Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Charging Connectors Market is valued at USD ~ billion based on a recent historical assessment supported by U.S. Department of Energy infrastructure deployment data and International Energy Agency electric vehicle statistics. The market size is driven by accelerated electric vehicle adoption, expansion of public DC fast charging networks, and federal infrastructure funding programs supporting nationwide charging corridor development. Increasing residential charging installations and commercial fleet electrification further contribute to sustained connector demand across passenger and heavy-duty vehicle segments.

Dominant regions within the USA Charging Connectors Market include California, Texas, and New York due to extensive electric vehicle registrations and large-scale charging infrastructure investments. California leads with clean transportation funding programs exceeding USD ~ billion supporting statewide charging deployment. Texas benefits from interstate freight electrification corridors and logistics hub expansion, while New York advances urban charging penetration through state-backed clean energy financing initiatives and municipal electrification mandates.

Market Segmentation

By Product Type

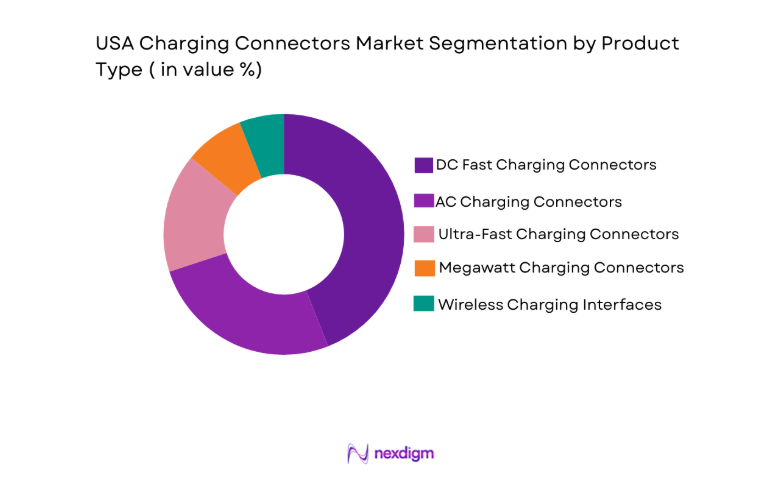

USA Charging Connectors market is segmented by product type into AC Charging Connectors, DC Fast Charging Connectors, Ultra-Fast Charging Connectors, Megawatt Charging Connectors, and Wireless Charging Interfaces. Recently, DC Fast Charging Connectors has a dominant market share due to rapid expansion of public fast charging infrastructure, increasing electric vehicle battery capacities requiring higher power transfer, strong federal corridor deployment programs, and widespread compatibility across passenger and commercial electric vehicle platforms in nationwide charging networks.

By Platform Type

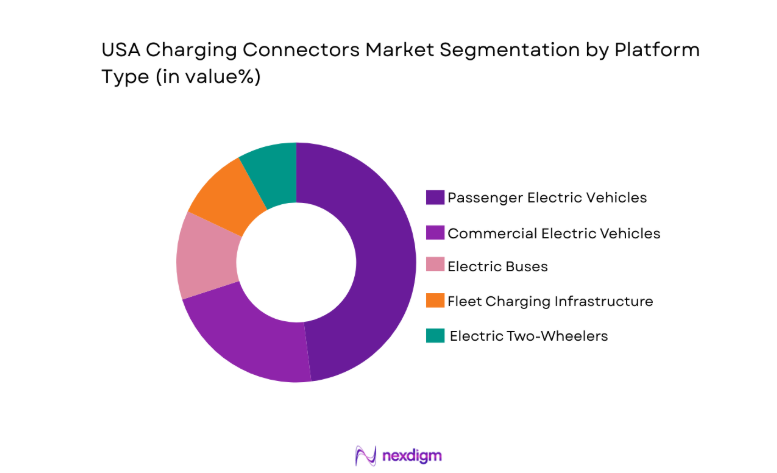

USA Charging Connectors Market is segmented by platform type into Passenger Electric Vehicles, Commercial Electric Vehicles, Electric Buses, Electric Two-Wheelers, and Fleet Charging Infrastructure. Recently, Passenger Electric Vehicles have a dominant market share due to strong consumer adoption, expanding residential charging installations, higher personal vehicle electrification rates, and growing availability of compatible connector standards across nationwide charging networks and automotive manufacturer partnerships.

Competitive Landscape

The USA Charging Connectors Market is moderately consolidated, with established automotive component manufacturers and charging infrastructure specialists influencing technological standardization and large-scale deployment. Strategic alliances between connector manufacturers and automakers are shaping interoperability, while investments in high-power fast charging technology are strengthening competitive positioning across commercial and passenger EV platforms.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Connector Power Rating Capability |

| TE Connectivity | 1941 | USA | ~ | ~ | ~ | ~ | ~ |

| Amphenol Corporation | 1932 | USA | ~ | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Tesla Inc | 2003 | USA | ~ | ~ | ~ | ~ | ~ |

| Phoenix Contact | 1923 | Germany | ~ | ~ | ~ | ~ | ~ |

USA Charging Connectors Market Analysis

Growth Drivers

Federal Infrastructure Investment and Electric Vehicle Expansion Funding

The United States government has committed substantial financial resources under nationwide infrastructure modernization initiatives, directing billions of dollars toward electric vehicle charging network development and interoperability enhancement programs across highways, urban centers, and rural corridors. These funding allocations reduce capital expenditure burdens for private charging network operators while incentivizing standardized connector adoption aligned with federal technical requirements, thereby accelerating deployment timelines. Automotive manufacturers are simultaneously expanding electric vehicle portfolios to comply with emissions standards and state-level zero-emission vehicle mandates, creating increased demand for compatible charging connectors. Public-private partnerships have strengthened large-scale procurement contracts for high-power DC fast charging connectors capable of supporting growing battery capacities and reduced charging durations. Expansion of freight electrification corridors and medium-duty commercial vehicle electrification further intensifies the need for high-current connector assemblies designed for durability and thermal stability. Additionally, federal tax credits and clean vehicle incentives encourage consumer adoption, indirectly stimulating connector manufacturing demand. Integration of charging infrastructure into multi-unit dwellings and workplace charging ecosystems increases distributed connector installations beyond public networks. State-level grants supplement federal funding, enabling municipal transit electrification programs that require standardized connectors for bus fleets and depot charging systems. Collectively, these policy-driven financial mechanisms create structural and sustained demand growth for charging connectors across diverse electric mobility applications.

Rapid Technological Advancement in High-Power Charging Systems

Continuous innovation in battery chemistry and vehicle energy storage capacity has elevated the requirement for connectors capable of safely transmitting higher voltage and current loads without performance degradation. High-power DC fast charging platforms exceeding 350 kW necessitate advanced thermal management features, liquid-cooled cable systems, and enhanced contact materials to minimize resistance losses and overheating risks. Manufacturers are investing in modular connector architectures that improve serviceability and compatibility with evolving communication protocols between vehicles and charging stations. Standardization convergence toward widely adopted systems improves cross-brand interoperability, encouraging network expansion and simplifying infrastructure planning. Growth in megawatt charging systems for heavy-duty commercial vehicles is driving demand for next-generation connector designs capable of handling extreme electrical loads. Advanced safety mechanisms such as arc detection, insulation monitoring, and fail-safe locking systems enhance user confidence and regulatory compliance. Integration of smart communication chips within connectors enables real-time monitoring, predictive maintenance analytics, and load balancing across charging networks. As charging durations decrease and vehicle battery capacities expand, connector reliability and lifespan become critical procurement criteria for operators. These technological advancements collectively enhance performance efficiency, operational safety, and infrastructure scalability, reinforcing sustained market expansion.

Market Challenges

Fragmented Connector Standardization Across Legacy and Emerging Platforms

The coexistence of multiple connector standards including CCS, CHAdeMO, and proprietary systems creates interoperability complexities that affect infrastructure planning and capital allocation decisions. Charging network operators must invest in multi-standard equipment configurations to accommodate diverse vehicle models, increasing procurement and maintenance costs. Automakers transitioning between connector standards generate uncertainty in long-term investment strategies for infrastructure providers and component manufacturers. Regulatory alignment between federal and state authorities can vary, influencing technical specifications and funding eligibility requirements. Legacy CHAdeMO installations require adapter solutions to integrate with newer platforms, adding operational constraints and potential reliability issues. Proprietary connector ecosystems may limit cross-network access, complicating universal accessibility objectives. Technical differences in communication protocols and power handling capabilities create engineering challenges in achieving seamless compatibility. Fleet operators managing mixed vehicle portfolios face logistical complexities in depot infrastructure upgrades. This fragmented environment slows universal standard adoption and increases transitional investment burdens across the value chain.

High Capital Intensity and Supply Chain Constraints

Manufacturing high-power charging connectors requires precision-engineered conductive materials, advanced insulation compounds, and robust thermal management systems that elevate production costs. Fluctuations in copper and specialized alloy pricing directly influence connector assembly expenses and margin structures. Semiconductor integration for smart communication capabilities introduces additional dependency on global electronics supply chains that have experienced volatility in recent years. Large-scale infrastructure deployment demands synchronized production capacity expansion, creating operational risk if demand projections shift. Certification compliance and safety testing standards increase time-to-market for newly developed connector models. International sourcing of specialized components may expose manufacturers to geopolitical trade disruptions and tariff adjustments. Logistics complexities associated with oversized or liquid-cooled cable assemblies increase transportation costs and installation planning requirements. Smaller market entrants may face barriers to scaling due to capital expenditure constraints in research, tooling, and quality assurance processes. These cumulative financial and operational pressures challenge profitability and strategic expansion planning across the industry.

Opportunities

Expansion of Fleet Electrification and Depot Charging Ecosystem

Rapid electrification of commercial delivery fleets, municipal transit systems, and corporate mobility services presents significant demand potential for standardized high-power connectors. Fleet operators require centralized depot charging systems capable of supporting overnight charging cycles with optimized load management, increasing procurement volumes for durable connector assemblies. Government emission reduction mandates and urban clean air policies accelerate replacement of internal combustion fleets with battery-electric alternatives. Integration of telematics platforms within fleet charging ecosystems enhances demand for connectors equipped with smart communication capabilities. Scaling of last-mile logistics electrification by e-commerce companies increases predictable, recurring connector demand. Dedicated charging hubs for commercial vehicles create opportunities for megawatt charging connectors designed for heavy-duty trucks. Public transit electrification programs funded through infrastructure grants require standardized connectors to ensure long-term compatibility and safety compliance. Private fleet investment in renewable energy-powered charging depots further supports integrated connector deployment strategies. This structural fleet transition provides stable, contract-based revenue streams for connector manufacturers and system integrators.

Development of Ultra-Fast and Megawatt Charging Corridors

Interstate freight electrification corridors are driving the rollout of ultra-fast and megawatt-scale charging stations capable of significantly reducing charging downtime for commercial vehicles. Connector designs must evolve to handle higher voltage architectures and advanced cooling technologies required for sustained high-current transmission. Infrastructure operators are prioritizing durable, weather-resistant connector systems suited for highway environments and high utilization rates. Federal corridor development programs incentivize uniform technical standards, benefiting manufacturers aligned with emerging megawatt charging specifications. Growing battery capacities in passenger and commercial vehicles necessitate scalable connector platforms that support future upgrades without complete infrastructure replacement. Utility companies collaborating on grid integration projects require connectors compatible with smart load balancing and energy storage integration systems. Cross-border harmonization of charging standards enhances export potential for U.S.-based connector manufacturers. Adoption of renewable-powered highway charging hubs further integrates sustainability objectives into connector design considerations. These advancements create long-term opportunities for innovation-driven market participants specializing in high-performance charging interface solutions.

Future Outlook

The USA Charging Connectors Market is expected to demonstrate steady expansion over the next five years supported by continued electric vehicle penetration and nationwide infrastructure upgrades. Advancements in high-power and megawatt charging technologies will reshape connector design standards and safety specifications. Regulatory alignment toward unified standards is anticipated to improve interoperability and reduce transitional fragmentation. Demand growth from commercial fleets and heavy-duty vehicle electrification will further strengthen long-term market fundamentals.

Major Players

- TE Connectivity

- Amphenol Corporation

- Aptiv PLC

- Tesla Inc

- Phoenix Contact

- Leviton Manufacturing Co

- ABB Ltd • Siemens AG

- Eaton Corporation

- Schneider Electric

- BorgWarner Inc

- Yazaki Corporation

- Sumitomo Electric Industries

- ITT Inc

- Hubbell Incorporated

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric vehicle manufacturers

- Charging infrastructure developers

- Automotive component suppliers

- Fleet operators

- Utility companies

- Transportation and logistics companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including connector types, voltage ratings, regulatory standards, infrastructure deployment volumes, and vehicle electrification trends were identified. Secondary data from government energy agencies and industry databases supported baseline parameter selection.

Step 2: Market Analysis and Construction

The market structure was constructed using value chain mapping and segmentation analysis. Supply-side manufacturing data and demand-side infrastructure deployment metrics were integrated to determine market sizing and share allocation.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including charging infrastructure engineers, automotive manufacturers, and procurement managers validated assumptions. Regulatory compliance insights and technology adoption trends were incorporated to refine market projections.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative findings were synthesized to generate actionable insights. Data triangulation ensured consistency across sources, and final outputs were structured according to standardized reporting frameworks.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of electric vehicle adoption across passenger and commercial segments

Federal and state funding programs supporting charging infrastructure deployment

Technological advancements in high power and ultra fast charging systems

Rising investments from utilities and private charging network operators

Integration of smart grid and vehicle to grid capabilities - Market Challenges

Standardization conflicts among connector formats and communication protocols

High capital expenditure for high power charging infrastructure

Supply chain volatility in copper and semiconductor components

Thermal management constraints in ultra fast charging connectors

Cybersecurity risks in smart connected charging system - Market Opportunities

Deployment of bidirectional charging connectors for grid stabilization

Expansion of fleet electrification programs across logistics and transit sectors

Development of liquid cooled ultra high power connector systems - Trends

Shift toward North American Charging Standard compatible connectors

Growing adoption of combined charging system architectures

Integration of digital authentication and billing technologies

Rise in public private partnerships for corridor charging projects

Increasing focus on sustainable and recyclable connector materials - Government Regulations & Defense Policy

Federal EV infrastructure funding under national clean transportation initiatives

State level zero emission vehicle mandates influencing connector demand

Safety certification standards under UL and SAE guidelines - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

AC Charging Connectors

DC Fast Charging Connectors

High Power Charging Connectors

Wireless Charging Interface Connectors

Bidirectional Charging Connectors - By Platform Type (In Value%)

Passenger Electric Vehicles

Commercial Electric Vehicles

Electric Buses

Two and Three Wheelers

Public Charging Infrastructure - By Fitment Type (In Value%)

OEM Factory Installed Connectors

Aftermarket Replacement Connectors

Retrofit Charging Port Systems

Fleet Integrated Charging Interfaces

Modular Connector Assemblies - By EndUser Segment (In Value%)

Automotive OEMs

Charging Network Operators

Fleet Operators

Residential EV Owners

Commercial Property Developers - By Procurement Channel (In Value%)

Direct OEM Contracts

Government Infrastructure Tenders

Private Charging Network Agreements

Distributor and Wholesaler Sales

Online B2B Procurement Platforms - By Material / Technology (in Value %)

Copper Alloy Conductive Connectors

Liquid Cooled Connector Systems

High Voltage Insulated Connectors

Smart Communication Enabled Connectors

Ruggedized Outdoor Grade Connectors

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Power Rating Capacity, Connector Standard Compatibility, Thermal Management Design, Communication Protocol Integration, Material Conductivity Grade

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

TE Connectivity

Amphenol Corporation

Aptiv PLC

Yazaki Corporation

Sumitomo Electric Industries

Phoenix Contact M

Hubbell Incorporated

Leviton Manufacturing

Schneider Electric

Siemens AG

ABB Ltd

Tesla Inc

ChargePoint Holdings

Eaton Corporation

Anderson Power Products

- Automotive OEMs prioritize interoperability and high power compatibility

- Charging network operators focus on durability and remote diagnostics capabilities

- Fleet operators demand fast turnaround and scalable connector solutions

- Residential users emphasize safety certifications and ease of installation

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now