Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Cameras market is part of the broader automotive sensing and safety ecosystem and exhibits substantial economic value in USD terms driven by advanced driver‑assistance systems (ADAS) and vehicle safety regulations. Based on a recent historical assessment, the North America Automotive Camera Market was valued around USD ~ billion in 2024, with the United States accounting for the majority of that regional figure due to rapid adoption of multi‑camera systems for parking assistance, surround view, blind‑spot detection and collision avoidance functions. Growing OEM integration and aftermarket upgrades support this market valuation.

Based on a recent historical assessment, the United States remains the dominant regional market for automotive cameras, propelled by stringent safety regulations such as mandated rear‑view cameras and rising consumer demand for vehicle safety technology. Michigan’s automotive manufacturing base and OEM clusters anchor production and R&D, while states like California and Texas drive adoption through high vehicle sales, autonomous vehicle testing ecosystems, and strong aftermarket service networks. The combination of regulatory support, advanced manufacturing infrastructure, and consumer preference for safety features underpins U.S. leadership in automotive camera deployment.

Market Segmentation

By System Type

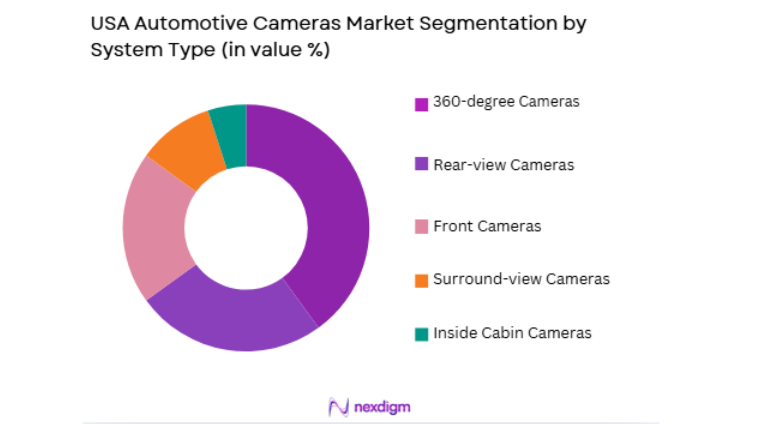

USA Automotive Cameras market is segmented by system type into rear-view cameras, 360-degree cameras, front cameras, surround-view cameras, and inside cabin cameras. Recently, 360-degree cameras have gained dominant market share due to increasing consumer demand for enhanced safety features in modern vehicles. These cameras provide a comprehensive view around the vehicle, significantly improving parking and maneuvering capabilities. Their integration with other ADAS functions, such as object detection and collision prevention, has driven widespread adoption, particularly in premium and autonomous vehicles.

By Platform Type

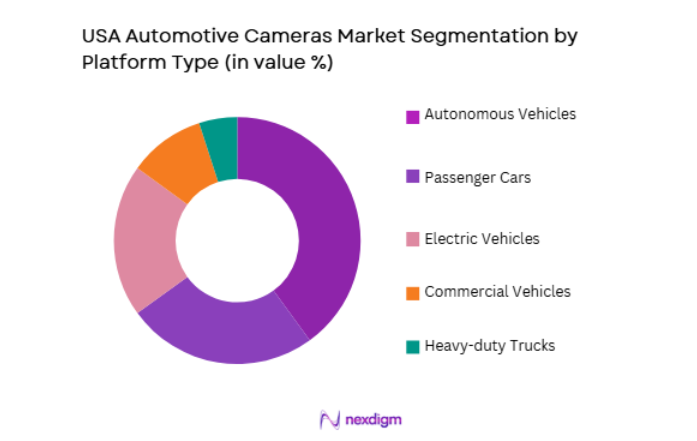

USA Automotive Cameras market is segmented by platform type into passenger cars, commercial vehicles, electric vehicles, autonomous vehicles, and heavy-duty trucks. Autonomous vehicles are dominating the market, driven by the growing demand for self-driving cars and advanced safety technologies. The integration of automotive cameras into autonomous driving systems is crucial for object detection, environment mapping, and ensuring the vehicle’s safe navigation in complex scenarios. As regulatory frameworks evolve to support autonomous vehicles, the adoption of automotive cameras in this segment is expected to expand rapidly.

Competitive Landscape

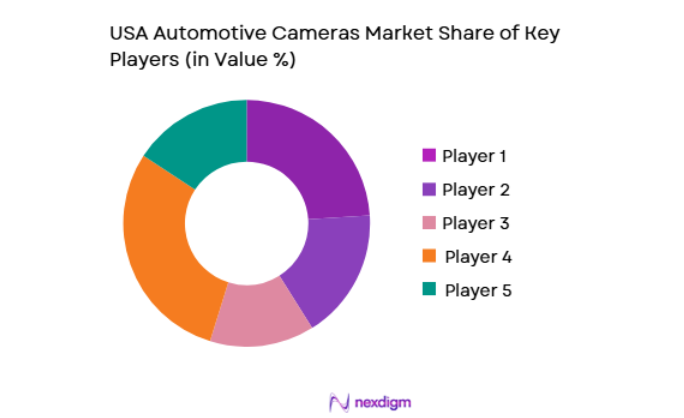

The USA Automotive Cameras market is highly competitive, with significant consolidation driven by key players like Bosch, Valeo, and Continental AG, who offer comprehensive automotive camera solutions. These companies leverage strategic partnerships, innovation in camera resolution, and integration with ADAS to strengthen their market position. Increasing demand for autonomous vehicles and enhanced vehicle safety continues to drive innovation and market consolidation. Smaller players are also emerging, focusing on specialized camera systems and niche applications.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) |

| Bosch | 1886 | Stuttgart, Germany | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Hanover, Germany | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Aurora, Ontario | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1999 | Dublin, Ireland | ~ | ~ | ~ | ~ |

USA Automotive Cameras Market Analysis

Growth Drivers

Increasing Demand for Vehicle Safety Systems

The increasing demand for advanced driver-assistance systems (ADAS) is a primary growth driver for the USA automotive cameras market. As safety regulations become stricter and consumers demand more comprehensive safety features, vehicle manufacturers are incorporating more cameras into their vehicles. These cameras play a critical role in assisting with parking, collision avoidance, and blind-spot detection, enhancing both safety and driver comfort. The rise of autonomous vehicles further fuels this demand, as cameras are essential for vehicle navigation and obstacle detection. Additionally, regulatory agencies in the U.S. are implementing laws that require certain safety features, such as rear-view cameras, further contributing to market growth. As technology advances, the role of automotive cameras will continue to expand in ensuring vehicle safety and enhancing overall driving experience.

Technological Advancements in Camera Systems

Technological advancements in camera resolution, artificial intelligence (AI), and image processing have been instrumental in the growth of the USA automotive cameras market. The integration of AI with automotive cameras allows for improved object recognition, real-time image processing, and enhanced decision-making, which are vital for autonomous vehicles and advanced safety systems. As cameras become more integrated with other vehicle technologies, such as radar and LIDAR, they form part of a comprehensive sensor suite that ensures accurate environmental sensing. Additionally, the miniaturization of camera systems and the development of higher-resolution imaging at lower costs have made these systems more accessible, further driving their adoption. With continuous improvements in image clarity, range, and system reliability, automotive cameras are becoming indispensable for modern vehicles, contributing significantly to the market’s expansion.

Market Challenges

High Cost of Advanced Camera Systems

One of the key challenges in the USA automotive cameras market is the high cost of advanced camera systems. As vehicle manufacturers integrate more sophisticated cameras for features such as 360-degree vision, object detection, and autonomous driving, the cost of these technologies increases. High-resolution cameras, AI integration, and advanced image processing technologies all contribute to higher production costs. These costs can be a significant barrier for automakers, particularly when it comes to mass-market vehicles. Although costs have been gradually decreasing due to technological advancements and economies of scale, high-end camera systems used in premium and autonomous vehicles remain expensive. This pricing issue limits the accessibility of advanced camera technologies, particularly for budget-conscious consumers and smaller manufacturers.

Integration with Other Sensor Technologies

Another challenge facing the automotive cameras market is the complexity of integrating camera systems with other sensor technologies, such as radar, LIDAR, and ultrasonic sensors. Modern vehicles rely on a combination of sensors to provide comprehensive situational awareness, but each sensor has its own strengths and limitations. Cameras provide excellent image capture and visual information, but they may struggle in low-light or adverse weather conditions. Combining camera systems with other sensors to ensure seamless sensor fusion requires significant technological expertise, as well as complex hardware and software integration. These challenges can drive up the development costs and time required to implement advanced safety and autonomous driving systems. As the demand for sensor fusion increases, addressing these integration challenges becomes crucial for further market growth.

Opportunities

Growth in Demand for Autonomous Vehicles

The increasing adoption of autonomous vehicles presents significant opportunities for the USA automotive cameras market. As autonomous driving technology advances, the need for reliable, high-performance cameras to capture real-time data about the vehicle’s surroundings becomes more crucial. Cameras are essential for the detection of obstacles, pedestrians, and other vehicles, forming an integral part of the sensor suite for autonomous systems. With the push for self-driving cars from companies like Waymo, Tesla, and traditional automakers, the demand for cameras in autonomous vehicles is set to grow rapidly. Additionally, regulatory support for autonomous vehicle testing and development will further fuel the demand for automotive cameras. As autonomous vehicles become more prevalent, cameras will continue to play a pivotal role in ensuring vehicle safety and navigation.

Expansion of Camera-based Systems in Electric Vehicles

The rise of electric vehicles (EVs) offers a promising opportunity for the automotive cameras market. As more consumers opt for EVs, manufacturers are incorporating advanced camera systems to support ADAS features, enhance safety, and improve driving experience. The integration of cameras in EVs allows for greater efficiency in parking assistance, range prediction, and energy-saving functions. Moreover, many EV manufacturers are incorporating autonomous driving features, further driving the demand for high-resolution cameras. As the electric vehicle market expands, the adoption of automotive cameras in EVs will continue to rise, providing an excellent growth opportunity for the industry.

Future Outlook

The future outlook for the USA Automotive Cameras market is highly positive, with significant growth expected across all vehicle types, especially electric and autonomous vehicles. Technological advancements in camera resolution, sensor fusion, and AI integration will continue to drive demand for advanced camera systems. The push towards stricter safety regulations, coupled with increased government support for autonomous vehicle development, will further fuel market growth. As the automotive industry moves toward greater automation and smarter safety systems, the role of automotive cameras will only become more critical in shaping the future of vehicle design and safety.

Major Players

- Bosch

- Valeo

- Continental AG

- Magna International

- Aptiv PLC

- Panasonic

- Omron Corporation

- Fujitsu Ten

- Visteon Corporation

- Autoliv

- Gentex Corporation

- ZF Friedrichshafen

- Samsung Electronics

- LG Electronics

- Denso Corporation

Key Target Audience

- Automotive Manufacturers

- Tier-1 Suppliers

- Vehicle Safety Manufacturers

- Technology Providers

- Automotive Aftermarket

- Government Agencies

- Research Institutions

- Investors and Venture Capitalists

Research Methodology

Step 1: Identification of Key Variables

Identify the primary growth drivers, challenges, and opportunities within the automotive cameras market.

Step 2: Market Analysis and Construction

Analyze data from primary and secondary sources to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Consult with industry experts and key stakeholders to validate the research hypotheses and refine market assumptions.

Step 4: Research Synthesis and Final Output

Synthesize the findings into a detailed market report that delivers actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for vehicle safety systems

Technological advancements in camera resolution and AI integration

Increasing adoption of autonomous vehicles and advanced driver-assistance systems (ADAS) - Market Challenges

High cost of advanced automotive cameras

Complexities in integrating automotive cameras with other ADAS technologies

Data security and privacy concerns related to in-vehicle cameras - Market Opportunities

Growing demand for cameras in electric vehicles

Expansion of camera-based systems for autonomous driving

Opportunities in the aftermarket camera system segment - Trends

Increasing use of 360-degree cameras for enhanced safety

Shift towards AI-based image recognition and processing

Rising focus on multi-functional cameras in vehicles - Government regulations

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Rear-view Cameras

360-degree Cameras

Front Cameras

Surround-view Cameras

Inside Cabin Cameras - By Platform Type (In Value%)

Passenger Cars

Commercial Vehicles

Electric Vehicles

Autonomous Vehicles

Heavy-duty Trucks - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Fitment

Integrated Systems

Modular Systems

Standalone Systems - By EndUser Segment (In Value%)

Automobile Manufacturers

Tier-1 Suppliers

Vehicle Safety Manufacturers

Technology Providers

Automotive Aftermarket - By Procurement Channel (In Value%)

Direct Procurement

Third-party Distributors

Online Procurement Platforms

Private Sector Procurement

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Technological Advancements, Geographic Reach, Camera Resolution, Price Sensitivity, Customer Demographics)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bosch

Continental AG

Denso Corporation

Valeo

Magna International

Aptiv PLC

Panasonic

Omron Corporation

Fujitsu Ten

Visteon Corporation

Autoliv

Gentex Corporation

ZF Friedrichshafen

Samsung Electronics

LG Electronics

- Increasing integration of cameras in ADAS systems

- Automobile manufacturers focusing on camera-based safety features

- Growing demand for cameras in electric and autonomous vehicles

- Aftermarket camera systems for vehicle upgrades and retrofits

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now