Download PDF

Download PDFMarket Overview

The USA ANA Testing Market is experiencing significant growth, driven by the increasing prevalence of autoimmune diseases, advancements in diagnostic technologies, and a rising focus on early diagnosis. Based on a recent historical assessment, the market is valued at USD ~ billion in 2024. The demand for ANA testing is influenced by factors such as the growing geriatric population and improved healthcare infrastructure. These factors are further supported by advancements in lab-based technologies, point-of-care devices, and innovations in testing platforms, which drive the expansion of the ANA testing market.

The USA remains the dominant player in the ANA testing market due to its established healthcare infrastructure, high healthcare expenditure, and the presence of leading diagnostic laboratories. The demand is particularly concentrated in states like California, New York, and Florida, where there is a high prevalence of autoimmune disorders, leading to an increased need for accurate diagnostic testing. Additionally, the integration of advanced technology solutions such as artificial intelligence (AI) and machine learning for testing has helped maintain the USA’s dominance in the market.

Market Segmentation

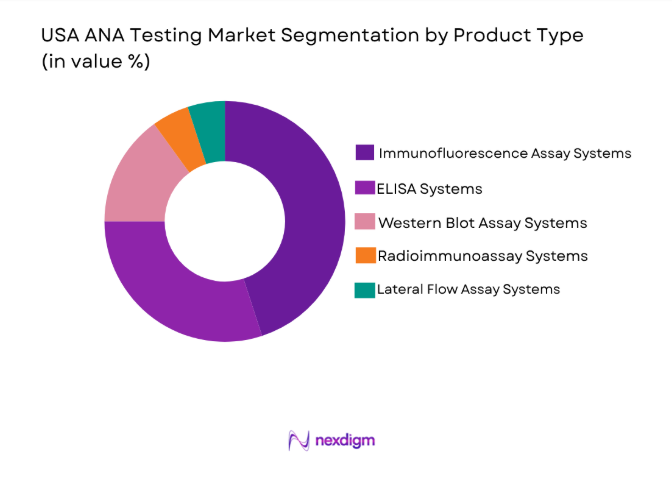

By Product Type

The USA ANA Testing market is segmented by product type into immunofluorescence assay systems, enzyme-linked immunosorbent assay (ELISA) systems, and Western blot assay systems. Recently, immunofluorescence assay systems have been dominating the market share due to their high accuracy and ability to detect a wide range of autoimmune diseases. These systems are widely preferred by diagnostic laboratories because they provide rapid and reliable results. Additionally, advancements in fluorescence detection technologies have further enhanced their popularity, making them the go-to choice for healthcare providers. The combination of high sensitivity and broad applicability to autoimmune conditions has ensured immunofluorescence assay systems’ leadership in the ANA testing market.

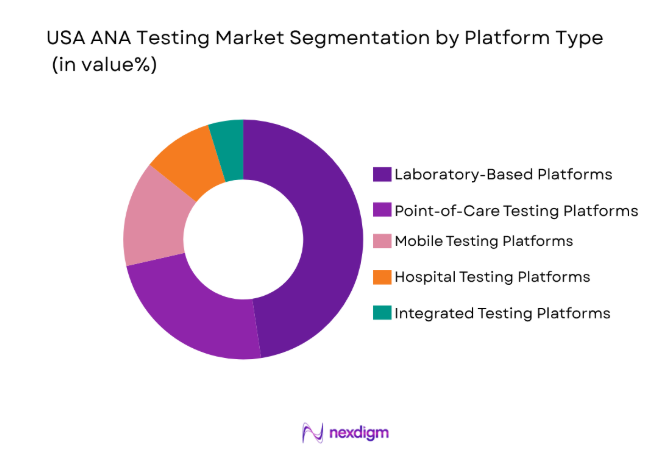

By Platform Type

The USA ANA Testing market is segmented by platform type into laboratory-based platforms, point-of-care testing platforms, mobile testing platforms, hospital testing platforms, and integrated testing platforms. Recently, laboratory-based platforms have dominated the market share due to their high throughput capacity and advanced diagnostic capabilities. These platforms are typically used in large diagnostic laboratories and hospitals, offering the ability to perform multiple tests with high accuracy. Their ability to deliver reliable and detailed results makes them the preferred choice for healthcare providers. As advancements in diagnostic technology continue, the demand for laboratory-based platforms is expected to increase further, solidifying their dominance in the ANA testing market.

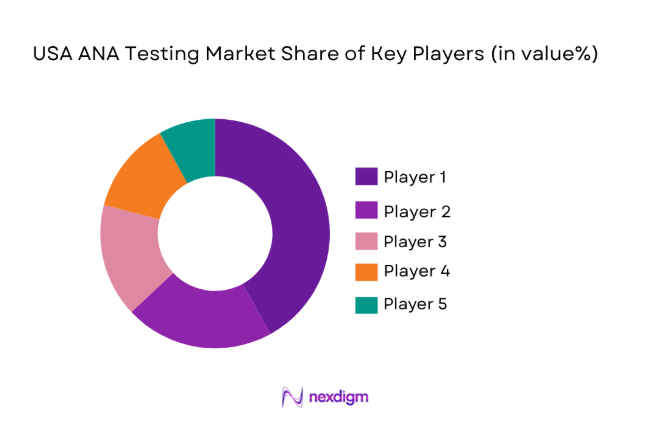

Competitive Landscape

The competitive landscape of the USA ANA Testing market is characterized by major players consolidating their market share through continuous innovations, acquisitions, and strategic partnerships. Key players in the market are investing heavily in developing advanced testing solutions, particularly those incorporating artificial intelligence and automation to improve accuracy and speed. These companies are also focused on expanding their product portfolios to address the growing demand for personalized and point-of-care diagnostic solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Market-Specific Parameter |

| Thermo Fisher Scientific | 1956 | Waltham, MA | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | Abbott Park, IL | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Basel, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| Bio-Rad Laboratories | 1952 | Hercules, CA | ~ | ~ | ~ | ~ | ~ |

USA ANA Testing Market Analysis

Growth Drivers

Rising Prevalence of Autoimmune Diseases

The rising prevalence of autoimmune diseases such as lupus, rheumatoid arthritis, and scleroderma is a primary driver for the growth of the ANA testing market. With an increasing number of diagnosed cases, the demand for accurate and reliable diagnostic tests has surged. Autoimmune diseases are often complex and difficult to diagnose, making early detection crucial. ANA testing has proven to be a key diagnostic tool for clinicians, offering a sensitive and specific method for detecting autoimmune disorders. This growing need for early and accurate detection is driving the demand for ANA testing across the USA. As awareness about autoimmune diseases continues to rise, the market for ANA testing will likely expand further, encouraging investments and innovations in testing platforms.

Technological Advancements in Diagnostic Testing

Technological advancements, particularly in AI and machine learning, are enhancing the diagnostic accuracy and efficiency of ANA testing. These innovations enable laboratories to process and analyze test results faster and with greater precision. Additionally, automation in the laboratory setting is reducing human error and improving operational efficiency. As AI-based tools are increasingly integrated into ANA testing, the market is witnessing a surge in demand for advanced diagnostic solutions. These technological advancements are not only improving test performance but also contributing to cost reduction, making ANA testing more accessible to healthcare providers and patients alike. The continuous development in this field is expected to significantly propel market growth over the coming years.

Market Challenges

High Cost of Diagnostic Tests

One of the major challenges in the USA ANA Testing market is the high cost associated with diagnostic tests, especially when using advanced technologies such as immunofluorescence and molecular diagnostics. These tests are often expensive due to the specialized equipment and reagents required. Additionally, the need for highly skilled personnel to perform and interpret tests increases the overall cost of testing. This poses a significant barrier for healthcare providers, particularly in low-resource settings, and can limit the widespread adoption of ANA testing. While insurance coverage may offset some of these costs, out-of-pocket expenses can still be burdensome for patients, leading to reduced test utilization.

Regulatory and Compliance Issues

The USA ANA Testing market faces significant regulatory and compliance challenges, particularly with the approval and validation of new diagnostic assays. The FDA’s stringent regulatory requirements for diagnostic tests can delay the introduction of new products into the market. Additionally, as new technologies, such as AI-powered diagnostic tools, are being developed, regulatory bodies face challenges in creating frameworks to assess their safety and effectiveness. These regulations are essential for ensuring patient safety but can slow down the pace of innovation and market expansion. Moreover, ensuring that diagnostic products meet various state-level requirements further complicates market entry for new companies.

Opportunities

Expansion of Point-of-Care Testing Solutions

The increasing demand for point-of-care (POC) testing solutions presents a significant opportunity for growth in the USA ANA Testing market. POC testing allows patients to receive diagnostic results quickly, often without the need to visit a laboratory. This is particularly important for patients in remote areas or those with limited access to healthcare facilities. Additionally, POC solutions offer healthcare providers the ability to make immediate clinical decisions based on test results, improving patient outcomes. As the technology continues to advance, POC testing is expected to gain further market traction, driving the growth of the ANA testing market by enabling faster and more accessible diagnostic options.

Strategic Partnerships with Biopharmaceutical Companies

Collaborations between diagnostic companies and biopharmaceutical firms present a unique opportunity for growth in the USA ANA Testing market. These partnerships can accelerate the development of innovative testing solutions tailored to specific autoimmune diseases. By combining the expertise of diagnostic companies in testing technology with the research and development capabilities of biopharmaceutical firms, new diagnostic tools that are both highly accurate and cost-effective can be brought to market. Furthermore, these collaborations can help in addressing unmet medical needs in the autoimmune disease space, further driving the demand for ANA testing and positioning companies for success in a rapidly evolving market.

Future Outlook

The future outlook of the USA ANA Testing market is positive, with continued growth expected due to advancements in technology, increased awareness of autoimmune diseases, and an expanding patient population. The market is anticipated to witness further innovation in diagnostic platforms, with a shift towards AI and machine learning integration to enhance testing accuracy and speed. Regulatory support for advanced diagnostic technologies and the rising demand for personalized medicine will further bolster the market’s expansion. Technological advancements will also lead to more affordable testing options, improving accessibility and adoption across the country.

Major Players

- Thermo Fisher Scientific

- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Bio-Rad Laboratories

- Quest Diagnostics

- Laboratory Corporation of America

- Danaher Corporation

- Cepheid

- Sysmex Corporation

- Hewlett Packard Enterprise

- GE Healthcare

- Beckman Coulter

- Agilent Technologies

- Mindray

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals

- Diagnostic laboratories

- Research institutions

- Healthcare providers

- Biopharmaceutical companies

Research Methodology

Step 1: Identification of Key Variables

The key variables impacting the market, such as autoimmune disease prevalence and diagnostic technologies, are identified.

Step 2: Market Analysis and Construction

A comprehensive analysis of market trends, technological advancements, and regulatory factors is conducted.

Step 3: Hypothesis Validation and Expert Consultation

Insights from experts in the diagnostics and healthcare sectors are gathered to validate the research hypothesis.

Step 4: Research Synthesis and Final Output

Data from primary and secondary research sources are synthesized into the final market report, offering actionable insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Prevalence of Autoimmune Diseases

Advancements in Diagnostic Technology

Government Initiatives for Healthcare Improvement - Market Challenges

High Cost of Diagnostic Tests

Lack of Skilled Labor for Advanced Testing

Stringent Regulatory Guidelines - Market Opportunities

Expansion of Point-of-Care Testing Solutions

Partnerships with Biopharmaceutical Companies

Rising Adoption of Home Testing Kits - Trends

Integration of Artificial Intelligence in Diagnostics

Shift Towards Personalized Medicine - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Immunofluorescence Assay Systems

Enzyme-Linked Immunosorbent Assay (ELISA) Systems

Western Blot Assay Systems

Radioimmunoassay Systems

Lateral Flow Assay Systems - By Platform Type (In Value%)

Laboratory-Based Platforms

Point-of-Care Testing Platforms

Home Testing Platforms

Mobile Testing Platforms

Hospital Testing Platforms - By Fitment Type (In Value%)

On-Premise Solutions

Cloud-Based Solutions

Hybrid Solutions

Modular Solutions - By End User Segment (In Value%)

Hospitals

Diagnostic Laboratories

Research Institutes

Physician Offices

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Price, Technology Integration, Market Reach)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Thermo Fisher Scientific

Abbott Laboratories

Roche Diagnostics

Siemens Healthineers

Bio-Rad Laboratories

Quest Diagnostics

Laboratory Corporation of America

Danaher Corporation

Cepheid

Sysmex Corporation

Hewlett Packard Enterprise

GE Healthcare

Beckman Coulter

Agilent Technologies

Mindray

- Increasing Adoption of ANA Testing in Hospitals

- Shift Towards Diagnostic Laboratories for Testing

- Growing Demand in Research Institutes

- Rising Number of Physician Offices Offering Testing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now