Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Center Consoles market current size stands at around USD ~ million, reflecting sustained demand for offshore-capable recreational vessels across coastal and inland waterways. The segment benefits from strong participation in saltwater fishing, growing premium leisure boating culture, and expanding marina and dry-stack ecosystems. Product innovation across hull design, digital helm integration, and multi-engine configurations continues to elevate buyer preference for performance-oriented center consoles with enhanced safety, range, and onboard comfort.

Demand concentration is strongest across the Southeast Atlantic and Gulf Coast corridors, supported by dense marina networks, year-round boating conditions, and established service ecosystems. South Florida acts as a customization and performance hub, while Texas and the Carolinas anchor offshore fishing communities. The Northeast contributes seasonal volume through established boating clubs and dry storage facilities. Pacific coastal markets emphasize multipurpose use cases, supported by regulatory clarity on emissions, safety equipment standards, and vessel registration frameworks.

Market Segmentation

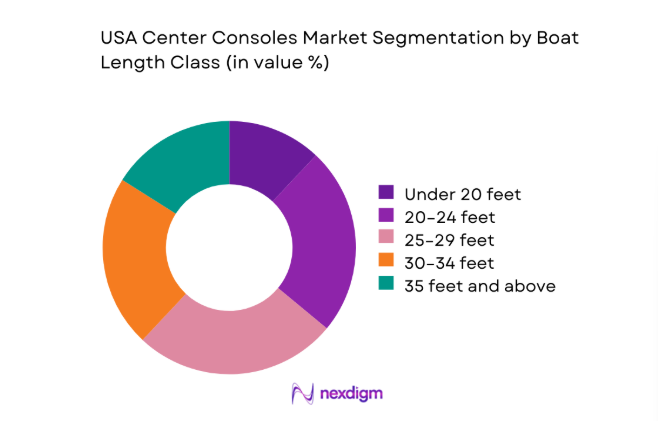

By Boat Length Class

Large-format center consoles dominate value share due to multi-engine configurations, higher onboard systems integration, and premium fit-out preferences among offshore anglers and leisure cruisers. Buyers increasingly favor 30 feet and above platforms for extended range, stability in open waters, and capacity for advanced electronics and safety systems. This segment benefits from repower cycles, customization programs, and strong aftermarket attachment rates. Mid-size vessels retain volume momentum among first-time buyers and coastal users seeking versatility. Smaller platforms remain relevant in inland and nearshore markets where trailering convenience and storage constraints shape purchasing decisions.

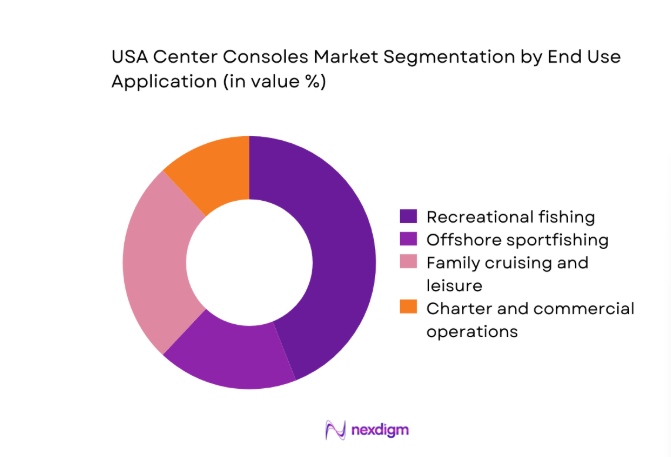

By End Use Application

Recreational fishing leads value contribution due to equipment intensity, higher engine power bands, and sustained participation in offshore angling. Family cruising and leisure applications are expanding as buyers prioritize comfort features, seating layouts, and stabilization systems that enable mixed-use outings. Charter and commercial operators contribute stable demand through fleet refresh cycles, prioritizing durability, uptime, and service coverage. Tournament sportfishing influences design trends and technology adoption, accelerating uptake of advanced navigation, fish-finding electronics, and livewell systems that cascade into mainstream consumer models.

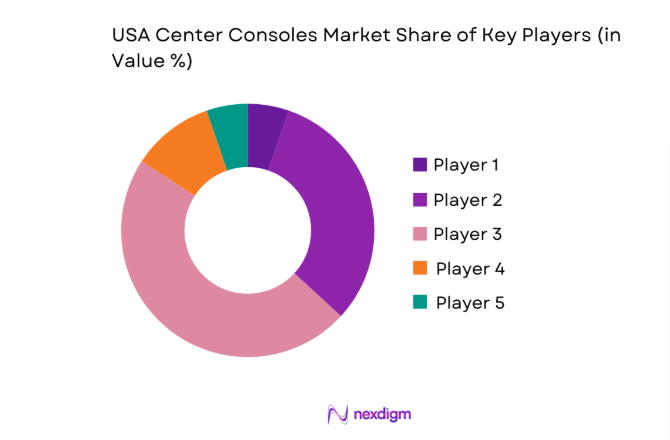

Competitive Landscape

The competitive landscape is characterized by differentiated positioning across performance, customization depth, dealer coverage, and aftersales service strength, with brands competing on offshore capability, fit-out flexibility, and delivery lead times.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Boston Whaler | 1958 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Grady-White Boats | 1959 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Scout Boats | 1989 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Everglades Boats | 2000 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Regulator Marine | 1988 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

USA Center Consoles Market Analysis

Growth Drivers

Rising participation in saltwater recreational fishing

Saltwater angler participation expanded across coastal counties, supported by 2023 license issuance records exceeding 2300000 permits in Florida, Texas, and North Carolina combined, indicating sustained usage intensity for offshore-capable vessels. Federal fisheries management updates in 2024 increased open-season days for key species by 18 days across multiple regions, extending boating activity windows. Marina berth counts across Southeast coastal metros reached 418000 slips by 2024, improving access to launch infrastructure. Coast Guard safety compliance checks in 2023 recorded 126000 inspections, reinforcing standardized equipment adoption. These institutional signals underpin durable demand for center consoles optimized for offshore fishing reliability.

Growth in coastal population and waterfront property ownership

Coastal county residential building permits in 2023 exceeded 412000 units across Florida, Texas, and the Carolinas, reflecting sustained migration toward waterfront-adjacent communities that favor private boat ownership. County-level boat ramp expansions in 2024 added 286 public access points along Atlantic and Gulf corridors, reducing congestion and increasing utilization frequency. State transportation agencies logged 214 new marina-adjacent access road upgrades during 2022–2024, improving tow-and-launch convenience. Insurance underwriting data in 2023 recorded 198000 new recreational marine policies across coastal ZIP codes, signaling structural growth in owner base aligned with center console usage patterns.

Challenges

High upfront vessel and ownership costs

Household interest rates for secured recreational loans averaged 8.1 during 2023–2024, increasing financing burdens for large-ticket marine assets. Marine insurance premiums rose by 19 index points across hurricane-prone counties between 2022 and 2024, elevating total cost of ownership. State registration and safety compliance fees across coastal states totaled ~ per vessel annually, creating friction for entry-level buyers. Storage constraints intensified as dry-stack facilities reported 91 utilization across South Florida in 2024, forcing buyers into higher-cost marina berths. These combined pressures constrain first-time adoption and slow replacement cycles for premium center consoles.

Fuel price volatility impacting usage frequency

Marine-grade gasoline price volatility during 2022–2024 exceeded 36 index points across Gulf Coast terminals, affecting trip frequency and voyage planning for offshore users. Port fuel depot throughput in 2023 declined by 140 million gallons across selected coastal hubs, reflecting demand sensitivity to price swings. State environmental agencies recorded 64 temporary fuel supply disruptions following storm events in 2024, complicating weekend boating availability. Vessel telematics providers observed average offshore trip durations contracting by 22 nautical miles in 2023 compared with 2022, indicating behavioral adaptation to operating cost uncertainty that disproportionately affects multi-engine center console usage patterns.

Opportunities

Growth in premium large-format center consoles

Registrations for vessels exceeding 30 feet increased by 12800 units across Atlantic and Gulf states during 2023–2024, reflecting structural shift toward large-format platforms with multi-engine propulsion. Marina redevelopment permits approved in 2024 added 1760 deep-water slips capable of accommodating wider beam vessels, improving berthing feasibility for premium center consoles. Coast Guard incident reports in 2023 showed lower offshore distress events per 1000 trips for vessels above 30 feet, reinforcing safety-driven buyer preference. Engine manufacturers expanded 450 to 600 horsepower production lines in 2024, supporting availability of high-power configurations aligned with premium demand.

Electrification and hybrid auxiliary power integration

State-level emissions guidance issued in 2024 introduced incentives for low-emission marine auxiliary systems across 9 coastal states, encouraging adoption of hybrid onboard power for electronics and hotel loads. Port authorities in 2023 installed 312 shore-power connections, enabling plug-in charging for auxiliary systems during berthing. Battery energy density certifications released in 2024 validated 280 watt-hours per kilogram for marine-grade packs, extending usable auxiliary runtime. Coast Guard equipment approvals in 2022 expanded acceptance of electric bilge and steering assist systems, lowering compliance barriers for hybrid integration in center consoles targeting environmentally conscious coastal communities.

Future Outlook

The outlook through 2030 reflects steady premiumization, continued offshore participation, and deeper integration of digital helm systems. Coastal infrastructure upgrades and marina redevelopment will shape access and utilization patterns. Policy emphasis on safety and emissions will guide design priorities, while hybrid auxiliary power adoption gains traction. Regional seasonality will persist, with Southeast corridors sustaining year-round activity.

Major Players

- Boston Whaler

- Grady-White Boats

- Sea Fox Boats

- Pursuit Boats

- Scout Boats

- Everglades Boats

- Contender Boats

- Regulator Marine

- Yellowfin Yachts

- Intrepid Powerboats

- Key West Boats

- Tidewater Boats

- Sportsman Boats

- Cobia Boats

- World Cat

Key Target Audience

- Offshore recreational anglers

- Family leisure boating households

- Charter and sportfishing operators

- Marina and dry storage facility owners

- Boat clubs and shared ownership platforms

- Outboard engine and marine electronics suppliers

- Investments and venture capital firms

- Government and regulatory bodies with agency names including the U.S. Coast Guard and state boating agencies

Research Methodology

Step 1: Identification of Key Variables

Primary variables included vessel class mix, propulsion configuration adoption, marina capacity, registration intensity, and compliance requirements across coastal states. Secondary variables captured usage frequency, storage availability, and service ecosystem coverage. Indicators were aligned to coastal infrastructure readiness and regulatory enforcement patterns.

Step 2: Market Analysis and Construction

The market framework integrated vessel class distribution, end-use applications, and channel structure across dealer and marina ecosystems. Demand signals were mapped to access infrastructure, insurance uptake, and licensing intensity. Supply-side inputs considered production cadence, engine availability, and service footprint coverage.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through structured interviews with marina operators, service technicians, coastal safety officers, and fleet managers. Triangulation was conducted against registration flows, berth utilization, and compliance inspection volumes. Divergences were reconciled through scenario testing across coastal corridors.

Step 4: Research Synthesis and Final Output

Findings were synthesized into a cohesive narrative connecting infrastructure readiness, regulatory clarity, and usage intensity. Segment-level insights were stress-tested against adoption constraints and operational risks. Outputs were structured to inform strategy, product positioning, and channel prioritization decisions.

- Executive Summary

- Research Methodology (Market Definitions and classification of center console vessels by size and propulsion, OEM production and shipment tracking across U.S. boat builders, dealer inventory audits and retail sell-through surveys, marina and dry storage operator interviews on usage patterns, engine supplier and electronics OEM shipment triangulation, pricing audits across dealer networks and online listings)

- Definition and Scope

- Market evolution

- Usage and application pathways

- Ecosystem structure

- Supply chain and dealer channel structure

- Regulatory and compliance environment

- Growth Drivers

Rising participation in saltwater recreational fishing

Growth in coastal population and waterfront property ownership

High-income consumer demand for premium offshore vessels

Advancements in outboard engine power and reliability

Expansion of marina, dry stack, and boat club infrastructure

Strong aftermarket electronics and accessories ecosystem - Challenges

High upfront vessel and ownership costs

Fuel price volatility impacting usage frequency

Limited marina and slip availability in key coastal hubs

Seasonality and weather-driven demand variability

Supply chain constraints for fiberglass, resins, and engines

Skilled labor shortages at boatyards and service centers - Opportunities

Growth in premium large-format center consoles

Electrification and hybrid auxiliary power integration

Subscription boat clubs and shared ownership models

Growth in repower and refit demand for aging fleets

Export demand from Caribbean and Latin American buyers

Financing innovation and bundled service packages - Trends

Upsizing toward multi-engine 30+ foot center consoles

Integration of advanced marine electronics and digital helm systems

Customization and factory-direct configuration programs

Lightweight materials and hull efficiency improvements

Enhanced safety, stabilization, and joystick docking systems

Growth of luxury amenities for family and leisure use - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Boat Length Class (in Value %)

Under 20 feet

20–24 feet

25–29 feet

30–34 feet

35 feet and above - By Propulsion Configuration (in Value %)

Single outboard

Twin outboard

Triple outboard

Quad outboard - By Engine Power Band (in Value %)

Under 200 HP

200–399 HP

400–699 HP

700 HP and above - By Hull and Build Type (in Value %)

Fiberglass production hulls

Composite and foam-core hulls

Semi-custom performance hulls

Custom-built offshore hulls - By End Use Application (in Value %)

Recreational fishing

Offshore sportfishing

Family cruising and leisure

Charter and commercial operations - By Sales Channel (in Value %)

Authorized dealer networks

Direct-to-consumer factory sales

Brokered pre-owned conversions

Boat shows and event sales

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (price positioning, model breadth, engine partnerships, customization depth, dealer network coverage, delivery lead times, warranty coverage, aftersales service footprint)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Boston Whaler

Grady-White Boats

Sea Fox Boats

Pursuit Boats

Scout Boats

Everglades Boats

Contender Boats

Regulator Marine

Yellowfin Yachts

Intrepid Powerboats

Key West Boats

Tidewater Boats

Sportsman Boats

Cobia Boats

World Cat

- Demand and utilization drivers

- Procurement and dealer negotiation dynamics

- Buying criteria and brand selection behavior

- Budget allocation and financing preferences

- Ownership, maintenance, and operational risk factors

- Post-purchase service and warranty expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now