Download PDF

Download PDFMarket Overview

The USA Battery Sensors market current size stands at around USD ~ million and reflects a rapidly evolving demand environment shaped by electrification priorities, safety mandates, and technology integration across multiple end-use systems. The market is defined by growing deployment of voltage, current, temperature, and gas sensing components within battery management systems, with procurement driven by automotive electrification, stationary energy storage safety requirements, and industrial power systems reliability needs. Adoption is influenced by regulatory compliance, functional safety standards, and long product qualification cycles.

The market is primarily concentrated in established automotive and energy storage hubs, with strong activity across California, Michigan, Texas, and emerging manufacturing corridors in the Southeast. Infrastructure maturity, domestic manufacturing incentives, and proximity to EV assembly and battery pack facilities shape demand concentration. Advanced R&D ecosystems, semiconductor fabrication presence, and integration with software-defined battery management platforms further reinforce regional clustering. Policy support for grid resilience and vehicle electrification also sustains ecosystem depth.

Market Segmentation

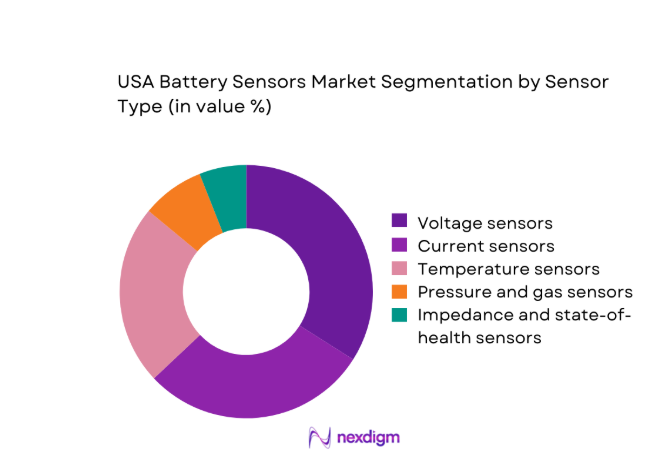

By Sensor Type

Voltage sensors and current sensors dominate the USA Battery Sensors market due to their foundational role in battery management systems across electric vehicles and stationary energy storage. Temperature sensors follow closely, driven by thermal safety requirements and regulatory compliance for lithium-ion packs. Pressure and gas sensors remain niche but are increasingly adopted in safety-critical designs for early fault detection. Impedance and state-of-health sensors are gaining traction in advanced diagnostics, enabling predictive maintenance and lifecycle optimization. Dominance is shaped by safety mandates, BMS architecture standardization, and OEM preferences for proven, automotive-grade components with long qualification histories and scalable supply availability.

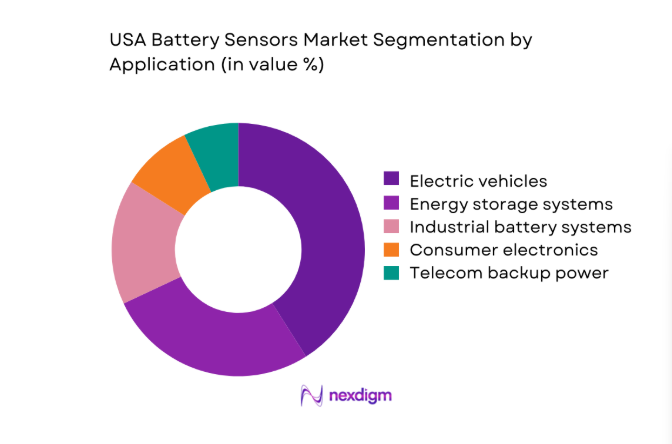

By Application

Electric vehicles represent the largest application segment due to high sensor density per battery pack and expanding domestic assembly footprints. Energy storage systems follow, supported by grid modernization and safety-driven monitoring mandates. Industrial battery systems contribute steady demand from material handling and backup power deployments. Consumer electronics show slower growth due to mature designs and cost sensitivity, while telecom backup power remains specialized with replacement-driven demand. Segment dominance is shaped by regulatory scrutiny, system criticality, and increasing adoption of advanced diagnostics in mission-critical applications requiring continuous monitoring and compliance with functional safety requirements.

Competitive Landscape

The USA Battery Sensors market is characterized by technologically advanced suppliers focused on automotive-grade reliability, functional safety compliance, and integration with battery management system architectures. Competition centers on sensor accuracy, thermal resilience, qualification depth, and the ability to support OEM validation cycles across evolving battery chemistries.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Texas Instruments | 1930 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Analog Devices | 1965 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Allegro MicroSystems | 1990 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

USA Battery Sensors Market Analysis

Growth Drivers

EV production ramp-up and domestic manufacturing incentives

Domestic EV assembly accelerated with 2022 production lines in 11 states, rising to 19 facilities by 2024, supported by federal manufacturing credits enacted in 2022. Battery pack integration expanded across 47 assembly plants in 2023, increasing sensor deployment per pack. Public charging connectors exceeded 180000 in 2024, driving safety compliance requirements within battery systems. State-level clean transportation targets adopted by 14 jurisdictions since 2023 mandate electrification in fleets. Automotive-grade electronics standards updated in 2022 require expanded sensing redundancy. Semiconductor capacity additions in Arizona and Texas between 2023 and 2025 improved localized component availability, supporting sensor supply stability and accelerated qualification cycles.

Grid-scale and behind-the-meter energy storage deployments

Utility-scale battery installations connected across 38 states by 2024, with 2022 grid resilience programs expanding interconnection queues. Grid operators approved 260 new storage interconnection requests during 2023, increasing demand for multi-parameter sensing within battery enclosures. Behind-the-meter deployments in commercial buildings expanded across 320 metropolitan areas in 2024, driven by resilience planning following 2022 extreme weather events recorded in 18 states. Interagency grid modernization initiatives launched in 2023 emphasized continuous monitoring standards. Fire safety codes updated in 2022 require thermal and gas detection layers in battery rooms. State energy offices issued 2024 technical guidelines reinforcing sensor redundancy within stationary storage systems.

Challenges

Cost pressure from automotive OEMs on sensor BOM

Automotive OEM sourcing cycles in 2023 consolidated sensor suppliers from 9 to 5 approved vendors across several platforms, intensifying price negotiations. Vehicle program budgets approved in 2022 imposed electronics cost ceilings across 14 major platforms, constraining component margins. Localization mandates tied to 2023 manufacturing incentives required dual sourcing in 7 states, increasing compliance overhead. Component qualification cycles average 24 months, delaying design wins amid 2024 model refreshes. Supply chain audits introduced in 2023 by federal procurement offices increased documentation requirements. Engineering change orders averaged 6 per platform during 2024, increasing nonrecurring validation burden without corresponding volume commitments.

Design complexity and integration with BMS firmware

Battery management firmware updates increased in frequency from 2022 to 2024, with 5 major revisions released across dominant automotive platforms in 2024. Sensor interface protocols expanded to include 3 new digital buses adopted in 2023, complicating integration testing. Functional safety audits conducted in 2022 require traceability across 21 documentation checkpoints. Validation cycles require 180 day environmental testing under revised 2024 safety standards. Interoperability testing expanded across 12 battery chemistries evaluated in 2023 programs. Engineering teams face staffing gaps reported by 9 state workforce agencies in 2024, slowing firmware-sensor co-development and prolonging qualification timelines across new battery platforms.

Opportunities

Solid-state battery development creating new sensing needs

Federal research programs funded 2022 solid-state pilot lines across 6 national laboratories, with 2023 demonstration cells tested in 4 automotive consortia. Solid-state architectures require monitoring across 3 additional parameters compared to liquid electrolyte systems, increasing sensing complexity. Prototype pack testing expanded in 2024 to 27 validation sites nationwide. Safety guidelines drafted in 2023 introduce new thermal interface monitoring requirements. University-industry partnerships established in 2022 across 12 states support accelerated materials testing. Manufacturing equipment upgrades planned for 2025 include in-line diagnostics integration. These developments create demand for novel sensing modalities compatible with solid electrolytes and high-voltage stack configurations.

Advanced diagnostics for predictive maintenance in BESS

Grid operators expanded predictive maintenance programs across 2023 to 2024 following 2022 outage assessments in 9 regions. Condition monitoring frameworks adopted by 6 regional transmission organizations require continuous sensor data streams. Asset management platforms integrated anomaly detection modules in 2024 across 140 utility control centers. Fire safety inspections mandated in 2022 increased demand for early fault indicators within battery enclosures. Workforce training programs launched in 2023 across 18 states emphasize data-driven maintenance workflows. Interoperability standards published in 2024 facilitate sensor data integration into supervisory control systems. These shifts enable sensor-enabled diagnostics to reduce downtime and improve compliance across stationary storage deployments.

Future Outlook

Future market development will be shaped by ongoing electrification policies, domestic manufacturing expansion, and evolving safety standards across mobility and grid storage. Integration of advanced diagnostics into battery management architectures will deepen sensor requirements. As solid-state and high-voltage platforms mature, sensor innovation will increasingly align with functional safety and digital integration priorities through 2030.

Major Players

- Texas Instruments

- Analog Devices

- Infineon Technologies

- STMicroelectronics

- Allegro MicroSystems

- TE Connectivity

- Honeywell

- Sensata Technologies

- TDK Corporation

- Murata Manufacturing

- ams OSRAM

- Littelfuse

- NXP Semiconductors

- ON Semiconductor

- Panasonic

Key Target Audience

- Electric vehicle OEMs and battery pack manufacturers

- Energy storage system integrators and EPC contractors

- Automotive Tier-1 battery management system suppliers

- Utility companies and grid operators

- Industrial equipment and material handling OEMs

- Investments and venture capital firms

- U.S. Department of Energy and National Highway Traffic Safety Administration

- State energy offices and fire safety regulatory agencies

Research Methodology

Step 1: Identification of Key Variables

Key performance parameters were mapped across voltage, current, thermal, and gas sensing needs within battery systems. Application-specific operating conditions were identified across mobility and stationary storage environments. Regulatory compliance variables and functional safety thresholds were defined. Channel dynamics and qualification pathways were outlined.

Step 2: Market Analysis and Construction

Demand drivers were structured around electrification programs, grid resilience initiatives, and domestic manufacturing policies. Application-specific deployment pathways were analyzed across vehicle platforms and storage installations. Technology evolution and integration complexity were assessed. Supply chain localization dynamics were incorporated into market construction logic.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on adoption pathways were validated through structured discussions with system integrators, battery engineers, and compliance specialists. Technology readiness assumptions were stress-tested against evolving safety codes. Integration challenges were reviewed through platform-level implementation scenarios. Regulatory alignment hypotheses were refined through policy interpretation exercises.

Step 4: Research Synthesis and Final Output

Findings were synthesized into a cohesive market narrative reflecting technology, policy, and deployment realities. Cross-segment insights were consolidated to highlight convergence trends. Risk factors and opportunity pathways were triangulated across applications. The final output integrates ecosystem dynamics with forward-looking adoption considerations.

- Executive Summary

- Research Methodology (Market Definitions and application boundaries for battery sensors, OEM and Tier-1 supplier interviews across EV and BESS programs, shipment tracking of current and voltage sensing components, teardown and BOM analysis of battery management systems, regulatory and safety standard mapping for UL and SAE, pricing and ASP benchmarking across sensor technologies)

- Definition and Scope

- Market evolution

- Usage and integration pathways within BMS architectures

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

EV production ramp-up and domestic manufacturing incentives

Grid-scale and behind-the-meter energy storage deployments

Stricter safety requirements for thermal runaway prevention

Rising adoption of advanced BMS architectures in automotive

Electrification of industrial equipment and material handling

Performance optimization needs for fast charging - Challenges

Cost pressure from automotive OEMs on sensor BOM

Design complexity and integration with BMS firmware

Supply chain volatility for semiconductor components

Accuracy drift and calibration requirements over battery life

Qualification cycles and automotive-grade reliability standards

Interoperability across diverse battery chemistries - Opportunities

Solid-state battery development creating new sensing needs

Advanced diagnostics for predictive maintenance in BESS

High-voltage platform migration in EV architectures

Localization of sensor manufacturing under reshoring initiatives

Integration of multi-parameter sensor modules

Growth in second-life battery monitoring solutions - Trends

Adoption of contactless current sensing for high-voltage systems

Integration of sensor data into AI-driven BMS algorithms

Miniaturization and higher temperature tolerance components

Cybersecure sensor interfaces within connected vehicles

Move toward redundant sensing for functional safety

Increased use of digital output sensors - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Sensor Type (in Value %)

Voltage sensors

Current sensors

Temperature sensors

Pressure and gas sensors

Impedance and state-of-health sensors - By Technology (in Value %)

Hall-effect sensors

Shunt-based sensors

Fiber optic sensors

MEMS-based sensors

NTC/PTC thermistors - By Application (in Value %)

Electric vehicles and hybrids

Energy storage systems (BESS)

Consumer electronics

Industrial battery systems

Telecom backup power - By Battery Chemistry (in Value %)

Lithium-ion

Lithium iron phosphate

Nickel metal hydride

Lead-acid

Solid-state batteries - By Sales Channel (in Value %)

Direct OEM supply

Tier-1 BMS integrators

Distributors and catalog sales

Aftermarket and service replacements

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (sensor accuracy, operating voltage range, temperature tolerance, functional safety compliance, integration with BMS ICs, manufacturing footprint in the USA, pricing tiers, customization capability)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Texas Instruments

Analog Devices

Infineon Technologies

STMicroelectronics

Allegro MicroSystems

TE Connectivity

Honeywell

Sensata Technologies

TDK Corporation

Murata Manufacturing

ams OSRAM

Littelfuse

NXP Semiconductors

ON Semiconductor

Panasonic

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now