Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA automotive displays market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerating adoption of digital cockpit architectures, premium infotainment systems, and advanced driver assistance visualization interfaces across passenger and electric vehicles. Automakers are integrating larger central touchscreens, digital instrument clusters, and head-up displays to enhance safety and user experience, while increasing vehicle electrification and software-defined cockpit strategies are expanding display content, functionality, and value per vehicle installed.

Within the USA automotive displays market, dominance is concentrated in technology and automotive manufacturing hubs such as California, Michigan, Texas, and Ohio due to strong automotive OEM presence, advanced electronics supply chains, and innovation ecosystems. California leads through electric and autonomous vehicle development clusters, while Michigan anchors traditional OEM engineering and production. Texas and Ohio benefit from semiconductor fabrication, automotive electronics manufacturing, and logistics infrastructure, enabling high-volume display integration across vehicle assembly operations nationwide.

Market Segmentation

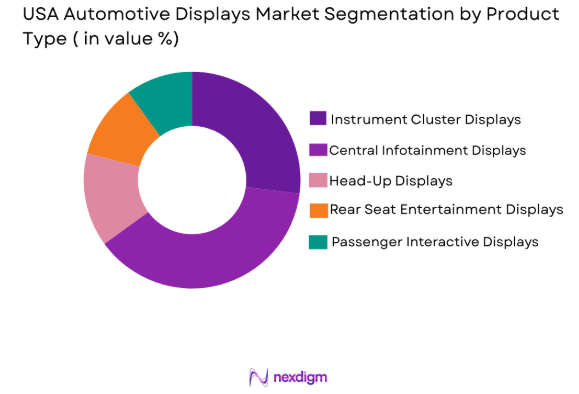

By Product Type

USA automotive displays market is segmented by product type into instrument cluster displays, central infotainment displays, head-up displays, rear seat entertainment displays, and passenger interactive displays. Recently, central infotainment displays have a dominant market share due to factors such as consumer demand for touchscreen-based vehicle control interfaces, integration of navigation and connectivity functions, and automaker differentiation through large-format display designs. Increasing software-defined vehicle architectures consolidate multiple functions into central displays, reducing physical controls and expanding screen size, while premium and electric vehicles emphasize immersive cabin experiences that further accelerate infotainment display adoption across mass-market models.

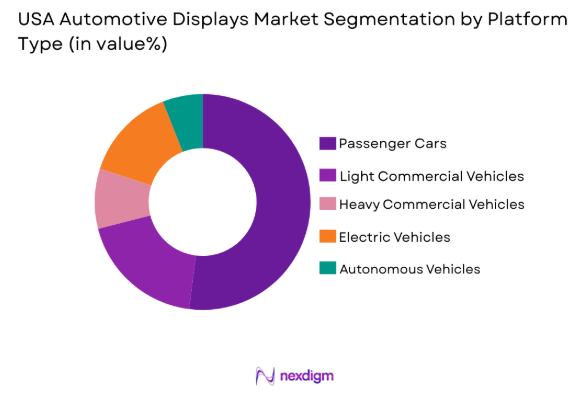

By Platform Type

USA automotive displays market is segmented by platform type into passenger cars, light commercial vehicles, heavy commercial vehicles, electric vehicles, and autonomous vehicles. Recently, passenger cars have a dominant market share due to factors such as higher production volumes, consumer expectations for connected infotainment, and rapid digital cockpit adoption across sedans and SUVs. Electric passenger vehicles further intensify display content requirements through energy management visualization, advanced driver assistance graphics, and over-the-air software interfaces, while commercial and autonomous platforms remain comparatively lower volume despite higher per-vehicle display complexity and specialized interface requirements.

Competitive Landscape

The USA automotive displays market shows moderate consolidation with global automotive electronics suppliers and display panel manufacturers dominating OEM supply chains through long-term contracts and integration capabilities. Major players leverage vertically integrated display technologies, automotive-grade manufacturing, and strong OEM relationships to secure design wins across digital cockpit platforms. Competitive intensity is shaped by innovation in OLED, curved, and large-format displays, while partnerships between semiconductors, software, and automotive firms influence technology leadership and market reach.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Automotive Display Integration Capability |

| Visteon Corporation | 2000 | USA | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| LG Display | 1985 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Panasonic Automotive Systems | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

USA Automotive Displays Market Analysis

Growth Drivers

Digital cockpit integration and software-defined vehicle architectures

The USA automotive displays market is experiencing sustained expansion as vehicle manufacturers transition from analog dashboards toward fully digital cockpit environments that integrate instrument clusters, infotainment, navigation, driver assistance visualization, and vehicle control functions into cohesive multi-display systems. Software-defined vehicle platforms require high-resolution graphical interfaces capable of supporting real-time data visualization, over-the-air updates, and customizable user interfaces, significantly increasing both the number and size of displays per vehicle. Electrification further intensifies display requirements through energy monitoring, charging management visualization, and advanced vehicle status interfaces that depend on screen-based interaction rather than mechanical controls. Automakers are redesigning interiors around centralized displays, reducing physical buttons and consolidating functions into touch and haptic-enabled surfaces, thereby structurally increasing display value per vehicle across multiple segments. Semiconductor and graphics processing advancements have enabled automotive-grade display performance with high brightness, durability, and responsiveness suitable for harsh cabin environments. Premium features such as curved OLED dashboards and pillar-spanning screens are gradually cascading into mid-range vehicles as costs decline and production scales improve. Safety regulations requiring visualization of advanced driver assistance systems also reinforce mandatory display integration across new vehicles. These combined technological and regulatory forces are embedding displays as a core architectural element within modern vehicles in the USA automotive displays market.

Consumer demand for immersive infotainment and connectivity interfaces

The USA automotive displays market is also driven by evolving consumer expectations that vehicles deliver digital experiences comparable to personal electronics, including large touchscreens, seamless smartphone integration, personalized interfaces, and high-definition multimedia capabilities across driver and passenger zones. Buyers increasingly associate large and visually sophisticated displays with technological advancement and premium vehicle perception, encouraging OEMs to prioritize display-centric interior design strategies across product portfolios. Growth of connected vehicle ecosystems, streaming services, app-based navigation, and voice-enabled digital assistants requires display platforms capable of supporting complex multimedia and interactive functions beyond traditional instrumentation. Electric and autonomous-ready vehicles emphasize cabin experience differentiation due to reduced mechanical noise and powertrain complexity, elevating infotainment and passenger display importance as key purchase drivers. Rear-seat entertainment and passenger interaction displays are expanding in family and ride-hailing vehicles, further increasing total display area per vehicle. Competitive pressure among automakers to deliver visually distinctive interiors accelerates adoption of wide, curved, and multi-screen configurations. Continuous software upgrades delivered through displays extend functionality over vehicle lifecycles, increasing perceived value and engagement. These consumer-driven design priorities are expanding display penetration across vehicle classes within the USA automotive displays market.

Market Challenges

High cost and automotive-grade reliability requirements of advanced displays

The USA automotive displays market faces persistent barriers due to the high manufacturing cost and stringent durability requirements associated with advanced automotive display technologies such as OLED, MicroLED, flexible panels, and large curved formats that must operate reliably under vibration, thermal cycling, humidity, and prolonged sunlight exposure over extended vehicle lifetimes. Automotive qualification standards exceed consumer electronics benchmarks, necessitating specialized materials, coatings, backlighting systems, and driver electronics that increase production complexity and capital investment. Supply chain dependencies on automotive-grade semiconductors, display driver ICs, and specialized substrates create exposure to shortages and price fluctuations, disrupting production planning. Integration of large displays into dashboards requires structural reinforcement, thermal management systems, and electromagnetic shielding, adding weight and cost to vehicle platforms. Repair and replacement of integrated displays remain expensive due to bonded assemblies and embedded electronics, increasing warranty risk and lifecycle maintenance costs for automakers and fleet operators. Cost sensitivity in entry-level and commercial vehicles limits adoption of premium display technologies despite consumer interest. Competitive OEM procurement practices exert pricing pressure on suppliers while technology complexity rises. These economic and engineering constraints continue to slow widespread penetration of advanced displays across all vehicle segments in the USA automotive displays market.

Integration complexity and driver distraction regulatory constraints

Automotive displays must be engineered within tightly regulated safety frameworks that limit placement, brightness, animation, and interactive functionality to reduce driver distraction and maintain compliance with transportation safety standards, creating design and engineering challenges for display manufacturers and automakers in the USA automotive displays market. Integration with vehicle electronic architectures requires compatibility with driver assistance systems, sensor data processing, cybersecurity protocols, and fail-safe redundancy to ensure safe operation under all conditions. Large or multi-screen layouts increase system integration complexity, requiring advanced software synchronization and human–machine interface validation to prevent information overload or unsafe interaction patterns. Regulations governing driver attention and interface usability restrict certain immersive or entertainment-oriented features in driver-visible displays, constraining innovation potential. Continuous testing for electromagnetic compatibility, environmental durability, and crash safety extends development cycles and costs. Software-defined cockpits require cybersecurity certification to prevent hacking or data compromise through display interfaces. Global regulatory variations necessitate region-specific display configurations and compliance validation. These technical and regulatory constraints complicate deployment of next-generation display architectures across vehicles in the USA automotive displays market.

Opportunities

Expansion of panoramic pillar-to-pillar cockpit display systems

The USA automotive displays market presents significant growth potential through adoption of panoramic dashboard displays spanning the full width of vehicle interiors, creating seamless digital surfaces that unify driver instrumentation, infotainment, and passenger interaction zones into a single integrated visual environment supporting advanced user experiences and brand differentiation. Electric vehicle platforms with flat floors and simplified mechanical layouts enable flexible interior packaging that accommodates larger display modules without structural constraints present in conventional vehicles. Panoramic displays allow customizable multi-user interfaces, enabling simultaneous driver and passenger interaction and enhancing cabin personalization. Advances in OLED and MicroLED technologies provide thin, flexible, and high-contrast panels suitable for curved and wide-format automotive installations with improved energy efficiency. Automakers are leveraging panoramic displays to create visually distinctive interiors that influence purchase decisions in premium and mid-range vehicles. Integration of ambient lighting, touch surfaces, and haptic feedback across wide displays enhances perceived technological sophistication. Software-defined cockpit architectures allow dynamic interface updates across panoramic surfaces, extending functionality over time. As manufacturing scales and costs decline, pillar-to-pillar display systems are expected to migrate beyond luxury vehicles, expanding addressable market volume in the USA automotive displays market.

Adoption of augmented reality head-up and passenger interactive displays

Augmented reality head-up displays and advanced passenger interaction screens represent a major opportunity within the USA automotive displays market by enabling contextual visualization of navigation, safety alerts, and environmental information directly aligned with the driver’s field of view while simultaneously delivering entertainment and control interfaces to passengers across connected cabin environments. Augmented reality overlays enhance situational awareness by projecting lane guidance, hazard indicators, and route cues onto the windshield, improving safety and regulatory acceptance of advanced visualization technologies. Passenger displays support media streaming, climate control, and vehicle settings interaction without driver involvement, enabling multi-occupant digital engagement. Autonomous-ready vehicles emphasize cabin experience and shared interaction surfaces, increasing relevance of passenger-focused displays. Advances in optical projection, graphics processing, and sensor fusion enable precise real-world alignment of augmented content. Integration of subscription services, personalized content, and app ecosystems through passenger displays creates new revenue channels for automakers. Electric vehicle architectures and premium interior strategies support deployment of additional display zones. These technological and experiential developments position augmented and passenger displays as key expansion vectors in next-generation vehicles within the USA automotive displays market.

Future Outlook

The USA automotive displays market is expected to experience sustained growth driven by digital cockpit standardization, increasing electric vehicle penetration, and integration of augmented reality visualization technologies. Advancements in OLED, MicroLED, and flexible display materials will enable larger and more immersive cabin interfaces. Regulatory focus on driver assistance visualization and safety interfaces will reinforce display integration across vehicle segments. Software-defined vehicle ecosystems and connected services will further expand display functionality and value per vehicle over the coming years.

Major Players

- Visteon Corporation

- Continental AG

- Denso Corporation

- Panasonic Automotive Systems

- LG Display

- Sharp Corporation

- AUO Corporation

- Innolux Corporation

- BOE Technology

- Samsung Display

- Japan Display Inc.

- Valeo SA

- Harman International

- Alps Alpine Co Ltd

- Gentex Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive OEM manufacturers

- Automotive electronics suppliers

- Electric vehicle manufacturers

- Semiconductor and displaycomponent manufacturers

- Fleet operators

- Automotive infotainment system integrators

Research Methodology

Step 1: Identification of Key Variables

Key variables including vehicle production volumes, display penetration per vehicle, display size trends, technology adoption rates, and OEM integration strategies were identified through secondary literature and industry datasets. Automotive electronics value chain mapping and regulatory frameworks were analyzed to determine demand drivers and technological constraints influencing market dynamics.

Step 2: Market Analysis and Construction

The market was constructed using a bottom-up approach integrating vehicle production statistics, average display content per vehicle, and technology mix across vehicle segments. OEM model analysis and supplier shipment data were triangulated to estimate market size, segmentation shares, and technology distribution within the USA automotive displays ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with automotive electronics engineers, display technology specialists, and industry analysts to confirm technology adoption trajectories and pricing structures. Expert feedback refined assumptions on display penetration, technology transition timelines, and OEM procurement strategies shaping the competitive landscape.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market segmentation, competitive analysis, and future outlook frameworks. Quantitative estimates and qualitative trends were integrated to ensure consistency across sections, producing a comprehensive analytical view of the USA automotive displays market and its evolving technological trajectory.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising adoption of digital cockpit architectures across vehicle segments

Increasing integration of ADAS visualization and driver assistance interfaces

Growth in electric and premium vehicle production with multi-display cabins

Consumer demand for immersive infotainment and connectivity features

Automaker differentiation through large-format and curved displays - Market Challenges

High cost of advanced display technologies such as OLED and MicroLED

Thermal management and durability requirements in automotive environments

Integration complexity with vehicle electronics and software platforms

Supply chain constraints for automotive-grade semiconductor components

Stringent safety and driver distraction regulatory compliance requirements - Market Opportunities

Expansion of panoramic pillar-to-pillar cockpit display systems

Integration of augmented reality head-up display technologies

Aftermarket upgrades for legacy vehicle infotainment systems - Trends

Shift toward curved and seamless multi-display dashboards

Growing adoption of OLED and flexible display panels in premium vehicles

Integration of haptic feedback and touch-sensitive surfaces

Software-defined cockpit interfaces with over-the-air updates

Convergence of instrument cluster and infotainment into unified displays - Government Regulations & Defense Policy

Driver distraction and in-vehicle display safety standards enforcement

Automotive electronic component reliability certification requirements

Cybersecurity regulations for connected vehicle display interfaces

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Instrument Cluster Displays

Central Infotainment Displays

Head-Up Displays

Rear Seat Entertainment Displays

Passenger Interactive Displays - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Autonomous Vehicles - By Fitment Type (In Value%)

OEM Integrated Displays

Aftermarket Retrofit Displays

Modular Dashboard Displays

Embedded Cockpit Displays

Panoramic Cockpit Displays - By End User Segment (In Value%)

Automotive OEM Manufacturers

Tier-1 Automotive Electronics Suppliers

Fleet Operators

Aftermarket Installers

Specialty Vehicle Integrators - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier-1 Supplier Agreements

Dealer Installed Options

Aftermarket Distribution Networks

Online Automotive Electronics Retail - By Material / Technology (in Value %)

LCD Automotive Displays

OLED Automotive Displays

MicroLED Displays

TFT-LCD Panels

Flexible Display Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Display Technology Portfolio, Automotive Qualification Standards, Integration Capability, Production Scale, OEM Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Visteon Corporation

Continental AG

Denso Corporation

Panasonic Automotive Systems

LG Display

Sharp Corporation

AUO Corporation

Innolux Corporation

BOE Technology Group

Samsung Display

Japan Display Inc.

Valeo SA

Harman International

Alps Alpine Co Ltd

Gentex Corporation

- OEMs increasing deployment of multi-display digital cockpit configurations

- Fleet operators adopting ruggedized infotainment and telematics displays

- Aftermarket installers targeting infotainment upgrades in aging vehicle fleets

- Specialty vehicle builders integrating custom interactive display solutions

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now