Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Cloud Infrastructure Market is valued at approximately USD ~ billion based on recent historical industry assessments derived from hyperscale provider financial disclosures and enterprise cloud spending datasets. Demand is driven by accelerated enterprise digitization, AI workload expansion, and large-scale data processing requirements across industries such as finance, healthcare, retail, and public sector services. Growth is further supported by continuous capital expenditure from hyperscale cloud providers building advanced data center capacity and specialized computing infrastructure nationwide.

Dominant regions include Northern Virginia, Silicon Valley, Dallas, Phoenix, and Seattle due to dense fiber connectivity, proximity to enterprise customers, skilled technology labor pools, and favorable energy and tax environments. Northern Virginia leads as the largest global data center hub because of network exchange concentration and federal agency demand. Western regions host innovation-driven cloud architecture development, while central states attract large campuses due to land availability, renewable energy access, and scalable power infrastructure.

Market Segmentation

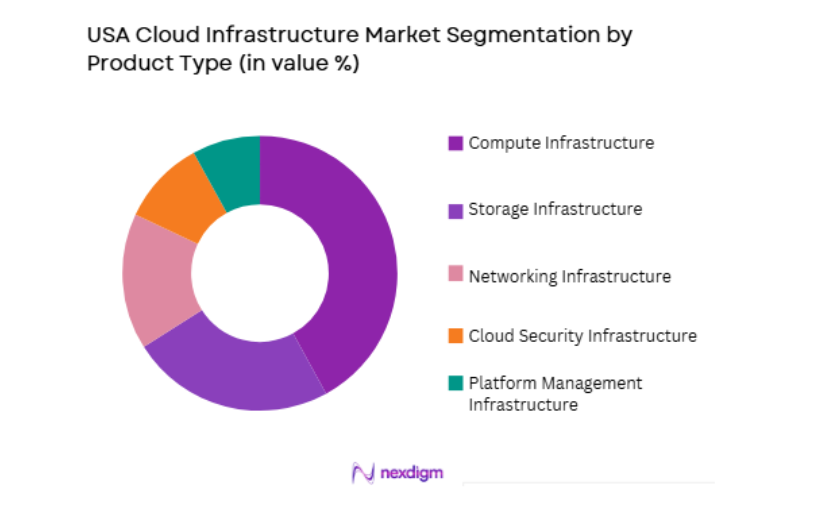

By Product Type

USA Cloud Infrastructure market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud security infrastructure, and platform management infrastructure. Recently, compute infrastructure has a dominant market share due to factors such as accelerated AI training workloads, enterprise application migration, containerized microservices architectures, and high-performance computing requirements across sectors. Hyperscale providers continuously expand GPU clusters, specialized AI accelerators, and virtualized compute pools to support generative AI and analytics workloads. Enterprise demand increasingly prioritizes scalable compute elasticity rather than static infrastructure ownership, strengthening compute consumption models.

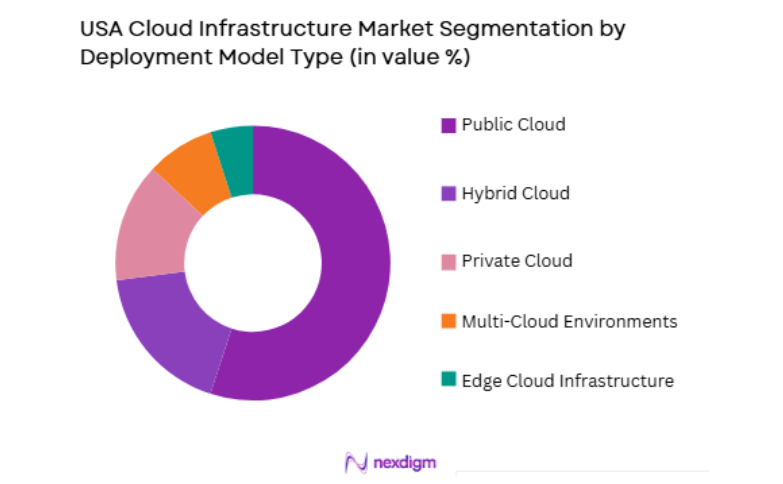

By Deployment Model

USA Cloud Infrastructure market is segmented by deployment model into public cloud, private cloud, hybrid cloud, multi-cloud environments, and edge cloud infrastructure. Recently, public cloud has a dominant market share due to factors such as on-demand scalability, global service availability, consumption-based pricing, and mature service ecosystems from hyperscale providers. Enterprises increasingly prioritize agility and rapid provisioning over capital-intensive on-premise systems, accelerating migration of mission-critical workloads to public environments. Public cloud platforms also provide integrated AI, analytics, and security services that reduce operational complexity compared to privately managed infrastructure. Additionally, software vendors optimize applications for public cloud deployment first, reinforcing default adoption pathways.

Competitive Landscape

The USA Cloud Infrastructure Market is highly consolidated, dominated by hyperscale technology firms with extensive capital expenditure capacity, proprietary hardware design, and global data center networks. Competitive intensity centers on AI compute leadership, data center scale, networking architecture efficiency, and integrated platform ecosystems. Major providers differentiate through specialized accelerators, enterprise cloud services portfolios, and hybrid cloud solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Capacity Scale |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

| Oracle | 1977 | Austin, USA | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | Armonk, USA | ~ | ~ | ~ | ~ | ~ |

USA Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise-Scale AI and Data Processing Infrastructure Expansion

Rapid enterprise adoption of artificial intelligence, machine learning analytics, and large-scale data platforms is significantly increasing demand for high-performance cloud compute, accelerated processing, and scalable storage architectures across industries. Organizations are migrating data-intensive workloads to cloud environments to leverage distributed processing and specialized AI accelerators unavailable in conventional IT infrastructure. Hyperscale providers are investing heavily in GPU clusters, AI chips, and high-bandwidth networking fabrics to support generative AI training and inference workloads at scale. Financial institutions, healthcare systems, and digital platforms are deploying advanced analytics pipelines that require elastic compute provisioning and petabyte-level storage throughput. AI-driven automation and decision intelligence applications further expand enterprise dependence on scalable infrastructure services rather than on-premise capacity. Software vendors increasingly design products optimized for cloud-native AI execution, reinforcing infrastructure demand alignment. The proliferation of data-centric business models, including personalization, predictive maintenance, and real-time optimization, multiplies processing requirements across sectors. Continuous innovation in foundation models and enterprise AI frameworks ensures sustained infrastructure consumption growth.

Large-Scale Digital Transformation and Application Modernization Programs

Enterprises across the United States are executing multi-year digital transformation initiatives that involve migrating legacy applications, modernizing enterprise resource systems, and deploying cloud-native architectures to enhance operational agility and scalability. Traditional data center environments lack the flexibility and automation capabilities required for modern software delivery models such as microservices, containers, and continuous integration pipelines. Cloud infrastructure enables standardized development platforms, automated provisioning, and elastic scaling essential for modern enterprise IT operations. Organizations are consolidating fragmented infrastructure estates into unified cloud platforms to reduce complexity and improve resource utilization efficiency. Hybrid integration tools and managed services simplify migration of mission-critical workloads from legacy systems into cloud environments without service disruption. Digital customer engagement platforms, omnichannel commerce systems, and connected enterprise ecosystems rely on resilient cloud backbones to support real-time interactions. Regulatory compliance frameworks increasingly accept secure cloud environments, accelerating migration in highly regulated sectors. Technology vendors prioritize cloud-first deployment strategies, encouraging enterprise transition through licensing and innovation alignment.

Market Challenges

Rising Data Center Energy Consumption and Sustainability Constraints

Expansion of hyperscale cloud infrastructure requires substantial electricity supply, cooling capacity, and land resources, creating sustainability and regulatory pressures that challenge continued rapid capacity deployment across key regions. Large data center campuses consume power equivalent to small cities, intensifying scrutiny from local governments, utilities, and environmental agencies concerned about grid stability and carbon emissions. Renewable energy sourcing and long-term power purchase agreements partially mitigate impact but require complex coordination and infrastructure investment. Water-intensive cooling technologies raise additional environmental concerns in water-stressed regions, complicating site approvals and operational sustainability strategies. Communities increasingly resist large data center developments due to land use, noise, and environmental considerations, slowing expansion timelines. Utilities must upgrade transmission infrastructure to support concentrated data center loads, increasing deployment costs and delays. Sustainability reporting requirements compel cloud providers to demonstrate measurable emissions reduction progress, influencing infrastructure design decisions. Energy price volatility also affects operating economics and long-term capacity planning across regions.

Cloud Security, Compliance, and Data Sovereignty Complexities

As enterprises migrate critical workloads and sensitive data into cloud environments, concerns regarding cybersecurity resilience, regulatory compliance, and jurisdictional data governance create barriers to adoption and infrastructure utilization expansion. High-profile cyber incidents and supply chain vulnerabilities heighten scrutiny of shared infrastructure environments and multi-tenant architectures. Regulated sectors such as healthcare, finance, and government require stringent compliance certifications and audit transparency from cloud providers before migrating sensitive systems. Data localization requirements and sector-specific regulations complicate centralized cloud deployment models across jurisdictions. Organizations must implement advanced identity management, encryption, and monitoring frameworks to ensure secure cloud operations, increasing operational complexity. Hybrid and multi-cloud environments further expand attack surfaces and governance challenges due to fragmented visibility across platforms. Rapid evolution of cybersecurity threats demands continuous infrastructure updates and security innovation from providers. Enterprises often maintain parallel on-premise systems to mitigate perceived risk, slowing full cloud adoption.

Opportunities

Edge Cloud Infrastructure for Distributed Digital Services

The proliferation of connected devices, real-time applications, and latency-sensitive digital services is creating significant opportunity for edge cloud infrastructure deployment across metropolitan and industrial environments throughout the United States. Autonomous systems, smart manufacturing, telemedicine, immersive media, and intelligent transportation require localized processing near data generation points rather than centralized hyperscale regions. Telecom operators, cloud providers, and infrastructure vendors are collaborating to deploy micro data centers and distributed compute nodes at network edges. Edge architectures reduce latency, bandwidth usage, and data transfer costs while enabling real-time analytics and decision automation capabilities. Enterprises adopting industrial IoT and operational technology integration increasingly demand edge compute to support machine-level intelligence and predictive control systems. Content delivery networks and streaming platforms also expand edge presence to improve user experience and service reliability. Government smart infrastructure initiatives further stimulate distributed cloud deployment across urban environments. Standardized edge orchestration platforms simplify management of distributed infrastructure fleets.

Specialized AI Cloud Platforms and Accelerated Computing Services

Growing demand for artificial intelligence training, inference, and high-performance data analytics is creating opportunities for specialized cloud platforms built around accelerated computing architectures and domain-specific AI services. Enterprises increasingly require GPU clusters, tensor accelerators, and optimized AI software stacks that exceed capabilities of traditional virtualized compute environments. Cloud providers are developing dedicated AI infrastructure offerings with preconfigured frameworks, model libraries, and scalable training environments tailored to enterprise use cases. Industry-specific AI clouds for healthcare diagnostics, financial modeling, scientific research, and media generation are emerging as differentiated service layers. Hardware innovation in AI accelerators and high-speed interconnects enables new performance tiers unavailable in conventional compute infrastructure. Managed AI services reduce barriers for enterprises lacking in-house expertise while increasing infrastructure consumption. Partnerships between semiconductor firms and cloud providers accelerate deployment of next-generation AI hardware into cloud environments. National AI strategy initiatives and research funding further support specialized infrastructure expansion. The transition from general-purpose cloud computing toward AI-optimized infrastructure therefore represents a substantial growth opportunity across the United States cloud ecosystem.

Future Outlook

The USA Cloud Infrastructure Market is expected to expand steadily over the next five years as enterprise AI adoption, application modernization, and digital platform expansion continue to accelerate infrastructure consumption. Hyperscale providers will invest heavily in AI-optimized data centers, edge cloud nodes, and sustainable energy-efficient facilities. Regulatory acceptance of secure cloud environments and public-sector cloud migration will broaden demand. Edge computing, hybrid architectures, and specialized AI clouds will diversify deployment models. Continued enterprise reliance on scalable digital infrastructure will sustain long-term market growth.

Major Players

- Amazon Web Services

- Microsoft

- Google Cloud

- Oracle

- IBM

- Cisco Systems

- Hewlett Packard Enterprise

- Dell Technologies

- Equinix

- Digital Realty

- NVIDIA

- Intel

- VMware

- Salesforce

- Akamai Technologies

Key Target Audience

- Cloud service providers

- Telecom operators

- Data center developers

- Enterprise IT infrastructure buyers

- Semiconductor and hardware manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI and digital platform companies

Research Methodology

Step 1: Identification of Key Variables

Core market variables including cloud spending by segment, hyperscale capital expenditure, data center capacity growth, enterprise workload migration rates, and AI infrastructure adoption indicators were defined. Supply-side metrics such as provider revenue, regional capacity distribution, and deployment models were mapped. Demand-side variables across industries and enterprise size categories were incorporated to ensure comprehensive coverage.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using triangulation of provider financial disclosures, infrastructure deployment datasets, enterprise IT spending patterns, and cloud workload distribution benchmarks. Product and deployment shares were estimated through usage distribution modeling across compute, storage, and service consumption layers. Regional infrastructure concentration and enterprise adoption intensity were integrated to refine allocation.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with cloud architects, data center strategists, enterprise CIO advisors, and infrastructure technology specialists. Adoption drivers, deployment trends, and infrastructure investment priorities were cross-checked against real-world implementation patterns. Expert insights ensured accuracy in segment dominance assumptions and technology trajectory interpretations.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized into structured market intelligence covering size, segmentation, competition, and strategic outlook. Analytical consistency checks ensured alignment between demand drivers, infrastructure supply expansion, and technology evolution trends. The final report integrates quantitative modeling with strategic interpretation for actionable market understanding.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Enterprise digital transformation and workload migration

AI and data intensive application infrastructure demand

Expansion of edge and low latency cloud services - Market Challenges

Data sovereignty and regulatory compliance complexity

Rising energy and data center operating costs

Vendor lock in and interoperability constraints - Market Opportunities

Sovereign and industry specific cloud platforms

AI optimized cloud infrastructure offerings

Sustainable and carbon efficient cloud data centers - Trends

Shift toward multi cloud and hybrid architectures

Growth of GPU accelerated cloud infrastructure

Automation driven cloud operations and AIOps - Government regulations

Federal cloud security and compliance frameworks

Data residency and privacy protection mandates

Energy efficiency and data center sustainability standards - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute Infrastructure as a Service

Storage Infrastructure as a Service

Network Infrastructure as a Service

Cloud Security Infrastructure

Cloud Management and Orchestration Infrastructure - By Platform Type (In Value%)

Hyperscale Public Cloud Platforms

Enterprise Private Cloud Platforms

Hybrid and Multi Cloud Platforms

Edge Cloud Infrastructure Platforms

Sovereign and Government Cloud Platforms - By Fitment Type (In Value%)

Greenfield Cloud Data Center Deployments

Brownfield Data Center Modernization

Cloud Native Platform Integration

Container and Kubernetes Infrastructure

Virtualization and Migration Infrastructure - By End User Segment (In Value%)

Large Enterprises and Digital Native Firms

Small and Medium Businesses

Government and Public Sector Agencies

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio Breadth, Data Center Footprint and Regional Coverage, AI and GPU Infrastructure Capability, Network Backbone and Edge Integration, Security and Compliance Certifications, Pricing Model Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud Platform

Oracle Cloud Infrastructure

IBM Cloud

Equinix

Digital Realty

Lumen Technologies

Cloudflare

Akamai Technologies

Salesforce

VMware

Hewlett Packard Enterprise

Cisco Systems

Alibaba Cloud

- Enterprises accelerating migration of mission critical workloads

- SMBs adopting managed and platform based cloud services

- Public sector expanding secure and sovereign cloud adoption

- Telecom operators integrating edge and cloud infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now