Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Chassis Market is valued at USD ~, reflecting its structural importance to vehicle manufacturing and mobility innovation across the country. The market is driven by sustained production of light trucks and utility vehicles, accelerating electrification programs, and rising safety and efficiency standards that increase the value contribution of chassis systems per vehicle. Demand logic is closely tied to platform redesign cycles, with OEMs increasingly investing in modular architectures that enable multi-powertrain compatibility. As chassis structures integrate battery housing, crash management, and suspension systems, their role has shifted from a purely mechanical foundation to a strategic performance and cost optimization lever across the automotive value chain.

Within the USA, the market is concentrated around manufacturing and engineering hubs such as the Midwest automotive belt, the Southeast production corridor, and the West Coast electric vehicle cluster, driven by proximity to major OEM assembly plants and dense Tier One supplier networks. These regions dominate due to advanced manufacturing infrastructure, skilled engineering talent, and strong logistics connectivity. At the same time, the market is influenced by global technology leaders shaping chassis innovation in areas such as lightweight materials, digital simulation, and EV platform design, setting benchmarks that guide domestic product development and capital investment priorities.

Market Segmentation

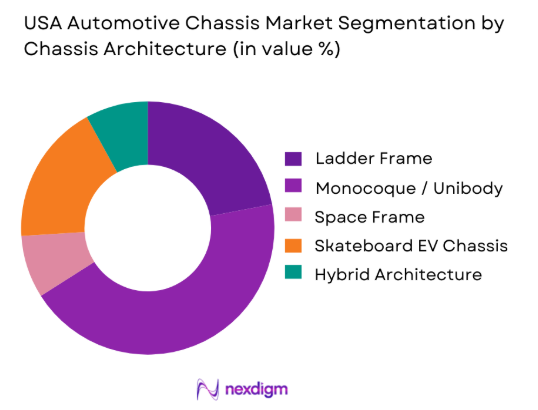

By Chassis Architecture

The USA Automotive Chassis Market is segmented by architecture into ladder frame, monocoque unibody, space frame, skateboard EV chassis, and hybrid architecture systems. Among these, monocoque unibody structures dominate due to their entrenched use in passenger vehicles and crossover platforms that account for the bulk of domestic vehicle output. Their dominance is reinforced by superior crash performance, lower overall weight compared to traditional frames, and streamlined manufacturing processes that align with high volume production economics. Leading OEMs continue to rely on unibody designs for both internal combustion and electrified models, adapting them with reinforced subframes and battery protection modules. This architectural flexibility allows manufacturers to balance cost efficiency with evolving regulatory requirements, ensuring unibody platforms remain central to mass market vehicle strategies and sustaining their leadership position in overall chassis demand.

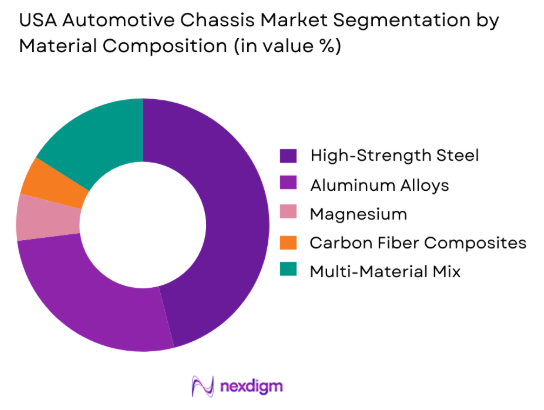

By Material Composition

The market is segmented into high strength steel, aluminum alloys, magnesium, carbon fiber composites, and multi material mixes. High strength steel remains the dominant material category due to its optimal balance of structural integrity, manufacturability, and cost efficiency for high volume vehicle programs. OEMs favor advanced steel grades to meet stringent crash standards while maintaining price competitiveness across mass market segments. The extensive domestic steel supply ecosystem further strengthens this position by ensuring stable availability and predictable input costs for chassis manufacturers. Although aluminum and composites are gaining traction in premium and electric vehicle platforms, steel continues to anchor mainstream chassis production, particularly for light trucks and utility vehicles where durability and towing performance are critical, reinforcing its leading role in the material mix.

Competitive Landscape

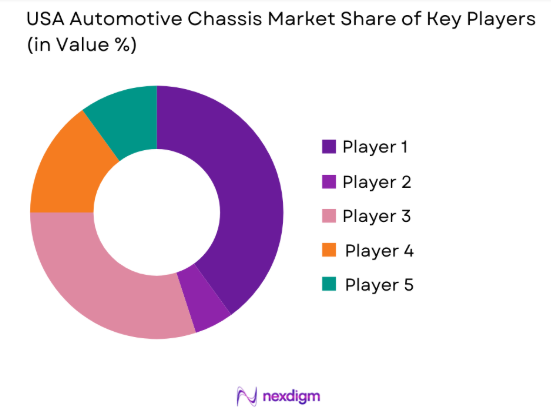

The USA Automotive Chassis Market market is dominated by a few major players, including Magna International and global or regional brands like Dana Incorporated, American Axle and Manufacturing, Benteler Automotive, and Gestamp. This consolidation highlights the significant influence of these key companies.

| Company | Establishment Year | Headquarters | Parameter 1 | Parameter 2 | Parameter 3 | Parameter 4 | Parameter 5 | Parameter 6 |

| Magna International | ~ | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | ~ | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| American Axle and Manufacturing | ~ | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Benteler Automotive | ~ | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Gestamp | ~ | USA | ~ | ~ | ~ | ~ | ~ | ~ |

USA Automotive Chassis Market Analysis

Growth Drivers

Electrification of Vehicle Platforms

The rapid electrification of vehicle platforms is reshaping the USA Automotive Chassis Market by fundamentally altering design priorities and procurement strategies. As OEMs transition toward battery electric and hybrid models, chassis systems are increasingly required to support heavy battery packs while maintaining crash safety and vehicle dynamics. This shift is driving demand for reinforced structures, skateboard architectures, and integrated battery enclosures, raising the overall value contribution of chassis components per vehicle. The impact extends across the supply chain, encouraging Tier One suppliers to invest in new tooling, advanced materials, and modular designs. The outcome is a market environment where innovation capability becomes a primary differentiator, enabling suppliers that align early with EV programs to secure long term contracts and strategic partnerships.

SUV and Light Truck Production Growth

Continued dominance of SUVs and light trucks in domestic vehicle production is another major growth driver for the chassis market. These vehicles require more robust structural systems to support higher payloads, towing capacity, and off road performance, directly increasing demand for higher value chassis assemblies. OEMs prioritize durability and safety in these segments, leading to the adoption of reinforced frames, advanced suspension integration, and multi material construction. This dynamic creates a virtuous cycle in which higher average selling prices for chassis systems improve supplier margins and justify further investment in capacity expansion and automation. As consumer preference continues to favor utility vehicles, chassis suppliers benefit from sustained volume stability and premiumization of product offerings.

Challenges

Raw Material Price Volatility

Volatility in raw material prices remains a persistent challenge for the USA Automotive Chassis Market, particularly in steel and aluminum inputs that account for a significant share of production costs. Sudden price fluctuations compress margins and complicate long term contract negotiations with OEMs that increasingly seek fixed cost agreements. This uncertainty forces suppliers to absorb short term cost pressures or engage in complex hedging strategies, diverting resources from innovation and capacity development. The impact is most pronounced for mid sized manufacturers with limited purchasing power, creating uneven competitive conditions across the supplier landscape. Over time, persistent cost instability can slow investment cycles and increase consolidation pressure within the market.

Skilled Labor Shortages

A tightening labor market poses another major constraint on the growth of the chassis industry in the USA. Advanced chassis manufacturing requires skilled welders, robotics technicians, and process engineers, roles that are increasingly difficult to fill due to demographic shifts and competition from other manufacturing sectors. Labor shortages elevate wage costs and limit production scalability, particularly in regions experiencing rapid automotive investment. The resulting bottlenecks affect delivery schedules and increase operational risk for OEM supply chains. In response, suppliers are accelerating automation and workforce upskilling programs, but these initiatives require significant upfront capital, adding to the financial burden faced by the industry.

Opportunities

EV Skateboard Platform Standardization

The move toward standardized skateboard platforms for electric vehicles presents a major opportunity for the USA Automotive Chassis Market. As OEMs seek to reduce development timelines and maximize platform reuse across multiple models, demand is rising for modular chassis systems that can support different body styles and powertrain configurations. Suppliers capable of delivering scalable, pre engineered skateboard solutions gain a strategic advantage by embedding themselves deeper into OEM product roadmaps. This opportunity extends beyond component supply into co development partnerships, allowing chassis manufacturers to influence vehicle architecture decisions at early design stages. Over time, this shift can elevate chassis suppliers from contract manufacturers to critical innovation partners within the automotive ecosystem.

Sustainable Materials Integration

Growing regulatory and consumer focus on sustainability is opening new avenues for chassis innovation centered on recyclable and low carbon materials. The adoption of green steel, aluminum with reduced emissions footprints, and bio based composites enables suppliers to differentiate their offerings while supporting OEM sustainability commitments. This transition creates opportunities for premium pricing in segments where environmental performance is a key purchasing criterion, particularly in electric and premium vehicles. Additionally, early investment in sustainable materials strengthens long term compliance readiness as environmental standards tighten, positioning forward looking suppliers to capture value as sustainability becomes a core competitive parameter.

Future Outlook

The USA Automotive Chassis Market is entering a phase of strategic transformation in which technology leadership, rather than production scale alone, will define competitive success. As electrification, automation, and sustainability reshape vehicle architectures, chassis systems will evolve into integrated platforms that combine structural integrity with energy management and digital intelligence. Suppliers that align their portfolios with modular EV platforms, multi material engineering, and advanced manufacturing will secure deeper partnerships with OEMs and capture a greater share of value creation across the automotive lifecycle.

Major Players

- Magna International

- Dana Incorporated

- American Axle and Manufacturing

- Benteler Automotive

- Gestamp

- ZF Chassis Solutions

- Bosch Chassis Systems

- Martinrea International

- Tower International

- Thyssenkrupp Automotive Technology

- Hyundai Mobis USA

- JFE Automotive USA

- Adient Structures

- Benteler Steel Tube North America

- Magna Steyr

Key Target Audience

- Automotive OEM procurement and strategy teams

- Tier One and Tier Two automotive component manufacturers

- Electric vehicle platform developers

- Fleet operators and commercial vehicle upfitters

- Investments and venture capitalist firms

- Government and regulatory bodies

- Raw material suppliers for steel aluminum and composites

- Industrial automation and manufacturing equipment providers

Research Methodology

Step 1: Identification of Key Variables

The research begins by mapping the full USA Automotive Chassis ecosystem, identifying OEMs, suppliers, material producers, and regulatory stakeholders that influence market dynamics. Extensive desk research is conducted using industry publications and corporate disclosures to define demand drivers, cost structures, and technology trajectories shaping the market.

Step 2: Market Analysis and Construction

Historical production and revenue data are analyzed to construct the market size using a bottom up framework, which is then reconciled through a top down validation process based on manufacturing output indicators. This dual approach ensures alignment between component level demand and macro industry trends.

Step 3: Hypothesis Validation and Expert Consultation

Key market assumptions are validated through structured interviews with senior executives from OEMs and Tier One suppliers. These discussions provide qualitative insight into pricing trends, sourcing strategies, and technology adoption patterns that refine the quantitative analysis.

Step 4: Research Synthesis and Final Output

All primary and secondary findings are synthesized into a consolidated market model, supported by triangulation across multiple data sources. The final output reflects a balanced perspective that integrates operational realities with strategic market outlooks.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, chassis system taxonomy and module mapping, market sizing logic by vehicle production and chassis content value, revenue attribution across modules materials and service parts, primary interview program with OEMs Tier 1s and material suppliers, data triangulation and validation approach, assumptions limitations and data gaps

- Definition and Scope

- Market Genesis and Evolution of Chassis Architectures in the USA

- Platform Strategies and Modularization Trends

- Chassis Value Chain Mapping Across OEMs Tier 1s and Sub Tier Suppliers

- Role of Light weighting and Electrification on Chassis Design

- Growth Drivers

SUV and pickup dominance driving chassis content demand

EV platform rollout increasing multi material chassis innovation

Safety regulations driving structural reinforcement and crash performance

Chassis module integration to reduce assembly complexity

Aftermarket demand for suspension steering and brake replacements - Challenges

Steel and aluminum price volatility affecting cost structures

Supply constraints for castings forgings and high strength steels

Weight cost and manufacturability trade offs in lightweight designs

High tooling investment and long platform cycles

Complexity of sourcing across global and domestic supply bases - Opportunities

Growth of gigacasting and large structural castings adoption

Shift to brake by wire and steer by wire chassis control evolution

Advanced corrosion protection for long life commercial fleets

Modular corner systems and integrated e axle chassis packages

Digital twin and CAE driven chassis optimization services - Trends

Move toward integrated chassis domain controllers

Increasing use of mixed material joining and adhesives

Growth of skateboard platforms for EVs and commercial vans

Adoption of active suspension and adaptive damping systems

Supplier consolidation and strategic sourcing in chassis modules - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- Vehicle Production Linked Chassis Content, 2019–2024

- By OEM vs Aftermarket Revenue Split, 2019–2024

- By Module Mix and ASP Waterfall, 2019–2024

- By Fleet Type (in Value %)

Passenger cars

SUVs and crossovers

Light commercial vehicles

Heavy duty trucks and vocational vehicles

Battery electric and hybrid vehicles - By Application (in Value %)

Body in white and frame structures

Suspension and subframe assemblies

Steering systems and columns

Braking systems and corner modules

Chassis electronics and control units - By Technology Architecture (in Value %)

Unibody chassis platforms

Body on frame architectures

Multi material chassis structures

Skateboard EV platforms

Integrated chassis domain control systems - By Connectivity Type (in Value %)

OEM direct sourcing and nomination

Tier 1 module supply and integration

Sub tier component and forging supply

Aftermarket service parts distribution

Contract manufacturing and stamping partnerships - By End-Use Industry (in Value %)

Light vehicle OEMs

Commercial vehicle OEMs

Tier 1 chassis module suppliers

Aftermarket parts and service networks

Material suppliers and fabricators - By Region (in Value %)

Midwest automotive manufacturing belt

Southeast production corridor

Texas and South Central truck hubs

West Coast EV production corridor

Northeast engineering and aftermarket clusters

- Competitive ecosystem structure across chassis module leaders and sub tier specialists

- Positioning driven by platform wins manufacturing scale and engineering capability

- Partnership models between OEMs Tier 1s and casting forging suppliers

- Cross Comparison Parameters (chassis content value per vehicle, lightweight material adoption level, manufacturing footprint and capacity, module integration capability, platform nomination depth, quality and warranty performance, lead time and supply resilience, cost competitiveness)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles of Major Companies

Magna International

American Axle and Manufacturing

Dana Incorporated

ZF Friedrichshafen

Continental

Bosch

Hyundai Mobis

Lear Corporation

Benteler

Gestamp

Adient

Tenneco

TRW Automotive

JTEKT

Nexteer Automotive

- OEM sourcing criteria for cost weight safety and manufacturability

- Tier 1 module integration priorities and delivery performance metrics

- Aftermarket buyer preferences for durability and fitment coverage

- Warranty and recall risk management considerations

- Total cost of ownership drivers for fleet operators

- By Value, 2025–2030

- By Vehicle Production Linked Chassis Content, 2025–2030

- By OEM vs Aftermarket Revenue Split, 2025–2030

- By Module Mix and ASP Waterfall, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now