Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Car Carpets and Floor Mats market is valued at approximately USD ~ billion based on a recent historical assessment, supported by data from automotive interior component shipments and aftermarket accessory sales reported by the Automotive Aftermarket Suppliers Association and US vehicle production statistics from federal transportation agencies. Demand is driven by sustained vehicle parc expansion exceeding 290 million registered vehicles and rising consumer spending on interior protection, comfort enhancement, and customization products across passenger and light truck segments.

Within the USA Car Carpets and Floor Mats market, dominant demand concentration is observed across major automotive production and vehicle ownership hubs including Michigan, Ohio, Texas, and California due to dense OEM manufacturing clusters, large vehicle fleets, and high aftermarket consumption. These regions benefit from established automotive supply chains, harsh seasonal weather requiring protective floor solutions, and strong retail accessory networks, reinforcing sustained purchasing cycles among consumers, fleet operators, and vehicle dealerships.

Market Segmentation

By Product Type

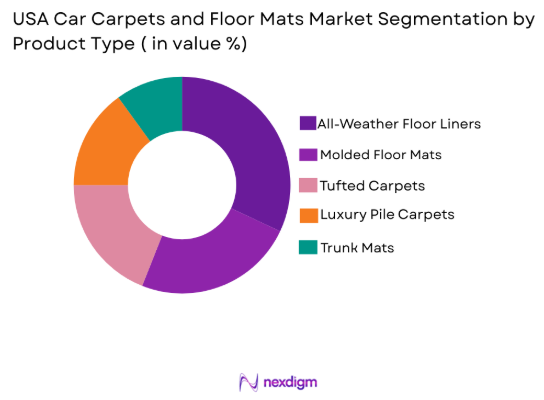

USA Car Carpets and Floor Mats market is segmented by product type into tufted carpets, molded floor mats, all-weather floor liners, luxury pile carpets, and trunk mats. Recently, all-weather floor liners has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Consumers increasingly prioritize durability, easy cleaning, and year-round protection against mud, snow, and spills, particularly in regions with extreme weather. OEMs and aftermarket brands have expanded custom-fit liner offerings supported by digital vehicle scanning technologies and strong e-commerce distribution. Fleet operators and ride-sharing vehicles also favor liners for lower maintenance costs and longer service life, accelerating adoption across both new vehicle fitment and replacement demand cycles nationwide.

By Platform Type

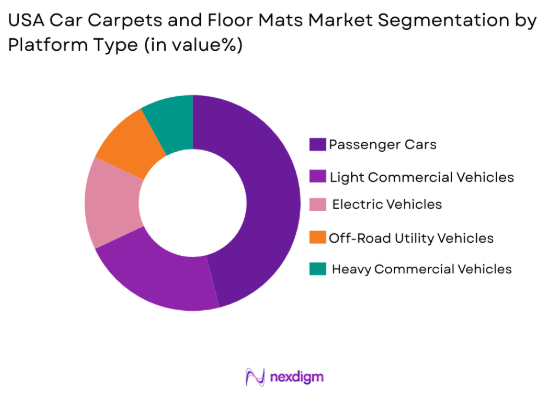

USA Car Carpets and Floor Mats market is segmented by platform type into passenger cars, light commercial vehicles, heavy commercial vehicles, electric vehicles, and off-road utility vehicles. Recently, passenger cars has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Passenger vehicles represent the largest installed vehicle base and highest ownership turnover, driving continuous replacement of interior protection components. Higher consumer emphasis on cabin aesthetics, comfort, and resale value further sustains carpet and mat purchases. OEM interior upgrades and aftermarket personalization trends are concentrated in passenger models, while urban commuting usage generates faster wear cycles, reinforcing recurring demand across dealerships, retailers, and digital sales channels.

Competitive Landscape

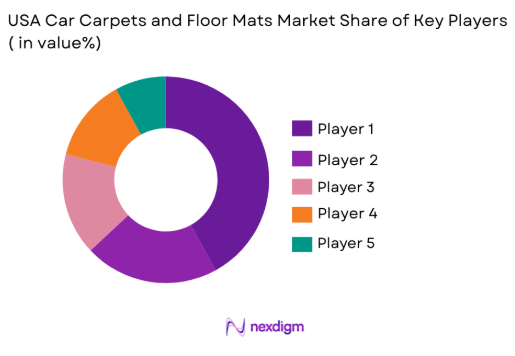

The USA Car Carpets and Floor Mats market exhibits moderate consolidation with a mix of OEM interior system suppliers and specialized aftermarket accessory manufacturers competing across price tiers and distribution channels. Established brands maintain strong market visibility through patented material technologies, custom-fit design capabilities, and nationwide dealer networks, while emerging direct-to-consumer firms leverage digital sales and vehicle-specific fit databases. Competitive positioning is shaped by durability performance, material innovation, and supply agreements with automotive manufacturers and large retail chains.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Integration Level |

| WeatherTech | 1989 | USA | ~ | ~ | ~ | ~ | ~ |

| Husky Liners | 1988 | USA | ~ | ~ | ~ | ~ | ~ |

| Auto Custom Carpets | 1977 | USA | ~ | ~ | ~ | ~ | ~ |

| Toyota Boshoku America | 2001 | USA | ~ | ~ | ~ | ~ | ~ |

| Lear Corporation | 1917 | USA | ~ | ~ | ~ | ~ | ~ |

USA Car Carpets and Floor Mats Market Analysis

Growth Drivers

Vehicle Parc Expansion and Interior Replacement Cycles

The USA maintains one of the world’s largest registered vehicle fleets, exceeding 290 million units, which directly sustains continuous demand for interior replacement components such as carpets and floor mats across both OEM and aftermarket channels. High average vehicle age in the country results in repeated wear and replacement of flooring materials due to daily usage, environmental exposure, and aesthetic deterioration, creating recurring purchasing cycles among consumers and fleet operators. Passenger vehicles and light trucks, which dominate ownership patterns, experience frequent ingress of dirt, moisture, and debris, accelerating carpet degradation and driving replacement demand. Replacement frequency is further amplified in regions with snow, mud, and road salt exposure that degrade textile and polymer flooring materials more rapidly than moderate climates. The strong aftermarket culture in the country encourages vehicle owners to invest in interior protection upgrades not only for durability but also for resale value preservation and comfort enhancement. Dealership accessory programs and digital aftermarket retailers actively promote replacement mat kits and liners, reinforcing recurring consumer engagement with flooring products. Fleet-based mobility services, delivery vehicles, and commercial light trucks experience higher interior wear rates due to continuous operation, intensifying procurement of durable mats and liners for maintenance efficiency. Insurance refurbishments and used vehicle reconditioning processes also contribute to flooring replacement demand, particularly in resale preparation cycles. As electric and hybrid vehicles expand within the fleet, manufacturers continue integrating specialized lightweight carpet systems, adding incremental OEM demand alongside traditional vehicle segments.

Rising Consumer Preference for Durable All-Weather Interior Protection

Consumers increasingly prioritize durable, easy-clean, and weather-resistant interior protection solutions as vehicle usage environments become more diverse and maintenance convenience becomes a key purchasing factor across both private and commercial ownership segments. All-weather thermoplastic and rubberized floor liners have gained strong acceptance because they provide superior containment of liquids, mud, and debris compared with traditional textile carpets, reducing cleaning effort and interior damage risk. Regions experiencing snow, rainfall, and off-road recreational usage generate particularly strong demand for protective liners due to persistent exposure to moisture and abrasive particles that degrade conventional carpets. Consumer awareness regarding interior hygiene and odor control has also increased demand for impermeable flooring materials that prevent moisture absorption and microbial growth within vehicle cabins. Premium automotive brands and dealerships increasingly bundle custom-fit floor liners and mats into accessory packages, reinforcing consumer perception of protective flooring as a standard interior enhancement rather than optional equipment. E-commerce automotive accessory platforms have expanded product visibility and availability of custom-fit liners tailored to specific vehicle models, simplifying consumer selection and accelerating adoption. Marketing by leading accessory brands emphasizes lifetime durability, laser-measured fitment, and stain resistance, shaping consumer expectations toward protective flooring solutions. Ride-sharing drivers and delivery vehicle operators favor protective liners due to reduced downtime for cleaning and longer service life compared with textile carpets. As vehicle interior aesthetics remain important for resale and ownership satisfaction, consumers continue replacing worn carpets with modern protective materials, sustaining long-term growth in all-weather flooring segments.

Market Challenges

Raw Material Price Volatility in Polymer and Rubber Inputs

The USA Car Carpets and Floor Mats market faces persistent cost pressure from volatility in key raw materials such as polypropylene fibers, nylon yarns, synthetic rubber, and thermoplastic elastomers that are derived from petrochemical feedstocks subject to global supply fluctuations and energy price shifts. Polymer pricing instability directly impacts manufacturing costs for molded mats, liners, and carpet backing layers, forcing producers to adjust pricing strategies and margin structures across OEM supply contracts and aftermarket retail channels. Automotive OEM contracts typically operate under long-term pricing agreements, limiting manufacturers’ ability to immediately pass through material cost increases and compressing profitability during commodity spikes. Small and mid-sized aftermarket producers are particularly vulnerable to raw material cost swings due to limited procurement scale and lower hedging capability compared with large interior system suppliers. Supply chain disruptions affecting resin availability, compounding additives, and textile fibers can delay production schedules and increase inventory holding costs across flooring manufacturers. Cost increases in rubber and polymer inputs also intensify price competition in retail channels as brands attempt to maintain consumer affordability while preserving margins. The need to reformulate materials to meet environmental and recyclability requirements can further increase development costs and manufacturing complexity. Transportation costs associated with bulky molded products amplify total cost sensitivity to material weight and density. Persistent raw material volatility therefore constrains pricing stability, planning visibility, and profitability across the flooring value chain, presenting an ongoing structural challenge for manufacturers.

Intense Price Competition from Low-Cost Imports

The USA Car Carpets and Floor Mats market experiences substantial competitive pressure from low-cost imported flooring products, particularly in the universal-fit mat and basic carpet replacement segments where price sensitivity among consumers is high and product differentiation is limited. Imported mats manufactured in low-cost production regions often enter retail and online channels at significantly lower price points, challenging domestic manufacturers that operate under higher labor, compliance, and material costs. These imports frequently target entry-level and mid-tier consumer segments, eroding market share for domestic aftermarket brands in value-oriented categories. Retailers and e-commerce platforms prioritize price competitiveness to attract consumers, increasing shelf space and digital visibility for imported products despite variability in durability and fit precision. Domestic producers must invest in branding, material quality, and custom-fit technologies to justify premium pricing, raising marketing and development expenditures. Counterfeit or imitation designs that replicate established brand aesthetics further dilute brand value and confuse consumers regarding quality differences. OEM suppliers also face indirect pressure as aftermarket pricing expectations influence perceived value of factory-installed flooring systems. Regulatory compliance costs related to safety and chemical emissions standards raise domestic production costs relative to imports produced under less stringent regimes. As price-driven purchasing behavior remains prevalent among many consumers, particularly for older vehicles, low-cost imports continue exerting downward pressure on margins and competitive positioning for domestic flooring manufacturers.

Opportunities

Adoption of Recyclable and Bio-Based Automotive Carpet Materials

The transition toward sustainable automotive interiors creates significant opportunity for manufacturers to develop recyclable and bio-based carpet fibers and backing materials that align with evolving environmental regulations and OEM sustainability targets across vehicle platforms. Automotive manufacturers increasingly seek interior components with reduced carbon footprint and improved end-of-life recyclability to meet corporate environmental commitments and regulatory expectations. Recycled polyethylene terephthalate fibers derived from post-consumer plastics offer viable alternatives to virgin synthetic yarns while maintaining durability and aesthetic properties required for automotive flooring applications. Bio-based polymers and natural fiber blends also provide opportunities for differentiated product positioning in premium and eco-conscious vehicle segments. Adoption of sustainable materials can enable flooring suppliers to secure long-term OEM contracts tied to green interior programs and electric vehicle platforms prioritizing lifecycle environmental performance. Consumers also demonstrate growing awareness of sustainable automotive accessories, particularly among electric vehicle owners who prioritize environmentally responsible products. Material innovation in recyclable backing layers and adhesives can improve disassembly and recycling of end-of-life carpets, supporting circular economy initiatives. Sustainable material adoption may also reduce exposure to petrochemical price volatility over time as alternative feedstocks diversify supply. As regulatory pressure and OEM sustainability goals intensify, suppliers investing in recyclable and bio-based flooring technologies can gain competitive advantage and access emerging vehicle interior programs.

Growth of Custom-Fit Digital Scanning and Direct-to-Consumer Sales

Advances in digital vehicle scanning, CAD-based patterning, and online configurators are transforming the USA Car Carpets and Floor Mats market by enabling highly precise custom-fit flooring products sold directly to consumers through e-commerce platforms, bypassing traditional retail distribution constraints. Laser-measured fitment technologies allow manufacturers to create vehicle-specific mat and carpet designs that match floor contours with high accuracy, improving functionality and aesthetic integration compared with universal products. Digital product databases covering thousands of vehicle models facilitate scalable mass customization while maintaining manufacturing efficiency. Direct-to-consumer online sales channels enable brands to offer extensive product variants, material options, and branding personalization without physical inventory limitations of retail stores. Consumers increasingly prefer online purchasing of vehicle-specific accessories due to convenience, transparent compatibility information, and home delivery. Digital marketing and data-driven customer targeting allow flooring brands to reach vehicle owners based on model ownership, usage patterns, and geographic conditions influencing flooring demand. Custom-fit product positioning supports premium pricing strategies and stronger brand loyalty compared with commoditized universal mats. Integration of 3D scanning and automated manufacturing processes reduces production lead times and enhances consistency of fitment quality. As digital retail penetration in automotive accessories continues expanding, manufacturers leveraging custom-fit technologies and direct distribution models can capture higher margins and strengthen market differentiation.

Major Player

- WeatherTech

- Husky Liners

- Auto Custom Carpets

- Lloyd Mats

- Toyota Boshoku America

- Lear Corporation

- Faurecia Interior Systems

- Autoneum North America

- 3M Automotive

- Suminoe Textile of America

- Flex-N-Gate Corporation

- Aurora Plastics

- Intro-Tech Automotive

- Rugged Ridge

Key Target Audience

- Automotive interiorcomponent suppliers

- Aftermarket accessory distributors

- Vehicle fleet operators

- Automotive dealerships

- E-commerce automotive retailers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Vehicle production, registered vehicle parc, aftermarket accessory sales, and automotive interior material consumption were identified as primary variables. Secondary variables included consumer spending patterns, replacement cycles, and climatic usage factors influencing floor protection demand across vehicle segments.

Step 2: Market Analysis and Construction

Supply-side data from OEM interior suppliers and aftermarket distributors were combined with vehicle fleet statistics and accessory sales indicators. Market sizing models integrated production fitment rates and replacement frequency to construct value and volume estimates across product and platform segments.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through interviews with automotive interior manufacturers, accessory retailers, and fleet maintenance managers. Cross-verification with industry associations and automotive production databases ensured consistency of demand drivers and regional consumption patterns.

Step 4: Research Synthesis and Final Output

Validated datasets were synthesized into segment-wise market estimates and competitive positioning analysis. Trend assessment incorporated material innovation, distribution shifts, and regulatory factors to generate forward-looking market outlook and strategic insights.

Executive Summary

Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising vehicle production and parc expansion in passenger and light truck segments

Increasing consumer preference for interior comfort and aesthetic upgrades

Growth of electric vehicles requiring lightweight interior materials

Expansion of automotive aftermarket customization culture

OEM focus on cabin noise reduction and insulation performance - Market Challenges

Volatility in polymer and rubber raw material prices

Intense price competition in aftermarket segments

Environmental compliance pressures on synthetic materials

Durability concerns in extreme weather usage conditions

Counterfeit and low-quality imports affecting brand trust - Market Opportunities

Adoption of recyclable and bio-based carpet fibers

Integration of antimicrobial and odor-resistant technologies

Premiumization through luxury interior personalization packages - Trends

Shift toward all-weather and easy-clean floor liner designs

Use of lightweight composite backing structures

Digital scanning for vehicle-specific custom-fit mats

Growth of direct-to-consumer automotive accessory brands

Increased use of recycled polymer content in carpets - Government Regulations & Defense Policy

Automotive interior flammability and safety compliance standards

Recycling and end-of-life vehicle material directives

Chemical emissions and cabin air quality regulations

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Tufted Automotive Carpets

Molded Floor Mats

All-Weather Floor Liners

Luxury Pile Carpets

Trunk and Cargo Mats - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Off-Road and Utility Vehicles - By Fitment Type (In Value%)

OEM Factory Fit

Dealer Installed Accessories

Aftermarket Custom Fit

Universal Fit Products

Retrofit Replacement Sets - By End User Segment (In Value%)

Automotive OEMs

Aftermarket Retail Consumers

Fleet Operators

Ride-Hailing and Mobility Providers

Commercial Vehicle Owners - By Procurement Channel (In Value%)

OEM Supply Contracts

Automotive Dealership Networks

Specialty Auto Accessory Stores

E-Commerce Platforms

Wholesale Distributors - By Material / Technology (in Value %)

Nylon Fiber Carpets

Polypropylene Fiber Carpets

Thermoplastic Elastomer Mats

Rubber Composite Mats

Recycled PET Fiber Carpets

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Material Technology, Fitment Precision, Product Durability, Price Range, Distribution Reach)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Auto Custom Carpets Inc

Lloyd Mats

WeatherTech

Husky Liners

3M Automotive

Toyota Boshoku America

Lear Corporation

Faurecia Interior Systems

Autoneum North America

Hyosung Advanced Materials America

Suminoe Textile of America

Aurora Plastics

Rugged Ridge

Intro-Tech Automotive

Flex-N-Gate Corporation

- OEMs prioritizing integrated interior system sourcing for cost efficiency

- Consumers seeking durable all-weather mats in harsh climate regions

- Fleet operators emphasizing easy-maintenance interior solutions

- Electric vehicle buyers favoring premium and eco-friendly materials

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now