Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA autonomous aircraft market is experiencing rapid growth, driven by increasing investments in unmanned aerial vehicle (UAV) technologies and the growing demand for efficient air transportation solutions. Based on a recent historical assessment, the market size for autonomous aircraft is expected to reach approximately USD ~ billion by 2025. The growth of this market is primarily influenced by advancements in artificial intelligence, autonomous flight technologies, and government regulations promoting UAVs in both military and commercial applications. The increasing need for logistics, surveillance, and passenger transport solutions also contributes to the expansion of this market.

The USA market for autonomous aircraft is dominated by several key regions, particularly those with strong aerospace industries such as California, Florida, and Texas. These states benefit from a combination of advanced technological ecosystems, large aerospace manufacturers, and supportive regulatory environments. California, with its high concentration of tech firms, is a hub for autonomous aircraft startups, while Texas and Florida are crucial for military and commercial applications. The dominance of these regions is also supported by federal initiatives and defense contracts focused on the development of unmanned aircraft systems.

Market Segmentation

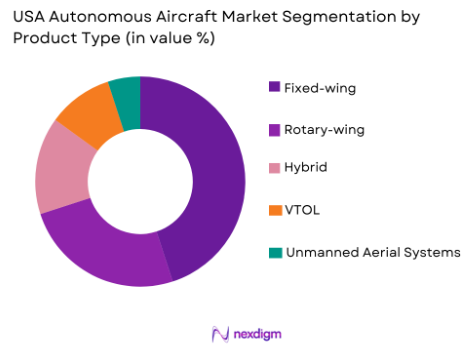

By Product Type

The USA Autonomous Aircraft Market is segmented by product type into fixed-wing, rotary-wing, hybrid, VTOL (Vertical Take-off and Landing), and unmanned aerial systems (UAS). Recently, fixed-wing autonomous aircraft have the largest market share due to their suitability for long-range flight, efficient fuel consumption, and cost-effectiveness for both military and commercial applications. Fixed-wing UAVs are increasingly adopted for cargo delivery, surveillance, and aerial mapping. Their capability to cover large distances with minimal maintenance and operational costs gives them a significant edge over other sub-segments, particularly for commercial logistics and military reconnaissance missions. The high demand for these aircraft in surveillance, agriculture, and package delivery services further accelerates their growth.

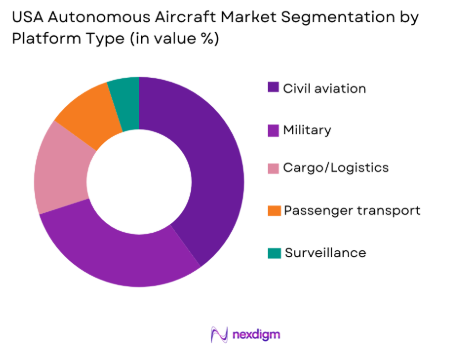

By Platform Type

The USA Autonomous Aircraft Market is segmented by platform type into civil aviation, military, cargo/logistics, passenger transport, and surveillance platforms. Among these, civil aviation platforms dominate the market share due to the increasing adoption of UAVs for commercial applications such as parcel delivery, aerial photography, and surveillance. The growing need for more efficient and cost-effective transportation methods has driven demand for autonomous aircraft in the civil sector. Additionally, the rise of urban air mobility (UAM) projects, including drone taxis, has also played a significant role in boosting the demand for autonomous civil aircraft. The regulatory approval of autonomous aircraft for commercial purposes further accelerates their adoption across various civil aviation sectors.

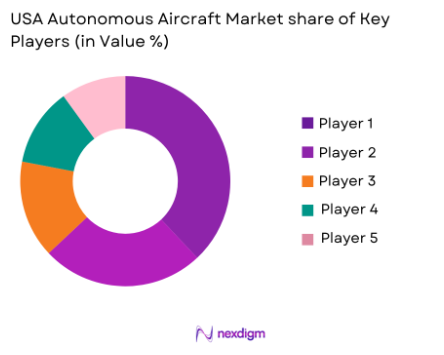

Competitive Landscape

The USA autonomous aircraft market is highly competitive, with significant consolidation in the aerospace and defense sectors, as well as increased collaboration between established players and tech startups. Major players are focusing on advancing autonomous flight technologies, expanding their product portfolios, and forming partnerships to tap into the growing demand for UAV solutions. The market is characterized by a blend of large corporations, such as Boeing and Lockheed Martin, and agile startups, like Joby Aviation and Lilium, that are leading the charge in innovation. The influence of these major players is driving market trends toward more efficient, reliable, and scalable autonomous systems for both military and civilian use.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Product Innovation Focus |

| Boeing | 1916 | Chicago, IL | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, MD | ~ | ~ | ~ | ~ | ~ |

| Joby Aviation | 2009 | Santa Cruz, CA | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church, VA | ~ | ~ | ~ | ~ | ~ |

| Lilium Aviation | 2015 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

USA Autonomous Aircraft Market Analysis

Growth Drivers

Technological Advancements in AI and Robotics

The technological advancements in AI and robotics play a pivotal role in driving the growth of the autonomous aircraft market in the USA. Autonomous aircraft systems rely heavily on AI technologies for navigation, obstacle detection, and mission planning, which has led to significant improvements in their operational capabilities. These advancements enable aircraft to perform tasks with minimal human intervention, reducing operational risks and costs. AI systems are also essential for data analysis, predictive maintenance, and real-time decision-making, ensuring optimal performance of autonomous aircraft. Robotics advancements further enable these aircraft to carry out precise movements and handle various complex tasks, including cargo handling, surveillance, and even passenger transportation. As AI technologies continue to evolve, autonomous aircraft are expected to become more reliable, efficient, and capable of handling a broader range of applications. With increasing investments in AI research and development, these advancements are expected to propel the market forward in the coming years.

Regulatory and Government Support

Government regulations and policy support are another significant driver for the growth of the autonomous aircraft market. Federal agencies such as the Federal Aviation Administration (FAA) in the USA are playing a critical role in establishing the regulatory framework necessary for the integration of autonomous aircraft into the national airspace system. Regulatory support includes setting standards for autonomous flight operations, air traffic management, safety protocols, and certification processes for UAVs. These regulations ensure that autonomous aircraft are safely integrated into existing aviation infrastructure, which is crucial for public acceptance and adoption. Moreover, government initiatives aimed at supporting research and development in autonomous aviation technologies, along with defense contracts, create a conducive environment for innovation and market expansion. With favorable regulations and continued government backing, autonomous aircraft are poised to become a significant part of the aerospace and defense industries, enabling more efficient and safer air travel and transportation.

Market Challenges

Regulatory Hurdles and Integration into National Airspace

One of the main challenges faced by the USA autonomous aircraft market is navigating the complex regulatory environment and integrating autonomous aircraft into the national airspace system. While there has been progress in regulatory frameworks, the approval processes for autonomous aircraft remain stringent and time-consuming. This regulatory uncertainty can delay product development and market entry, limiting the ability of manufacturers to meet the growing demand for UAV solutions. Additionally, airspace integration remains a complex issue, as autonomous aircraft need to coexist with manned aircraft while adhering to safety standards. Challenges include ensuring that autonomous aircraft can safely navigate airspace, communicate with air traffic control, and avoid conflicts with other air traffic. The slow pace of regulatory approval and the need for new infrastructure and technology to support these systems continue to present significant challenges to the widespread adoption of autonomous aircraft.

Public Perception and Trust Issues

Another challenge facing the autonomous aircraft market is the public’s perception of safety and reliability. While autonomous systems have demonstrated their potential in various industries, there are still concerns regarding their ability to operate safely in all conditions. Accidents or malfunctions involving autonomous aircraft could damage public trust and slow the adoption of these systems. Furthermore, regulatory bodies and manufacturers must address concerns about cybersecurity risks associated with autonomous aircraft, as these systems are highly reliant on networked technologies. Cyberattacks or vulnerabilities in autonomous flight systems could lead to catastrophic failures. Therefore, ensuring the public’s confidence in autonomous aircraft is essential for their widespread adoption. Manufacturers and regulators need to continuously work to improve the reliability, safety, and security of autonomous systems to mitigate these concerns and build trust among the public.

Opportunities

Expansion of Urban Air Mobility (UAM)

The expansion of urban air mobility (UAM) presents significant opportunities for the USA autonomous aircraft market. UAM refers to the use of autonomous aircraft for short-distance urban transport, including passenger air taxis, cargo drones, and other air-based services within cities. As urbanization continues to grow, traditional transportation infrastructure becomes increasingly congested, leading to a need for alternative modes of transport. Autonomous aircraft can help alleviate traffic congestion and provide more efficient, faster, and environmentally friendly alternatives to ground-based transportation. Furthermore, advancements in electric vertical takeoff and landing (eVTOL) technology are enabling the development of aircraft that can operate in dense urban environments with minimal noise and environmental impact. The commercialization of UAM solutions presents a substantial market opportunity, particularly in cities with high traffic congestion and growing populations. As UAM becomes a reality, autonomous aircraft will play a central role in reshaping urban transportation systems.

Military and Defense Applications

Military and defense applications present another key opportunity for the USA autonomous aircraft market. Autonomous aircraft are already being used for a variety of defense purposes, including surveillance, reconnaissance, combat missions, and logistics. The growing need for more effective and efficient military operations has driven increased demand for unmanned systems, which can operate in high-risk environments without endangering human lives. Autonomous aircraft offer several advantages, including the ability to fly in challenging environments, perform long-duration missions, and conduct real-time data collection and analysis. The increasing investments in defense technologies and the demand for advanced unmanned systems create a significant opportunity for manufacturers of autonomous aircraft. As military forces worldwide continue to explore autonomous solutions for tactical and strategic operations, the USA market is poised to benefit from rising defense contracts and the demand for cutting-edge UAV technologies.

Future Outlook

Over the next five years, the USA autonomous aircraft market is expected to experience steady growth, driven by ongoing advancements in technology, increasing regulatory support, and rising demand for efficient air transportation solutions. Technological developments such as improved battery life, AI, and autonomous navigation systems are expected to enhance the capabilities of autonomous aircraft, enabling them to handle a wider range of applications. Regulatory bodies, including the FAA, are expected to continue developing frameworks that facilitate the integration of autonomous aircraft into national airspace, providing a favorable environment for growth. Additionally, consumer and commercial demand for more efficient transportation solutions, particularly in urban areas, is expected to increase, driving further adoption of autonomous aircraft for urban air mobility, cargo delivery, and passenger transport.

Major Players

- Boeing

- Lockheed Martin

- Joby Aviation

- Northrop Grumman

- Lilium Aviation

- Volocopter

- Aurora Flight Sciences

- Textron

- General Atomics

- Raytheon Technologies

- Airbus

- Thales Group

- DJI Innovations

- Wing Aviation

- AeroVironment

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Military and defense contractors

- Commercial aviation operators

- Logistics and courier companies

- Urban air mobility providers

- Autonomous vehicle developers

Research Methodology

Step 1: Identification of Key Variables

The identification of key variables involves determining the essential factors that influence the market, such as technological trends, regulatory requirements, and industry needs.

Step 2: Market Analysis and Construction

Market analysis and construction involve studying current market trends, historical performance, and future forecasts to develop a comprehensive understanding of market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultation is conducted to validate hypotheses, gather insights from industry leaders, and ensure the accuracy of the findings.

Step 4: Research Synthesis and Final Output

Research synthesis involves combining collected data and expert insights to generate a cohesive report, providing actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for autonomous delivery systems

Technological advancements in AI and robotics

Government initiatives supporting autonomous aviation

Increased investment in unmanned aircraft technologies

Expanding applications in urban air mobility - Market Challenges

Regulatory challenges and airspace integration

High cost of autonomous aircraft systems

Technological limitations in safety and reliability

Public acceptance and trust in autonomous systems

Security and cybersecurity concerns for autonomous platforms - Market Opportunities

Growth in urban air mobility applications

Advancements in autonomous cargo transport

Rising demand for autonomous surveillance systems - Trends

Increasing collaborations between aerospace manufacturers and tech companies

Emerging use of hybrid electric propulsion in autonomous aircraft

Focus on sustainable aviation solutions

Growth of drone-based delivery services in urban areas

Integration of advanced sensors for autonomous navigation - Government Regulations & Defense Policy

FAA regulations for unmanned aircraft systems

Military adaptation of autonomous aircraft

Government funding for autonomous aviation research

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed-wing Autonomous Aircraft

Rotary-wing Autonomous Aircraft

Hybrid Autonomous Aircraft

Vertical Take-off and Landing (VTOL) Aircraft

Unmanned Aerial Systems (UAS) - By Platform Type (In Value%)

Civil Aviation Platforms

Military Platforms

Cargo/Logistics Platforms

Passenger Transport Platforms

Surveillance Platforms - By Fitment Type (In Value%)

OEM (Original Equipment Manufacturer)

Aftermarket Fitments

Custom Built Aircraft

Modular Systems

Autonomous Retrofit Systems - By End User Segment (In Value%)

Commercial Operators

Government and Military

Research and Development Organizations

Logistics and Supply Chain Companies

Agricultural and Environmental Services - By Procurement Channel (In Value%)

Direct Procurement

Third-Party Procurement

Online Platforms

Government Contracts

Leasing Services - By Material / Technology (In Value%)

Carbon Fiber Composites

Lightweight Alloys

Battery Technology

Electric Propulsion Systems

AI and Machine Learning Technologies

- Market share snapshot of major players

- Cross Comparison Parameters (Price, Technology, System Performance, Customization, Availability, Safety, Battery Life, Range, Certification, Customer Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Boeing

Lockheed Martin

General Atomics

Northrop Grumman

AeroVironment

Raytheon Technologies

Thales Group

Aurora Flight Sciences

DJI Innovations

Airbus

Textron

Volocopter

Lilium Aviation

Joby Aviation

Wing Aviation

- Expansion of autonomous aircraft in commercial logistics

- Military applications driving autonomous aircraft development

- Increased adoption of autonomous aircraft in agricultural services

- Research organizations pushing innovation in autonomous aviation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

- By System Type (In Value%)

Fixed-wing Autonomous Aircraft

Rotary-wing Autonomous Aircraft

Hybrid Autonomous Aircraft

Vertical Take-off and Landing (VTOL) Aircraft

Unmanned Aerial Systems (UAS) - By Platform Type (In Value%)

Civil Aviation Platforms

Military Platforms

Cargo/Logistics Platforms

Passenger Transport Platforms

Surveillance Platforms - By Fitment Type (In Value%)

OEM (Original Equipment Manufacturer)

Aftermarket Fitments

Custom Built Aircraft

Modular Systems

Autonomous Retrofit Systems - By End User Segment (In Value%)

Commercial Operators

Government and Military

Research and Development Organizations

Logistics and Supply Chain Companies

Agricultural and Environmental Services - By Procurement Channel (In Value%)

Direct Procurement

Third-Party Procurement

Online Platforms

Government Contracts

Leasing Services - By Material / Technology (In Value%)

Carbon Fiber Composites

Lightweight Alloys

Battery Technology

Electric Propulsion Systems

AI and Machine Learning Technologies

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now