Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Paints and Coatings market current size stands at around USD ~ million, reflecting sustained demand across OEM production lines and refinish channels. Growth is supported by stable vehicle manufacturing pipelines, consistent aftermarket repair activity, and ongoing shifts toward compliant coating technologies. Capital allocation within coating lines continues to prioritize efficiency upgrades and quality consistency, while supplier ecosystems remain anchored to long-term production programs and multi-year qualification cycles.

Activity is concentrated across Midwest automotive manufacturing corridors and Southern production hubs, with refinish demand densest in large metropolitan repair networks. Coastal states exhibit stronger regulatory oversight shaping technology adoption, while industrial clusters benefit from proximity to logistics infrastructure and chemical feedstock supply. Mature distributor networks support nationwide coverage, and regional technical service teams enable rapid deployment of new formulations aligned to evolving environmental and safety requirements.

Market Segmentation

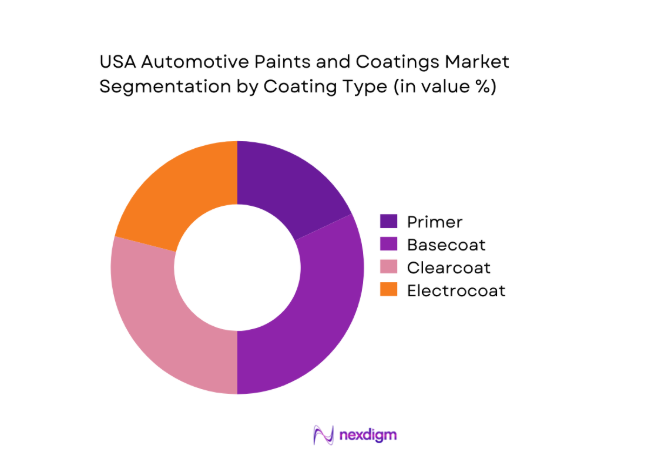

By Coating Type

Clearcoat and basecoat systems dominate adoption due to durability requirements, aesthetic differentiation needs, and compatibility with high-throughput paint shop processes. Electrocoat penetration remains structurally entrenched in corrosion protection across body-in-white stages, while primers are optimized for adhesion across mixed substrates. Multi-layer architectures are increasingly standardized within OEM lines, driving steady demand for tightly specified coating stacks. Refinish channels prioritize clearcoat performance for UV resistance and scratch mitigation, supporting premium product uptake. Technology validation cycles, shop throughput constraints, and warranty performance expectations reinforce concentration toward high-performance coating types with predictable curing behavior and stable finish consistency across diverse vehicle platforms and model refresh programs.

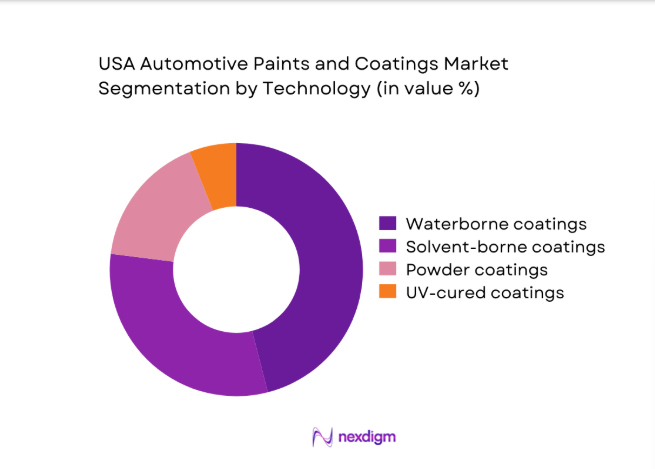

By Technology

Waterborne systems lead adoption as compliance alignment, indoor air quality management, and waste handling efficiencies increasingly shape procurement decisions. Solvent-borne formulations persist in niche performance-critical applications, particularly within specialized refinish environments. Powder coatings are expanding across components requiring high transfer efficiency and durability, while UV-cured systems gain selective traction where rapid curing and energy efficiency support throughput optimization. Technology selection is increasingly governed by lifecycle performance, shop retrofitting constraints, and workforce safety protocols, reinforcing momentum toward low-emission platforms compatible with automation and robotics integration across high-volume production and repair operations nationwide.

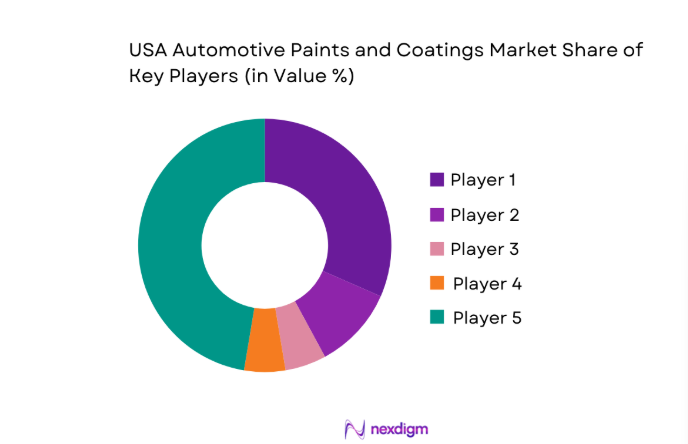

Competitive Landscape

The competitive environment reflects a mix of vertically integrated formulation specialists and application-focused solution providers supporting OEM and refinish ecosystems. Differentiation centers on formulation depth, regulatory readiness, technical service coverage, and the ability to support high-throughput operations with consistent quality outcomes.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| PPG Industries | 1883 | Pittsburgh, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Axalta Coating Systems | 2013 | Philadelphia, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| BASF Coatings | 1865 | Ludwigshafen, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Sherwin-Williams | 1866 | Cleveland, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| AkzoNobel | 1792 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

USA Automotive Paints and Coatings Market Analysis

Growth Drivers

Rising vehicle production and model refresh cycles in the US

Automotive assembly volumes rebounded across multiple plants following capacity normalization, with 2023 production schedules restoring multi-shift operations and 2024 model refresh programs expanding color and finish variants. The Department of Transportation recorded new vehicle registrations exceeding 15000000 units in 2023, while Federal Highway Administration data showed fleet age stability supporting sustained replacement cycles. Manufacturing modernization programs added 1200 robots to paint shops during 2024, improving throughput consistency and coating utilization. Expanded platform sharing across manufacturers increased standardized coating stacks, raising baseline coating consumption per unit. Workforce stabilization across industrial counties supported steady line utilization, reinforcing coating demand.

Shift toward waterborne and low-VOC coatings driven by regulations

Environmental compliance requirements tightened under federal and state air quality frameworks during 2023 and 2024, prompting accelerated conversion of paint shops to low-emission systems. The Environmental Protection Agency updated hazardous air pollutant guidance in 2023, while 12 states adopted stricter VOC thresholds in 2024. Over 900 OEM and Tier 1 facilities reported process audits to transition legacy solvent systems toward compliant technologies. Investments in abatement equipment increased installation of 320 regenerative thermal oxidizers across industrial corridors. Occupational safety agencies documented reduced solvent exposure incidents during 2024 inspections, reinforcing institutional preference for waterborne formulations within regulated manufacturing environments nationwide.

Challenges

Volatility in raw material prices for resins and pigments

Feedstock markets experienced pronounced variability across 2023 and 2024, driven by petrochemical maintenance cycles, shipping disruptions across Gulf Coast terminals, and constrained pigment capacity in Asia. The Energy Information Administration reported refinery utilization swings of 6 points during 2023 maintenance seasons, affecting resin precursor availability. Freight dwell times at major ports extended by 4 days during 2024 peak periods, delaying specialty additives. Manufacturing purchasing indices signaled supplier delivery volatility across 9 consecutive months in 2024. These fluctuations complicated formulation planning, increased inventory buffers, and constrained consistent batch production schedules across domestic coating facilities.

Stringent VOC and hazardous air pollutant regulations increasing compliance costs

Compliance obligations intensified following updated federal enforcement protocols in 2023 and state-level permitting revisions in 2024 across California, New York, and Texas. Over 480 coating lines underwent recertification audits, requiring equipment upgrades and process revalidation. Occupational safety inspections cited 210 facilities for ventilation nonconformance during 2024. Engineering retrofits added 18 months to project timelines for older plants, constraining production continuity. Documentation requirements expanded under revised recordkeeping rules, increasing administrative burden for environmental health teams. These regulatory pressures elevated operational complexity and constrained rapid technology transitions for smaller coating operators.

Opportunities

Adoption of bio-based and sustainable resin systems

Policy incentives for sustainable materials expanded during 2023 and 2024 through federal procurement guidelines favoring low-toxicity inputs across public fleets. The Department of Energy funded 24 pilot projects exploring bio-derived polymer intermediates for industrial coatings. University-industry consortia advanced 7 scalable synthesis pathways for renewable acrylic substitutes validated at semi-commercial scale in 2024. Corporate sustainability reporting frameworks increasingly required scope 3 disclosures, encouraging suppliers to demonstrate material traceability. Regional clean manufacturing grants supported retrofitting of 14 plants for renewable feedstock handling, creating favorable conditions for accelerated adoption of bio-based coating resins.

Growth in advanced protective coatings for EV battery enclosures

Electric vehicle assembly expanded across new plants commissioned during 2023 and 2024, with 9 facilities integrating dedicated battery enclosure lines. The Department of Transportation recorded 1300000 EV registrations in 2024, intensifying requirements for thermal management and corrosion protection of enclosures. Safety standards issued by national testing laboratories in 2023 specified flame-retardant and dielectric performance thresholds for enclosure coatings. Manufacturing pilots validated 4 multilayer coating architectures to improve abrasion resistance during underbody exposure. Federal infrastructure grants supported localized battery supply chains, increasing demand for specialized protective coating systems within EV manufacturing ecosystems.

Future Outlook

Through 2030, the market will reflect accelerating regulatory alignment, deeper automation within paint shops, and broader penetration of low-emission technologies. Regional manufacturing hubs are expected to sustain investment momentum, while refinish channels adapt to advanced finish expectations and faster curing processes. Policy continuity and supply chain localization will shape technology roadmaps.

Major Players

- PPG Industries

- Axalta Coating Systems

- BASF Coatings

- Sherwin-Williams

- AkzoNobel

- Nippon Paint Automotive Coatings

- Kansai Paint

- Covestro

- Allnex

- Clariant

- LANXESS

- Solvay

- Dow

- Arkema

- RPM International

Key Target Audience

- Automotive OEM manufacturing groups

- Tier 1 and Tier 2 component suppliers

- Refinish distributors and body shop networks

- Chemical and resin producers

- Equipment and paint shop automation providers

- Logistics and specialty chemical distributors

- Investments and venture capital firms

- Government and regulatory bodies including the Environmental Protection Agency and Department of Transportation

Research Methodology

Step 1: Identification of Key Variables

Key variables were defined across coating technologies, application stages, regulatory constraints, and operational requirements of OEM and refinish environments. Input parameters emphasized compliance thresholds, process compatibility, and durability specifications. Variables were screened for relevance to production throughput and environmental performance outcomes.

Step 2: Market Analysis and Construction

The analytical framework mapped supply chains, application workflows, and technology adoption pathways across regional manufacturing hubs. Operational indicators were synthesized to construct demand patterns aligned with production scheduling and refinish cycles. Scenario structuring reflected regulatory evolution and infrastructure readiness.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were stress-tested through structured consultations with manufacturing engineers, environmental compliance specialists, and coating formulation experts. Process-level insights validated feasibility of technology transitions and operational constraints. Institutional indicators were used to confirm regulatory and infrastructure alignment.

Step 4: Research Synthesis and Final Output

Findings were consolidated into a coherent narrative integrating regulatory context, operational dynamics, and technology pathways. Cross-validation ensured internal consistency across sections. Outputs were refined to support strategic planning and implementation considerations for industry stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and OEM/refinish coatings scope alignment, Primary interviews with US OEM paint shops and Tier-1 coating suppliers, Channel checks with refinish distributors and body shop networks, Plant-level capacity and utilization benchmarking of US coating facilities, Raw material price tracking for resins pigments and solvents, Import-export flow analysis for automotive-grade coatings, Regulatory and compliance review of EPA VOC and state-level mandates)

- Definition and Scope

- Market evolution

- Usage and coating application pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising vehicle production and model refresh cycles in the US

Shift toward waterborne and low-VOC coatings driven by regulations

Increasing demand for premium finishes and customization

Growth of electric vehicle manufacturing requiring specialized coatings

Rising collision repair volumes supporting refinish demand

Technological advancements in fast-curing and high-durability coatings - Challenges

Volatility in raw material prices for resins and pigments

Stringent VOC and hazardous air pollutant regulations increasing compliance costs

High capital expenditure for coating line upgrades in OEM plants

Skilled labor shortages in paint shops and refinish centers

Environmental scrutiny over solvent usage and waste disposal

Supply chain disruptions for specialty additives and pigments - Opportunities

Adoption of bio-based and sustainable resin systems

Growth in advanced protective coatings for EV battery enclosures

Expansion of high-solid and powder coatings in OEM applications

Digital color matching and smart coating solutions for refinish

Partnerships with OEMs for long-term coating supply contracts

Aftermarket growth driven by vehicle aging fleet in the US - Trends

Increasing penetration of waterborne basecoats across OEM plants

Rising use of matte and textured finishes in premium segments

Integration of automation and robotics in paint shops

Adoption of anti-microbial and self-healing coating technologies

Growth of low-temperature curing technologies to reduce energy use

Customization and limited-edition color programs by OEMs - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Coating Type (in Value %)

Primer

Basecoat

Clearcoat

Electrocoat - By Technology (in Value %)

Waterborne coatings

Solvent-borne coatings

Powder coatings

UV-cured coatings - By Resin Type (in Value %)

Acrylic

Polyurethane

Epoxy

Alkyd

Polyester - By Vehicle Type (in Value %)

Passenger vehicles

Light commercial vehicles

Heavy commercial vehicles

Electric vehicles - By Application (in Value %)

OEM coatings

Refinish coatings

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product portfolio breadth, Technology leadership in low-VOC systems, OEM approvals and long-term supply contracts, Manufacturing footprint in the US, Cost competitiveness and pricing flexibility, R&D investment intensity, Supply chain reliability and local sourcing, Sustainability and regulatory compliance performance)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

PPG Industries

Axalta Coating Systems

BASF Coatings

Sherwin-Williams

AkzoNobel

Nippon Paint Automotive Coatings

Kansai Paint

Covestro

Allnex

Clariant

LANXESS

Solvay

Dow

Arkema

RPM International

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now