Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Body Panels market current size stands at around USD ~ million, reflecting robust demand across original equipment manufacturing and replacement channels driven by vehicle parc expansion and repair intensity. The market is characterized by diversified material adoption, including steel, aluminum, and advanced composites, supported by localized stamping capacity and integration with body-in-white architectures. Supply networks span Tier 1 component manufacturers, tool and die specialists, and downstream service parts distribution, with quality, fitment precision, and logistics reliability shaping procurement decisions across OEM and aftermarket ecosystems.

Dominant activity clusters around automotive manufacturing and repair hubs in the Midwest and Southeast, supported by dense supplier networks, logistics corridors, and skilled labor pools. Coastal port regions reinforce import of aluminum sheet and specialty resins, while proximity to assembly plants accelerates just-in-time delivery. Urban collision repair concentrations elevate replacement demand, and state-level policy emphasis on lightweighting and emissions compliance strengthens adoption of advanced materials. Mature testing infrastructure, recycling partnerships, and industrial automation investments further reinforce regional leadership and supply resilience.

Market Segmentation

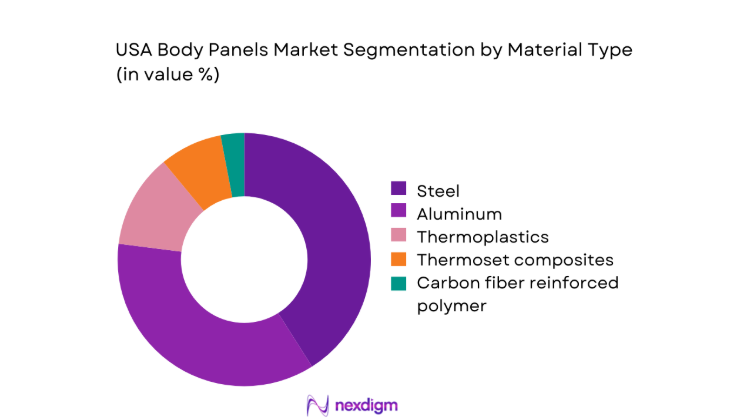

By Material Type

Aluminum-led closures and mixed-material architectures dominate demand as OEMs pursue lightweighting for fuel efficiency and EV range, while advanced high-strength steels remain integral for structural integrity. Thermoplastics and thermoset composites expand in exterior modules where corrosion resistance and design flexibility matter, particularly for fascia and tailgates. Carbon fiber use remains selective due to manufacturing complexity, but its application in performance variants supports premium positioning. Recycling loops and closed-loop aluminum sourcing improve material security, and localized sheet supply strengthens lead-time reliability. Process capability, repairability, and compatibility with joining technologies increasingly shape material choice across OEM and service channels.

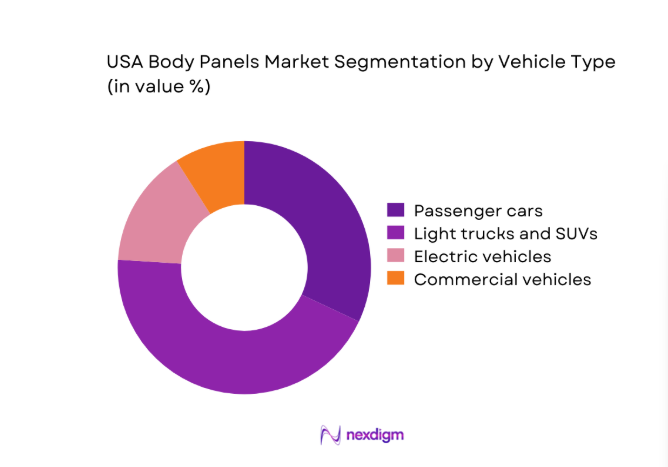

By Vehicle Type

Light trucks and SUVs lead panel demand due to higher production volumes, larger surface area per vehicle, and frequent redesign cycles. Passenger cars retain stable replacement flows through urban collision repair networks. Electric vehicles accelerate adoption of aluminum closures to offset battery mass, while commercial vehicles sustain steady replacement demand tied to fleet utilization intensity. Platform refreshes and safety updates increase tooling cadence across segments. Regional assembly proximity drives sourcing decisions, and modular front-end assemblies streamline logistics. Repair complexity for advanced materials influences aftermarket channel preferences, reinforcing certified network growth in urban and highway corridors.

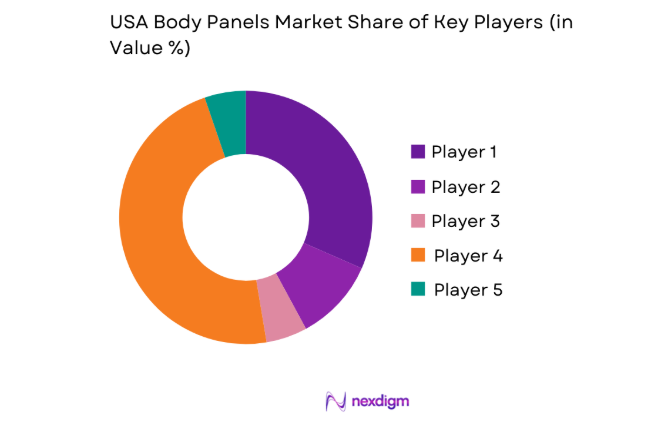

Competitive Landscape

Competition is shaped by vertically integrated stamping capabilities, tooling depth, and proximity to OEM assembly footprints. Suppliers differentiate through mixed-material forming, automation, and quality systems that reduce launch risk and improve first-time-right rates. Long-term program awards anchor capacity planning, while aftermarket channels value fitment accuracy and rapid fulfillment. Regulatory readiness around safety and sustainability compliance strengthens preferred supplier status across OEM and service networks.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ | ~ |

| Gestamp | 1997 | Spain | ~ | ~ | ~ | ~ | ~ | ~ |

| Martinrea International | 1986 | Canada | ~ | ~ | ~ | ~ | ~ | ~ |

| Tower International | 1993 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Flex-N-Gate | 1956 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

USA Body Panels Market Analysis

Growth Drivers

Lightweighting mandates to improve fuel economy and EV range

Federal efficiency standards and emissions frameworks intensified between 2022 and 2025, encouraging aluminum and advanced steel adoption in closures and exterior modules. EV programs expanded charging corridors by 2024, supporting broader electrification, while battery pack weights above 450 kilograms drove OEMs to offset mass through lighter hoods and doors. Aluminum sheet capacity additions in the Midwest improved availability. Recycling loops expanded collection rates at 14 facilities, strengthening closed-loop supply. Highway safety requirements increased pedestrian protection features, integrating energy-absorbing panel designs. Manufacturing automation rose with 38 robotic cells commissioned across stamping lines, improving throughput and dimensional consistency nationally.

Rising SUV and light truck production volumes

Assembly plants across the Southeast and Midwest expanded shifts during 2023 and 2024, lifting light truck and SUV build schedules amid strong consumer preference. Highway freight volumes exceeded 2022 baselines, reinforcing logistics demand for larger body panels. New model launches added wider hoods and liftgates, increasing material intensity per vehicle. Dealer inventories normalized in 2024 following constrained supply in 2022, supporting steadier replacement flows. Collision severity trends increased average panel replacements per incident. State infrastructure investments upgraded interstates across 12 corridors, shortening transit times for stamped components and improving just-in-time reliability for nearby assembly clusters.

Challenges

High tooling and die investment for new panel programs

Program launches between 2022 and 2025 required multiple die sets per panel variant, increasing capital intensity and elongating break-even timelines. Tooling lead times averaged 28 weeks, compressing validation windows for model-year changes. Die steel supply volatility disrupted maintenance cycles, raising downtime risk. Plant retrofits for mixed-material forming required specialized presses and joining cells, complicating scheduling. Workforce shortages across machining trades constrained die tryout capacity. Environmental permitting for new press installations extended approval cycles in several states, slowing capacity additions and limiting rapid response to platform refreshes and late-stage design changes nationwide.

Volatility in steel and aluminum input prices

Commodity fluctuations during 2022 to 2025 destabilized procurement planning and contract pass-through mechanisms. Import dependency for specialty aluminum sheet exposed mills to shipping disruptions at two major ports, elongating replenishment cycles. Inventory buffering increased floor space utilization and working capital strain. Hedging practices varied across suppliers, creating uneven exposure. Alloy qualification delays constrained substitution options when primary grades tightened. Energy price swings affected rolling mill output stability, creating batch variability that complicated surface finish consistency for visible panels, elevating rework rates and increasing scrap management burdens across stamping operations nationwide.

Opportunities

Expansion of aluminum and mixed-material body structures

EV platform rollouts from 2023 to 2025 accelerated adoption of aluminum closures to offset battery mass exceeding 480 kilograms. Federal corridor electrification initiatives increased utilization of lightweight designs to extend range in mixed driving cycles. New joining methods validated peel and clinch strength across 6 test programs, enabling mixed-material assemblies at scale. Recycling partnerships expanded closed-loop feedstock collection at 9 regional hubs, improving supply security. Press upgrades for hot forming enabled higher-strength aluminum grades. Design-for-repair guidelines reduced insurance friction, supporting broader aftermarket acceptance and faster replacement cycles for aluminum-intensive panels nationwide.

Aftermarket replacement growth for high-turn panels

Urban collision frequencies increased across 2023 and 2024, driving replacement demand for doors, fenders, and hoods with shorter fulfillment windows. Insurer-approved repair networks expanded to 21 metropolitan areas, standardizing fitment tolerances and quality protocols. Digital parts catalogs integrated VIN-level panel matching, reducing mis-shipments and returns. Regional distribution centers optimized last-mile delivery within 24-hour service radii. Technician certification programs scaled to 1,400 new trainees, improving aluminum repair capability. Fleet utilization in commercial corridors sustained wear-related replacements, reinforcing stable aftermarket throughput across logistics-intensive regions.

Future Outlook

Through 2030, the market will advance with platform refresh cycles, rising electrification, and deeper mixed-material integration across closures and exterior modules. Policy continuity around efficiency and safety will sustain lightweighting adoption, while automation and digital tooling compress launch timelines. Regional supply chains will tighten through localized aluminum sheet sourcing and recycling partnerships, improving resilience. Aftermarket networks will professionalize aluminum repair capabilities, supporting replacement throughput. Collaboration across OEMs, Tier 1s, and recyclers will shape durable, compliant body panel ecosystems.

Major Players

- Magna International

- Gestamp

- Martinrea International

- Tower International

- Flex-N-Gate

- Kirchhoff Automotive

- Benteler International

- Shape Corp

- Aisin Corporation

- Dura Automotive Systems

- Norsk Hydro Automotive Structures

- Novelis Automotive

- Thyssenkrupp Automotive Technology

- Autoneum

- American Axle & Manufacturing

Key Target Audience

- OEM procurement and vehicle platform sourcing teams

- Tier 1 body-in-white and exterior module suppliers

- Automotive stamping and tooling manufacturers

- Authorized service parts distributors and networks

- Collision repair chains and certified repair networks

- Fleet operators and commercial vehicle maintenance managers

- Investments and venture capital firms

- Government and regulatory bodies with agency names

Research Methodology

Step 1: Identification of Key Variables

Material mix, panel type demand, vehicle production mix, repairability constraints, and regulatory compliance factors were scoped. Manufacturing process capabilities and regional capacity footprints were mapped. Logistics reliability and recycling loop maturity were included to capture supply resilience.

Step 2: Market Analysis and Construction

Program-level mapping aligned OEM platform cycles with stamping capacity and material transitions. Channel flows across OEM, service parts, and collision repair were structured. Process readiness across hot forming, mixed-material joining, and surface finishing informed capability benchmarking.

Step 3: Hypothesis Validation and Expert Consultation

Manufacturing engineers, tooling specialists, and repair network leads validated process constraints and adoption pathways. Policy experts assessed compliance trajectories for efficiency and safety standards. Recycling operators confirmed closed-loop feasibility across regions.

Step 4: Research Synthesis and Final Output

Insights were synthesized into demand drivers, constraints, and opportunity pathways aligned to platform refresh cycles. Cross-functional linkages across OEMs, Tier 1s, and aftermarket channels informed ecosystem readiness. Findings were consolidated into actionable strategic perspectives.

- Executive Summary

- Research Methodology (Market Definitions and body panel scope across OEM and aftermarket, Primary interviews with Tier 1 suppliers and stamping operations, OEM procurement and teardown analysis of model-year platforms, Import-export and tariff impact assessment on panels and stampings, Production capacity mapping of steel and aluminum stamping plants, Dealer and collision repair channel surveys on replacement demand, Teardown-based material cost benchmarking)

- Definition and Scope

- Market evolution

- Usage and replacement pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Lightweighting mandates to improve fuel economy and EV range

Rising SUV and light truck production volumes

Increasing adoption of aluminum closures by OEMs

Growth in collision repair demand due to higher vehicle parc

Platform refresh cycles and model-year redesigns

Localization of stamping capacity under USMCA - Challenges

High tooling and die investment for new panel programs

Volatility in steel and aluminum input prices

Supply chain disruptions for resins and aluminum sheet

Fitment complexity and higher repair costs for advanced materials

OEM pricing pressure on Tier 1 panel suppliers

Tariff exposure on imported stampings and blanks - Opportunities

Expansion of aluminum and mixed-material body structures

Aftermarket replacement growth for high-turn panels

Localization of EV body panel programs in the US

Adoption of hot stamping and tailored blanks

Recycling and closed-loop aluminum sourcing partnerships

Digital die simulation and virtual tryout adoption - Trends

Shift from steel to aluminum for hoods, doors, and closures

Increased use of tailor-welded and tailor-rolled blanks

Integration of sensor mounts and aerodynamic features in panels

Growth of modular front-end and closure assemblies

Use of high-strength steels for crash management zones

Automation and robotics in stamping and finishing lines - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Material Type (in Value %)

Steel

Aluminum

Thermoplastics

Thermoset composites

Carbon fiber reinforced polymer - By Vehicle Type (in Value %)

Passenger cars

Light trucks and SUVs

Electric vehicles

Commercial vehicles - By Panel Type (in Value %)

Hood

Fenders

Doors

Roof

Quarter panels

Tailgates and liftgates - By Manufacturing Process (in Value %)

Stamping

Injection molding

Compression molding

Resin transfer molding

Sheet molding compound - By Sales Channel (in Value %)

OEM supply

Authorized service parts

Independent aftermarket

Collision repair networks

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (material portfolio breadth, OEM program coverage, stamping tonnage capacity, aluminum forming capability, geographic plant footprint in the US, tooling and die design capability, cost competitiveness, quality and defect rates)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Magna International

Gestamp

Martinrea International

Tower International

American Axle & Manufacturing

Benteler International

Kirchhoff Automotive

Flex-N-Gate

Thyssenkrupp Automotive Technology

Aisin Corporation

Dura Automotive Systems

Norsk Hydro Automotive Structures

Novelis Automotive

Shape Corp

Autoneum

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now