Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Agrochemical Market is valued at approximately USD ~billion based on recent historical assessment, driven primarily by the increasing demand for high-yield crops, advancements in farming technologies, and the need for effective pest control. The market is also supported by governmental policies promoting agricultural productivity and environmental sustainability, fostering the adoption of both traditional and new agrochemical products. The growth of organic farming and precision agriculture technologies further contributes to the expansion of the agrochemical sector, with notable market players focusing on innovating and developing new products to cater to evolving agricultural needs.

The dominant cities and states in the USA’s agrochemical market are primarily located in the Midwest, particularly in states like Iowa, Illinois, and Nebraska. These regions benefit from a strong agricultural base, making them key players in agrochemical consumption. The dominance of these areas is also attributed to their large-scale farming operations, which demand significant agrochemical inputs for crop protection and fertility management. California and Texas are also substantial contributors, with California’s large-scale production of fruits and vegetables and Texas’ diverse agricultural industry driving the demand for various agrochemical products.

Market Segmentation

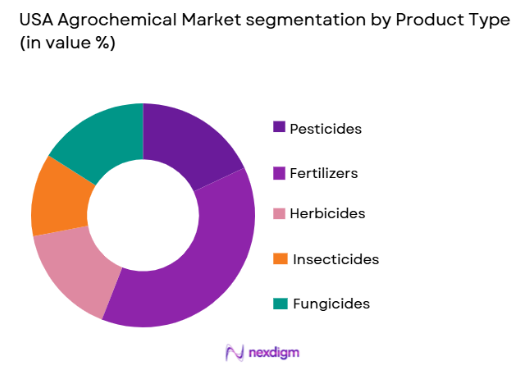

By Product Type:

USA Agrochemical market is segmented by product type into pesticides, fertilizers, herbicides, insecticides, and fungicides. Recently, fertilizers have been the dominant sub-segment, primarily due to the growing need for nutrient management in large-scale agricultural operations. This segment benefits from the rising global food demand, along with increased focus on soil health and crop yield enhancement. Fertilizers are integral to sustaining crop growth and improving productivity, making them essential for agricultural practices in both traditional and organic farming.

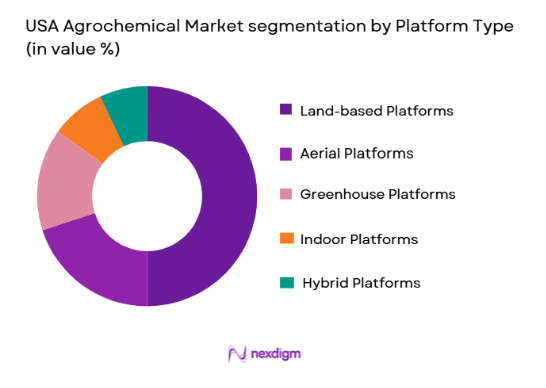

By Platform Type:

USA Agrochemical market is segmented by platform type into land-based platforms, aerial platforms, greenhouse platforms, indoor platforms, and hybrid platforms. Land-based platforms dominate this segment due to the vast expanse of arable land in the USA used for agricultural practices. The ease of application and cost-effectiveness of land-based platforms contribute to their market share, making them ideal for a wide variety of crops. Additionally, technological advancements have made land-based platforms more efficient, improving application accuracy and reducing wastage, further boosting their demand.

Competitive Landscape

The USA agrochemical market is highly competitive, with a few major players dominating the landscape. Market consolidation is evident, as larger corporations continue to acquire smaller firms to expand their product offerings and geographical presence. These companies focus on improving research and development efforts, creating more sustainable and efficient products to address the needs of modern agriculture.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| BASF | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Syngenta | 2000 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DowDuPont | 1897 | USA | ~ | ~ | ~ | ~ | ~ |

| Bayer | 1863 | Germany | ~ | ~ | ~ | ~ | ~ |

| Corteva Agriscience | 2019 | USA | ~ | ~ | ~ | ~ | ~ |

USA Agrochemical Market Analysis

Growth Drivers

Technological Advancements in Crop Protection:

Technological advancements in crop protection are a significant growth driver for the USA agrochemical market. The rise in crop protection technologies, such as precision farming and smart agrochemicals, has led to better management of pests, diseases, and weeds, thus enhancing productivity. The use of drones and remote sensing tools has made it possible to apply agrochemicals more efficiently, reducing the overall usage of chemicals and minimizing environmental impact. Precision agriculture technology also helps farmers in monitoring crop health and optimizing input usage, leading to more sustainable farming practices. The integration of artificial intelligence and machine learning in agrochemical formulations is driving innovation, allowing the development of smarter products that are more effective and less harmful to the environment. These innovations contribute to the increased demand for crop protection products, which in turn drives the overall growth of the market.

Government Policies and Support for Agriculture:

Government policies and subsidies that support agriculture in the USA play a key role in driving the growth of the agrochemical market. Programs designed to support sustainable farming practices and crop yields are particularly influential. These policies encourage the use of agrochemicals to enhance soil health and ensure the protection of crops against pests and diseases. Financial incentives such as subsidies for agrochemical products and agricultural grants further contribute to market growth by reducing the financial burden on farmers. Government-led initiatives to promote sustainable farming methods, such as organic and precision farming, have also increased the use of eco-friendly agrochemicals. Additionally, the increasing focus on food security and the growing global demand for food are pushing the government to foster innovation and investment in the agrochemical sector, driving the market’s expansion.

Market Challenges

Environmental and Regulatory Constraints:

Environmental concerns and stringent regulations are significant challenges for the USA agrochemical market. There is increasing pressure on companies to develop products that are environmentally friendly and comply with rigorous environmental standards. For instance, the EPA (Environmental Protection Agency) continuously updates its regulations concerning pesticide use, ensuring that agrochemicals do not harm non-target species or contribute to soil and water contamination. The compliance with these regulations often involves additional costs for agrochemical manufacturers, affecting profitability. Moreover, the growing public awareness and demand for sustainable farming methods are forcing companies to focus on eco-friendly products, which, while in demand, are more expensive to develop and implement. These environmental and regulatory hurdles restrict the pace at which the market can innovate and expand.

Price Volatility of Raw Materials:

The price volatility of raw materials used in the production of agrochemicals is another significant challenge facing the USA agrochemical market. The cost of key ingredients like petroleum, sulfur, and other chemicals fluctuates due to global market trends, geopolitical tensions, and environmental policies. These price fluctuations impact the overall cost structure of agrochemical products, making it difficult for companies to maintain consistent pricing strategies. Additionally, any sudden increase in raw material costs can result in higher prices for end consumers, affecting demand, especially among small-scale farmers. The increasing costs of transportation and labor also add to the challenges of raw material pricing. These factors combined make it harder for agrochemical companies to maintain margins while ensuring product affordability and accessibility to all segments of the agricultural industry.

Opportunities

Expansion of Organic Agrochemicals:

One of the most significant opportunities for the USA agrochemical market lies in the growing demand for organic agrochemicals. As consumers and farmers become more aware of the environmental impact of traditional agrochemicals, there is an increasing shift towards organic farming. This trend is creating a demand for organic agrochemicals such as biological pesticides and fertilizers that are safer for the environment and human health. The expansion of organic farming in the USA, driven by consumer preferences for organic food products, presents a lucrative opportunity for agrochemical manufacturers to diversify their product offerings. Companies that can innovate and bring sustainable, organic agrochemical solutions to the market are poised to capture a significant share of the growing organic farming sector. The rise in organic certification and government support for organic farming practices further strengthens this opportunity.

Digital Agriculture Solutions:

The rise of digital agriculture is another growing opportunity for the USA agrochemical market. As farmers increasingly adopt precision farming techniques, the demand for digital tools such as sensors, data analytics, and cloud-based solutions is growing. These technologies help farmers optimize their use of agrochemicals by providing real-time data on soil conditions, crop health, and environmental factors. Digital solutions not only improve the efficiency of agrochemical applications but also reduce waste and environmental impact. The integration of artificial intelligence, machine learning, and Internet of Things (IoT) technologies into farming practices is revolutionizing the way agrochemicals are used, offering a significant opportunity for agrochemical companies to develop smart, data-driven products that cater to the needs of modern farmers. Companies investing in digital agriculture technologies are positioned to stay ahead of the curve and tap into a fast-growing market segment.

Future Outlook

The future outlook for the USA agrochemical market is positive, with growth expected to be driven by technological advancements, increasing agricultural productivity, and the growing demand for sustainable farming practices. In the coming years, the market will likely witness further innovations in crop protection technologies, with a focus on precision agriculture, digital tools, and eco-friendly agrochemical solutions. Government policies supporting sustainable agriculture and food security will continue to shape market trends, offering opportunities for growth. The shift towards organic farming and the increasing adoption of digital agriculture solutions will drive demand for innovative and sustainable agrochemical products. Overall, the market is poised for steady growth, driven by a combination of regulatory support, technological innovation, and evolving consumer preferences.

Major Players

- BASF

- Syngenta

- DowDuPont

- Bayer

- Corteva Agriscience

- FMC Corporation

- ADAMA Agricultural Solutions

- Nufarm Limited

- UPL Limited

- Sumitomo Chemical

- Arysta LifeScience

- Haifa Group

- K+S AG

- ICL Group

- Koch Industries

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural producers and farmers

- Agrochemical manufacturers

- Retailers and distributors

- Environmental consultancy firms

- Food processing companies

- Farm equipment manufacturers

Research Methodology

Step 1: Identification of Key Variables

The initial step involved identifying key variables that influence the agrochemical market, such as product types, regional preferences, regulatory frameworks, and technological innovations.

Step 2: Market Analysis and Construction

Data on the agrochemical market was gathered from various primary and secondary sources, including industry reports, government publications, and interviews with market experts.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market trends and forecasts were validated by consulting with industry experts, including agrochemical producers, farmers, and agricultural consultants.

Step 4: Research Synthesis and Final Output

The collected data and expert insights were synthesized to generate comprehensive market analyses, ensuring the final output addressed all relevant factors and accurately predicted future trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Demand for Sustainable Farming Practices

Advancements in Crop Protection Technologies

Government Support for Agrochemical Use in Agriculture

Rising Global Food Demand

Technological Innovations in Agrochemical Formulations - Market Challenges

High Regulatory Compliance Costs

Environmental Impact Concerns

Resistance of Pests to Agrochemicals

Availability of Raw Materials

Price Volatility of Raw Inputs - Market Opportunities

Expansion of Organic and Biologically Derived Agrochemicals

Development of Smart Agrochemical Solutions

Increased Investment in Agrochemical Research & Development - Trends

Growing Adoption of Precision Agriculture

Shift Towards Eco-friendly Agrochemical Alternatives

Rising Integration of Digital Technologies in Agrochemical Applications

Development of Agrochemicals for Climate Resilient Crops

Focus on Improving Agrochemical Efficacy and Safety - Government Regulations & Defense Policy

Environmental Regulations on Agrochemical Use

Pesticide Registration and Compliance Laws

Subsidies and Grants for Eco-friendly Agrochemical Development - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Pesticides

Fertilizers

Herbicides

Insecticides

Fungicides - By Platform Type (In Value%)

Land-based Platforms

Aerial Platforms

Greenhouse Platforms

Indoor Platforms

Hybrid Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Integrated Solutions

Modular Solutions

Hybrid Solutions - By EndUser Segment (In Value%)

Farmers

Agrochemical Manufacturers

Distributors

Agricultural Consultants

Research Institutes - By Procurement Channel (In Value%)

Direct Procurement

Third-party Distributors

Online Bidding Platforms

Government Tenders

Private Sector Procurement - By Material / Technology (In Value%)

Organic Agrochemicals

Synthetic Agrochemicals

Biologicals

Nanotechnology-based Agrochemicals

Smart Agrochemicals

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material / Technology, Regulatory Compliance, Product Innovation, Pricing, Distribution Network)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BASF

Syngenta

DowDuPont

Bayer

Monsanto

Corteva Agriscience

FMC Corporation

ADAMA Agricultural Solutions

Nufarm

UPL Limited

Sumitomo Chemical

Arysta LifeScience

Ishihara Sangyo Kaisha

Haifa Group

K+S AG

- Farmers’ Increasing Preference for High-yield Crops

- Agrochemical Manufacturers’ Investment in Research & Development

- Government’s Role in Regulating Agrochemical Use

- Rise of Agrochemical Distributors and Retailers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now