Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Automotive Clutches market represents a vital component of the broader automotive drivetrain industry, driven by ongoing demand for manual, semi‑automatic, and dual‑clutch systems across passenger and commercial vehicles. Based on a recent regional assessment, the North America automotive clutch market size—driven predominantly by the United States—was valued at approximately USD ~ billion in USD on a historical basis, reflecting widespread integration in manual transmissions and growing use in performance and hybrid vehicles. OEM production for clutches and related aftermarket replacement demand supports this valuation.

Based on a recent regional assessment, the United States remains the principal market for automotive clutches in North America due to its large automotive manufacturing base, substantial vehicle ownership, and strong demand for diverse transmission systems. Automotive hubs such as Michigan and Ohio host major OEM facilities and extensive supplier networks that integrate clutch systems into vehicles across various segments. Additionally, states such as California and Texas, with advanced automotive engineering and high aftermarket activity, support continued adoption of clutch technologies for both traditional and hybrid drivetrain applications.

Market Segmentation

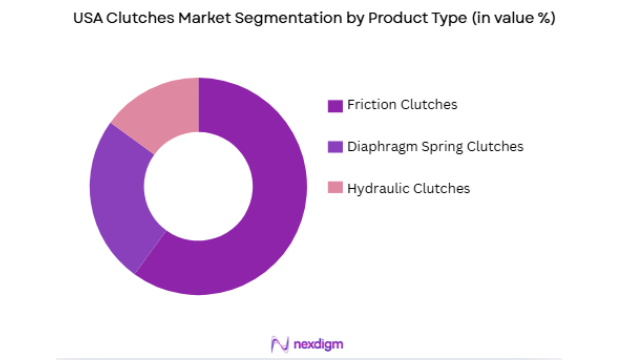

By Product Type

The USA clutches market is segmented by product type into friction clutches, diaphragm spring clutches, and hydraulic clutches. Recently, friction clutches have dominated the market due to factors such as their widespread use in passenger vehicles, light-duty trucks, and motorcycles. The high demand for these clutches can be attributed to their ability to offer smoother engagement and more reliable performance, which aligns with consumer expectations for ease of driving and enhanced vehicle longevity. These products also benefit from advances in materials, such as carbon and ceramic composites, which improve durability and performance. The increasing penetration of automated and electric vehicles has also contributed to the market’s growth, further cementing the dominance of friction clutches in various applications.

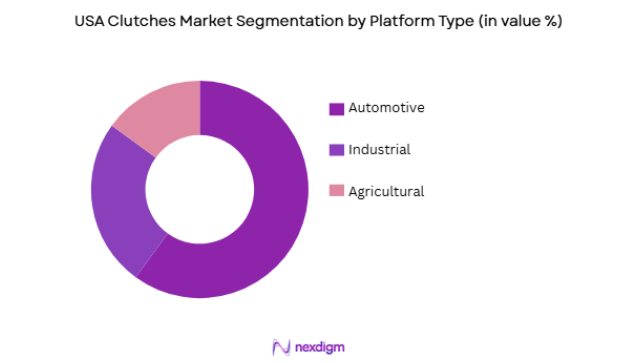

By Platform Type

The USA clutch market is segmented by platform type into automotive, industrial, and agricultural platforms. Recently, the automotive platform has dominated the market due to the continued high demand for vehicles across various segments, including light-duty cars and trucks. The rising adoption of automatic and hybrid transmission systems has also played a significant role in driving the demand for clutches tailored for such platforms. Additionally, with increased consumer interest in electric vehicles, manufacturers are working to develop clutches that meet the unique requirements of electric drivetrains, further consolidating the automotive sector’s dominant position in the market.

Competitive Landscape

The competitive landscape of the USA clutches market is highly consolidated, with key players dominating the market through strategic mergers and acquisitions. Major players continue to focus on technological advancements, particularly in the areas of efficiency, durability, and environmental impact. The strong presence of both global and regional manufacturers has fostered intense competition, driving innovations and influencing pricing strategies. As electric and hybrid vehicles rise in popularity, these players are expanding their product offerings to meet the needs of these emerging segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Market-Specific Parameter |

| BorgWarner | 1928 | Auburn Hills, MI | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen | 1915 | Friedrichshafen, DE | ~ | ~ | ~ | ~ | ~ |

| Eaton | 1911 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

| Schaeffler | 1946 | Herzogenaurach, DE | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ | ~ |

USA Clutches Market Analysis

Growth Drivers

Demand for Hybrid and Electric Vehicles

The increasing shift towards hybrid and electric vehicles (EVs) has fueled the demand for innovative clutch systems designed specifically for these vehicles. Traditional clutch systems, often designed for internal combustion engine (ICE) vehicles, are not always compatible with electric drivetrains, requiring the development of new clutch technologies. Manufacturers are focusing on the creation of clutches that can handle high torque and frequent engagement/disengagement, characteristics typical of electric vehicles. As EV adoption rises, the need for such advanced systems will continue to drive market growth. This shift is supported by both government incentives for cleaner vehicles and consumer interest in sustainable alternatives to traditional vehicles. As a result, companies in the clutch manufacturing sector are aligning their product development with the increasing demand for EVs and their unique requirements.

Technological Advancements in Clutch Systems

Another key growth driver is the rapid development of more durable and efficient clutch systems. Technological innovations, such as the development of friction materials that enhance performance and longevity, are propelling the market forward. These advancements reduce the wear and tear of traditional clutches and improve vehicle fuel efficiency, meeting the increasing demand for better-performing systems. Additionally, the development of automated manual transmission (AMT) systems, which rely on advanced clutch technology, is expected to boost the market, as AMT systems are becoming more prevalent in modern vehicles. As new technologies continue to emerge, manufacturers are investing heavily in R&D to stay competitive and meet changing consumer demands, ensuring sustained market growth.

Market Challenges

High Cost of Advanced Clutch Systems

One of the significant challenges facing the USA clutches market is the high cost associated with the development and integration of advanced clutch systems, particularly for electric and hybrid vehicles. While these systems provide significant performance and efficiency improvements, their high manufacturing costs pose a barrier to their widespread adoption. This challenge is especially acute for smaller vehicle manufacturers who may not have the resources to invest in cutting-edge clutch technologies. The price disparity between traditional and advanced systems may also discourage consumers from opting for vehicles equipped with more sophisticated clutch solutions, which can affect overall market growth. As the demand for advanced vehicle systems continues to rise, addressing the cost factor will be crucial for manufacturers looking to remain competitive in the marketplace.

Supply Chain Disruptions

The USA clutches market has also faced challenges from ongoing global supply chain disruptions, exacerbated by geopolitical tensions, pandemics, and natural disasters. These disruptions have led to delays in the production and delivery of critical raw materials, such as specialized metals and friction materials, which are essential for clutch system manufacturing. Shortages in these materials have affected production schedules, leading to a delay in the availability of new clutch systems to market. Furthermore, fluctuations in the costs of raw materials have caused price volatility, impacting both manufacturers and end consumers. These supply chain issues have made it difficult for companies to maintain consistent product availability, which is essential for meeting consumer demand and driving market growth.

Opportunities

Integration of Smart Technologies in Clutch Systems

The integration of smart technologies into clutch systems presents a significant opportunity for growth in the USA clutches market. With the rise of connected vehicles and autonomous driving technologies, there is an increasing need for clutches that can be controlled electronically for smoother operation and better performance. The development of intelligent clutches, which can automatically adjust to driving conditions and vehicle needs, has the potential to revolutionize the market. Such systems are expected to provide enhanced efficiency, improve fuel economy, and reduce emissions. As the automotive industry pushes toward greater automation and smarter vehicle systems, the demand for clutches with integrated smart technologies will increase, presenting a promising opportunity for manufacturers.

Expansion into Emerging Markets

Another opportunity for growth lies in expanding the presence of USA clutch manufacturers in emerging markets, particularly in regions like Asia-Pacific and Latin America. As these regions experience increased automotive production and sales, there is a growing demand for high-quality clutch systems, which USA-based manufacturers are well-positioned to meet. Additionally, emerging markets are witnessing significant infrastructure development, which will spur demand for industrial and agricultural vehicles, further driving clutch sales. By leveraging their established expertise and technological innovations, USA manufacturers can capitalize on these emerging markets, fostering long-term growth and expanding their global footprint.

Future Outlook

Over the next five years, the USA clutches market is expected to see sustained growth, driven by increasing demand from the automotive and industrial sectors. Technological advancements in clutch materials, designs, and automation are expected to enhance the performance and efficiency of clutch systems, especially for electric and hybrid vehicles. The continued emphasis on sustainability and reduced emissions will further fuel innovation in the sector, aligning with government regulations and consumer preferences for greener alternatives. Strong demand from both the automotive sector and emerging industrial applications will continue to drive market dynamics.

Major Players

- BorgWarner

- ZF Friedrichshafen

- Eaton

- Schaeffler

- Valeo

- Aisin Seiki

- Clutch Masters

- EXEDY Corporation

- LuK GmbH & Co. KG

- Sachs

- Mahle GmbH

- Tenneco Inc.

- Federal-Mogul Motorparts

- Light Vehicle Clutch Systems

- Eaton Corp.

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Private automotive manufacturers

- Automotive part suppliers

- Industrial equipment manufacturers

- Agricultural equipment producers

- Vehicle fleet operators

- Electric vehicle developers

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the critical factors influencing the USA clutches market, such as product types, technological advancements, and key geographical regions.

Step 2: Market Analysis and Construction

This step includes gathering data from multiple sources, analyzing industry reports, consumer surveys, and market trends to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Experts from the automotive, industrial, and research sectors are consulted to validate the hypotheses and ensure the accuracy of market projections.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all gathered information into a coherent market report, including actionable insights and forecasts for future market trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Demand for Fuel-Efficient Vehicles

Technological Advancements in Transmission Systems

Rising Vehicle Production Across Segments - Market Challenges

Stringent Regulatory Requirements

High Maintenance Costs

Rising Raw Material Prices - Market Opportunities

Emerging Demand for Electric Vehicle (EV) Clutches

Expansion of Aftermarket Services

Growth in Emerging Automotive Markets - Trends

Increase in Adoption of Dual-Clutch Systems

Rising Preference for Automated Transmission Systems

Integration of Smart Technology in Clutches - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Manual Clutches

Automatic Clutches

Semi-Automatic Clutches

Pneumatic Clutches

Hydraulic Clutches - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Off-Highway Vehicles

Motorcycles

Heavy Duty Equipment - By Fitment Type (In Value%)

Original Equipment Manufacturer (OEM)

Aftermarket

Replacement

Custom Fit

Retrofit - By EndUser Segment (In Value%)

Automotive Industry

Agricultural Sector

Construction Sector

Aerospace Industry

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Price Range, Product Lifecycle, Manufacturing Technology, Distribution Network, Customer Demographics)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BorgWarner

ZF Friedrichshafen AG

Schaeffler Group

Valeo SA

Eaton Corporation

Clutch Masters

Exedy Corporation

Automann

Aisin Seiki

Wabco Holdings

Sachs (ZF)

Daimler AG

Ford Motor Company

Tenneco Inc.

Magna International

- Automotive Industry’s Shift Toward More Efficient Transmissions

- Agricultural Sector’s Need for Reliable Clutch Systems

- Growth in Demand from Commercial and Heavy-Duty Vehicles

- Increasing Focus on Aftermarket Parts in Automotive Services

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now