Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Commercial Aircraft Aftermarket Outlook to 2035 market current size stands at around USD ~ million, reflecting sustained demand for maintenance, repair, and overhaul services across commercial fleets. Ongoing fleet utilization patterns, component replacement cycles, and compliance-driven maintenance events underpin steady aftermarket activity. Parts availability, repair turnaround time, and service network coverage continue to shape procurement decisions. Contractual service models and long-term maintenance agreements influence operator preferences, while technical documentation access and certification frameworks affect competitive positioning across the service ecosystem.

Activity is concentrated around major aviation hubs such as Dallas–Fort Worth, Atlanta, Miami, Chicago, Los Angeles, and Seattle, supported by dense airline operations, engine and component repair clusters, and established logistics infrastructure. These regions benefit from mature hangar capacity, proximity to aircraft fleets, skilled technician pools, and regulatory familiarity. Policy environments that prioritize safety compliance and domestic repair station certification reinforce localized service ecosystems, while cargo corridors and coastal gateways concentrate heavy maintenance and parts distribution activities.

Market Segmentation

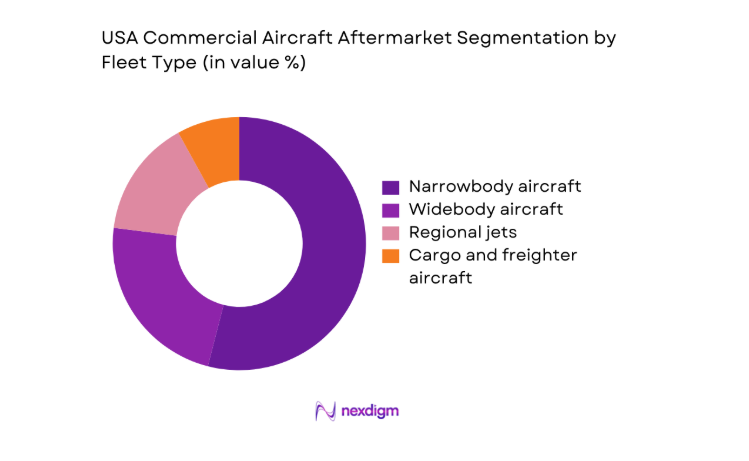

By Fleet Type

Narrowbody aircraft dominate aftermarket demand due to high-frequency short-haul operations, dense domestic route networks, and elevated flight cycle accumulation. These aircraft experience accelerated wear on landing gear, brakes, and avionics, increasing line maintenance and component exchange volumes. Widebody aircraft generate concentrated heavy maintenance demand linked to structural checks and engine shop visits, while regional jets contribute steady base-load activity through commuter networks. Freighter fleets intensify structural modification and cargo handling system maintenance, supported by strong logistics utilization across hub-and-spoke cargo routes and integrated express networks.

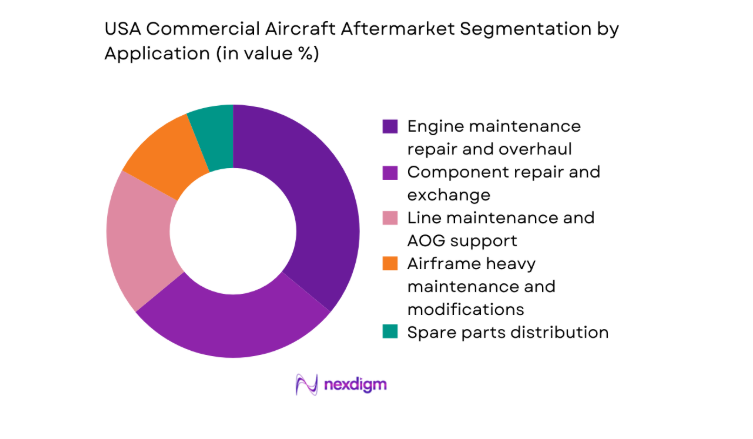

By Application

Engine maintenance repair and overhaul represents the most complex and resource-intensive application, driven by life-limited part cycles, performance restoration events, and compliance with airworthiness directives. Component repair and exchange sustains recurring demand due to high-failure-rate rotables across avionics, hydraulics, and environmental control systems. Line maintenance supports daily operational continuity through scheduled checks and AOG response, while airframe heavy maintenance concentrates on structural inspections and cabin modifications. Spare parts distribution underpins the ecosystem through inventory pooling, logistics coordination, and turnaround time optimization across operator networks.

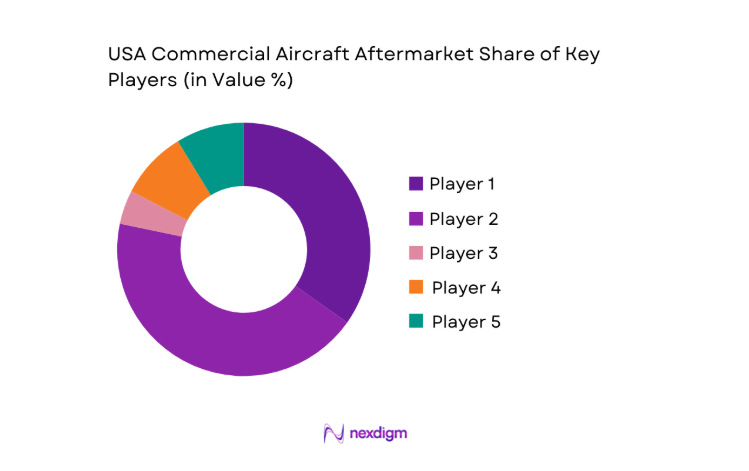

Competitive Landscape

The competitive landscape reflects a mix of airline-affiliated maintenance organizations, independent service providers, and OEM-aligned support entities. Competition is shaped by certification breadth, turnaround reliability, digital maintenance integration, and depth of component capabilities, with regional proximity to fleet hubs influencing service adoption.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Boeing Global Services | 2017 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| GE Aerospace | 1917 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| RTX Pratt & Whitney | 1925 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Lufthansa Technik | 1954 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| AAR Corp. | 1951 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

USA Commercial Aircraft Aftermarket Market Analysis

Growth Drivers

Expansion of narrowbody fleets driven by domestic route growth

Domestic air travel volumes in the United States recovered to 860 million passenger boardings during 2024, supported by 19 major hub airports handling more than 30 million passengers each. Fleet planners added 412 narrowbody aircraft into active service across 2024 and 2025, increasing average daily flight cycles per aircraft to 5.6 on high-density routes. FAA traffic operations reached 45 million movements in 2024, intensifying brake, tire, and avionics replacement frequencies. Higher utilization rates elevate scheduled maintenance events, driving demand for line maintenance capacity, component exchange pools, and rapid turnaround support across domestic networks.

Rising average fleet age increasing heavy maintenance events

The average age of active commercial aircraft in the United States reached 13.2 years in 2025, compared with 11.8 years in 2022, increasing the frequency of structural inspections and corrosion mitigation tasks. FAA records show 18,400 heavy maintenance checks conducted across large transport category aircraft during 2024, reflecting elevated D-check and C-check volumes. Deferred retirements added 286 older airframes into continued service during 2024 and 2025, expanding demand for landing gear overhauls, wiring inspections, and cabin system refurbishments. Aging fleets require deeper maintenance packages, extending shop visit durations and raising component shop workloads nationwide.

Challenges

Skilled labor shortages in licensed A&P mechanics

The United States recorded 21,400 active airframe and powerplant technicians entering retirement eligibility by 2025, while training pipelines produced 12,600 newly certified technicians across 2024 and 2025. FAA-approved maintenance schools reported 9,300 graduates in 2024, insufficient to offset attrition across major hubs. Technician vacancy rates exceeded 14 across large maintenance bases in 2025, increasing overtime hours and maintenance backlogs. Workforce shortages lengthen turnaround times for heavy checks, constrain hangar throughput, and elevate compliance risks during peak demand periods. Competition for licensed personnel intensifies recruitment costs and delays service capacity expansions.

Supply chain disruptions for rotables and life-limited parts

Component lead times for selected rotables extended from 42 days in 2022 to 78 days in 2025 due to constrained machining capacity and material bottlenecks. FAA Parts Manufacturer Approval processing averaged 146 days in 2024, delaying alternate sourcing approvals. Inventory backorders affected 6,800 aircraft-on-ground incidents recorded by large carriers in 2024, up from 4,900 in 2022. Logistics congestion at five major cargo gateways added 3 to 5 days to inbound part delivery windows. Prolonged supply variability complicates maintenance scheduling, increases AOG exposure, and strains exchange pool availability across fleets.

Opportunities

Expansion of engine MRO capacity for LEAP and GTF platforms

The active installed base of next-generation narrowbody engines exceeded 6,400 units across U.S.-operated fleets by 2025, with shop visit intervals tightening after 3,200 flight cycles for early production batches. FAA certification of 11 additional engine test cells during 2024 expanded domestic throughput potential. Hangar expansions added 24 dedicated engine bays across three major maintenance clusters in 2025. Increased shop visit frequency and parts replacement cycles create sustained demand for engine disassembly, module repair, and performance restoration services, enabling capacity investments to capture rising maintenance volumes within domestic networks.

Aftermarket demand for used serviceable material

Aircraft retirements and part-out events supplied 1,120 airframes into dismantling channels across 2024 and 2025, increasing availability of serviceable components for legacy platforms. Component reuse cycles shortened average procurement lead times by 19 days in 2024 for avionics and hydraulic units. Regulatory acceptance of traceable used serviceable material supported 27 additional repair station approvals in 2025, expanding certified distribution networks. Operators increased pooling participation across 14 major hubs, reducing AOG exposure. Expanded part-out throughput and traceability systems create opportunities to stabilize supply for aging fleets under cost containment pressures.

Future Outlook

The market is expected to experience sustained operational intensity through 2030 and beyond, driven by high utilization of narrowbody fleets and prolonged service lives of in-service aircraft. Digital maintenance integration and predictive analytics adoption will continue to reshape maintenance planning. Domestic capacity expansions across engine and component shops are likely to rebalance turnaround timelines. Regulatory oversight will remain stringent, reinforcing compliance-driven service demand. Strategic partnerships across airlines and service providers are set to deepen ecosystem coordination.

Major Players

- Boeing Global Services

- GE Aerospace

- RTX Pratt & Whitney

- Lufthansa Technik

- AAR Corp.

- StandardAero

- Delta TechOps

- United Airlines Tech Ops

- American Airlines Tech Ops

- HAECO Americas

- STS Aviation Group

- Sabreliner Aviation

- FEAM Aero

- Air France Industries KLM Engineering & Maintenance

- Barnes Aerospace

Key Target Audience

- Commercial passenger airlines

- Cargo and logistics operators

- Aircraft leasing companies

- Independent maintenance, repair, and overhaul providers

- Parts distributors and inventory pooling organizations

- Investments and venture capital firms

- Federal Aviation Administration and U.S. Department of Transportation

- State-level aviation authorities and airport commissions

Research Methodology

Step 1: Identification of Key Variables

Fleet utilization intensity, maintenance interval thresholds, regulatory compliance cycles, and component failure patterns were mapped across domestic commercial operations. Variables reflected aircraft age profiles, route density, and shop visit frequencies across major hubs.

Step 2: Market Analysis and Construction

Operational indicators, maintenance event counts, and capacity availability were synthesized to construct service demand profiles. Application-level workflows were structured across engine, airframe, line maintenance, and component repair domains.

Step 3: Hypothesis Validation and Expert Consultation

Insights were validated through structured discussions with airline maintenance leadership, certified repair station managers, and regulatory compliance officers. Assumptions on utilization recovery and capacity constraints were stress-tested against operational benchmarks.

Step 4: Research Synthesis and Final Output

Findings were reconciled through cross-validation of operational indicators and service workflows. Scenario narratives were developed to reflect utilization normalization, capacity expansion pathways, and regulatory enforcement trajectories.

- Executive Summary

- Research Methodology (Market Definitions and scope boundaries for U.S. commercial aircraft MRO and parts aftermarket, Fleet and component-level taxonomy across airframe engine component and line maintenance segments, Bottom-up market sizing using fleet utilization flight cycles and maintenance event frequencies, Revenue attribution through parts consumption rates labor hours and MRO contract values)

- Definition and Scope

- Market evolution

- Usage and maintenance pathways

- Ecosystem structure

- Supply chain and distribution channels

- Regulatory environment

- Growth Drivers

Expansion of narrowbody fleets driven by domestic route growth

Rising average fleet age increasing heavy maintenance events

Growth in cargo operations and freighter conversions

FAA safety and compliance mandates increasing inspection cycles

Higher utilization rates post-pandemic normalization

Long-term service agreements by OEMs and MRO providers - Challenges

Skilled labor shortages in licensed A&P mechanics

Supply chain disruptions for rotables and life-limited parts

OEM parts pricing pressure and proprietary data access limits

Aircraft-on-ground events due to parts availability constraints

Capacity bottlenecks at U.S. MRO facilities

Regulatory certification timelines for new repair capabilities - Opportunities

Expansion of engine MRO capacity for LEAP and GTF platforms

Aftermarket demand for used serviceable material

Digital MRO platforms for predictive maintenance adoption

Growth in freighter conversion and P2F modification programs

Localization of component repair capabilities within the U.S.

Additive manufacturing for low-volume and legacy parts - Trends

Shift toward power-by-the-hour and integrated MRO contracts

Increasing use of aircraft health monitoring and analytics

Rising demand for used serviceable material in cost-sensitive fleets

Strategic partnerships between airlines and independent MROs

Investments in automation and robotics in hangar operations

Consolidation among independent MRO providers - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Narrowbody aircraft

Widebody aircraft

Regional jets

Cargo and freighter aircraft - By Application (in Value %)

Engine maintenance repair and overhaul

Airframe heavy maintenance and modifications

Line maintenance and AOG support

Component repair and exchange

Spare parts distribution - By Technology Architecture (in Value %)

Traditional scheduled maintenance programs

Power-by-the-hour and performance-based logistics

Predictive maintenance and digital MRO platforms

Additive manufacturing for spare parts

Condition-based monitoring systems - By End-Use Industry (in Value %)

Passenger airlines

Cargo and logistics operators

Aircraft lessors

Charter and ACMI operators

Government and public service operators - By Connectivity Type (in Value %)

Connected aircraft health monitoring systems

Non-connected maintenance operations

Real-time telematics and AHM platforms

Ground-based maintenance IT systems - By Region (in Value %)

Northeast

Midwest

South

West

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (fleet coverage, engine platform capability, FAA repair station certifications, turnaround time performance, geographic footprint in the U.S., pricing models and contract structures, digital MRO platform maturity, parts availability and exchange pool depth)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarketing

- Detailed Profiles of Major Companies

Boeing Global Services

GE Aerospace

RTX Pratt & Whitney

Lufthansa Technik

AAR Corp.

StandardAero

Delta TechOps

United Airlines Tech Ops

American Airlines Tech Ops

HAECO Americas

STS Aviation Group

Sabreliner Aviation

FEAM Aero

Air France Industries KLM Engineering & Maintenance

Barnes Aerospace

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now