Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Autonomous Driving Systems market reached approximately USD ~ billion based on a recent historical assessment, driven by increasing investments in artificial intelligence, sensor fusion technologies, and advanced mobility solutions. Strong funding from automotive OEMs and technology firms has accelerated commercialization, while regulatory pilots and smart mobility initiatives have expanded deployment. Growing demand for safety systems and reduction in road fatalities continues to support system adoption across passenger and commercial vehicle segments.

Key regions such as California, Michigan, and Texas dominate the market due to strong automotive ecosystems, technology hubs, and supportive testing regulations. California leads through innovation clusters and autonomous testing permits, while Michigan benefits from legacy automotive manufacturing and R&D infrastructure. Texas has emerged due to favorable regulatory frameworks and logistics demand. These regions collectively attract investments from OEMs and technology companies, enabling large scale deployment and real world testing environments.

Market Segmentation

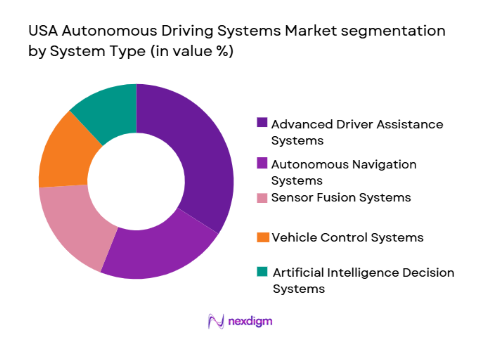

By System Type

USA Autonomous Driving Systems market is segmented by system type into Advanced Driver Assistance Systems, Autonomous Navigation Systems, Sensor Fusion Systems, Vehicle Control Systems, and Artificial Intelligence Decision Systems. Recently, Advanced Driver Assistance Systems has a dominant market share due to widespread adoption across passenger vehicles, regulatory push for safety features, and cost-effective integration compared to fully autonomous systems, making it a preferred choice for automakers and consumers.

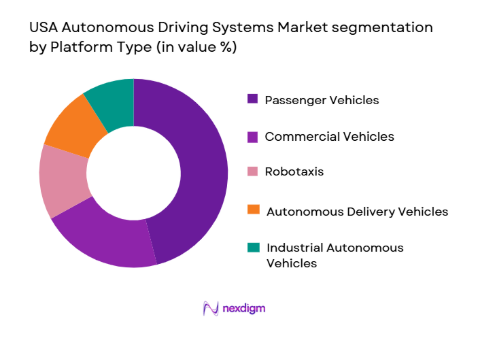

By Platform Type

USA Autonomous Driving Systems market is segmented by platform type into Passenger Vehicles, Commercial Vehicles, Robotaxis, Autonomous Delivery Vehicles, and Industrial Autonomous Vehicles. Recently, Passenger Vehicles has a dominant market share due to high consumer demand, strong OEM integration, and increasing inclusion of semi autonomous features in mainstream vehicle models, supported by regulatory safety mandates and competitive differentiation strategies among manufacturers.

Competitive Landscape

The USA Autonomous Driving Systems market is moderately consolidated, with a mix of technology companies and traditional automotive manufacturers competing through innovation and strategic partnerships. Major players dominate through proprietary AI platforms, sensor technologies, and large-scale testing capabilities. Collaborations between OEMs and technology firms are shaping the ecosystem, while high entry barriers limit new entrants. Competitive intensity remains strong due to continuous advancements and significant capital investments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Autonomous Level Capability |

| Waymo | 2009 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

| Tesla | 2003 | Austin, USA | ~ | ~ | ~ | ~ | ~ |

| Cruise | 2013 | San Francisco, USA | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| Mobileye | 1999 | Jerusalem, Israel | ~ | ~ | ~ | ~ | ~ |

USA Autonomous Driving Systems Market Analysis

Growth Drivers

Rapid Integration of Advanced Safety and ADAS Technologies Across Vehicles:

The widespread integration of advanced driver assistance systems into passenger and commercial vehicles is significantly driving the USA Autonomous Driving Systems market. Automakers are increasingly incorporating features such as lane keeping assist, adaptive cruise control, and automated braking to comply with safety regulations and enhance vehicle appeal. These technologies serve as foundational components for higher levels of autonomy, enabling gradual transition toward fully autonomous driving. Consumer awareness regarding road safety has increased substantially, encouraging adoption of vehicles equipped with these systems. Insurance incentives and regulatory mandates further reinforce adoption trends across various vehicle segments. Additionally, advancements in sensor technologies, including radar, lidar, and cameras, have improved system reliability and cost efficiency. OEMs are leveraging economies of scale to integrate these systems into mid-range vehicles, expanding market penetration. Continuous innovation in AI algorithms has enhanced decision-making capabilities and system accuracy. The combination of safety, convenience, and regulatory support continues to accelerate demand for autonomous driving systems across the automotive ecosystem.

Expansion of Mobility as a Service and Autonomous Fleet Deployment:

The growing demand for shared mobility solutions and fleet based transportation services is a major growth driver for the USA Autonomous Driving Systems market. Companies are increasingly investing in robotaxi services and autonomous delivery fleets to reduce operational costs and improve efficiency. Urbanization and changing consumer preferences toward on demand transportation have accelerated the adoption of mobility as a service platforms. Autonomous fleets offer advantages such as reduced labor costs, optimized routing, and improved asset utilization. Technology companies and automotive manufacturers are collaborating to develop scalable autonomous solutions for commercial deployment. Regulatory support in selected states has enabled pilot programs and limited commercial operations of autonomous vehicles. The logistics and e commerce sectors are also driving demand for autonomous delivery systems, particularly for last mile operations. Continuous improvements in vehicle connectivity and data analytics are enhancing fleet management capabilities. As infrastructure and regulatory frameworks evolve, the deployment of autonomous fleets is expected to expand significantly across urban and suburban regions.

Market Challenges

High Capital Investment and Development Costs of Autonomous Technologies:

The development and deployment of autonomous driving systems require substantial capital investment, posing a major challenge for market growth. Companies must invest heavily in research and development, sensor technologies, software engineering, and testing infrastructure to achieve reliable autonomy. The cost of high precision lidar systems, computing platforms, and safety validation processes remains significantly high. Smaller companies face difficulties in competing with established players due to financial constraints. Additionally, long development cycles and uncertain returns on investment increase financial risks for stakeholders. The need for extensive real world testing and simulation further adds to operational expenses. Integration of complex systems across hardware and software components requires significant expertise and coordination. Regulatory compliance and certification processes also contribute to increased costs and delays. These financial barriers limit the pace of innovation and commercialization, particularly for emerging players in the ecosystem.

Regulatory Uncertainty and Safety Validation Complexities:

The lack of uniform regulatory frameworks across states presents a significant challenge for the USA Autonomous Driving Systems market. Different states have varying rules regarding testing, deployment, and liability, creating complexities for companies operating nationwide. Ensuring safety and reliability of autonomous systems remains a critical concern, requiring rigorous validation and testing processes. Public perception and trust issues further complicate adoption, especially following high profile incidents involving autonomous vehicles. Legal ambiguities related to liability and insurance in case of accidents create additional challenges for stakeholders. The absence of standardized testing protocols makes it difficult to benchmark system performance across the industry. Companies must continuously adapt to evolving regulations, increasing operational complexity. Collaboration between regulators, industry players, and policymakers is essential to establish clear guidelines. Until regulatory harmonization is achieved, market expansion will continue to face structural barriers.

Opportunities

Growth of Autonomous Logistics and Last Mile Delivery Solutions:

The increasing demand for efficient logistics and last mile delivery services presents a significant opportunity for the USA Autonomous Driving Systems market. E commerce growth has intensified the need for faster and cost effective delivery solutions, driving interest in autonomous delivery vehicles. Companies are exploring the use of self driving vans and robots to optimize delivery operations and reduce labor dependency. Autonomous systems enable continuous operations, improving efficiency and reducing delivery times. Technological advancements in navigation and obstacle detection are enhancing the reliability of these systems. Partnerships between logistics companies and technology providers are accelerating deployment across urban areas. Regulatory approvals for pilot programs are enabling real world testing and gradual commercialization. The scalability of autonomous delivery solutions offers long term cost advantages for businesses. As consumer demand for quick delivery continues to rise, autonomous logistics is expected to become a key growth avenue for the market.

Advancements in Artificial Intelligence and Edge Computing for Real Time Decision Making:

Continuous advancements in artificial intelligence and edge computing technologies are creating significant opportunities in the USA Autonomous Driving Systems market. AI driven perception and decision making systems are becoming more sophisticated, enabling vehicles to navigate complex environments with greater accuracy. Edge computing allows real time data processing within the vehicle, reducing latency and improving responsiveness. These advancements enhance safety and reliability, making autonomous systems more viable for widespread adoption. Companies are investing heavily in developing high performance computing platforms to support advanced autonomy levels. Integration of machine learning algorithms is improving system adaptability and performance over time. The availability of large datasets from connected vehicles is further accelerating AI development. Collaboration between technology firms and automotive manufacturers is driving innovation in this space. As these technologies mature, they are expected to significantly enhance the capabilities and adoption of autonomous driving systems.

Future Outlook

The USA Autonomous Driving Systems market is expected to witness steady expansion over the next five years, driven by advancements in artificial intelligence, sensor technologies, and vehicle connectivity. Increasing regulatory clarity and pilot programs will support commercialization, while demand for safer and efficient mobility solutions will continue to rise. Growth in autonomous fleets, logistics applications, and smart city initiatives will further strengthen adoption. Continuous innovation and strategic partnerships will shape the competitive landscape and accelerate market evolution.

Major Players

- Waymo

- Tesla

- Cruise

- NVIDIA

- Mobileye

- Aurora Innovation

- Zoox

- Aptiv

- Bosch

- Continental

- Denso

- Valeo

- Qualcomm

- Intel

- Argo AI

Key Target Audience

- Automotive manufacturers

- Fleet operators

- Ride hailing companies

- Logistics and delivery firms

- Technology platform providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Mobility service providers

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying key variables influencing the USA Autonomous Driving Systems market including technology adoption, regulatory factors, and investment trends. These variables form the foundation for data collection and analysis.

Step 2: Market Analysis and Construction

Data is gathered from industry reports, company disclosures, and government sources to construct market models. Market segmentation and sizing are performed using validated analytical frameworks and industry benchmarks.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through expert interviews with industry professionals and stakeholders. Feedback is incorporated to refine assumptions and ensure accuracy of the analysis.

Step 4: Research Synthesis and Final Output

All insights are synthesized into a structured report, ensuring consistency, reliability, and clarity. Final outputs are reviewed for accuracy and aligned with industry standards and research objectives.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing investments in autonomous vehicle R&D by automotive and technology companies

Rising demand for enhanced road safety and accident reduction systems

Advancements in AI, sensor technologies, and high performance computing

Expansion of mobility as a service and shared transportation models

Government support for smart mobility and autonomous infrastructure development - Market Challenges

High development and deployment costs of autonomous systems

Regulatory uncertainties and varying state level policies

Complexity in achieving full level 5 autonomy

Cybersecurity risks and data privacy concerns

Limited infrastructure readiness for large scale deployment - Market Opportunities

Expansion of autonomous delivery and logistics solutions

Integration of autonomous systems in public transportation networks

Growth in partnerships between automakers and technology firms - Trends

Shift toward software defined vehicles and OTA updates

Increasing adoption of AI driven perception and decision systems

Growth of robotaxi and autonomous fleet services

Integration of 5G and V2X communication technologies

Rising focus on simulation based testing and validation - Government Regulations & Defense Policy

Federal and state level autonomous vehicle testing regulations

Safety standards and certification frameworks for autonomous systems

Government funding for smart mobility and connected infrastructure - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Driver Assistance Systems

Autonomous Navigation Systems

Sensor Fusion Systems

Vehicle Control Systems

Artificial Intelligence Decision Systems - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Robotaxis

Autonomous Delivery Vehicles

Industrial Autonomous Vehicles - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Retrofit Systems

Embedded Vehicle Platforms

Cloud Connected Systems

Edge Computing Integrated Systems - By EndUser Segment (In Value%)

Automotive Manufacturers

Fleet Operators

Ride Hailing Companies

Logistics and Delivery Firms

Public Transportation Authorities - By Procurement Channel (In Value%)

Direct OEM Contracts

Technology Partnerships

Government Procurement Programs

Third Party System Integrators

Software Licensing Models - By Material / Technology (in Value %)

Lidar Based Systems

Radar Based Systems

Camera Vision Systems

AI and Machine Learning Platforms

High Performance Computing Chips

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Technology Capability, Product Portfolio Diversity, AI Integration Level, Sensor Technology Adoption, Strategic Partnerships, R&D Investment Intensity, Geographic Presence, Production Scalability, Software Ecosystem Strength, Regulatory Compliance Readiness)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Waymo

Cruise

Tesla

NVIDIA

Mobileye

Aurora Innovation

Zoox

Argo AI Technologies

Qualcomm Technologies

Intel Corporation

Aptiv PLC

Bosch Mobility Solutions

Continental AG

Denso Corporation

Valeo SA

- Automotive manufacturers focusing on integrating advanced autonomy levels into new models

- Fleet operators adopting autonomous systems to reduce operational costs

- Ride hailing companies investing in robotaxi deployment strategies

- Logistics firms leveraging autonomy for last mile and long haul efficiency

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now