cleaner agricultural equipment technologies. OEMs invest in electrification research to meet future regulatory and market expectations. Electrified tractors can integrate seamlessly with digital control architectures used in precision agriculture. Sustainability certification and carbon reduction initiatives among agribusinesses further stimulate interest in alternative powertrains. These factors create a pathway for new product categories and market expansion within agricultural mechanization.

Future Outlook

The USA Agricultural Tractor market is expected to sustain steady expansion driven by mechanization intensity, digital agriculture integration, and replacement demand across commercial farming enterprises. Technological evolution toward autonomy, connectivity, and alternative powertrains will reshape product portfolios and competitive positioning. Regulatory emphasis on emissions and sustainability will accelerate innovation in powertrain and efficiency technologies. Large-scale farming structures and financing ecosystems will continue to support capital equipment investment, reinforcing long-term demand stability across major agricultural regions.

Major Players

- John Deere

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- CLAAS Group

- Mahindra North America

- SAME Deutz-Fahr

- Kioti Tractor

- Yanmar America

- Versatile

- TYM Corporation

- LS Tractor USA

- McCormick Tractors

- Fendt

- Massey Ferguson

Key Target Audience

- Agricultural equipment manufacturers

- Farm machinery distributors and dealers

- Commercial farming enterprises

- Agribusiness corporations

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural cooperatives

- Precision agriculture technology providers

Research Methodology

Step 1: Identification of Key Variables

Core market variables including tractor product categories, horsepower classes, regional demand centers, technology adoption factors, and procurement drivers were defined. Supply-side indicators such as OEM production, dealer distribution, and component sourcing were mapped. Demand-side variables including farm size structure, crop patterns, and mechanization intensity were identified for analysis.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using triangulation of industry shipment data, retail sales consolidation, and agricultural mechanization indicators. Regional demand distribution and product mix were derived from farming structure and equipment utilization patterns. Competitive positioning and technology penetration were analyzed across OEM portfolios and dealer ecosystems.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions regarding adoption drivers, technology trends, and procurement behavior were validated through consultation with agricultural equipment specialists, dealers, and farm management experts. Cross-verification ensured alignment between demand indicators and equipment deployment realities across major agricultural regions. Sensitivity checks were applied to structural demand factors.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured market narratives covering segmentation, competition, drivers, challenges, and opportunities. Quantitative and qualitative findings were integrated to present a coherent assessment of market dynamics. The final report reflects consolidated analysis of supply-side, demand-side, and technological factors shaping the USA Agricultural Tractor market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Farm consolidation driving high horsepower tractor demand

Technological advancement in precision and autonomous tractors

Replacement demand from aging tractor fleets - Market Challenges

High acquisition and ownership cost of advanced tractors

Cyclical demand linked to commodity price volatility

Labor shortages influencing mechanization investment - Market Opportunities

Adoption of autonomous and electric tractor platforms

Growth of tractor leasing and equipment as a service models

Integration of digital agriculture and data platforms - Trends

Shift toward high horsepower and articulated tractors

Precision agriculture and automation integration

Telematics and remote fleet management adoption - Government regulations

Emission standards for non road tractor engines

Farm subsidy and financing support programs

Safety and operator certification regulations - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility Tractors

Row Crop Tractors

High Horsepower Tractors

Compact Tractors

Specialty Crop Tractors - By Platform Type (In Value%)

Two Wheel Drive Tractors

Four Wheel Drive Tractors

Tracked Tractors

Articulated Tractors

Autonomous Ready Tractors - By Fitment Type (In Value%)

Open Station Tractors

Cab Enclosed Tractors

Precision Agriculture Equipped Tractors

Autonomous Ready Configurations

High Capacity Commercial Tractors - By End User Segment (In Value%)

Large Commercial Farms

Corporate Agribusiness Enterprises

Contract Farming Operators

Agricultural Cooperatives

- Market Share Analysis

- Cross Comparison Parameters (Horsepower Range Coverage, Engine Torque Performance, Transmission Technology Options, Precision Agriculture Integration Depth, Automation and Autonomy Capability, Electrification Readiness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere

CNH Industrial

AGCO Corporation

Kubota North America

Claas of America

Case IH

New Holland Agriculture

Massey Ferguson

Fendt

Versatile

McCormick Tractors North America

LS Tractor USA

TYM North America

Branson Tractors

Kioti Tractor

- Large farms driving high horsepower tractor adoption

- Corporate agribusiness investing in precision tractors

- Contract operators expanding tractor fleets

- Specialty crop producers adopting compact tractors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now