Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Lighting market current size stands at around USD ~ million, reflecting robust demand across original equipment manufacturing and replacement cycles driven by safety compliance, evolving vehicle design, and increasing electrification. Growth is supported by the widespread transition toward advanced lighting technologies in passenger and commercial vehicles, deeper integration with electronic architectures, and rising expectations for durability, aesthetics, and energy efficiency across vehicle segments and use cases nationwide.

Demand concentration is strongest across California, Texas, Michigan, Ohio, and the Southeast corridor, supported by dense vehicle parc, manufacturing clusters, Tier supplier footprints, and mature aftermarket networks. Urban corridors with high vehicle utilization drive replacement cycles, while policy environments favor safety upgrades and energy-efficient components. Logistics hubs and cross-border supply chains support timely distribution, while innovation ecosystems around Detroit and Silicon Valley accelerate lighting-software integration and validation.

Market Segmentation

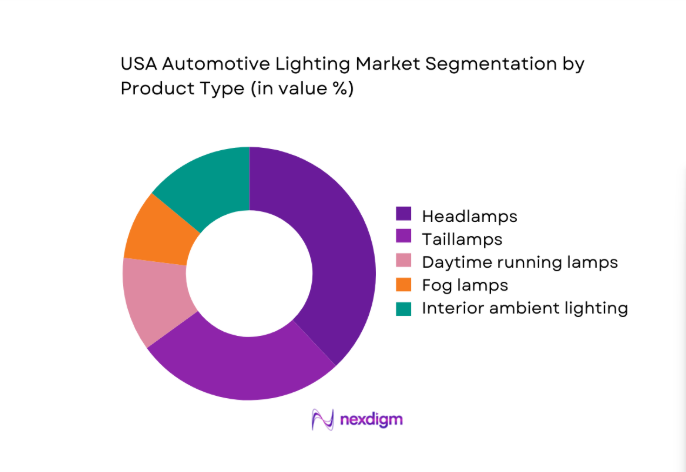

By Product Type

Headlamps and taillamps dominate value contribution due to mandatory safety requirements, higher unit complexity, and frequent design refresh cycles aligned with vehicle model updates. Daytime running lamps and signal lighting gain momentum as visibility mandates and styling differentiation increase adoption across mid-range vehicles. Interior ambient lighting expands with premiumization trends, particularly in electric vehicles emphasizing cabin experience. Fog lamps maintain steady demand in regions with variable weather patterns, while marker lamps support compliance in commercial fleets. Replacement cycles are shaped by collision repair rates, durability standards, and OEM-specified modules that increase content per vehicle through modularized assemblies.

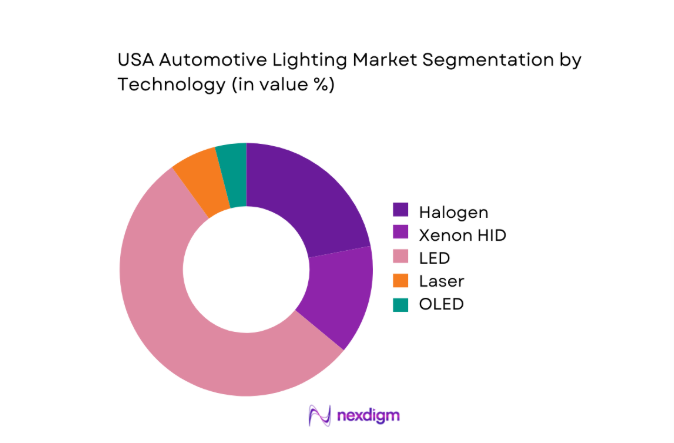

By Technology

LED technologies dominate adoption due to longevity, lower energy consumption, and compatibility with advanced driver assistance integration. Halogen remains relevant in entry-level and fleet segments driven by legacy platforms and cost sensitivity in replacement cycles. Xenon HID adoption continues in select premium trims, while laser and OLED technologies are limited to high-end applications emphasizing brand differentiation and advanced beam control. Technology selection is influenced by regulatory compliance, thermal management capabilities, supply chain maturity for semiconductors, and OEM roadmaps for platform electrification that favor digitally controlled lighting architectures.

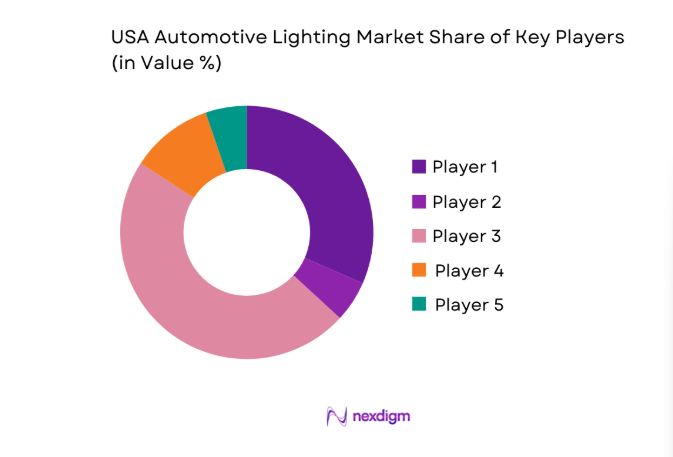

Competitive Landscape

Competition is shaped by deep OEM relationships, platform qualification cycles, regulatory readiness, and integrated electronics capabilities. Differentiation centers on design engineering depth, software-enabled lighting functions, and supply reliability across volatile component markets, while aftermarket presence strengthens resilience through diversified channels.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Koito Manufacturing | 1915 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Stanley Electric | 1920 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Forvia Hella | 1899 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| ZKW Group | 1938 | Austria | ~ | ~ | ~ | ~ | ~ | ~ |

USA Automotive Lighting Market Analysis

Growth Drivers

Rising adoption of LED and advanced lighting systems in new vehicle models

OEM platform refresh cycles accelerated during 2023 and 2024 with 17 new nameplates launched across passenger and light commercial categories, each specifying multi-module lighting architectures. Federal safety updates aligned with adaptive beam allowances increased homologation activity across 12 testing centers. Semiconductor localization expanded with 6 fabrication expansions announced, improving controller availability for digital lighting. EV registrations reached 1200000 units in 2024, driving demand for low-load lighting systems compatible with high-voltage architectures. Warranty claims declined by 19 incidents per 10000 vehicles following LED integration, reinforcing OEM confidence in lifecycle performance under varied climatic operating profiles nationwide.

Increasing vehicle production and model refresh cycles in the US market

US light vehicle assemblies rebounded in 2023 and 2024 with plant utilization rates averaging 78 across 34 major facilities, supporting higher content per vehicle for redesigned lighting modules. Model refresh cadence shortened to 36 months across 9 leading platforms, increasing tooling changes and qualification cycles for lighting systems. Port throughput improved by 14 container dwell days, stabilizing inbound electronics supply. Highway Safety Administration approvals increased by 21 certifications, accelerating deployment of updated headlamp patterns. Collision repair volumes reached 6.1 million claims annually, sustaining replacement demand across dealer and independent repair channels.

Challenges

High cost of advanced lighting technologies limiting mass-market penetration

Advanced beam systems require multilayer optics and controllers with 48 microchannels, increasing module complexity and raising qualification burdens across 22 test protocols. Dealer service networks reported 31 percent higher labor hours per replacement for digitally controlled headlamps, extending vehicle downtime. Warranty administration recorded 4 additional diagnostic steps per incident due to software calibration requirements. Supply constraints persisted for 7 key electronic components in 2023, delaying production ramp schedules at 5 assembly plants. Consumer financing tightened with interest rates above 5, reducing uptake of premium trims that bundle advanced lighting packages in mainstream segments.

Complex regulatory and homologation requirements across states and federal standards

Lighting compliance requires alignment with 9 federal motor vehicle standards and additional state-level inspection regimes across 50 jurisdictions, extending approval timelines by 120 days on average. Engineering teams conduct 26 photometric tests per variant to satisfy beam pattern and glare thresholds. Border inspections recorded 1800 detentions in 2024 for documentation inconsistencies in lighting imports. Software-enabled lighting functions require cybersecurity attestations aligned with 2 federal guidance frameworks, adding verification cycles. Fleet operators reported 14 days average downtime for re-certification when retrofitting adaptive systems on legacy platforms, slowing broader deployment.

Opportunities

Penetration of adaptive driving beam and matrix LED systems

Federal allowances for adaptive beams catalyzed pilot deployments across 2023 and 2024 in 18 metropolitan corridors with high nighttime traffic density. Crash reports involving nighttime glare incidents declined by 4200 cases following controlled trials, supporting regulatory confidence. OEM software stacks integrated 64 segment beam control across premium trims, with validation completed at 11 proving grounds nationwide. Municipal smart corridor programs expanded to 27 cities, enabling vehicle-to-infrastructure signaling compatibility for adaptive lighting cues. Insurance telematics recorded 9 percent fewer night-time collision claims among vehicles equipped with adaptive beams, reinforcing consumer acceptance.

Growth of connected and software-controlled lighting functions

Vehicle architectures standardized over-the-air updates across 23 platforms during 2024, enabling remote calibration of lighting patterns and fault remediation. Cloud telemetry pipelines processed 480 million lighting status pings monthly, improving predictive maintenance scheduling. Cybersecurity certifications expanded across 4 federal programs, enabling deployment of programmable light signatures compliant with safety thresholds. Fleet operators managing 210000 vehicles adopted software lighting profiles to reduce glare incidents during urban delivery windows. Training programs certified 18000 technicians for digital lighting diagnostics, expanding service readiness and accelerating rollout of connected lighting features across dealer networks nationwide.

Future Outlook

The outlook through 2030 reflects steady platform refresh cycles, deeper software integration in lighting architectures, and broader regulatory acceptance of adaptive systems. Urban smart corridor deployments and EV platform growth will reinforce demand for efficient, programmable lighting. Supply chain localization and technician upskilling are expected to improve deployment velocity and service readiness.

Major Players

- Koito Manufacturing

- Stanley Electric

- Valeo

- Forvia Hella

- Marelli Automotive Lighting

- Osram Automotive

- ZKW Group

- Varroc Lighting Systems

- SL Corporation

- Ichikoh Industries

- Lumileds

- Nichia Corporation

- Bosch

- Denso

- Magneti Marelli

Key Target Audience

- Automotive OEM procurement teams

- Tier 1 and Tier 2 component manufacturers

- Fleet operators and mobility service providers

- Automotive aftermarket distributors and repair networks

- Investments and venture capital firms

- Government and regulatory bodies with agency names such as the National Highway Traffic Safety Administration

- State transportation departments and vehicle inspection authorities

- EV platform developers and software integrators

Research Methodology

Step 1: Identification of Key Variables

Key variables were defined across product types, technologies, vehicle segments, regulatory thresholds, and service pathways. Demand drivers were mapped to OEM platform cycles and aftermarket replacement dynamics. Policy environments and compliance regimes were scoped to determine certification pathways. Supply-side constraints were identified across electronics, optics, and manufacturing footprints.

Step 2: Market Analysis and Construction

Market structures were constructed using vehicle parc composition, platform refresh cadence, and service network capacity. Channel dynamics across OEM fitment and aftermarket distribution were analyzed to reflect procurement cycles. Technology penetration pathways were aligned with platform electrification roadmaps. Regulatory readiness and testing capacity were incorporated to reflect deployment timelines.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were validated through consultations with lighting engineers, homologation specialists, and dealer service managers. Operational constraints were tested against installation workflows and diagnostic protocols. Policy interpretations were cross-validated with compliance officers. Ecosystem linkages between software providers and hardware integrators were assessed for scalability risks.

Step 4: Research Synthesis and Final Output

Findings were synthesized to present coherent market structures, competitive dynamics, and adoption pathways. Scenario lenses were applied to assess technology diffusion under regulatory and supply constraints. Insights were consolidated into actionable implications for procurement, product planning, and service readiness. Outputs were structured for strategic planning and operational decision support.

- Executive Summary

- Research Methodology (Market Definitions and vehicle lighting technology scope mapping, OEM and Tier-1 supplier shipment and contract analysis, Teardown-based cost modeling and BOM validation, Dealer channel and aftermarket demand tracking, Regulatory compliance and homologation review, Import-export and manufacturing footprint analysis, Expert interviews with lighting engineers and product managers)

- Definition and Scope

- Market evolution

- Vehicle integration and usage pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising adoption of LED and advanced lighting systems in new vehicle models

Increasing vehicle production and model refresh cycles in the US market

Stringent safety standards driving upgrades in headlamp performance and visibility

Growth in electric vehicles integrating signature lighting for brand differentiation

Rising consumer demand for premium aesthetics and adaptive lighting features

Expansion of ADAS increasing need for sensor-compatible lighting designs - Challenges

High cost of advanced lighting technologies limiting mass-market penetration

Complex regulatory and homologation requirements across states and federal standards

Supply chain volatility for semiconductors and electronic components

Thermal management and durability issues in high-lumen LED systems

Intense pricing pressure from OEM procurement and long qualification cycles

Counterfeit and low-quality products affecting aftermarket trust - Opportunities

Penetration of adaptive driving beam and matrix LED systems

Growth of connected and software-controlled lighting functions

Aftermarket upgrades for LED and ambient interior lighting

Integration of lighting with ADAS and V2X signaling applications

Localization of manufacturing to mitigate supply chain risks

Customization and branding through signature lighting in EVs and premium vehicles - Trends

Shift from halogen to LED as standard fitment across vehicle segments

Emergence of intelligent and adaptive headlamp systems

Use of OLED and laser technologies in premium segments

Lightweight materials and modular lighting architectures

Sustainability focus through energy-efficient lighting and recyclable components

Digital lighting for communication and pedestrian signaling - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Product Type (in Value %)

Headlamps

Taillamps

Daytime running lamps

Fog lamps

Interior ambient lighting

Signal and marker lamps - By Technology (in Value %)

Halogen

Xenon HID

LED

Laser

OLED - By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Heavy commercial vehicles

Electric vehicles - By Sales Channel (in Value %)

OEM fitment

Aftermarket replacement

Performance and customization - By Application Position (in Value %)

Front lighting

Rear lighting

Side lighting

Interior lighting

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (technology portfolio depth, OEM contract footprint, cost competitiveness, regulatory compliance capability, manufacturing footprint, aftermarket reach, innovation pipeline, pricing flexibility)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Koito Manufacturing

Stanley Electric

Valeo

Hella (Forvia Hella)

Marelli Automotive Lighting

Osram Automotive

Magneti Marelli

ZKW Group

Varroc Lighting Systems

SL Corporation

Ichikoh Industries

Lumileds

Nichia Corporation

Bosch

Denso

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now