Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Battery Management Systems market is valued at approximately USD ~ based on a recent historical assessment derived from U.S. electric vehicle battery production data reported by the Energy Information Administration and revenue disclosures from automotive battery electronics suppliers. Market expansion is driven by rising electric vehicle battery capacity, increasing deployment of stationary energy storage systems, and stringent battery safety monitoring requirements across automotive and grid-scale applications, alongside OEM electrification programs and battery manufacturing investments nationwide.

California, Michigan, Texas, and Nevada dominate the USA Battery Management Systems (BMS) market due to concentration of electric vehicle and battery manufacturing facilities, power electronics engineering centers, and energy storage deployment projects. These states benefit from established automotive and battery supply chains, large-scale gigafactory investments, and strong collaboration between automakers and battery suppliers. Proximity to semiconductor production and advanced electronics manufacturing further reinforces regional leadership in battery monitoring system integration across electrified mobility and storage ecosystems.

Market Segmentation

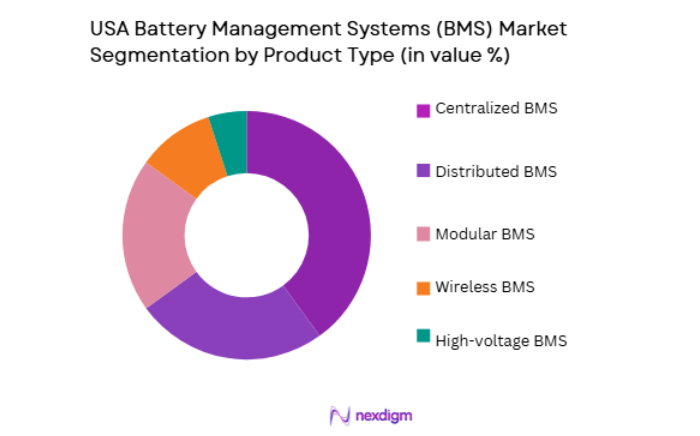

By Product Type

USA Battery Management Systems (BMS) market is segmented by product type into Centralized BMS, Distributed BMS, Modular BMS, Wireless BMS, and High-voltage BMS. Recently, Modular BMS has a dominant market share due to factors such as scalability across varying battery pack sizes, improved fault isolation capability, and compatibility with both automotive and stationary storage architectures. Modular designs enable flexible configuration across different vehicle platforms and energy storage capacities without complete system redesign, reducing engineering cost and development time for manufacturers. Automotive OEMs favor modular BMS to support platform standardization and multi-model electrification strategies. Enhanced reliability through distributed monitoring units reduces risk of full-pack failure, improving safety compliance. Battery manufacturers adopt modular architectures to simplify assembly and maintenance. As battery pack complexity and capacity increase, modular BMS offers superior manageability and expandability, reinforcing its dominant adoption across electric mobility and energy storage applications.

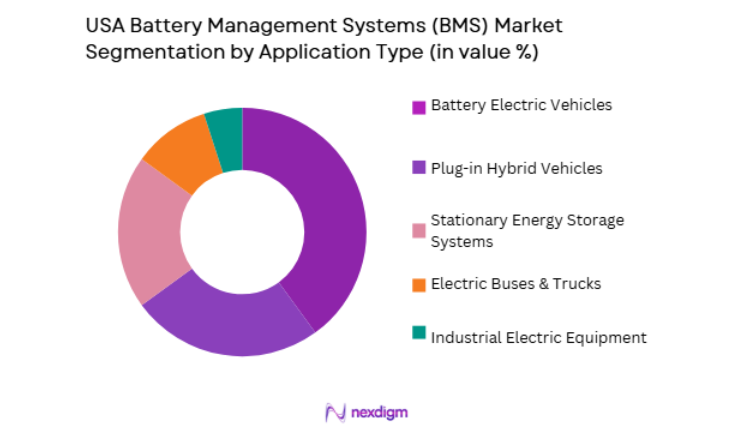

By Application

USA Battery Management Systems (BMS) market is segmented by application into Battery Electric Vehicles, Plug-in Hybrid Vehicles, Stationary Energy Storage Systems, Electric Buses & Trucks, and Industrial Electric Equipment. Recently, Battery Electric Vehicles has a dominant market share due to factors such as higher battery capacity per vehicle, rapid production growth, and stringent safety monitoring requirements in automotive electrification. Each electric vehicle requires a dedicated BMS integrated into its battery pack, generating cumulative demand proportional to EV production volumes. Automotive batteries operate under dynamic load and temperature conditions requiring advanced monitoring and balancing functionality, increasing system complexity and value. Government incentives and emissions regulations accelerate electric vehicle adoption, expanding installed BMS base. Battery manufacturers prioritize automotive BMS development due to large-scale production and safety compliance requirements. Passenger EV dominance in electrified mobility further concentrates BMS demand in this application. As EV production continues to expand faster than other electrified segments, automotive BMS remains the largest market application.

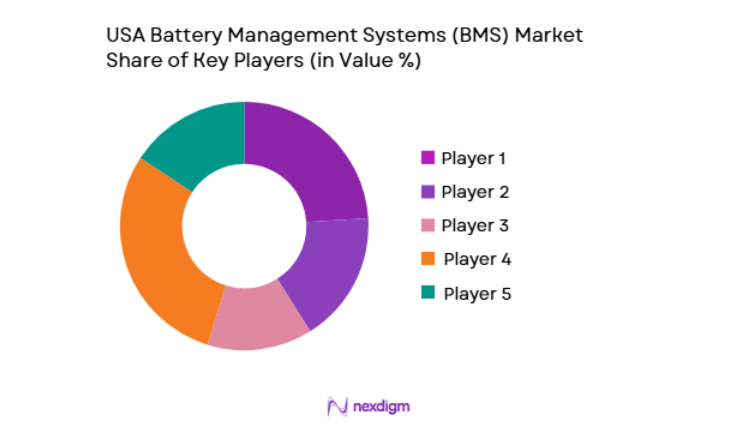

Competitive Landscape

The USA Battery Management Systems (BMS) market is moderately consolidated, led by semiconductor firms and automotive electronics suppliers providing integrated battery monitoring and control solutions to EV and energy storage manufacturers. Leading companies leverage proprietary battery algorithms, safety-certified architectures, and OEM partnerships to secure long-term supply contracts. Technology differentiation in wireless communication, cell monitoring accuracy, and functional safety compliance shapes competitive positioning, while increasing battery capacity and electrification scale drive supplier consolidation and strategic collaborations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | BMS Architecture |

| Analog Devices | 1965 | USA | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | USA | ~ | ~ | ~ | ~ | ~ |

| NXP Semiconductors | 2006 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Renesas Electronics | 2010 | Japan | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

USA Battery Management Systems Market Analysis

Growth Drivers

Rapid Expansion of Electric Vehicle Battery Capacity and Production

The rapid increase in electric vehicle battery capacity and production volumes is a primary growth driver for the USA Battery Management Systems (BMS) market, as every battery pack requires sophisticated monitoring and control electronics to ensure safety, performance, and longevity. Automotive manufacturers are deploying higher-capacity lithium-ion battery packs to extend vehicle range and support high-power propulsion, significantly increasing the complexity and value of BMS integration per vehicle. Each additional battery cell and module requires precise voltage, temperature, and current monitoring, expanding semiconductor and control circuitry content within BMS architectures. Electrification strategies across passenger cars, commercial vehicles, and buses multiply total battery pack production, directly scaling BMS demand. Gigafactory investments in domestic battery manufacturing further strengthen local supply chains for BMS electronics. Safety regulations mandate advanced battery monitoring and fault detection capability, reinforcing integration across all EV platforms. As battery energy density and voltage levels increase, BMS functionality must expand to manage thermal and electrical risks effectively. Continuous growth in EV production ensures proportional expansion of BMS deployment across the automotive sector.

Growth of Grid-scale and Distributed Energy Storage Systems

The expansion of stationary energy storage deployment across utilities, commercial facilities, and renewable energy integration projects is a major growth driver for the USA Battery Management Systems (BMS) market, as large-scale battery systems require advanced monitoring and control to operate safely and efficiently. Renewable energy generation variability necessitates battery storage to balance supply and demand, increasing installations of lithium-ion battery packs integrated with BMS. Utility-scale storage facilities contain thousands of battery cells requiring precise state-of-charge and health monitoring, driving demand for high-capacity BMS architectures. Commercial and industrial energy storage systems supporting peak shaving and backup power also rely on robust BMS solutions. Government incentives and grid modernization programs accelerate storage deployment across regions with renewable energy growth. BMS technology enables battery lifecycle optimization, safety assurance, and predictive maintenance essential for long-term storage operation. Integration of distributed storage with smart grids further increases BMS complexity and value. As energy storage adoption expands alongside renewable generation, stationary battery systems become a major parallel demand source for BMS technology.

Market Challenges

Complexity of Battery Monitoring Algorithms and Functional Safety Requirements

The increasing complexity of battery monitoring algorithms and stringent functional safety requirements represents a significant challenge for the USA Battery Management Systems (BMS) market, particularly as battery packs grow in size and voltage. Modern lithium-ion batteries require accurate estimation of state of charge, state of health, and thermal conditions under dynamic operating environments, demanding advanced algorithm development and validation. Automotive safety standards require fail-safe architectures, redundancy, and diagnostic capability, increasing design complexity and development cost. Variability in battery chemistry and cell characteristics across suppliers complicates universal BMS calibration and modeling. Real-time monitoring across hundreds of cells requires high-precision sensing and robust communication networks within battery packs. Thermal runaway prevention and fault detection algorithms must operate reliably across extreme temperatures and load conditions. Validation and certification of safety-compliant BMS systems extend development cycles. As battery technology evolves, maintaining algorithm accuracy and safety compliance remains a persistent technical challenge.

Semiconductor Supply Dependency and Cost Pressure in BMS Electronics

The USA Battery Management Systems (BMS) market faces challenges related to dependency on semiconductor components and cost pressure from automotive electrification economics. BMS architectures rely heavily on precision analog front-end ICs, microcontrollers, sensors, and communication chips, whose availability and pricing are subject to global semiconductor supply conditions. Automotive-grade semiconductor qualification requires specialized manufacturing processes and long production cycles, limiting supplier diversity. Rapid EV production growth intensifies demand for BMS chips, creating potential shortages and cost volatility. OEMs seek cost reductions in electrified powertrains, pressuring BMS suppliers to lower pricing despite rising semiconductor complexity. Supply disruptions or geopolitical trade constraints can affect electronic component availability. Increasing functional integration within BMS electronics raises development and manufacturing cost. Ensuring stable semiconductor supply and cost competitiveness remains a critical challenge for scalable BMS deployment.

Opportunities

Adoption of Wireless Battery Management Systems Architectures

The adoption of wireless battery management system architectures represents a significant opportunity for the USA Battery Management Systems (BMS) market by eliminating complex wiring harnesses and improving scalability in battery pack design. Wireless BMS replaces physical communication links between battery modules with secure wireless data transmission, reducing weight, assembly complexity, and potential failure points. Automotive manufacturers benefit from simplified battery pack assembly and modular scalability across vehicle platforms. Reduced wiring enables flexible pack configuration and easier maintenance or module replacement. Wireless communication supports advanced diagnostics and over-the-air updates for battery monitoring systems. Safety redundancy can be enhanced through distributed wireless nodes. As battery pack sizes and cell counts increase, wireless architectures become more efficient and cost-effective than traditional wired systems. Integration of wireless BMS with advanced analytics and cloud connectivity further enhances lifecycle management. Growing EV and storage deployment creates expanding demand for wireless-enabled battery monitoring solutions.

Integration of Advanced Analytics and Predictive Battery Health Management

Integration of advanced analytics and predictive battery health management capabilities offers a major opportunity for the USA Battery Management Systems (BMS) market by improving battery performance, safety, and lifecycle optimization. Modern BMS platforms increasingly incorporate machine learning and data analytics to predict battery degradation, detect anomalies, and optimize charging behavior. Predictive health monitoring reduces maintenance cost and extends battery lifespan for vehicles and energy storage systems. Fleet operators and utilities benefit from real-time battery diagnostics enabling proactive service and asset management. Automotive OEMs use predictive BMS to enhance warranty management and customer confidence. Cloud-connected BMS platforms allow continuous performance monitoring across deployed battery fleets. Integration with vehicle and energy management systems enables optimized charging and energy utilization strategies. As battery assets grow in value and scale, analytics-enabled BMS solutions provide competitive differentiation and new service-based revenue models for suppliers.

Future Outlook

The USA Battery Management Systems (BMS) market is expected to expand strongly over the next five years, driven by accelerating electric vehicle production and large-scale energy storage deployment. Advancements in wireless BMS, analytics-driven monitoring, and high-voltage battery architectures will enhance safety and performance. Regulatory requirements for battery safety and lifecycle management will reinforce adoption across mobility and grid applications. Increasing battery capacity and electrification scale will sustain long-term demand for advanced BMS technologies.

Major Players

- Analog Devices

- Texas Instruments

- NXP Semiconductors

- Renesas Electronics

- Infineon Technologies

- STMicroelectronics

- Panasonic Automotive

- LG Energy Solution

- Samsung SDI

- Sensata Technologies

- BorgWarner

- Hitachi Astemo

- Eberspächer

- AVL

- Nuvation Energy

Key Target Audience

- Automotive OEM Manufacturers

- Battery Pack Manufacturers

- Energy Storage System Integrators

- Electric Vehicle Platform Developers

- Commercial Fleet Operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial Equipment Manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key variables including EV battery capacity, cell count, BMS architecture type, semiconductor content, and storage deployment volumes were identified through government energy statistics, battery manufacturing data, and supplier financial disclosures to establish market scope and segmentation.

Step 2: Market Analysis and Construction

Market structure was constructed by mapping BMS system architectures, application segments, battery pack configurations, and supplier roles across automotive and energy storage industries. Production volumes and component revenues were synthesized to estimate market size and shares.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions and analytical models were validated through consultations with battery engineers, automotive electronics specialists, and energy storage system integrators. Expert insights refined safety requirements, architecture trends, and competitive positioning.

Step 4: Research Synthesis and Final Output

Validated datasets and expert insights were integrated into a unified analytical framework to produce segmentation, competitive landscape, and future outlook. Consistency checks ensured alignment between battery production data, supplier revenues, and technology adoption trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Electric Vehicle Production and Battery Capacity

Expansion of Stationary Energy Storage Deployment

Increasing Safety and Thermal Monitoring Requirements - Market Challenges

Complexity of Battery Monitoring and Control Algorithms

Semiconductor and Sensor Cost Pressures

Integration Challenges with High-voltage Architectures - Market Opportunities

Wireless BMS and Reduced Wiring Architectures

Second-life Battery and Storage Applications

Advanced State-of-health Analytics Integration - Trends

Adoption of AI-enabled Battery Analytics

Wireless Communication in Battery Packs

Higher Voltage EV Battery Platforms - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Centralized Battery Management Systems

Distributed Battery Management Systems

Modular Battery Management Systems

Wireless Battery Management Systems

High-voltage Battery Management Systems - By Platform Type (In Value%)

Battery Electric Passenger Vehicles

Plug-in Hybrid Vehicles

Electric Commercial Vehicles

Stationary Energy Storage Systems

Electric Buses and Trucks - By Fitment Type (In Value%)

OEM Integrated BMS

Aftermarket Retrofit BMS

Pack-level Integrated BMS

Cell-level Integrated BMS

Module-level Integrated BMS - By EndUser Segment (In Value%)

Automotive OEMs

Battery Pack Manufacturers

Energy Storage System Integrators

Commercial Fleet Operators

Electric Bus Manufacturers - By Procurement Channel (In Value%)

Direct OEM Procurement

Battery Supplier Partnerships

Tier-1 Electronics Suppliers

- Market Share Analysis

- Cross Comparison Parameters (BMS Architecture, Voltage Range Support, Cell Monitoring Accuracy, Thermal Management Integration, Wireless Capability, BMS Architecture, Voltage Range Support, Cell Monitoring Accuracy, Thermal Management Integration, Wireless Communication Capability, State of Charge Estimation Accuracy, State of Health Analytics)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Analog Devices

Texas Instruments

NXP Semiconductors

Renesas Electronics

Infineon Technologies

STMicroelectronics

Panasonic Automotive

LG Energy Solution

Samsung SDI

Denso

BorgWarner

Hitachi Astemo

Eberspächer

Lithium Balance

AVL

- Automotive OEMs demand advanced battery safety control

- Battery manufacturers integrate BMS at pack level

- Energy storage integrators require scalable BMS

- Fleet operators prioritize battery health monitoring

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now