Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA combine harvester market recorded a market size of approximately USD ~ billion, supported by replacement demand cycles and sustained mechanization intensity across large grain operations. The market is driven by high harvesting capacity requirements in corn and soybean cultivation zones, rising labor scarcity, and increasing adoption of precision harvesting technologies such as yield monitoring and automated guidance systems, which improve operational efficiency and reduce harvest losses across large-scale farming enterprises.

Dominance in the USA combine harvester market is concentrated in Midwest agricultural states including Iowa, Illinois, Nebraska, Minnesota, and Kansas, where extensive grain acreage and large farm sizes necessitate high-capacity harvesting machinery. These regions benefit from advanced dealer networks, strong agricultural financing infrastructure, and proximity to manufacturing clusters in Wisconsin and Illinois. Favorable logistics, established service ecosystems, and high mechanization intensity reinforce regional leadership in combine harvester utilization and procurement activity.

Market Segmentation

By Product Type

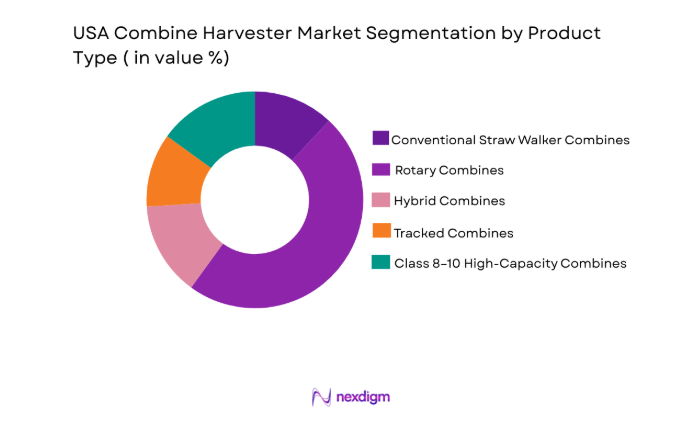

USA combine harvester market is segmented by product type into conventional straw walker combines, rotary combines, hybrid combines, tracked combines, and class 8–10 high-capacity combines. Recently, rotary combines has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rotary combines offer superior throughput, lower grain loss in corn and soybean harvesting, and better adaptability to high-moisture crops prevalent in major grain belts. Leading manufacturers emphasize rotary platforms in premium product lines, supported by dealer familiarity and established service capabilities. Larger farms prioritize rotary combines for continuous harvesting efficiency and reduced downtime during narrow harvest windows. Technology integration including yield sensing and automation is also more advanced in rotary platforms. Financing availability for high-capacity machines further reinforces their adoption across commercial operations.

By Platform Type

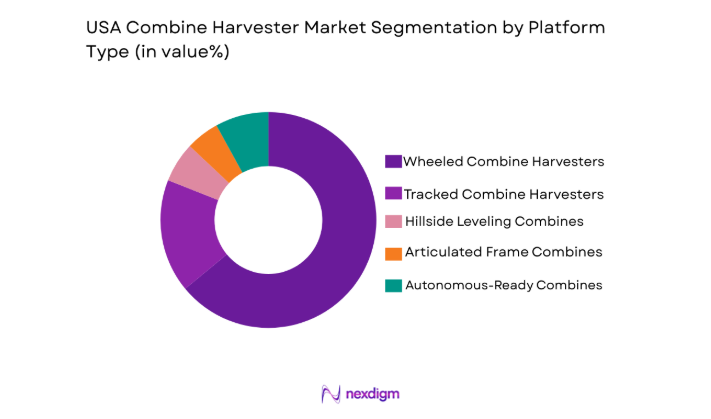

USA combine harvester market is segmented by platform type into wheeled combine harvesters, tracked combine harvesters, hillside leveling combines, articulated frame combines, and autonomous-ready combines. Recently, wheeled combine harvesters has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Wheeled platforms align with the flat terrain and large contiguous fields across major grain belts, enabling efficient high-speed harvesting and easy transport between fields and storage sites. Extensive dealer inventories, spare parts availability, and operator familiarity further reinforce wheeled platform preference. Lower acquisition and maintenance costs compared with tracked or specialized platforms improve lifecycle economics for farms. Financing, resale liquidity, and compatibility with existing headers and grain logistics systems also sustain wheeled platform dominance across commercial grain operations.

Competitive Landscape

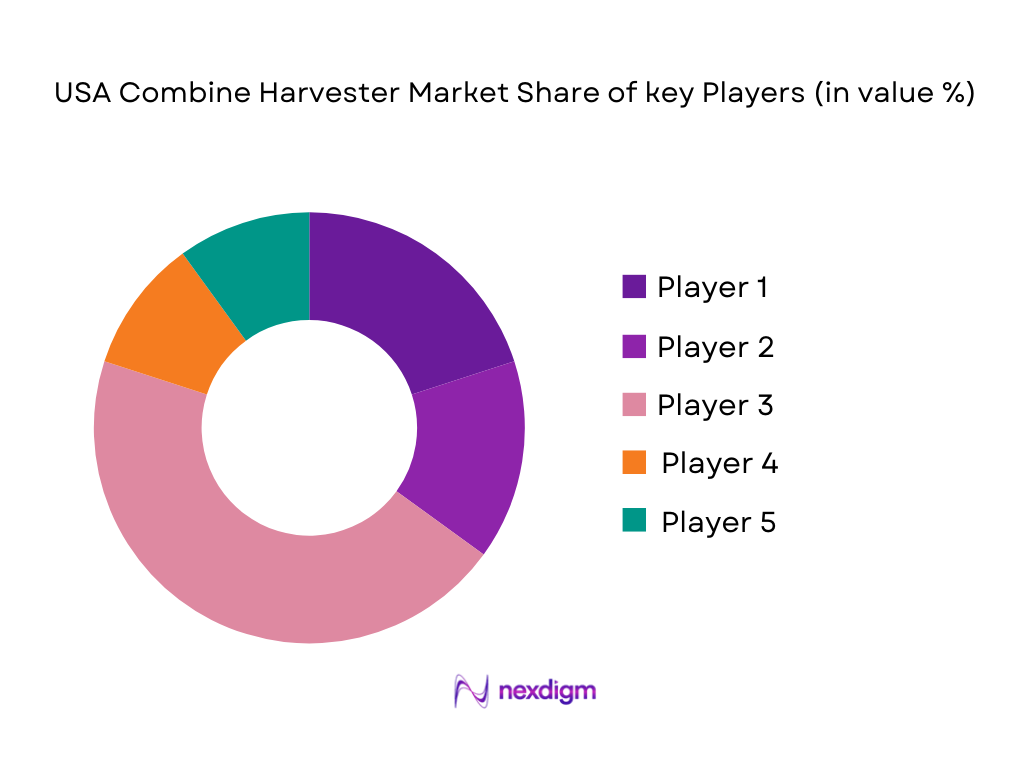

The USA combine harvester market exhibits high consolidation, dominated by a small number of multinational agricultural machinery manufacturers with extensive dealer networks and integrated precision agriculture ecosystems. Leading firms compete through harvesting capacity, automation features, reliability, and service coverage, while regional manufacturers focus on niche segments such as specialty crops or headers. Strong brand loyalty, installed fleet base, and financing programs reinforce market concentration and barriers to entry.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Strength |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~

|

|

| CNH Industrial (Case IH) | 1842 | UK/Netherlands | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial (New Holland) | 1895 | Italy | ~ | ~ | ~ | ~ | ~ |

| AGCO (Gleaner/Massey) | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

USA Combine Harvester Market Analysis

Growth Drivers

Expansion of large-scale grain farming operations in the USA

The structural shift toward larger commercial grain farms in the USA has intensified demand for high-capacity combine harvesters capable of efficiently harvesting extensive corn and soybean acreage within narrow agronomic windows, as farm consolidation has increased average farm sizes and reduced the number of operators available per hectare harvested. Larger farms prioritize productivity per machine hour, driving adoption of Class 8–10 combines with wide headers, high grain tank capacities, and automated harvesting features that reduce operator fatigue and maximize throughput across long harvest days. Replacement cycles are also accelerating because high-utilization farms accumulate operating hours faster, necessitating earlier fleet renewal to maintain reliability during critical harvest periods when weather risks can rapidly degrade crop quality and yield. Mechanization intensity has risen further due to persistent agricultural labor shortages, particularly seasonal skilled operators capable of managing harvesting machinery, pushing farms to invest in technologically advanced combines that simplify operation and enable fewer workers to manage larger harvested areas. Financial institutions and equipment manufacturers have expanded leasing, financing, and trade-in programs tailored to large-scale producers, lowering upfront capital barriers and enabling continuous fleet modernization across the commercial farming segment. Grain logistics infrastructure such as on-farm storage, grain carts, and transport systems has also scaled with farm expansion, allowing large combines to operate at full capacity without unloading delays, which reinforces the economic advantage of high-throughput machines. Precision agriculture integration within modern combines, including yield mapping and real-time crop sensing, enables large farms to optimize field management decisions, further strengthening the business case for advanced harvesting platforms. Agricultural policy support and crop insurance frameworks that incentivize productivity and risk mitigation have indirectly encouraged investment in efficient harvesting machinery across large grain-producing states. As farm consolidation continues, the economic necessity of maximizing harvested acreage per operator and per machine will sustain structural demand for high-capacity combines across the USA agricultural landscape.

Rising adoption of precision harvesting and automation technologies

The increasing integration of precision agriculture technologies into combine harvesters has significantly enhanced harvesting efficiency, grain quality preservation, and field data generation, making technologically advanced combines economically attractive to USA grain producers seeking to optimize yields and operational decision-making. Modern combines incorporate yield monitoring sensors, moisture detection, automated header height control, and machine-learning-assisted crop flow optimization systems that adjust threshing and separation parameters in real time based on crop conditions, reducing grain loss and improving harvest consistency across heterogeneous fields. Data generated during harvesting integrates with farm management platforms, enabling producers to analyze yield variability, soil performance, and input effectiveness, thereby transforming the combine from a harvesting machine into a critical agronomic data collection asset within digital farming ecosystems. Automation features such as auto-steering, path optimization, and predictive maintenance diagnostics reduce operator skill requirements and downtime risk, addressing labor scarcity while increasing machine utilization efficiency during time-sensitive harvest seasons. Equipment manufacturers have expanded telematics connectivity, allowing remote monitoring, software updates, and service diagnostics that minimize breakdown duration and enhance lifecycle productivity of harvesting fleets across dispersed farm locations. Farms adopting precision harvesting technologies often achieve improved grain quality and reduced post-harvest losses, strengthening revenue outcomes and reinforcing reinvestment in advanced machinery. Government-supported digital agriculture initiatives and connectivity expansion in rural regions have further enabled adoption of telematics-enabled combines and cloud-based agronomic analytics platforms. Dealer networks increasingly provide technology training and support services, lowering adoption barriers and accelerating technology penetration within the installed combine fleet. As precision agriculture becomes central to profitability and sustainability in grain farming, technologically advanced combine harvesters will remain a primary investment priority across the USA agricultural sector.

Market Challenges

High capital acquisition and ownership cost of advanced combine harvesters

The purchase price of modern high-capacity combine harvesters equipped with precision agriculture technologies represents a substantial capital investment for USA grain producers, often exceeding the financial capacity of small and mid-sized farms and creating significant barriers to ownership despite productivity benefits. Financing costs, interest rate fluctuations, and depreciation risks further increase total ownership expenses, particularly during periods of volatile commodity prices that reduce farm cash flow and delay machinery investment decisions. High acquisition costs are compounded by the need for complementary equipment such as headers, grain carts, and transport infrastructure, increasing overall harvesting system investment requirements beyond the combine itself. Maintenance and service expenses for technologically advanced combines are also elevated due to complex electronic systems, sensors, and specialized components that require skilled technicians and OEM parts, raising lifecycle operating costs relative to older machines. Seasonal utilization patterns in grain harvesting limit annual operating hours compared to other agricultural machinery, which reduces capital productivity and extends payback periods, making investment decisions highly sensitive to farm size and harvest acreage. Used equipment markets partially mitigate acquisition barriers but often involve trade-offs in technology capability, fuel efficiency, and reliability, constraining productivity improvements for cost-sensitive farms. Economic uncertainty in agricultural markets, including crop price volatility and input cost fluctuations, further discourages high-value machinery investment during downturn periods. Manufacturers have introduced leasing and financing programs to address affordability, yet many farms remain hesitant to commit to high-cost assets amid uncertain revenue outlooks. The persistent gap between combine technology capability and farm financial capacity remains a structural constraint on broader fleet modernization across the USA combine harvester market.

Seasonal utilization constraints and labor skill requirements in harvesting operations

Combine harvesters in the USA agricultural system operate primarily during limited harvest windows for major crops such as corn and soybeans, resulting in relatively low annual utilization compared with their high capital cost and creating economic inefficiencies in ownership models, especially for smaller farms with limited acreage. Weather variability can further compress harvest periods, forcing farms to operate machines intensively for short durations while remaining idle for extended off-season periods, reducing overall asset productivity and increasing cost per harvested hectare. Skilled operator requirements for advanced combines, including knowledge of machine settings, crop flow optimization, and precision technology use, create additional labor constraints in rural regions where agricultural workforce availability is declining and aging. Training requirements for modern harvesting technology increase operational complexity, and insufficient operator expertise can lead to grain losses, machine wear, and reduced harvesting efficiency, undermining expected productivity gains from advanced equipment.

Opportunities

Integration of autonomous harvesting systems and AI-driven field operations

Autonomous and semi-autonomous combine harvesting technologies present a transformative opportunity in the USA combine harvester market by addressing labor shortages, improving harvesting precision, and enabling continuous machine operation with reduced human intervention across large-scale grain farms. Advances in machine vision, LiDAR sensing, and AI-based crop detection systems allow combines to navigate fields, adjust harvesting parameters, and coordinate with grain carts autonomously, reducing reliance on skilled operators and minimizing human error in harvesting processes. Autonomous systems can optimize harvesting routes, minimize overlap, and maintain consistent throughput, improving fuel efficiency and reducing grain losses compared with manual operation under variable field conditions. Integration with digital farm management platforms enables coordinated fleet harvesting where multiple machines operate collaboratively across large fields, maximizing harvested acreage per day and reducing weather-related harvest risks. Remote supervision models allow a single operator to oversee multiple autonomous machines, increasing labor productivity and reducing workforce constraints in rural agricultural regions. Early adoption by large commercial farms demonstrates productivity gains and cost efficiencies, encouraging further technological investment and scaling within the agricultural machinery sector. Manufacturers are investing heavily in autonomous combine development, supported by partnerships with technology firms specializing in robotics and artificial intelligence, accelerating commercialization pathways. Regulatory acceptance of autonomous agricultural machinery operation in controlled farm environments is comparatively favorable relative to public-road automation, facilitating deployment. As automation technology matures and costs decline, autonomous harvesting systems are expected to become a major growth segment within the USA combine harvester market, reshaping operational models and equipment demand patterns.

Expansion of equipment-as-a-service and cooperative harvesting models

Alternative ownership and utilization models such as equipment leasing, harvesting-as-a-service, and cooperative machinery sharing are emerging as significant opportunities within the USA combine harvester market by improving asset utilization and reducing capital barriers for farms unable to justify individual ownership of high-cost combines. Leasing and subscription-based harvesting services allow farms to access advanced harvesting technology during peak seasons without large upfront investment, aligning machinery costs with operational revenue cycles and improving financial flexibility in volatile agricultural markets. Custom harvesting contractors equipped with high-capacity combines provide scalable harvesting capacity across multiple farms, increasing machine utilization rates and spreading capital costs over larger harvested acreage, which enhances economic efficiency compared with individual ownership. Agricultural cooperatives are increasingly investing in shared combine fleets to serve member farms, particularly in regions with moderate farm sizes where individual machine ownership is inefficient, enabling access to modern harvesting technology and professional operation services. Digital scheduling and fleet management platforms improve coordination and availability of shared harvesting equipment, reducing delays and increasing operational reliability during narrow harvest windows. Manufacturers and dealers are exploring service-based business models that bundle machinery, maintenance, and technology support into usage-based contracts, creating recurring revenue streams while lowering adoption barriers for farmers. Financing institutions support these models through structured leasing and cooperative lending programs tailored to agricultural machinery assets. As economic pressures and technology costs rise, service-oriented harvesting models are expected to expand significantly, creating new revenue channels and reshaping ownership patterns within the USA combine harvester market.

Future Outlook

The USA combine harvester market is expected to experience steady technological evolution over the next five years driven by automation, precision agriculture integration, and digital farm management connectivity. High-capacity and autonomous-ready combines will gain traction as farms scale operations and labor constraints intensify. Regulatory support for emissions-compliant machinery and digital agriculture adoption will further encourage fleet modernization. Demand will remain strongest in major grain belts where large-scale mechanized harvesting remains essential to crop productivity and profitability.

Major Players

- John Deere

- Case IH

- New Holland Agriculture

- CLAAS

- AGCO Corporation

- Gleaner

- Massey Ferguson

- Fendt

- Kubota

- Versatile

- Sampo Rosenlew

- Oxbo International

- Mac DonIndustries

- Honey Bee Manufacturing

- Kincaid Equipment Manufacturing

Key Target Audience

- Agricultural equipment manufacturers

- Grain farm operators

- Agricultural cooperatives

- Custom harvesting service providers

- Farm equipment dealers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural finance institutions

Research Methodology

Step 1: Identification of Key Variables

Key market variables including combine sales, installed fleet, replacement cycles, crop acreage, and mechanization intensity were identified through agricultural statistics and machinery databases. Technology adoption indicators such as precision agriculture penetration and automation readiness were also mapped. Regional demand drivers across grain-producing states were incorporated to define market structure.

Step 2: Market Analysis and Construction

Market sizing was constructed using equipment shipment data, average selling prices, and installed base estimates across combine classes and regions. Segmentation was derived from product configurations, mobility systems, and end-user structures. Value chain analysis incorporated OEM production, dealer distribution, financing, and service ecosystems across the USA agricultural machinery sector.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market models were validated through consultation with agricultural machinery dealers, farm equipment analysts, and harvesting contractors. Technology adoption trends and replacement cycle assumptions were cross-checked with OEM product portfolios and farm mechanization studies. Regional demand assumptions were aligned with crop production and farm structure data.

Step 4: Research Synthesis and Final Output

Validated datasets were synthesized into market estimates, segmentation shares, and competitive structure assessments. Insights on growth drivers, challenges, and opportunities were integrated with technological and structural trends in USA grain farming. Final outputs were structured to support strategic decision-making for stakeholders in the combine harvester ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of large scale commercial grain farming operations

Adoption of precision agriculture and yield optimization technologies

Replacement demand from aging combine fleets

Rising labor scarcity accelerating mechanization intensity

Government supported farm productivity programs - Market Challenges

High capital cost of advanced combine harvesters

Volatility in farm incomes linked to commodity prices

Supply chain disruptions in agricultural machinery components

Skilled technician shortages for servicing complex machines

Seasonal utilization leading to low asset productivity - Market Opportunities

Integration of autonomous harvesting capabilities

Growth in leasing and pay per use harvesting models

Demand for high capacity machines in expanding corn and soybean belts - Trends

Shift toward Class 9–10 high throughput combines

Rapid adoption of telematics and remote diagnostics

Header automation and crop sensing integration

Electrification of auxiliary systems in harvesters

Data driven harvest optimization platforms - Government Regulations & Defense Policy

EPA Tier 4 Final emission compliance requirements

USDA farm mechanization and productivity incentives

Occupational safety standards for agricultural machinery - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Straw Walker Combines

Rotary Combines

Hybrid Combines

Tracked Combines

High-Capacity Combines - By Platform Type (In Value%)

Wheeled Combine Harvesters

Tracked Combine Harvesters

Hillside Levelling Combines

Articulated Frame Combines

Autonomous Ready Combines - By Fitment Type (In Value%)

Factory Installed Precision Harvesting Systems

Dealer Installed Retrofit Kits

Telematics Enabled Combines

Header Integrated Combines

Aftermarket Upgraded Combines - By End-user Segment (In Value%)

Large Commercial Grain Farms

Family-Owned Mid Size Farms

Custom Harvesting Contractors

Agricultural Cooperatives

Research and Institutional Farms - By Procurement Channel (In Value%)

Authorized Dealer Networks

Direct OEM Sales

Agricultural Equipment Auctions

Leasing and Financing Providers

Used Equipment Dealers - By Material / Technology (in Value %)

High Strength Structural Steel Frames

Advanced Threshing Rotor Technology

Precision Yield Monitoring Systems

Telematics and Remote Diagnostics

Autonomous Guidance and AI Vision Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Harvesting Capacity, Engine Power Range, Grain Tank Size, Automation Level, Precision Farming Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere

Case IH

New Holland Agriculture

AGCO Corporation

CLAAS of America

Gleaner

Fendt

Massey Ferguson

Kubota North America

Versatile

Sampo Rosenlew North America

Oxbo International

Kincaid Equipment Manufacturing

MacDon Industries

Honey Bee Manufacturing

- Large farms prioritize high capacity and automation ready combines

- Custom harvesters demand durable machines with rapid serviceability

- Mid size farms prefer financing and leasing based procurement

- Cooperatives emphasize shared utilization and fleet management

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now