Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA car finance market recorded a transaction value of approximately USD ~ billion in outstanding auto loan balances according to the Federal Reserve Bank of New York Consumer Credit Panel. The market continues to expand as financial institutions, credit unions, and captive finance companies support vehicle purchases through structured loan programs. Demand is primarily driven by high vehicle ownership rates, rising vehicle prices exceeding USD ~ thousand for new passenger vehicles according to Kelley Blue Book, and increasing consumer preference for installment-based vehicle acquisition models.

Dominance within the USA car finance ecosystem is concentrated in major metropolitan areas where vehicle demand and dealership density remain high. Cities such as Los Angeles, Houston, Dallas, Chicago, and Atlanta represent significant financing activity due to large populations and extensive automobile retail networks. Financial services hubs such as New York and Charlotte also play a major role because leading lenders and auto finance companies operate headquarters and lending platforms there. High personal mobility requirements, suburban commuting patterns, and dealership networks strengthen financing demand in these regions.

Market Segmentation

By Product Type

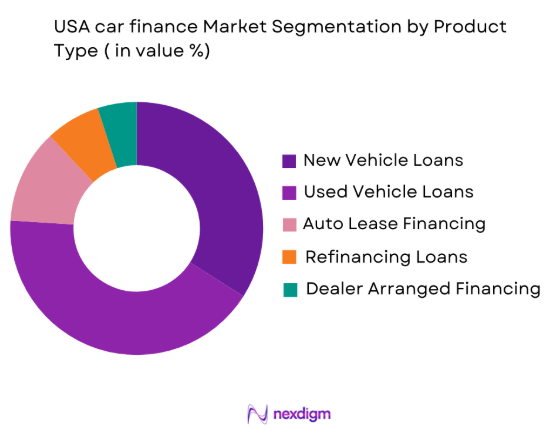

USA car finance market is segmented by product type into new vehicle loans, used vehicle loans, auto lease financing, refinancing loans, and dealer arranged financing. Recently, used vehicle loans has a dominant market share due to factors such as strong consumer demand for affordable transportation and increasing vehicle prices that push buyers toward the pre-owned segment. Financial institutions actively promote used vehicle financing programs because loan sizes remain attractive while credit risk is diversified across borrowers. Digital auto marketplaces and dealership networks also expand financing accessibility for pre-owned vehicles. As a result, used vehicle financing has become a central revenue stream for banks, captive finance companies, and credit unions operating in the automobile lending ecosystem across the United States.

By Platform Type

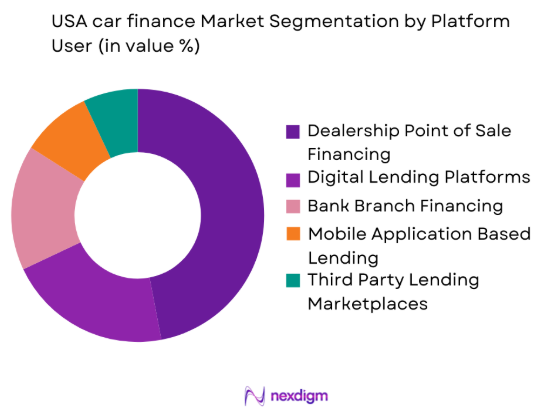

USA car finance market is segmented by platform type into dealership point of sale financing, digital lending platforms, bank branch financing, mobile application based lending, and third-party lending marketplaces. Recently, dealership point of sale financing has a dominant market share due to the convenience and integrated purchasing experience it offers to consumers during vehicle acquisition. Auto dealerships maintain partnerships with multiple lenders including banks, captive finance companies, and credit unions, enabling customers to compare financing options instantly while completing vehicle purchases. This arrangement accelerates loan approvals and reduces administrative effort for buyers. Dealers also provide promotional financing incentives supported by manufacturers, which further encourages borrowers to secure loans directly at the dealership.

Competitive Landscape

The USA car finance market is moderately consolidated with large banks, captive automotive finance companies, and specialized lending institutions controlling a significant portion of financing activity. Established lenders benefit from extensive dealership partnerships, strong credit evaluation systems, and nationwide lending networks. Competition continues to intensify as fintech platforms introduce digital lending solutions and faster credit approval systems. Captive finance arms of automobile manufacturers also maintain strong influence because they offer promotional financing programs that directly support vehicle sales across dealership networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Coverage |

| Ally Financial | 1919 | Detroit, USA | ~ | ~ | ~ | ~ | ~ |

| Capital One Auto Finance | 1994 | Virginia, USA | ~ | ~ | ~ | ~ | ~ |

| Chase Auto | 2000 | New York, USA | ~ | ~ | ~ | ~ | ~ |

| GM Financial | 1992 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

| Santander Consumer USA | 1995 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

USA car finance Market Analysis

Growth Drivers

Expansion of Digital Auto Lending Platforms

The rapid development of digital lending platforms is accelerating growth in the USA car finance market by enabling faster and more accessible loan processing. Financial institutions increasingly invest in technology driven credit approval systems that significantly reduce application processing time. Online platforms allow borrowers to complete applications, identity verification, credit checks, and loan approvals through digital channels without extensive physical documentation. Fintech firms collaborate with banks and dealerships to create integrated financing ecosystems that deliver personalized loan offers. Smartphone usage and internet access also expand financing availability through mobile applications and online marketplaces. Artificial intelligence based credit assessment tools further improve loan approval accuracy and operational efficiency.

Rising Vehicle Prices and Increasing Dependence on Consumer Financing

Rising vehicle prices in the United States have increased consumer reliance on automobile financing because upfront cash purchases have become difficult for many households. Average new vehicle transaction prices often exceed USD ~ thousand according to Kelley Blue Book, making installment based financing essential for buyers seeking manageable monthly payments. Financial institutions and captive finance companies provide flexible loan terms that extend repayment periods. Many consumers also finance used vehicles to reduce purchase costs. Automakers support financing demand through promotional interest rates and leasing programs offered via dealership networks. Limited public transportation and suburban commuting patterns further reinforce the need for vehicle ownership and structured financing solutions.

Market Challenges

Increasing Delinquency Risk in Subprime Auto Lending

Expanding automobile financing across diverse borrower groups has increased credit risk exposure, particularly within the subprime lending segment where borrowers may have limited credit history or weaker financial stability. Lenders competing for market share often extend loans to lower credit score borrowers, increasing the likelihood of payment delays and defaults. Subprime loans usually carry higher interest rates, which can create repayment pressure when household expenses rise. Economic volatility, employment instability, and inflation may further reduce repayment capacity. Regulators monitor lending practices to ensure responsible underwriting and transparent loan terms. Lenders must also manage vehicle depreciation risks while strengthening credit assessment systems to maintain portfolio stability.

Rising Interest Rate Environment Impacting Loan Affordability

Interest rate movements strongly influence automobile financing conditions because borrowing costs directly affect consumer affordability for vehicle loans offered by banks, credit unions, and captive finance companies. When benchmark interest rates increase, lenders typically raise auto loan rates, which raises monthly payments and reduces the number of borrowers who qualify for financing. Higher borrowing costs may discourage consumers from purchasing vehicles or delay buying decisions. Dealerships may experience slower vehicle sales during such periods. Lenders must balance competitive pricing with profitability while managing credit risk. To maintain demand, financial institutions introduce flexible loan structures, promotional financing offers, and refinancing options that help borrowers manage repayment obligations.

Opportunities

Integration of Artificial Intelligence in Credit Risk Assessment

Artificial intelligence technologies create strong opportunities for lenders in the USA car finance market by improving the accuracy and efficiency of credit evaluation. Advanced analytics systems allow financial institutions to assess borrower creditworthiness using broader financial data rather than relying only on traditional credit scores. AI tools analyze transaction histories, employment patterns, and digital payment behavior to generate more comprehensive borrower profiles. Machine learning models help lenders identify repayment reliability and expand financing access to underserved groups such as younger borrowers and gig economy workers. Automated credit assessment also reduces processing time and operational costs. Predictive analytics further enables lenders to monitor repayment patterns and reduce delinquency risks.

Growth of Electric Vehicle Financing Programs

The transition toward electric mobility in the United States is creating significant financing opportunities for lenders as electric vehicles typically involve higher upfront purchase costs than conventional vehicles. Financial institutions and captive finance companies are introducing specialized loan and leasing products designed for electric vehicle buyers. These vehicles incorporate advanced battery technologies and digital systems that increase manufacturing costs, making financing a key purchasing factor. Government incentives including federal tax credits also reduce effective ownership costs and support financing adoption. Manufacturers collaborate with lenders to provide promotional financing and leasing offers through dealerships and online platforms. Expanding charging infrastructure further strengthens consumer confidence and financing demand.

Future Outlook

The USA car finance market is expected to experience steady structural expansion as digital lending technologies, electric vehicle adoption, and evolving consumer financing models reshape the automobile purchasing ecosystem. Financial institutions are increasingly integrating advanced credit analytics and automated lending systems to accelerate loan approvals and improve borrower risk management. Regulatory oversight and responsible lending frameworks will continue to guide industry practices while maintaining consumer protection standards. Rising vehicle technology costs and continued reliance on private mobility are expected to sustain long term demand for vehicle financing solutions.

Major Players

- Ally Financial

- Capital One Auto Finance

- Chase Auto

- Bank of America Auto Loans

- Wells Fargo Dealer Services

- Toyota Financial Services

- Ford Motor Credit Company

- GM Financial

- Santander Consumer USA

- Credit Acceptance Corporation

- Westlake Financial Services

- TD Auto Finance

- Huntington Bank Auto Finance

- PNC Bank Auto Loans

- U.S. Bank Auto Loans

Key Target Audience

- Automobile manufacturers

- Vehicle dealership groups

- Automotive financing companies

- Commercial banks providing vehicle loans

- Investments and venture capitalist firms

- Government and regulatory bodies

- Vehicle leasing companies

- Digital automotive marketplaces

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables that influence the USA car finance market including vehicle sales volume, lending interest rates, consumer credit conditions, dealership networks, and digital financing platforms. These variables form the foundation for market analysis and data modeling.

Step 2: Market Analysis and Construction

Market data is constructed using financial reports from lending institutions, automobile sales statistics, and consumer credit databases. Data sources include financial institutions, automotive associations, and government economic databases to ensure reliable market insights.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists, financial analysts, and automotive finance professionals review the collected data to validate research assumptions and refine analytical models. Expert consultation ensures that industry dynamics and policy impacts are accurately reflected in the final analysis.

Step 4: Research Synthesis and Final Output

Validated data is synthesized through analytical frameworks to generate the final market insights, competitive analysis, segmentation structure, and long term outlook. The final report integrates quantitative data and qualitative insights to provide a comprehensive view of the market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Digital Auto Lending Platforms

Rising Vehicle Ownership Demand Across Urban Regions

Increasing Partnerships Between Dealerships and Financial Institutions - Market Challenges

Rising Interest Rate Environment Impacting Loan Affordability

Increasing Delinquency Risk in Subprime Auto Lending

Regulatory Compliance Requirements in Consumer Finance - Market Opportunities

Integration of Artificial Intelligence in Auto Credit Assessment

Growth of Electric Vehicle Financing Programs

Expansion of Online Used Car Financing Marketplaces - Trends

Adoption of Fully Digital Loan Origination Processes

Increasing Use of Credit Scoring Analytics in Loan Approval

Growth of Buy Now Pay Later Models for Vehicle Purchases - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Dealer Arranged Financing

Bank Auto Loans

Credit Union Auto Loans

Captive Finance Company Loans

Online Auto Lending Platforms - By Platform Type (In Value%)

Dealership Point of Sale Financing

Digital Lending Platforms

Bank Branch Financing

Mobile Application Based Financing

Third Party Lending Marketplaces - By Fitment Type (In Value%)

New Vehicle Financing

Used Vehicle Financing

Refinancing Loans

Lease Financing

Balloon Payment Financing - By End User Segment (In Value%)

Individual Consumers

Small Business Fleet Buyers

Corporate Fleet Operators

Ride Hailing Drivers

Vehicle Leasing Companies - By Procurement Channel (In Value%)

Direct Bank Lending

Auto Dealership Financing

Credit Union Financing

Online Financial Platforms

Captive Finance Institutions

- Market Share Analysis

- Cross Comparison Parameters (Loan Interest Rates, Loan Tenure Flexibility, Digital Lending Capability, Dealer Partnership Network, Credit Approval Speed, Loan Processing Time, Down Payment Requirements, Credit Score Eligibility Criteria, Refinancing Options, Early Loan Repayment Policies)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ally Financial

Capital One Auto Finance

Chase Auto

Bank of America Auto Loans

Wells Fargo Dealer Services

Toyota Financial Services

Ford Motor Credit Company

GM Financial

Santander Consumer USA

Credit Acceptance Corporation

Westlake Financial Services

TD Auto Finance

Huntington Bank Auto Finance

PNC Bank Auto Loans

U.S. Bank Auto Loans

- Growing Financing Demand from First Time Vehicle Buyers

- Increasing Adoption of Auto Loans by Gig Economy Drivers

- Rising Corporate Fleet Financing Requirements

- Expanding Used Vehicle Financing Among Value Conscious Consumers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now