Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA commercial aircraft materials market is valued at USD ~billion, driven by increasing demand for lightweight and fuel-efficient materials in the aviation industry. This growth is largely influenced by advancements in material science, which enable aircraft manufacturers to enhance performance, reduce operational costs, and meet stringent environmental regulations. The market also benefits from the ongoing modernization of the U.S. airline fleet and the increasing focus on improving aircraft efficiency through the adoption of composite materials and high-strength alloys.

The U.S. is a dominant player in the commercial aircraft materials market, owing to its robust aerospace sector and the presence of major aircraft manufacturers such as Boeing. With advanced research and development capabilities, coupled with a well-established infrastructure for manufacturing and testing, the U.S. leads in the production of high-performance materials. The strategic importance of the aviation sector to the economy further reinforces the country’s position as a global leader in commercial aircraft materials.

Market Segmentation

By Product Type:

The commercial aircraft materials market is segmented by system type into airframe materials, engine materials, landing gear materials, interior materials, and composites and alloys. Recently, airframe materials have dominated the market share due to their critical role in ensuring the structural integrity and performance of commercial aircraft. These materials, often made of high-strength alloys and composites, are essential for weight reduction, fuel efficiency, and compliance with safety standards. As airlines prioritize reducing operating costs, the demand for advanced airframe materials continues to rise, supporting the dominance of this sub-segment.

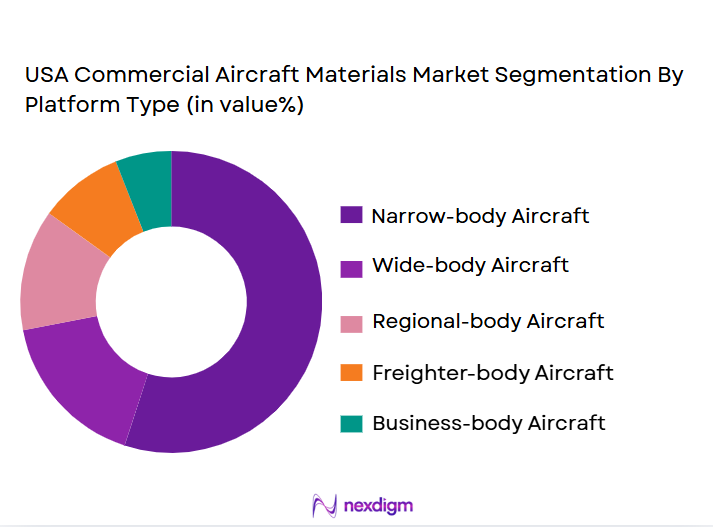

By Platform Type:

The market is segmented into narrow-body aircraft, wide-body aircraft, regional aircraft, freighter aircraft, and business jets. Narrow-body aircraft materials dominate the market due to their widespread use in both domestic and international travel. These aircraft are more cost-effective, operate on high-frequency routes, and demand materials that enhance fuel efficiency and reduce weight. As global air travel increases, especially in the low-cost carrier segment, the demand for narrow-body aircraft materials continues to outpace other platforms, ensuring its market dominance.

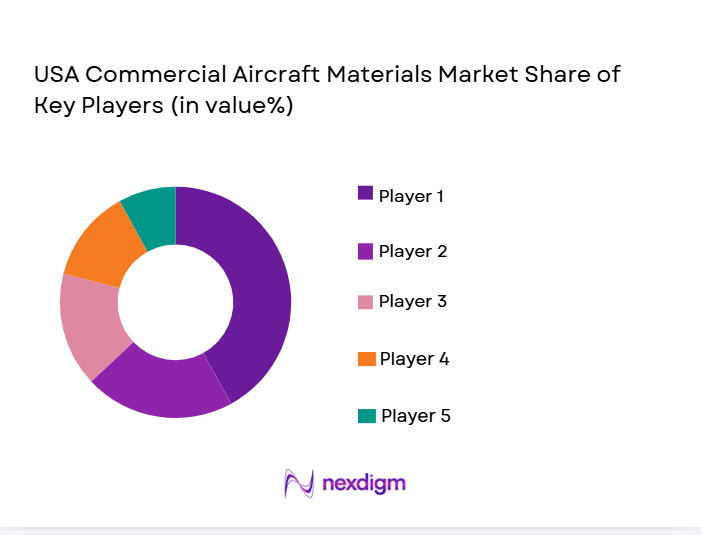

Competitive Landscape

The USA commercial aircraft materials market is highly competitive, with major players driving innovation and efficiency. The market sees a blend of consolidation and collaboration, with leading aerospace companies working alongside specialized materials suppliers to enhance product offerings. As companies invest heavily in R&D and manufacturing capabilities, the competition focuses on technological advancements in material composition, sustainability, and cost reduction, which are pivotal for the future of the industry.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Market-specific Parameter |

| Boeing | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | USA | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Spirit AeroSystems | 2005 | USA | ~ | ~ | ~ | ~ | ~ |

USA Commercial Aircraft Materials Market Analysis

Growth Drivers

Increase in Aircraft Production:

The rapid increase in aircraft production, especially driven by global demand for air travel, is a key growth driver for the commercial aircraft materials market. The surge in both narrow-body and wide-body aircraft production is directly impacting the demand for lightweight, high-performance materials that enhance fuel efficiency, reduce operational costs, and ensure structural integrity. This growth is also fueled by the increasing need for replacement parts as older aircraft are retired and replaced with newer, more efficient models. Aircraft manufacturers, such as Boeing and Airbus, are scaling up their production rates to meet the needs of expanding airlines, increasing the overall demand for advanced materials. The continuous focus on innovation in material technologies, such as carbon composites and advanced alloys, also supports the increasing aircraft production. As commercial aviation continues to grow globally, this trend will result in sustained demand for aircraft materials, especially in the U.S., which plays a pivotal role in aircraft manufacturing. Furthermore, the push for environmental sustainability is prompting the development of new materials that help reduce the carbon footprint of aircraft, further driving growth.

Technological Advancements in Aircraft Materials:

Advancements in material technologies are driving significant growth in the USA commercial aircraft materials market. Innovations such as carbon fiber composites, high-strength alloys, and titanium-based materials offer improved performance, higher durability, and reduced weight, which are essential for enhancing fuel efficiency and reducing emissions in modern aircraft. Aircraft manufacturers are increasingly adopting these advanced materials to meet the growing demand for more sustainable, fuel-efficient aircraft that comply with stringent environmental regulations. Additionally, advancements in 3D printing technology and additive manufacturing are allowing for the production of lighter and more complex components, further boosting the demand for new materials. As the need for eco-friendly solutions in aviation intensifies, these technological innovations are expected to shape the future of the commercial aircraft materials market. The U.S. is at the forefront of this transformation, with its advanced aerospace research and development infrastructure. Companies like Boeing and Lockheed Martin are leading the way in integrating these cutting-edge materials into their aircraft production processes, driving growth in the market.

Market Challenges

High Raw Material Costs:

One of the major challenges facing the USA commercial aircraft materials market is the rising cost of raw materials. The production of advanced aircraft materials such as carbon fiber composites, titanium alloys, and other high-performance materials involves substantial costs, which directly impact the pricing of the final product. As raw material costs continue to rise due to supply chain disruptions, geopolitical tensions, and increased demand for these materials across various industries, aircraft manufacturers and material suppliers are faced with higher production costs. This challenge puts pressure on the profitability of companies operating in the market and may limit their ability to invest in new technologies. Additionally, the cost burden is often passed onto airlines, which are already grappling with high fuel prices and other operational expenses. This could potentially slow the adoption of advanced materials, especially in smaller, budget-conscious carriers, and delay the overall growth of the commercial aircraft materials market.

Supply Chain Volatility:

The commercial aircraft materials market is also affected by supply chain volatility, particularly when it comes to sourcing critical materials like rare earth metals and specialty alloys. Disruptions in the supply chain, whether due to natural disasters, political instability, or trade restrictions, can delay production schedules and lead to shortages in the availability of essential materials. These supply chain challenges are exacerbated by the fact that many of the raw materials used in commercial aircraft manufacturing are sourced from specific regions, creating dependency on those regions. For example, titanium is primarily sourced from a few countries, and any disruption in the supply of this material can have significant ramifications on production timelines and costs. The increasing complexity of global supply chains and the reliance on specific suppliers for niche materials makes it difficult for manufacturers to maintain consistent production levels. As a result, supply chain volatility remains a key challenge for the USA commercial aircraft materials market, impacting everything from pricing to delivery schedules and overall market stability.

Opportunities

Adoption of Advanced Materials for Fuel Efficiency:

The growing focus on fuel efficiency presents a significant opportunity for the USA commercial aircraft materials market. With the global aviation industry striving to reduce its carbon footprint and lower operating costs, the demand for advanced materials that enhance fuel efficiency is on the rise. Lightweight materials such as carbon fiber composites and advanced aluminum alloys are particularly in demand due to their ability to reduce aircraft weight, thereby improving fuel efficiency. As airlines increasingly seek to lower their environmental impact and operational expenses, manufacturers are under pressure to innovate and incorporate these advanced materials into their fleets. The U.S., with its established aerospace manufacturing base and strong R&D infrastructure, is well-positioned to capitalize on this trend by developing and supplying high-performance materials that meet the aviation industry’s sustainability goals. This opportunity is further driven by government initiatives aimed at promoting greener technologies, which incentivize the adoption of fuel-efficient materials in the commercial aircraft sector.

Growth of Emerging Aircraft Manufacturers:

The rise of new and emerging aircraft manufacturers presents an exciting opportunity for the USA commercial aircraft materials market. As countries like China and India ramp up their aerospace production capabilities, there is a growing demand for high-performance materials to support the development of new aircraft models. These emerging manufacturers often look to established suppliers in the U.S. for advanced materials, creating significant export opportunities. The global expansion of air travel, particularly in Asia-Pacific, has created a need for new, cost-efficient aircraft that can meet rising passenger and cargo demands. As new manufacturers enter the market and existing manufacturers scale their operations, the demand for high-quality materials such as lightweight composites, advanced alloys, and durable coatings will continue to increase. U.S.-based suppliers of commercial aircraft materials stand to benefit from this growth by establishing long-term relationships with these emerging manufacturers, ensuring a steady stream of demand for their products in the coming years.

Future Outlook

The future outlook for the USA commercial aircraft materials market remains optimistic, with steady growth expected over the next five years. Driven by advancements in material technologies, increasing demand for fuel-efficient and sustainable solutions, and the continuous expansion of global air travel, the market is poised for continued development. Key trends such as the adoption of lightweight composites, advancements in 3D printing, and government support for eco-friendly innovations will shape the market. With the ongoing modernization of fleets and increasing demand for new aircraft, the market is set to benefit from technological innovations and increasing focus on sustainability.

Major Players

- Boeing

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Spirit AeroSystems

- General Electric Aviation

- Honeywell Aerospace

- United Technologies

- Rolls-Royce

- Airbus

- Pratt & Whitney

- Safran

- MTU Aero Engines

- Embraer

- Bombardier

Key Target Audience

- Aircraft manufacturers

- Material suppliers

- Aerospace research and development companies

- Aircraft operators

- Aircraft maintenance companies

- Defense contractors

- Aviation regulatory bodies

- Investment and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Identification of key market drivers, challenges, and growth opportunities based on industry trends, demand patterns, and technology advancements.

Step 2: Market Analysis and Construction

Analyze the market structure, segment sizes, and key players to construct a comprehensive view of the market landscape.

Step 3: Hypothesis Validation and Expert Consultation

Consult with industry experts and stakeholders to validate key hypotheses and gain insights into market dynamics.

Step 4: Research Synthesis and Final Output

Synthesize data from multiple sources to create a final market report, highlighting the most relevant trends, forecasts, and strategic insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Aircraft Production

Technological Advancements in Materials

Rising Demand for Lightweight and Fuel-Efficient Materials - Market Challenges

High Raw Material Costs

Supply Chain Volatility

Strict Regulatory and Certification Standards - Market Opportunities

Adoption of Advanced Materials for Fuel Efficiency

Growth of Emerging Aircraft Manufacturers

Increasing Focus on Sustainable Aviation Materials - Trends

Shift Toward Carbon Fiber and Lightweight Materials

Innovation in Composite Materials

Use of Recyclable and Sustainable Materials in Aircraft - Government Regulations & Defense Policy

Emissions Regulations and Environmental Compliance

Aerospace Certification and Safety Standards

Government Support for Aerospace Innovation - SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Airframe Materials

Engine Materials

Landing Gear Materials

Interior Materials

Composites and Alloys - By Platform Type (In Value%)

Narrow-body Aircraft

Wide-body Aircraft

Regional Aircraft

Freighter Aircraft

Business Jets - By Fitment Type (In Value%)

OEM Equipment

Replacement Materials

Aftermarket Parts

Upgraded Systems

Refurbishment Materials - By EndUser Segment (In Value%)

Aircraft Manufacturers

MRO Service Providers

Aircraft Leasing Companies

Aircraft Operators

Government and Defense - By Procurement Channel (In Value%)

Direct Procurement

Aircraft Leasing

Government Tenders

Private Sector Procurement

Third-Party Distributors - By Material / Technology (In Value%)

Titanium Alloys

Aluminum Alloys

Composites

Carbon Fiber Reinforced Polymers

High-Temperature Alloys

- Market structure and competitive positioning

- Market share snapshot of major players

CrossComparison Parameters (Material Type, Procurement Channel, Platform Type, EndUser Segment, Fitment Type, Aircraft Type, Certification Process, Sustainability, Cost Efficiency, Technology Adoption) - SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Boeing

Lockheed Martin

Airbus

Northrop Grumman

Raytheon Technologies

L3 Technologies

General Electric Aviation

Pratt & Whitney

Rolls-Royce

Safran

Honeywell Aerospace

United Technologies

MTU Aero Engines

Embraer

Spirit AeroSystems

- Increased Demand from OEMs

- Growth of the MRO Sector

- Expanding Aircraft Leasing Market

- Focus on Long-Term Sustainability in Aircraft Design

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now