Download PDF

Download PDFMarket Overview

The USA collagen market is valued at USD ~ million, compared with USD ~ million in the previous base year, supported by dietary supplements, functional food, beauty-from-within products, healthcare formulations, gelatin-based food applications and pharmaceutical excipients. Growth is primarily driven by demand from food & beverage, healthcare & pharmaceutical sectors, and higher adoption of collagen-based products for gelling, emulsification, binding, skin hydration, joint health and muscle-support formulations. California, New York, Florida and Texas are the strongest U.S. demand clusters because they combine large consumer bases, premium wellness retail, beauty supplement adoption, e-commerce penetration and healthcare infrastructure. California recorded 39,198,693 residents in the previous base year and 39,431,263 residents in the latest base year, while Texas rose from 30,727,890 to 31,290,831, strengthening mass-market collagen supplement consumption and functional food manufacturing demand.

Market Segmentation

By Source

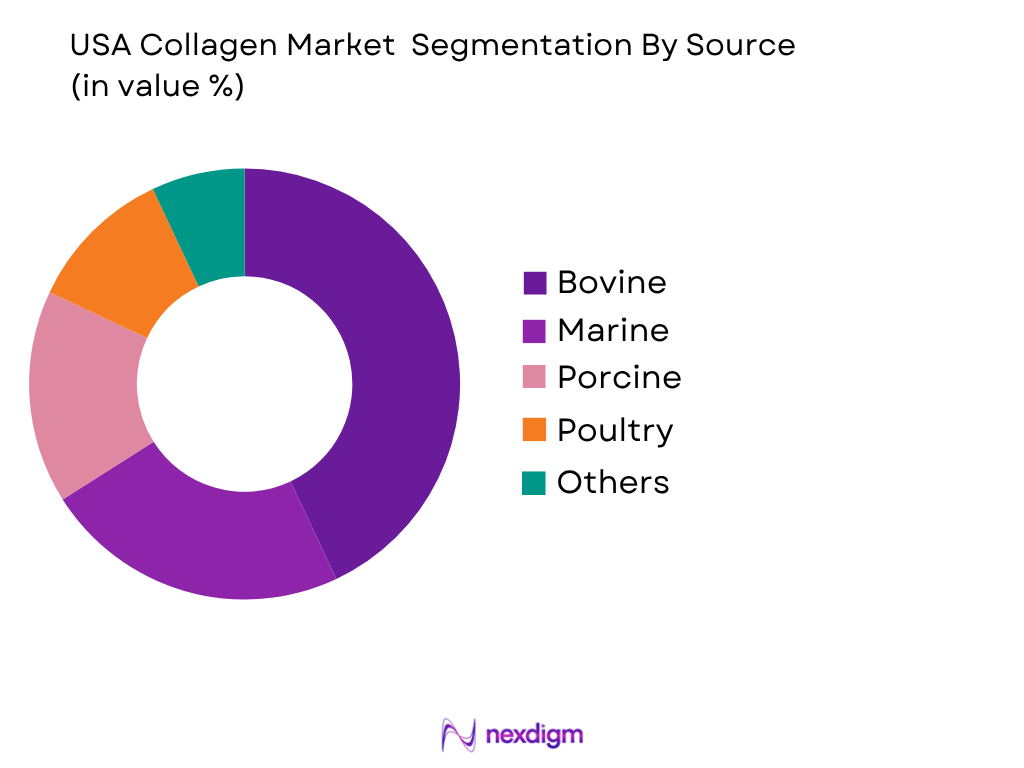

The USA collagen market is segmented by source into bovine, marine, porcine, poultry and other sources. Recently, bovine collagen has a dominant market share in the USA under the source segmentation because of its abundant domestic cattle-linked raw material availability, lower cost compared with marine collagen, high suitability for hydrolyzed peptide production and widespread acceptance in food, nutraceutical and pharmaceutical applications. Bovine collagen is used extensively in powder supplements, gummies, capsules, protein-enriched foods, gelatin applications and medical-grade material streams. The segment benefits from established procurement channels for cow hides, bones and cartilage, allowing suppliers to maintain larger-volume production and competitive pricing. It is also preferred by brands targeting joint health, skin elasticity, bone density and sports recovery claims because bovine-derived Type I and Type III collagen can be positioned across multiple wellness use cases. Grand View Research identifies bovine as the leading U.S. source segment.

By Product Type

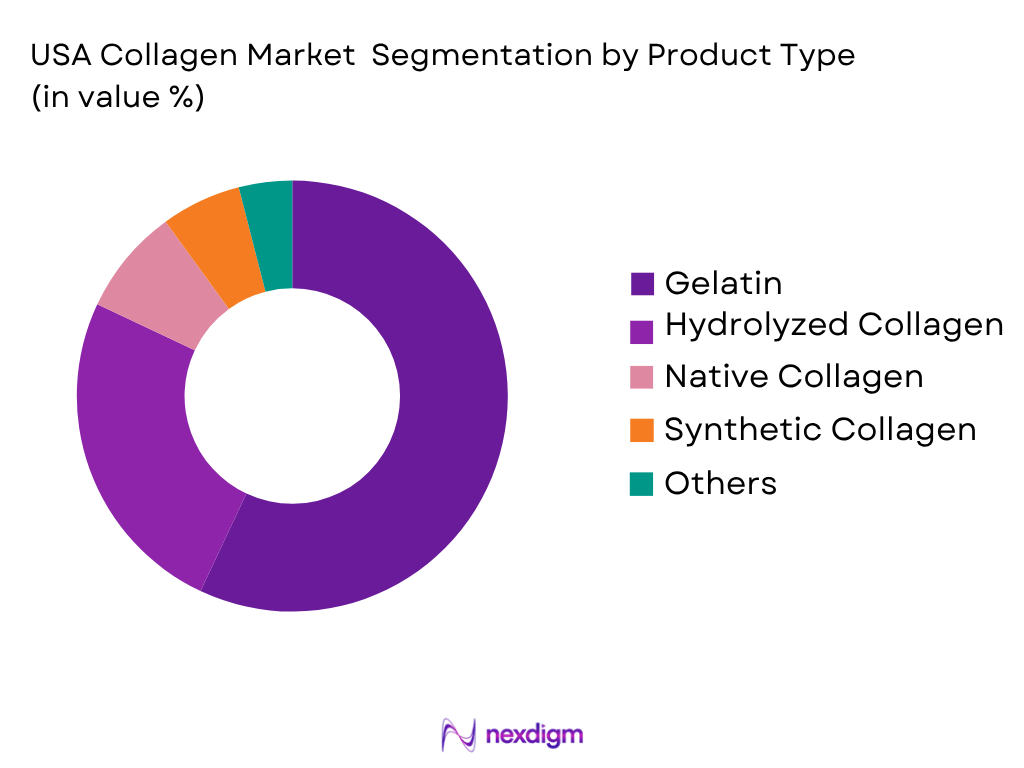

The USA collagen market is segmented by product type into gelatin, hydrolyzed collagen, native collagen, synthetic collagen and others. Recently, gelatin has a dominant market share under product type because it has long-standing use in confectionery, dairy, meat processing, capsules, gummies, pharmaceutical shells and food-texture applications. Gelatin’s functional benefits—gelling, stabilizing, thickening, foaming, binding and film-forming—make it commercially important beyond wellness supplements. It also serves both B2B food manufacturers and pharmaceutical companies, creating a broader demand base than premium collagen peptides alone. The segment is supported by large-scale animal by-product processing and established regulatory familiarity in food and pharma supply chains. Grand View Research valued the U.S. gelatin segment at USD 1,575.6 million, making it the largest product category within the U.S. collagen market.

Competitive Landscape

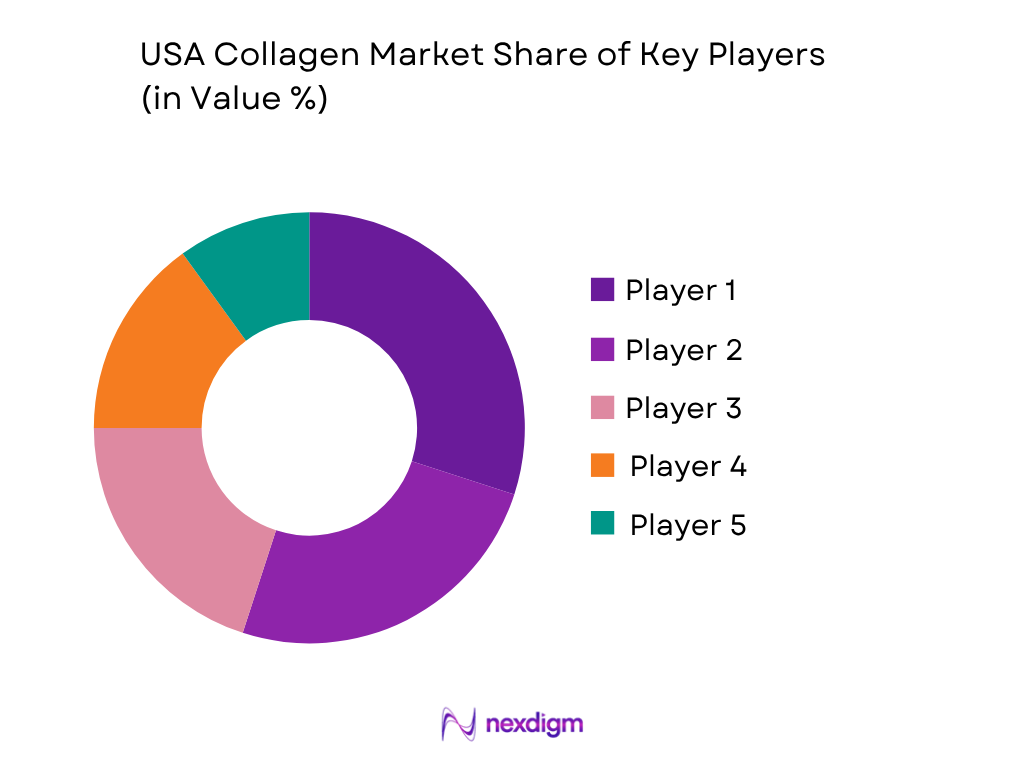

The USA collagen market is moderately consolidated at the B2B ingredient level and more fragmented at the branded supplement level. Large global ingredient companies such as Rousselot, GELITA, PB Leiner, Nitta Gelatin and Darling Ingredients influence supply through collagen peptide, gelatin and biomaterial capabilities, while consumer-facing brands compete through source claims, clinical positioning, flavor systems, Amazon ranking, retail distribution and subscription-based D2C sales. Grand View Research lists Rousselot, GELITA, Sterling Gelatin, Croda International, Collagen Matrix and JBS among key U.S. market participants.

| Company | Establishment Year | Headquarters | Collagen Portfolio | Main Source Focus | Application Coverage | U.S. Market Role | Certification/Quality Positioning | Strategic Strength |

| Rousselot / Darling Ingredients | 1891 | Irving, Texas / Son, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| GELITA AG | 1875 | Eberbach, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| PB Leiner / Tessenderlo Group | 1870s | Vilvoorde, Belgium | ~ | ~ | ~ | ~ | ~ | ~ |

| Nitta Gelatin Inc. | 1918 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Collagen Matrix Inc. | 1997 | Oakland, New Jersey | ~ | ~ | ~ | ~ | ~ | ~ |

USA Collagen Market Analysis

Growth Drivers

Rising Wellness Consumption and High Household Purchasing Capacity

The USA collagen market is supported by a large consumer economy where wellness, beauty-from-within, joint health and protein-enriched nutrition products have broad commercial relevance. The World Bank reports U.S. GDP at USD 28.75 trillion and GDP per capita at USD 84,534.0 for 2024, indicating strong purchasing capacity for discretionary health and wellness products such as collagen powders, capsules, gummies and functional beverages. The U.S. Bureau of Labor Statistics reports average annual consumer-unit expenditure of USD 78,535 and average income before taxes of USD 104,207 in 2024, creating a strong affordability base for premium supplement formats. The collagen category benefits because products are positioned across beauty, active aging, sports recovery and preventive wellness rather than only clinical nutrition. BEA data also shows U.S. pharmaceutical-product personal consumption expenditure at USD 668.973 billion in 2024 and USD 720.219 billion in 2025, reflecting continued household and healthcare-linked spending on ingestible health products.

Aging Population Expanding Demand for Joint, Bone and Skin Support

The USA collagen market is strongly driven by the aging population because collagen supplements are marketed around joint mobility, skin elasticity, bone support, muscle recovery and healthy-aging routines. The U.S. Census Bureau reports that the population aged 65 years and older reached 61.2 million in 2024, while the population under age 18 reached 73.1 million in the same period. This demographic base is directly relevant to collagen because older consumers are more likely to seek products associated with mobility maintenance, cartilage support, bone health and skin aging. The healthcare context also supports the market: CMS reports national health expenditure at USD 5.3 trillion and per-person health expenditure at USD 15,474 in 2024, indicating a large health-focused consumption environment. Collagen brands benefit from this ecosystem by positioning Type I and Type III collagen for skin and bone support, and Type II collagen for cartilage and mobility applications. The aging population also strengthens demand from practitioner channels, pharmacies, senior-wellness programs and functional nutrition brands.

Market Challenges

Tight Bovine Raw Material Availability and Feedstock Dependence

The USA collagen market faces a supply-side challenge because bovine collagen depends heavily on cattle-linked raw materials such as hides, bones and connective tissues. USDA NASS reports 87.2 million cattle and calves on U.S. farms as of January 1, 2024. The same USDA series shows 86.7 million cattle and calves as of January 1, 2025, and 86.2 million as of January 1, 2026, showing a continued narrowing of the domestic livestock base used by downstream hide, gelatin and collagen processors. USDA also reports the U.S. calf crop at 32.9 million head and cattle on feed at 13.8 million head in 2026, which matters for long-term raw material availability. This creates procurement pressure for bovine collagen suppliers because supplement, food, gelatin and pharmaceutical users all compete for traceable animal-derived feedstock. The challenge is market-specific because bovine collagen is central to hydrolyzed peptides, gelatin, capsules, gummies and functional food formulations in the United States.

Regulatory Burden Around Supplement Claims, Labeling and Manufacturing Controls

The USA collagen market faces a compliance challenge because collagen products are often sold with skin, joint, hair, nail, bone and recovery claims that must remain within permitted dietary supplement claim boundaries. FDA states that structure/function claims are not pre-approved, but manufacturers must submit claim notification to FDA no later than 30 days after marketing a dietary supplement with the claim. This is important for collagen brands because claims such as “supports joint health” or “supports skin elasticity” require substantiation and cannot imply disease treatment. FDA also regulates dietary supplements separately from conventional foods and drug products under DSHEA, covering both finished dietary supplement products and dietary ingredients. Manufacturing requirements add another operational burden: 21 CFR Part 111 applies to firms that manufacture, package, label or hold dietary supplements, including imported supplements offered in U.S. states and territories. For food-format collagen, FDA’s CGMP framework under 21 CFR Part 117 applies to human food manufacturing and preventive controls.

Market Opportunities

Expansion in Functional Food, Beverage and Everyday Nutrition Formats

The USA collagen market has a strong opportunity in functional foods and beverages because collagen is increasingly used beyond traditional capsules and powders. BEA reports total U.S. personal consumption expenditure increased by USD 156.1 billion in May 2026, while spending on goods increased by USD 13.6 billion in the same month, indicating sustained consumer activity across goods categories where functional nutrition products are sold. The BLS consumer expenditure dataset shows food-at-home expenditure of USD 6,224 per consumer unit and meats, poultry, fish and eggs expenditure of USD 1,414 in 2024, showing continued household engagement with protein-linked food categories. This supports collagen’s future growth in ready-to-drink beverages, coffee creamers, protein bars, fortified snacks, gummies and clean-label food systems. USDA ERS also maintains food-availability data for several hundred commodities moving through U.S. marketing channels, which supports formulation planning for food manufacturers using collagen as a gelling, stabilizing, binding or protein-fortification ingredient.

Growth in Medical, Pharmaceutical and Regenerative Collagen Applications

The USA collagen market has a future opportunity in medical-grade collagen because collagen is used in wound care, dental membranes, hemostatic products, tissue matrices, drug delivery systems and pharmaceutical gelatin applications. CMS reports U.S. national health expenditure at USD 5.3 trillion and Medicare expenditure at USD 1,118.0 billion in 2024, creating a large healthcare ecosystem for biomaterials, surgical products and pharmaceutical inputs. Private health insurance spending reached USD 1,644.6 billion, while out-of-pocket spending reached USD 556.6 billion in 2024, supporting demand across clinical, pharmacy and patient-paid healthcare channels. BEA reports pharmaceutical-product personal consumption expenditure of USD 668.973 billion in 2024 and USD 720.219 billion in 2025, reinforcing the opportunity for gelatin capsules, collagen-based delivery materials and regulated health products. FDA oversight of medical devices, drugs, biologics, foods and cosmetics also creates a defined regulatory pathway for companies that can meet documentation, quality and sterility requirements.

Future Outlook

The USA collagen market is expected to expand steadily as collagen moves from a niche supplement ingredient into mainstream wellness, functional food, beauty nutrition and medical biomaterial applications. Forecast demand is projected to grow from USD 2.73 billion to USD 8.44 billion, reflecting a CAGR of 11.9% over the long-term outlook period, with bovine and gelatin remaining core revenue anchors. Future growth will be supported by higher consumption of powders, gummies, ready-to-drink collagen beverages, multi-collagen blends, marine collagen beauty products, Type II joint-health formats and collagen-based medical matrices. The strongest premiumization will come from grass-fed bovine claims, sustainable marine sourcing, clinical substantiation, third-party testing, clean-label positioning and animal-free recombinant collagen development. The market will also benefit from functional food fortification and pharmaceutical use of gelatin. Collagen’s role as a gelling, emulsifying and binding ingredient allows it to maintain relevance in confectionery, capsules, gummies, meat processing and clean-label food systems, while hydrolyzed collagen peptides will continue to gain traction in beauty, sports recovery and healthy-aging routines.

Major Players

- Rousselot S.A.S. / Darling Ingredients

- GELITA AG

- PB Leiner / Tessenderlo Group

- Nitta Gelatin Inc.

- Collagen Matrix Inc.

- JBS S.A.

- Croda International Plc

- Sterling Gelatin

- Weishardt Holding SA

- Lapi Gelatine S.p.A.

- Gelnex

- Vital Proteins / Nestlé Health Science

- Great Lakes Wellness

- Sports Research

- Ancient Nutrition

Key Target Audience

- Collagen ingredient manufacturers

- Nutraceutical and dietary supplement brands

- Functional food and beverage manufacturers

- Pharmaceutical capsule and excipient manufacturers

- Cosmetic and nutricosmetic brands

- Medical device and regenerative medicine companies

- Investments and venture capitalist firms

- Government and regulatory bodies: U.S. Food and Drug Administration, U.S. Department of Agriculture, Federal Trade Commission, National Institutes of Health Office of Dietary Supplements

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map covering collagen raw material suppliers, gelatin manufacturers, peptide processors, supplement brands, food manufacturers, pharmaceutical users, medical device companies, retailers and regulators. Key variables include collagen source, product type, application, form factor, pricing, grade, channel and regulatory compliance requirements.

Step 2: Market Analysis and Construction

Historical market data is compiled through published market research, company disclosures, ingredient-level revenue mapping, trade information and channel-level checks. The analysis includes assessment of gelatin consumption, hydrolyzed peptide demand, supplement penetration, B2B ingredient pricing, retail SKU movement and medical-grade collagen usage.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through discussions with ingredient suppliers, supplement formulators, contract manufacturers, distributors, food technologists, beauty supplement brands and medical biomaterial specialists. These consultations are used to test assumptions around source dominance, product pricing, channel preference, substitution risk and demand acceleration.

Step 4: Research Synthesis and Final Output

The final stage synthesizes top-down market validation with bottom-up demand estimates across source, product type, application and channel. Outputs are cross-checked against credible market publications, regulatory sources and company positioning to produce a validated view of market size, segmentation, competition, risks and future growth potential.

- Executive Summary

- Research Methodology (Market Definition, Collagen Scope, Ingredient Classification, Primary Research Interviews, Supplier Validation, Channel Checks, SKU Benchmarking, Bottom-Up Demand Mapping, Top-Down Industry Validation, Import-Export Review, Regulatory Screening, Forecast Assumptions)

- Definition and Scope

- Market Genesis and Evolution

- Collagen Value Chain Overview

- Business Cycle and Demand Seasonality

- Supply Chain Mapping

- Growth Drivers (Beauty-from-Within, Active Aging, Sports Recovery, Protein Fortification, Medical Biomaterials, Pet Humanization, E-Commerce Penetration)

- Market Challenges (Raw Material Price Volatility, Animal-Origin Concerns, Allergen Risk, Claim Substantiation, Private Label Competition, Clinical Evidence Variability)

- Market Opportunities (Animal-Free Collagen, Personalized Nutrition, Women’s Health, Sports Medicine, Medical-Grade Collagen, Pet Supplements, Clean Label Formulations)

- Market Trends (Multi-Collagen Blends, Clean Label, Third-Party Testing, Marine Premiumization, Gummy Growth, D2C Subscriptions, Influencer-Led Education)

- SWOT Analysis

- Porter’s Five Forces

- PESTLE Analysis

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Product Type (In Value %)

Hydrolyzed Collagen Peptides

Gelatin

Native Collagen

Undenatured Type II Collagen

- By Application (In Value %)

Nutraceuticals and Dietary Supplements

Food and Beverage

Cosmetics and Personal Care

Healthcare and Pharmaceuticals

Biomedical and Regenerative Medic - By Distribution Channel (In Value %)

B2B Ingredient Supply

Contract Manufacturing and Private Label

Supermarkets and Mass Retail

Pharmacies and Drugstores

Online Marketplaces - By Region (In Value %)

West

Northeast

Midwest

South

- Market Share Analysis of Major Players (Ingredient Revenue, Branded Supplement Sales, B2B Supply Share, Product Portfolio Breadth, Channel Reach)

- Cross Comparison Parameters (Collagen Source Portfolio, Product Format Portfolio, Collagen Type Coverage, Application Coverage, Certifications & Compliance, U.S. Distribution Reach, Clinical/Claims Support, Pricing & Margin Positioning)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Rousselot / Darling Ingredients

GELITA

PB Leiner / Tessenderlo Group

Nitta Gelatin

Weishardt Group

Gelnex

Lapi Gelatine

JBS

Vital Proteins / Nestlé Health Science

Great Lakes Wellness

Sports Research

Ancient Nutrition

NeoCell

BUBS Naturals

Collagen Matrix

- Nutraceutical Brand Demand Analysis

- Food and Beverage Manufacturer Demand Analysis

- Cosmetics and Personal Care Demand Analysis

- Healthcare and Biomedical Demand Analysis

- Retail Consumer Demand Analysis

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now