Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Blind Spot Detection Systems market is valued at USD ~ billion based on a recent historical assessment supported by automotive safety component disclosures and National Highway Traffic Safety Administration reporting. Growth is driven by rising integration of advanced driver assistance systems across passenger vehicles and light trucks, increasing safety awareness among consumers, and OEM standardization of radar-based monitoring systems. Expanding electric vehicle production and fleet modernization programs further accelerate demand for sensor-based side detection technologies.

The United States leads this market, with dominant activity concentrated in Michigan, Ohio, California, and Texas due to strong automotive manufacturing ecosystems and advanced mobility technology hubs. Detroit remains central because of established OEM headquarters and supplier networks, while Silicon Valley drives innovation in sensor fusion and software integration. High vehicle ownership levels and regulatory safety oversight contribute to widespread deployment of blind spot detection systems across both private and commercial vehicle segments.

Market Segmentation

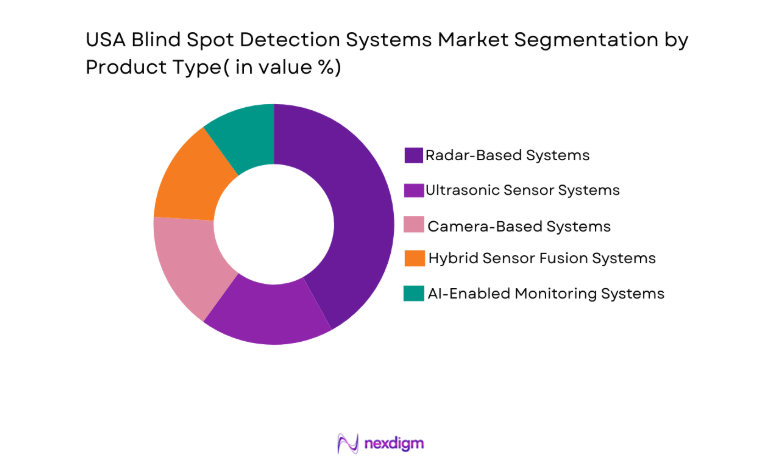

By Product Type

USA Blind Spot Detection Systems market is segmented by product type into Radar-Based Systems, Ultrasonic Sensor Systems, Camera-Based Systems, Hybrid Sensor Fusion Systems, and AI-Enabled Monitoring Systems. Recently, Radar-Based Systems have a dominant market share due to superior detection range, high reliability in adverse weather conditions, and strong OEM integration across mid-range and premium vehicle platforms. Automotive manufacturers prefer radar modules because they deliver consistent side-object tracking performance at highway speeds, which enhances lane-change safety and regulatory compliance. Continuous advancements in millimeter-wave radar technology and semiconductor optimization further strengthen their competitive positioning across both passenger and commercial vehicle applications.

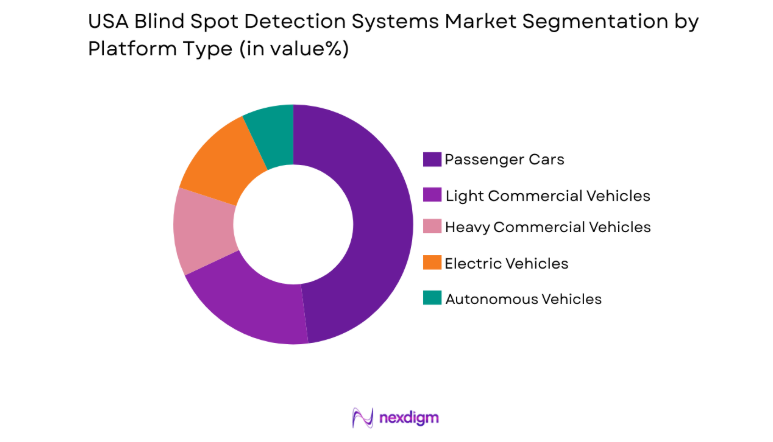

By Platform Type

USA Blind Spot Detection Systems market is segmented by platform type into Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, and Autonomous Vehicles. Passenger Cars dominate the market due to large-scale production, widespread integration of advanced driver assistance systems, and strong consumer preference for enhanced safety features. SUVs and crossover vehicles significantly contribute to installations because of larger blind zones. Commercial fleets are increasingly adopting these systems to reduce accident liability, while electric and autonomous platforms integrate blind spot detection within advanced sensor fusion architectures.

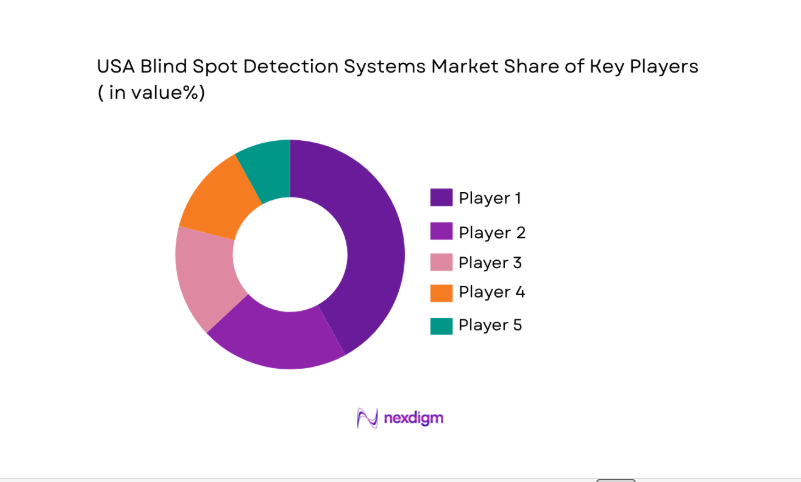

Competitive Landscape

The USA Blind Spot Detection Systems market is moderately consolidated, with automotive suppliers and semiconductor manufacturers holding strong influence over innovation and supply chains. Established global players dominate OEM partnerships, while specialized sensor and software firms compete through technological differentiation and AI-enabled capabilities. Strategic collaborations, long-term supply agreements, and continuous R&D investment define competitive positioning in this safety-focused market.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Partnerships |

| Bosch Mobility Solutions | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

USA Blind Spot Detection Systems Market Analysis

Growth Drivers

Regulatory Expansion of Advanced Driver Assistance Systems Requirements

The significantly accelerate adoption of blind spot detection technologies across the United States automotive sector. Federal Motor Vehicle Safety Standards and consumer safety assessment programs increasingly emphasize collision avoidance and side-impact mitigation systems, which incentivizes manufacturers to integrate blind spot monitoring as either standard or optional equipment across vehicle portfolios. Insurance providers also reward vehicles equipped with advanced safety features, encouraging consumers to prioritize models offering integrated radar-based detection capabilities. As regulatory bodies intensify scrutiny on lane-change accidents and side-impact collisions, automakers respond by expanding deployment even within entry-level trims. Growing alignment between safety advocacy groups and federal agencies further strengthens compliance momentum across domestic and imported vehicles. Additionally, state-level road safety campaigns promote awareness of blind zone hazards, indirectly stimulating aftermarket upgrades. Technological standardization across Tier-1 suppliers reduces integration complexity, enabling broader deployment without extensive redesign. This evolving regulatory ecosystem sustains continuous growth in sensor installations and software upgrades throughout passenger and commercial vehicle segments.

Rising Consumer Demand for Enhanced Vehicle Safety and Driver Assistance Technologies

Plays a pivotal role in expanding the USA Blind Spot Detection Systems market. Buyers increasingly evaluate vehicles based on safety ratings and embedded ADAS capabilities, making blind spot monitoring a decisive purchasing factor in competitive segments such as SUVs and crossovers. Urban traffic congestion and multi-lane highway usage heighten awareness of blind zone risks, reinforcing preference for radar-enabled monitoring systems. Automakers capitalize on this trend by bundling blind spot detection within comprehensive driver assistance packages that include lane departure warnings and cross-traffic alerts. Growing familiarity with semi-autonomous features also elevates expectations for real-time hazard detection. Digital dashboards and advanced infotainment systems seamlessly integrate blind spot alerts, improving user experience and reinforcing adoption. The rapid growth of electric vehicles further contributes, as EV manufacturers position advanced safety systems as standard components. Continuous marketing emphasizing proactive accident prevention strengthens long-term consumer confidence and sustained demand.

Market Challenges

High System Integration Costs in Entry-Level Vehicle Segments

present a substantial challenge for manufacturers seeking widespread deployment of blind spot detection technologies. Incorporating radar modules, control units, and software calibration into lower-priced vehicles increases production expenses and can compress profit margins in cost-sensitive categories. Semiconductor supply volatility and raw material price fluctuations further amplify cost pressures, limiting affordability for mass-market consumers. Smaller OEMs may struggle to absorb these integration costs without raising retail prices, potentially slowing penetration rates. Calibration complexity during assembly adds labor and testing requirements, increasing operational overhead. Aftermarket solutions offer alternatives but often lack seamless integration compared to factory-installed systems. Competitive pricing strategies among global suppliers also create margin constraints within Tier-1 partnerships. These financial and logistical barriers can delay universal standardization across all vehicle classes.

Sensor Performance Limitations in Adverse Weather and Complex Traffic Conditions

create operational reliability concerns within the USA Blind Spot Detection Systems market. Heavy rain, snow accumulation, and road debris can interfere with radar and camera accuracy, leading to false alerts or temporary detection loss. Urban environments with dense vehicle clustering and reflective surfaces may also reduce signal clarity. Drivers experiencing inconsistent system performance may question reliability, potentially affecting consumer confidence. Continuous software updates and hardware refinement require sustained R&D investment from suppliers. Integration with other ADAS modules adds system interdependency, increasing diagnostic complexity. Regulatory scrutiny over malfunction incidents may impose stricter validation requirements. Addressing these technical constraints demands ongoing innovation to ensure consistent safety outcomes across varied driving environments.

Opportunities

Expansion of Blind Spot Detection Integration in Electric and Connected Vehicle Platforms

Platforms present a major growth opportunity for manufacturers and technology providers. Electric vehicles increasingly incorporate advanced electronic architectures capable of supporting sensor fusion and AI-driven analytics, enabling seamless blind zone monitoring integration. EV manufacturers emphasize safety innovation to differentiate products in competitive markets, often including blind spot detection as a standard feature. Connected vehicle ecosystems allow real-time data exchange, improving predictive object tracking and system responsiveness. Integration with over-the-air update capabilities ensures continuous performance enhancement. Rising EV production volumes across US assembly plants amplify installation rates. Fleet electrification initiatives further extend deployment within logistics and urban mobility sectors. These combined factors create scalable expansion potential for advanced detection systems.

Integration with Autonomous Driving and Advanced Mobility Ecosystems

provides transformative potential for blind spot detection systems in the United States automotive industry. As semi-autonomous features become more prevalent, blind spot monitoring evolves into a core component of comprehensive situational awareness architectures. Sensor fusion combining radar, camera, and AI analytics enhances object classification accuracy during lane changes. Autonomous vehicle developers prioritize redundant sensing systems, increasing demand for high-precision blind zone modules. Smart city infrastructure initiatives further encourage vehicle-to-infrastructure data interaction, strengthening safety coordination. Collaboration between semiconductor manufacturers and software developers accelerates innovation cycles. Investment in next-generation automotive computing platforms enables advanced real-time hazard prediction. This integration trajectory positions blind spot detection systems as foundational elements within future mobility frameworks.

Future Outlook

Over the next five years, the USA Blind Spot Detection Systems market is expected to witness sustained expansion driven by regulatory support, technological innovation, and increasing vehicle electrification. Advancements in AI-enabled sensor fusion and improved radar accuracy will enhance detection reliability. OEM standardization across mid-range vehicle trims will broaden adoption. Growing fleet modernization and autonomous mobility development will further strengthen long-term demand for advanced blind zone monitoring technologies.

Major Players

- Bosch Mobility Solutions

- Continental AG

- AptivPLC

- ZF Friedrichshafen AG

- Magna International Inc.

- Denso Corporation

- Valeo SA • Autoliv Inc.

- Texas Instruments Automotive

- Infineon Technologies

- NXP Semiconductors

- Mobileye Global Inc

- Hella GmbH

- Panasonic Automotive Systems

- Gentex Corporation

Key Target Audience

- Automotive OEMs

- Automotive Suppliers

- Electric Vehicle Manufacturers

- Commercial Fleet Operators

- Insurance Companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Component Distributors

Research Methodology

Step 1: Identification of Key Variables

Key technological, regulatory, and demand-side variables influencing the USA Blind Spot Detection Systems market were identified through analysis of safety standards, OEM adoption rates, and semiconductor supply trends. Data points included installation volumes, pricing tiers, and integration levels across vehicle categories.

Step 2: Market Analysis and Construction

Market size was constructed using automotive production statistics, ADAS penetration rates, and supplier revenue disclosures. Cross-validation was performed using industry databases and regulatory publications to ensure accuracy and reliability.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from automotive OEMs, Tier-1 suppliers, and safety compliance agencies were consulted to validate adoption trends and technology evolution assumptions. Feedback was incorporated to refine growth projections and structural assessments.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured framework covering segmentation, competitive positioning, and market dynamics. Final validation ensured consistency across data models, regulatory references, and demand-side interpretations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising regulatory mandates for vehicle safety compliance

Increasing penetration of advanced driver assistance systems in mid-range vehicles

Growth in SUV and pickup truck sales requiring enhanced side monitoring

Technological advancements in radar miniaturization and sensor fusion

Insurance incentives promoting collision avoidance technologies - Market Challenges

High integration costs in entry-level vehicle segments

Calibration and maintenance complexity in aftermarket installations

False alert issues under adverse weather conditions

Supply chain disruptions affecting semiconductor availability

Cybersecurity risks in connected vehicle architectures - Market Opportunities

Expansion of blind spot detection in electric vehicle platforms

Integration with autonomous driving ecosystems

Growth in commercial fleet safety modernization programs - Trends

Adoption of AI-driven object recognition algorithms

Integration with lane change assist and cross-traffic alert systems

Standardization of blind spot detection in mid-tier vehicle trims

Development of 360-degree surround sensing systems

Increased collaboration between OEMs and semiconductor manufacturers - Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standards influencing ADAS integration

NHTSA safety assessment programs encouraging collision avoidance systems

State-level initiatives promoting advanced vehicle safety technologies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Radar-Based Blind Spot Detection Systems

Ultrasonic Sensor-Based Systems

Camera-Based Monitoring Systems

Hybrid Sensor Fusion Systems

AI-Enabled Predictive Blind Spot Systems - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Autonomous and Semi-Autonomous Vehicles - By Fitment Type (In Value%)

OEM Factory-Installed Systems

Dealer-Installed Systems

Aftermarket Retrofit Kits

Integrated ADAS Packages

Fleet Custom Installations - By EndUser Segment (In Value%)

Private Vehicle Owners

Commercial Fleet Operators

Ride-Hailing Service Providers

Logistics and Delivery Companies

Government and Municipal Fleets - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier-1 Supplier Agreements

Aftermarket Distributors

Online Automotive Retail Platforms

Fleet Procurement Programs - By Material / Technology (in Value %)

Millimeter Wave Radar Modules

CMOS Camera Sensors

Ultrasonic Transducers

Embedded Control Units

Sensor Fusion Software Platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Sensor Accuracy, Detection Range, Integration Capability, System Cost, Software Intelligence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bosch Mobility Solutions

Continental AG

Aptiv PLC

ZF Friedrichshafen AG

Magna International Inc.

Denso Corporation

Valeo SA

Autoliv Inc.

Texas Instruments Automotive

Infineon Technologies

NXP Semiconductors

Mobileye Global Inc.

Hella GmbH

Panasonic Automotive Systems

Gentex Corporation

- Private vehicle owners prioritize safety and insurance benefits

- Fleet operators focus on accident reduction and liability control

- Ride-hailing providers emphasize passenger safety compliance

- Government fleets adopt systems to meet public safety standards

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now