Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Semiconductors market current size stands at around USD ~ million, reflecting robust integration of vehicle electronics across safety, powertrain control, infotainment, and advanced driver assistance functions. Demand is shaped by increasing electronic content per vehicle, platform standardization, and stringent reliability requirements for automotive-grade components. Supply is influenced by qualification cycles, fabrication node transitions, and long-term sourcing agreements that prioritize resilience and lifecycle continuity across vehicle programs.

The market is concentrated across manufacturing and technology hubs with mature automotive ecosystems, deep supplier networks, and established testing and validation infrastructure. Demand clusters around regions with strong vehicle assembly footprints, software-defined vehicle development centers, and power electronics competence. Policy frameworks emphasizing domestic manufacturing resilience, functional safety compliance, and secure supply chains reinforce localized partnerships among vehicle manufacturers, module suppliers, and component vendors, accelerating co-development and long-term sourcing alignment.

Market Segmentation

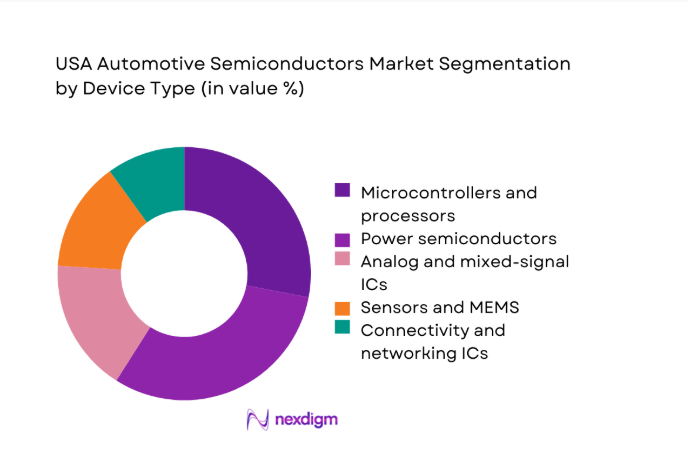

By Device Type

Power and control devices dominate value contribution due to electrification and safety-critical compute requirements across propulsion, chassis, and driver assistance domains. Wide-bandgap power devices are gaining traction in traction inverters and onboard chargers, while microcontrollers and domain processors capture rising content as zonal architectures replace distributed control units. Sensors and connectivity ICs expand with perception and vehicle networking needs, yet remain secondary to power semiconductors and compute platforms that carry higher qualification costs, longer validation cycles, and deeper integration into vehicle platforms.

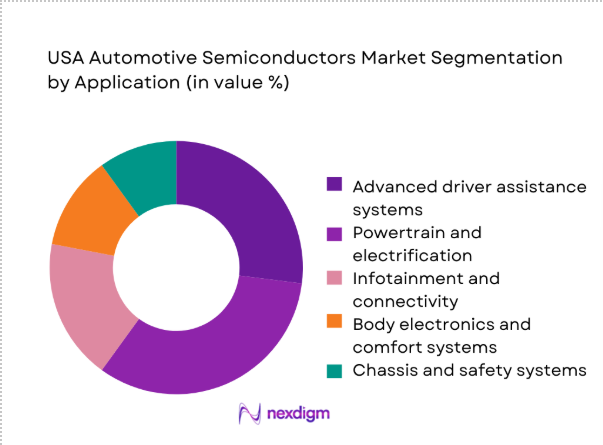

By Application

Electrification and advanced driver assistance account for the largest value pools as vehicles integrate high-voltage architectures, perception stacks, and centralized compute. Powertrain control and battery management drive sustained demand for power devices and safety-qualified controllers. Infotainment and connectivity grow with software-defined features, while body electronics maintain steady volumes across comfort and access systems. Chassis and safety applications remain structurally important due to regulatory requirements, redundancy design, and validation rigor that increase silicon content per platform.

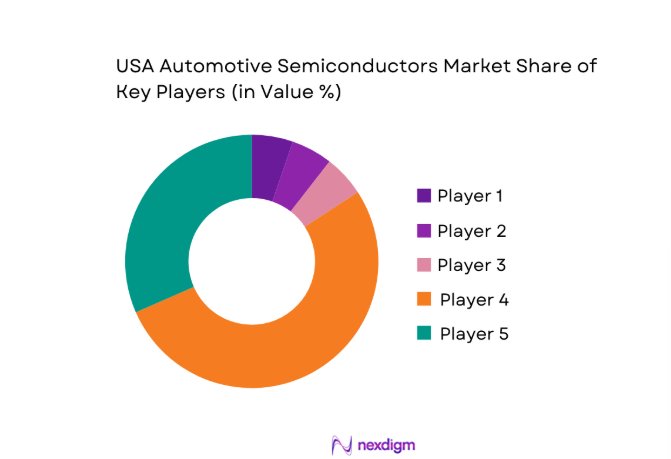

Competitive Landscape

The competitive landscape is characterized by vertically integrated portfolios, long-term supply agreements with vehicle manufacturers and Tier-1 suppliers, and differentiated capabilities across power electronics, safety-certified controllers, and automotive-qualified manufacturing. Competitive positioning depends on process node roadmaps, lifecycle support commitments, and collaboration across vehicle platform programs, alongside compliance readiness for functional safety and cybersecurity requirements.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| NXP Semiconductors | 2006 | Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| onsemi | 1999 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

USA Automotive Semiconductors Market Analysis

Growth Drivers

Electrification-driven increase in power device content per vehicle

Electrification increases semiconductor intensity per vehicle through traction inverters, onboard chargers, DC-DC converters, and battery management systems. Vehicle production in the United States exceeded 10 in 2023 and reached 11 in 2024, raising aggregate device demand across high-voltage architectures. Public charging connectors installed expanded from 170000 in 2023 to 195000 in 2024, accelerating deployment of power modules and control ICs. Safety certification mandates require redundant gate drivers and isolation components, increasing component counts. Utility interconnection approvals processed rose from 4200 in 2023 to 5100 in 2024, reinforcing grid-compatible power electronics integration within vehicles.

Rising ADAS penetration boosting compute and sensor demand

Advanced driver assistance adoption is accelerating as safety mandates and consumer demand expand perception and compute content. New vehicle models launched with multi-camera and radar configurations increased from 58 in 2023 to 71 in 2024, driving higher processor throughput and sensor fusion requirements. Roadway safety initiatives reported 43000 fatalities in 2023 and 41000 in 2024, reinforcing regulatory emphasis on collision mitigation technologies. Dedicated ADAS validation miles logged by test fleets exceeded 12000000 in 2023 and 14500000 in 2024, increasing demand for high-reliability SoCs, memory controllers, and automotive Ethernet transceivers integrated into zonal architectures.

Challenges

Automotive-grade qualification cycles extending time-to-market

Automotive qualification imposes lengthy validation cycles across functional safety, reliability, and environmental stress. AEC testing protocols require more than 1000 hours of high-temperature operating life and over 200 temperature cycles, extending development timelines. Platform freeze milestones in vehicle programs often occur 24 months before start of production, constraining semiconductor design changes. In 2023, over 4800 validation test lots were queued across accredited labs, rising to 5200 in 2024, creating bottlenecks. Compliance with ISO 26262 and cybersecurity process audits adds documentation burdens that slow iteration and limit rapid adoption of new nodes within production vehicle platforms.

Foundry capacity constraints for mature automotive nodes

Automotive devices rely heavily on mature nodes such as 90, 65, and 40, where capacity is contested by industrial and IoT demand. Fab utilization at these nodes exceeded 85 in 2023 and reached 88 in 2024, constraining allocation flexibility for automotive-grade lots. Automotive qualification restricts rapid migration to alternative processes due to revalidation requirements. Wafer lead times extended from 18 weeks in 2023 to 24 weeks in 2024 for qualified lines, increasing buffer inventory needs across Tier-1 suppliers. Equipment delivery cycles for mature-node tools surpassed 52 weeks, limiting near-term capacity expansion and exposing supply risk.

Opportunities

SiC and GaN adoption in EV inverters and onboard chargers

Wide-bandgap adoption enables higher switching frequencies, reduced thermal losses, and compact powertrain architectures. EV platform certifications increased from 24 in 2023 to 31 in 2024, expanding qualified use cases for SiC MOSFETs and GaN devices. Fast-charging corridors added 6200 new DC fast chargers in 2024, increasing demand for vehicle-side power electronics compatible with higher voltage classes. Grid interconnection standards updated in 2023 mandate tighter harmonic limits, favoring advanced power devices. Workforce training programs certified 1800 power electronics technicians in 2024, supporting broader deployment and system integration across vehicle programs.

Zonal and centralized compute architectures increasing high-value SoC content

Vehicle architectures are shifting from distributed ECUs toward zonal and centralized compute, increasing demand for high-integration SoCs and networking ICs. Zonal controller pilots expanded from 6 platforms in 2023 to 11 in 2024 across major vehicle programs. Automotive Ethernet ports per vehicle increased from 8 in 2023 to 14 in 2024, necessitating higher-throughput switching silicon. Software-defined vehicle roadmaps adopted by 9 OEM programs in 2024 emphasize centralized compute consolidation. Validation labs added 27 new hardware-in-the-loop benches in 2024 to support zonal architecture testing, enabling faster integration of high-performance automotive-grade processors.

Future Outlook

Future growth will be shaped by the continued shift toward software-defined vehicles, zonal compute architectures, and electrified powertrains. Policy support for domestic manufacturing resilience and secure supply chains will reinforce localized partnerships. As validation frameworks mature, adoption of advanced power devices and centralized compute platforms is expected to accelerate across upcoming vehicle programs through the latter half of the decade.

Major Players

- Infineon Technologies

- NXP Semiconductors

- Texas Instruments

- onsemi

- STMicroelectronics

- Renesas Electronics

- Analog Devices

- Microchip Technology

- Qualcomm

- NVIDIA

- Broadcom

- Bosch Semiconductor

- GlobalFoundries

- Intel

- Wolfspeed

Key Target Audience

- Automotive OEM procurement and platform engineering teams

- Tier-1 automotive module and system integrators

- Power electronics and vehicle compute platform manufacturers

- Semiconductor foundries and packaging service providers

- Authorized electronics distributors and channel partners

- Investments and venture capital firms

- Government and regulatory bodies with agency names

- Automotive aftermarket electronics service providers

Research Methodology

Step 1: Identification of Key Variables

Key variables were defined across device categories, qualification standards, process nodes, and application domains relevant to vehicle architectures. Policy frameworks, safety certification requirements, and domestic manufacturing initiatives were mapped to establish boundary conditions. Demand indicators from vehicle programs and charging infrastructure deployment were aligned to usage contexts.

Step 2: Market Analysis and Construction

The market construct was built by mapping semiconductor device classes to vehicle subsystems and platform architectures. Supply-side capabilities across qualified manufacturing nodes and packaging formats were assessed. Channel structures and lifecycle support requirements were integrated to reflect long-term sourcing realities within automotive programs.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on adoption pathways, architecture shifts, and qualification bottlenecks were validated through consultations with platform engineers, reliability specialists, and supply chain managers. Validation focused on feasibility across certification cycles, integration complexity, and manufacturing readiness aligned with vehicle program timelines.

Step 4: Research Synthesis and Final Output

Insights were synthesized into structured narratives across drivers, challenges, and opportunities, ensuring internal consistency and market specificity. Findings were reconciled with policy environments, infrastructure maturity, and ecosystem readiness to present a coherent outlook aligned with near-term deployment realities.

- Executive Summary

- Research Methodology (Market Definitions and vehicle-grade semiconductor taxonomy, OEM and Tier-1 procurement mapping and bill-of-materials teardown analysis, Foundry capacity utilization and node migration tracking for automotive-qualified processes, ASP and cost curve modeling by device class and qualification grade, Channel checks with distributors and authorized resellers for lead times and inventory, Import-export and trade flow analysis for semiconductor components into the US automotive supply chain)

- Definition and Scope

- Market evolution

- Usage pathways across vehicle architectures

- Ecosystem structure

- Supply chain and channel structure

- Regulatory and qualification environment

- Growth Drivers

Electrification-driven increase in power device content per vehicle

Rising ADAS penetration boosting compute and sensor demand

Vehicle software-defined architectures increasing MCU and SoC adoption

US reshoring incentives expanding local automotive-grade semiconductor sourcing

Stricter safety standards driving redundancy and functional safety silicon

Connected vehicle features increasing networking and connectivity IC demand - Challenges

Automotive-grade qualification cycles extending time-to-market

Foundry capacity constraints for mature automotive nodes

Supply chain exposure to geopolitical trade restrictions

Long-term OEM supply agreements limiting pricing flexibility

Complex validation requirements for safety-critical applications

Inventory volatility and demand forecasting inaccuracies across model cycles - Opportunities

SiC and GaN adoption in EV inverters and onboard chargers

Zonal and centralized compute architectures increasing high-value SoC content

Domestic fab investments creating local sourcing partnerships with OEMs

Lifecycle management and second-source strategies for long-lived vehicle platforms

Cybersecurity hardware integration within vehicle ECUs

Edge AI acceleration for perception and in-cabin monitoring - Trends

Migration toward 28nm and below for automotive compute

Standardization of zonal controllers reducing ECU count but increasing silicon value

Growing use of wide-bandgap power devices in EV platforms

Long-term supply agreements between OEMs and semiconductor vendors

Increased use of functional safety and secure elements

Vertical collaboration between OEMs, Tier-1s, and chipmakers - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Device Type (in Value %)

Microcontrollers and processors

Power semiconductors

Analog and mixed-signal ICs

Sensors and MEMS

Connectivity and networking ICs

Memory devices - By Vehicle Type (in Value %)

Passenger vehicles

Light commercial vehicles

Heavy commercial vehicles

Electric vehicles

Hybrid vehicles - By Application (in Value %)

Advanced driver assistance systems

Powertrain and electrification

Infotainment and connectivity

Body electronics and comfort systems

Chassis and safety systems - By Propulsion Architecture (in Value %)

Internal combustion engine vehicles

Battery electric vehicles

Plug-in hybrid electric vehicles

Hybrid electric vehicles

Fuel cell electric vehicles - By Sales Channel (in Value %)

Direct OEM supply

Tier-1 module suppliers

Authorized semiconductor distributors

Aftermarket and service channels

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (technology node roadmap, automotive qualification portfolio, product breadth across device types, OEM and Tier-1 partnerships, manufacturing footprint and foundry access, pricing and long-term supply terms, functional safety and security certifications, innovation pipeline and IP strength)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Infineon Technologies

NXP Semiconductors

Texas Instruments

onsemi

STMicroelectronics

Renesas Electronics

Analog Devices

Microchip Technology

Qualcomm

NVIDIA

Broadcom

Bosch Semiconductor

GlobalFoundries

Intel

Wolfspeed

- Demand and utilization drivers

- Procurement and sourcing dynamics

- Buying criteria and vendor selection

- Budget allocation and long-term supply agreements

- Implementation barriers and qualification risks

- Post-purchase support and lifecycle management expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now