Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Bumpers market current size stands at around USD ~ million, reflecting steady demand anchored in vehicle production cycles, collision repair frequency, and model refresh activity across passenger and commercial segments. The market structure is shaped by OEM program sourcing, tiered supplier manufacturing, and aftermarket replacement flows tied to insurance-driven repairs. Product differentiation centers on lightweight materials, integrated safety features, and styling requirements aligned with evolving vehicle architectures and electrification pathways.

Demand concentration is strongest across major automotive manufacturing corridors and logistics hubs where assembly plants, molding facilities, and repair networks co-locate. High vehicle density metros drive replacement intensity through collision incidence and cosmetic upgrades. The ecosystem maturity benefits from established tooling clusters, resin supply availability, and testing infrastructure. Policy environments emphasizing safety compliance and domestic manufacturing incentives reinforce localized production footprints and supplier partnerships across the national automotive value chain.

Market Segmentation

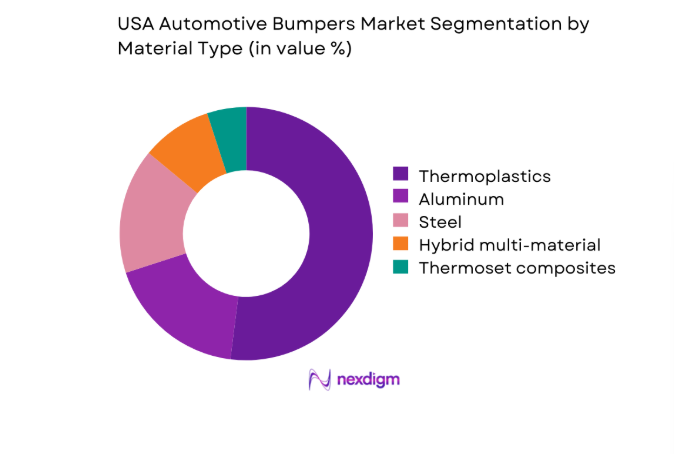

By Material Type

Thermoplastics dominate adoption due to design flexibility, paintability, and compatibility with integrated sensor housings required for advanced safety systems. Aluminum and steel retain relevance in reinforcement structures where impact performance and stiffness targets are critical. Hybrid multi-material architectures are increasingly specified to balance lightweighting with durability, especially in electric vehicle platforms. Thermoset composites find niche use in premium styling applications and performance trims. Material selection is driven by crash performance requirements, tooling economics, recyclability mandates, and OEM preferences for modular bumper systems that support platform commonality across multiple vehicle models.

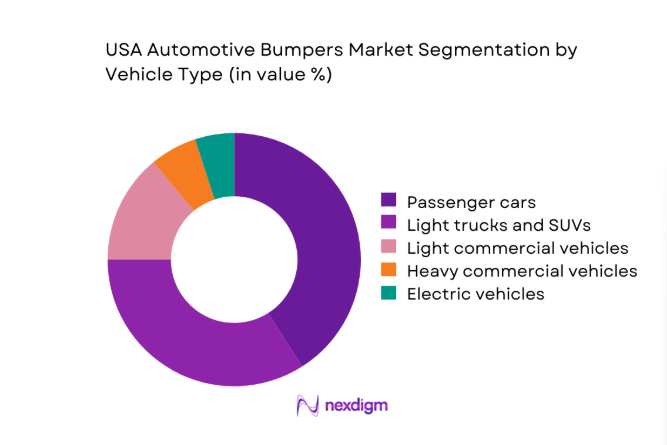

By Vehicle Type

Passenger cars and light trucks account for the majority of bumper installations due to high model turnover and repair frequency in urban corridors. Light commercial vehicles contribute steady replacement demand from fleet operations, last-mile delivery, and municipal services. Heavy commercial vehicles represent a smaller base but require reinforced bumper systems for durability in logistics operations. Electric vehicles are a fast-rising segment, driving redesign of bumper fascias to accommodate sensor integration and aerodynamic optimization. Vehicle mix shifts influence tooling investments, module complexity, and aftermarket stocking strategies across distribution channels.

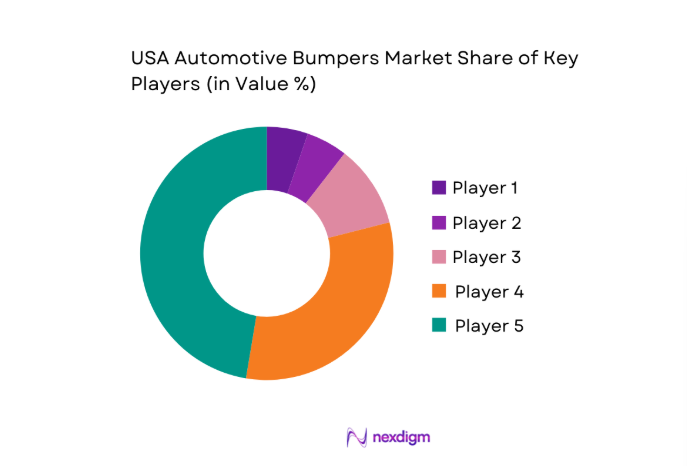

Competitive Landscape

The competitive landscape is shaped by vertically integrated suppliers with strong OEM program coverage and regional manufacturing footprints aligned to assembly plant clusters. Differentiation centers on material science capability, tooling speed, and readiness for sensor-integrated fascia designs. Channel strength in aftermarket networks supports recurring replacement volumes and service responsiveness across collision repair ecosystems.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ | ~ |

| Plastic Omnium | 1946 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Flex-N-Gate | 1956 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Faurecia | 1914 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Hyundai Mobis | 1977 | South Korea | ~ | ~ | ~ | ~ | ~ | ~ |

USA Automotive Bumpers Market Analysis

Growth Drivers

Rising vehicle parc and collision repair frequency in urban markets

Urbanization and vehicle density across major metropolitan corridors continue to elevate collision incidence, supporting recurring bumper replacement demand. Department of Transportation records show over 4200000 police-reported crashes in 2022, with urban counties accounting for the majority of minor impact events requiring fascia replacement. Insurance claim processing times improved in 2023 with average repair cycle days declining from 18 to 15 due to digital appraisal adoption. In 2024, registered vehicles surpassed 280000000 nationwide, intensifying exposure in dense commuting zones. Municipal traffic volumes rebounded post-pandemic with average weekday vehicle miles traveled exceeding 3200000000 in 2023, sustaining repair throughput capacity.

Stricter federal crash safety and pedestrian protection standards

Federal Motor Vehicle Safety Standards revisions and pedestrian safety guidance have expanded bumper performance requirements, driving redesign cycles. In 2022, updated impact testing protocols incorporated lower-legform assessments across additional vehicle categories, prompting OEM validation programs exceeding 120 test iterations per platform. National Highway Traffic Safety Administration compliance audits increased inspection frequency in 2023 with over 900 conformity assessments across safety components. By 2024, pedestrian fatality counts exceeded 7700 nationally, intensifying regulatory scrutiny and accelerating adoption of energy-absorbing structures and deformable fascias. Engineering change orders per model increased above 40 annually, reinforcing continuous bumper system reengineering pipelines.

Challenges

Volatility in resin and aluminum input costs impacting margins

Feedstock volatility disrupts procurement planning for molded bumper components and reinforcements. Petrochemical price indices recorded monthly swings exceeding 20 points across 2022 and 2023, while aluminum benchmark spreads fluctuated across 1800 to 2600 per metric ton ranges during 2022–2024. Port congestion episodes in 2023 extended average lead times from 45 to 72 days for imported resins, forcing buffer inventory increases. Domestic smelting capacity utilization hovered near 70 in 2024, tightening spot availability. These dynamics complicate contract pricing, elevate working capital cycles beyond 60 days, and pressure suppliers to renegotiate supply agreements frequently.

Complexity of integrating sensors without compromising impact performance

ADAS proliferation increases engineering complexity within bumper fascias. In 2023, over 180 vehicle models sold domestically included forward radar or camera modules embedded behind bumper covers, up from 120 in 2022. Sensor alignment tolerances narrowed to within 2 millimeters for calibration stability, increasing tooling precision requirements. Validation cycles expanded with combined environmental and impact testing exceeding 600 hours per program in 2024. Road salt exposure rates in northern states reached 130 pounds per lane mile annually, elevating corrosion risk for sensor housings. These constraints raise rework rates above 3 per 100 assemblies during pilot builds.

Opportunities

Adoption of recyclable and bio-based polymer bumper materials

Sustainability mandates and OEM decarbonization targets create momentum for recyclable and bio-based polymers in exterior modules. In 2022, recycled polymer content in automotive exteriors averaged below 10, while pilot programs in 2024 achieved 25 content across selected fascia programs. State-level extended producer responsibility initiatives expanded to over 6 jurisdictions by 2024, incentivizing circular material pathways. Corporate climate disclosures now track scope 3 materials intensity annually, with more than 400 automotive suppliers reporting reductions in 2023. Recycling facility throughput for automotive-grade plastics increased by 2 facilities nationwide in 2024, enabling scalable sourcing for bumper applications.

Growth in sensor-ready modular bumper platforms for ADAS-equipped vehicles

Standardized modular fascias that accommodate radar and camera housings offer scalable program wins as ADAS penetration accelerates. In 2023, Level 2 driver assistance features were present on more than 70 new nameplates sold domestically, rising from 52 in 2022. Calibration bay counts at certified repair centers increased from 3400 in 2022 to over 5100 in 2024, supporting post-collision sensor realignment. Federal safety campaigns documented 12 technology updates to automated braking guidelines in 2024, driving OEM refresh cycles. Modularization shortens tooling changeovers from 26 weeks to 14, improving platform rollout speed.

Future Outlook

The market outlook through 2030 reflects continued platform redesign cycles, deeper integration of sensing technologies, and material transitions aligned with sustainability mandates. Regional manufacturing footprints are expected to expand near assembly clusters, while aftermarket channels professionalize calibration and pre-painted module offerings. Policy-driven safety updates and electrification pathways will sustain engineering change frequency.

Major Players

- Magna International

- Plastic Omnium

- Flex-N-Gate

- Faurecia

- Hyundai Mobis

- Toyoda Gosei

- Gestamp

- Valeo

- Tong Yang Group

- Motherson Group

- SRG Global

- CIE Automotive

- Ningbo Joyson Automotive Systems

- Sankei Industry

- Bumper USA Inc.

Key Target Audience

- Automotive OEM procurement and engineering teams

- Tier-1 and Tier-2 component manufacturers

- Collision repair networks and certified calibration centers

- Automotive aftermarket distributors and retailers

- Insurance claims and fleet management operators

- Investments and venture capital firms

- Government and regulatory bodies with agency names

- Logistics and industrial tooling providers

Research Methodology

Step 1: Identification of Key Variables

Product architectures, material pathways, safety compliance requirements, and channel structures were mapped to define the analytical framework. Program sourcing cycles and platform refresh timelines were delineated to anchor demand drivers. Regulatory checkpoints and validation protocols were enumerated to structure compliance assessment.

Step 2: Market Analysis and Construction

Primary operational indicators across production, repair throughput, and technology penetration were synthesized to construct demand scenarios. Supply-side capability mapping captured tooling readiness, material access, and calibration infrastructure. Scenario logic aligned platform cadence with replacement cycles.

Step 3: Hypothesis Validation and Expert Consultation

Engineering leads, repair network operators, and compliance specialists reviewed assumptions on integration complexity and modularization benefits. Feedback loops refined impact pathways for sustainability materials and ADAS packaging. Iterative validation improved scenario robustness.

Step 4: Research Synthesis and Final Output

Findings were consolidated into actionable insights across demand, supply, and regulatory dimensions. Cross-functional implications for procurement, design, and aftermarket readiness were synthesized. The final output prioritized decision-relevant narratives.

- Executive Summary

- Research Methodology (Market Definitions and bumper system scope mapping, OEM and Tier-1 supplier shipment tracking, aftermarket replacement and collision repair channel surveys, teardown and bill of materials cost modeling, material and resin price benchmarking, regulatory and safety standard compliance analysis)

- Definition and Scope

- Market evolution

- Usage and replacement pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising vehicle parc and collision repair frequency in urban markets

Stricter federal crash safety and pedestrian protection standards

OEM lightweighting initiatives to improve fuel economy and EV range

Increasing integration of ADAS sensors and camera modules into bumpers

Growth of EV production requiring redesigned bumper architectures

Rising customization demand in pickup trucks and SUVs - Challenges

Volatility in resin and aluminum input costs impacting margins

Complexity of integrating sensors without compromising impact performance

Higher tooling and capex for multi-material bumper systems

Supply chain disruptions for molded plastics and reinforcements

Stringent homologation and testing requirements increasing time-to-market

Price sensitivity in aftermarket replacement channels - Opportunities

Adoption of recyclable and bio-based polymer bumper materials

Growth in sensor-ready modular bumper platforms for ADAS-equipped vehicles

Expansion of domestic manufacturing to reduce import dependence

Rising demand for lightweight bumpers in EV and hybrid platforms

Aftermarket premiumization through painted and pre-assembled bumper kits

Partnerships with collision repair networks for preferred supplier status - Trends

Shift toward multi-material and modular bumper architectures

Increased integration of radar, lidar, and camera housings in bumper fascias

Use of simulation-driven crash optimization in bumper design

Growth of pre-painted bumper assemblies for faster repair cycles

Localization of tooling and molding capacity in the US

Design convergence between aesthetic styling and safety performance - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis|

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Material Type (in Value %)

Thermoplastics

Thermoset composites

Steel

Aluminum

Hybrid multi-material structures - By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Heavy commercial vehicles

Electric vehicles - By Bumper Type (in Value %)

Front bumpers

Rear bumpers

Energy absorbers and reinforcements - By Sales Channel (in Value %)

OEM fitment

Aftermarket replacement

Collision repair networks - By Application Technology (in Value %)

Conventional impact bumpers

Pedestrian safety-compliant bumpers

Sensor-integrated ADAS bumpers

Lightweight aerodynamic bumper systems

- Market structure and competitive positioning

Market share snapshot of major players| - Cross Comparison Parameters (manufacturing footprint, OEM program coverage, material technology capability, ADAS integration readiness, cost competitiveness, quality and defect rates, tooling and design lead time, aftermarket channel reach)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Magna International

Faurecia (Forvia)

Plastic Omnium

Flex-N-Gate

Gestamp

Valeo

Toyoda Gosei

Tong Yang Group

Motherson Group

Hyundai Mobis

Ningbo Joyson Automotive Systems

CIE Automotive

Sankei Industry

SRG Global

Bumper USA Inc.

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now