Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Airbags Market is valued at USD ~ Billion based on a recent historical assessment, supported by data from the National Highway Traffic Safety Administration and the U.S. Department of Transportation regarding vehicle production and safety system installations. Growth is primarily driven by mandatory frontal and side impact safety standards, rising production of light trucks and SUVs, and increasing integration of advanced restraint systems. Technological improvements in inflator modules and occupant detection sensors further reinforce demand across OEM channels.

Automotive manufacturing hubs such as Michigan, Ohio, Kentucky, Alabama, and Texas dominate the USA Airbags Market due to concentrated vehicle assembly plants and supplier networks. These states host major OEM facilities and advanced safety component manufacturing clusters, supported by skilled labor availability and established logistics infrastructure. Strong domestic vehicle production volumes, combined with proximity to cross-border North American supply chains, enable consistent integration of multi-airbag configurations across passenger and commercial vehicle platforms.

Market Segmentation

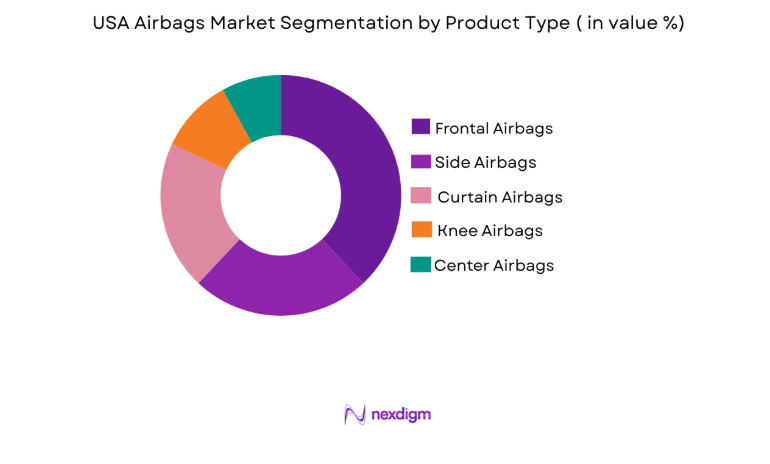

By Product Type

USA Airbags Market is segmented by product type into frontal airbags, side airbags, curtain airbags, knee airbags, and center airbags. Recently, frontal airbags have a dominant market share due to federal safety mandates requiring driver and passenger frontal protection systems in all new vehicles, along with high installation rates across passenger cars, SUVs, and light trucks. Strong OEM compliance requirements established production scalability, and cost-effective manufacturing processes further contribute to sustained dominance across both domestic and imported vehicle models.

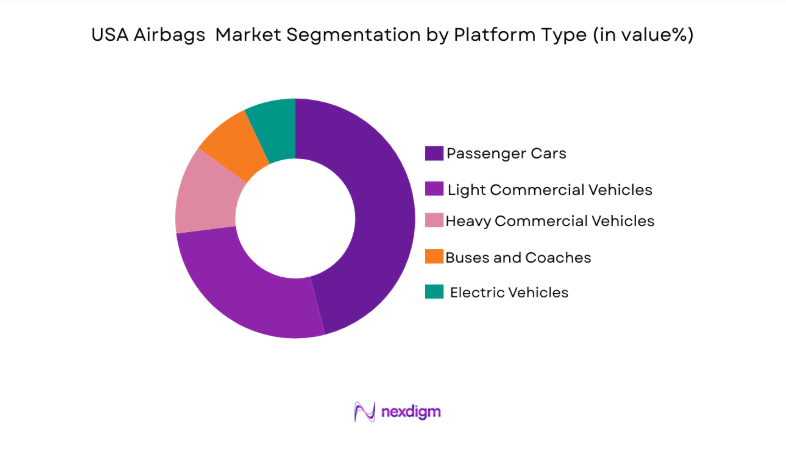

By Platform Type

USA Airbags Market is segmented by platform type into passenger cars, light commercial vehicles, heavy commercial vehicles, buses and coaches, and electric vehicles. Recently, passenger cars have a dominant market share due to the highest production volumes, mandatory multi-airbag installation regulations, and widespread consumer adoption across sedans and SUVs. Established OEM manufacturing ecosystems and safety compliance requirements further reinforce integration density in passenger vehicles compared to commercial and niche mobility platforms.

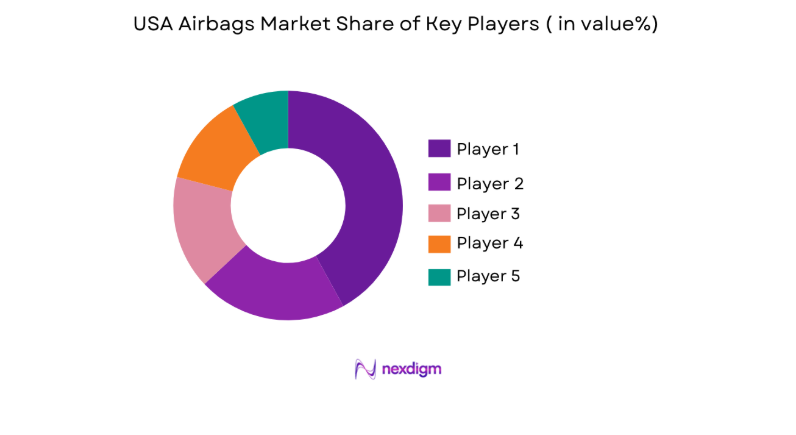

Competitive Landscape

The USA Airbags Market demonstrates moderate consolidation, with established global automotive safety suppliers controlling major OEM contracts and technology platforms. Large multinational players dominate through advanced inflator technologies, integrated sensor systems, and long-term supply agreements with domestic vehicle manufacturers. Competitive positioning is influenced by R&D capabilities, regulatory compliance track records, and manufacturing footprint within North America.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Inflator Technology Capability |

| Autoliv Inc. | 1953 | Sweden | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Joyson Safety Systems | 2018 | USA | ~ | ~ | ~ | ~ | ~ |

| Toyota Gosei Co., Ltd. | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Hyundai Mobis Co., Ltd. | 1977 | South Korea | ~ | ~ | ~ | ~ | ~ |

USA Airbags Market Analysis

Growth Drivers

Stringent Federal Motor Vehicle Safety Regulations and Crash Compliance Mandates

The implementation of strict federal motor vehicle safety standards has significantly accelerated the adoption of advanced airbag systems across all new vehicle categories in the United States. Regulatory bodies require comprehensive occupant protection systems, compelling automakers to integrate multiple airbags as standard features rather than optional upgrades. This regulatory environment increases baseline demand for frontal, side, curtain, and knee airbags in both passenger and commercial vehicles. Automakers must comply with crash test ratings and safety performance benchmarks, which incentivize continuous enhancement of airbag deployment accuracy and reliability. As vehicle safety ratings increasingly influence consumer purchasing decisions, manufacturers allocate higher budgets toward advanced restraint system development. Compliance obligations also reduce the likelihood of minimal safety configurations, strengthening consistent installation volumes across entry-level and premium vehicle segments. Technological integration with electronic control units and crash sensors further raises system complexity, increasing overall airbag system value per vehicle. Collectively, mandatory safety frameworks and enforcement oversight sustain stable demand growth and encourage ongoing innovation within the USA Airbags Market.

Expansion of Light Truck and SUV Production Across Domestic Manufacturing Hubs

The sustained growth in light truck and SUV production across major automotive states has significantly influenced airbag system demand. Consumer preference shifts toward larger vehicles necessitate additional side curtain and multi-point restraint systems due to higher rollover and side-impact protection requirements. Manufacturing facilities in Michigan, Ohio, Kentucky, Alabama, and Texas continue to expand assembly capacities, directly supporting higher installation volumes of integrated airbag modules. Larger vehicle architectures require extended curtain airbags and reinforced deployment mechanisms, increasing system content per unit. OEM investment in upgraded safety platforms aligns with insurance and crash performance standards, encouraging higher-grade airbag configurations. Domestic production growth reduces reliance on imports and strengthens local supplier ecosystems specializing in inflators and textile airbag components. The combination of high production throughput and evolving vehicle safety architecture amplifies airbag integration across mainstream models. This production-driven expansion remains a structural contributor to long-term market growth within the USA Airbags Market.

Market Challenges

Product Recall Risks and Inflator Defect Liabilities

Historical recall events related to defective inflators have created substantial financial and reputational risks for airbag manufacturers operating in the United States. Large-scale recalls impose significant replacement costs, regulatory penalties, and litigation exposure that can disrupt long-term OEM relationships. Compliance investigations often require extensive testing, documentation, and supply chain audits, increasing operational overhead. Manufacturers must allocate substantial resources to quality assurance, material validation, and post-installation monitoring systems to mitigate similar risks. Even isolated component failures can trigger widespread recall mandates due to safety-critical classification of airbags. Insurance premiums and warranty reserves also rise in response to potential liability exposure. This environment increases cost pressures on suppliers while intensifying scrutiny from regulatory agencies and automakers. Persistent recall sensitivity therefore remains a structural challenge affecting profitability and operational stability in the USA Airbags Market.

Volatility in Raw Material and Semiconductor Supply Chains

Airbag production depends heavily on specialized nylon fabrics, propellant chemicals, microcontrollers, and crash sensors, many of which are exposed to global supply chain disruptions. Price volatility in petrochemical derivatives used in nylon weaving can significantly affect manufacturing margins. Semiconductor shortages impact electronic control units that regulate deployment timing and occupant sensing, creating production bottlenecks. Geopolitical trade tensions and transportation constraints may delay inflator components and precision metal housings required for assembly. Automotive OEMs demand strict delivery schedules, leaving limited tolerance for supply interruptions. Suppliers must diversify sourcing networks and maintain strategic inventory buffers, increasing capital requirements. Currency fluctuations further complicate procurement strategies for imported components. These combined supply uncertainties represent a persistent operational challenge influencing cost structures and production continuity in the USA Airbags Market.

Opportunities

Integration of Smart Airbags with Advanced Occupant Sensing Systems

The evolution of vehicle interior intelligence systems creates opportunities for next-generation smart airbags capable of adaptive deployment. Modern vehicles increasingly incorporate occupant detection sensors, seat position monitors, and weight classification systems that allow tailored airbag inflation levels. Integrating airbags with these intelligent systems enhances passenger protection while reducing injury risks associated with improper deployment. Automakers investing in connected vehicle platforms require harmonized safety modules capable of real-time communication with electronic control units. This demand stimulates research into predictive crash algorithms and data-driven deployment calibration. Smart airbag development also aligns with consumer expectations for technologically advanced safety features in premium and electric vehicles. Suppliers that pioneer integrated sensing and deployment solutions can secure long-term OEM partnerships. As digital vehicle architecture becomes more sophisticated, intelligent airbag systems represent a substantial growth opportunity within the USA Airbags Market.

Expansion of Airbag Deployment in Rear Seats and Emerging Vehicle Segments

Increasing regulatory and consumer focus on rear-seat passenger safety provides a new avenue for airbag system expansion. Historically, frontal protection received primary emphasis, but safety assessments now consider rear occupant injury mitigation more comprehensively. This shift encourages deployment of center airbags and advanced curtain systems covering extended cabin zones. Electric and autonomous vehicle concepts also introduce new seating configurations that require innovative airbag placement and deployment strategies. OEM experimentation with swivel seats and flexible cabin layouts creates demand for modular restraint systems adaptable to unconventional interiors. As mobility platforms diversify, safety architectures must evolve correspondingly. Manufacturers capable of designing versatile deployment modules for varied cabin geometries gain competitive advantage. These emerging vehicle design trends offer meaningful long-term growth potential in the USA Airbags Market.

Future Outlook

Over the next five years, the USA Airbags Market is expected to witness steady expansion driven by advanced safety regulations, increased SUV production, and integration with intelligent vehicle systems. Technological advancements in smart inflators and adaptive deployment algorithms will enhance system efficiency and passenger protection. Regulatory reinforcement of occupant safety standards will continue to mandate higher airbag counts per vehicle. Growing electric vehicle manufacturing and evolving cabin configurations are likely to stimulate innovation in next-generation airbag solutions.

Major Players

- Autoliv Inc.

- ZF Friedrichshafen AG

- Joyson Safety Systems

- Toyoda Gosei Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Daicel Corporation

- Nihon Plast Co., Ltd.

- Ashimori Industry Co., Ltd.

- ARC Automotive Inc.

- Toray Industries, Inc.

- Kolon Industries, Inc.

- Yanfeng International Automotive Technology Co., Ltd.

Key Target Audience

- Passenger vehicle OEMs

- Commercial vehicle OEMs

- Electric vehicle manufacturers

- Tier-1 automotive system integrators

- Automotive safety regulators and certification bodies

- Automotive aftermarket and replacement parts distributors

- Autonomous and ADAS technology developers

Research Methodology

Step 1: Identification of Key Variables

Primary variables such as vehicle production volume, safety regulation mandates, and airbag installation rates were identified. Secondary variables included technology adoption levels and regional manufacturing concentration.

Step 2: Market Analysis and Construction

Historical vehicle production and safety compliance data were analyzed to construct the overall market size. Integration rates per vehicle category were mapped against pricing structures to estimate total market valuation.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, OEM procurement specialists, and safety system engineers were consulted to validate assumptions. Cross-verification ensured consistency across production data and installation metrics.

Step 4: Research Synthesis and Final Output

Validated data points were consolidated into structured market segments. Analytical frameworks were applied to derive insights on growth patterns, competition, and future demand dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Stringent Federal Motor Vehicle Safety Standards enforcement

Increasing adoption of advanced driver assistance systems integration

Rising penetration of multi-airbag configurations in SUVs and pickups

Expansion of electric vehicle manufacturing capacity

Continuous innovation in lightweight inflator technologies - Market Challenges

High recall risks associated with inflator defects

Volatility in raw material prices for nylon and propellants

Complex compliance requirements across federal and state regulations

Supply chain disruptions affecting semiconductor-based crash sensors

Pricing pressure from OEM contract negotiation - Market Opportunities

Integration of smart airbags with occupant sensing systems

Expansion of center and rear-seat airbag deployment

Development of lightweight, eco-friendly inflator materials - Trends

Shift toward adaptive multi-stage deployment systems

Integration of airbag control units with ADAS platforms

Rising adoption of pedestrian protection airbags

Increasing focus on lightweight material engineering

Digital simulation and crash analytics in airbag design - Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standard compliance mandates

National Highway Traffic Safety Administration crash test protocols

Vehicle occupant protection guidelines for advanced restraint systems - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Frontal Airbag Systems

Side Impact Airbag Systems

Curtain Airbag Systems

Knee Airbag Systems

Center Airbag Systems - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Hybrid Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Replacement Systems

Modular Integrated Systems

Retrofit Safety Systems

Adaptive Multi-Stage System - By EndUser Segment (In Value%)

Passenger Vehicle Owners

Fleet Operators

Automotive OEMs

Aftermarket Service Providers

Commercial Transport Operators - By Procurement Channel (In Value%)

Direct OEM Contracts

Supplier Agreements

Aftermarket Distribution Networks

Online Automotive Parts Platforms

Government Fleet Procurement Programs - By Material / Technology (in Value %)

Pyrotechnic Inflator Systems

Hybrid Inflator Systems

Cold Gas Inflator Systems

Silicone-Coated Nylon Fabric Airbags

Advanced Crash Sensor Modules

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Portfolio Breadth, Inflator Technology Type, OEM Contract Strength, Manufacturing Footprint, R&D Capability, Regulatory Compliance Record, Pricing Strategy, Distribution Network, Aftermarket Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Autoliv Inc.

ZF Friedrichshafen AG

Joyson Safety Systems

Toyota Gosei Co., Ltd.

Hyundai Mobis Co., Ltd.

Nihon Plast Co., Ltd.

Ashimori Industry Co., Ltd.

ARC Automotive Inc.

Daicel Corporation

Toyoda Gosei North America Corporation

Key Safety Systems Inc.

Takata Corporation

Faurecia SE

Continental AG

Bosch Automotive Systems

- Automotive OEMs prioritizing integrated safety architecture

- Fleet operators demanding cost-effective replacement systems

- Electric vehicle manufacturers incorporating advanced restraint modules

- Aftermarket distributors expanding multi-brand airbag portfolios

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now