Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Connected Car Platforms market current size stands at around USD ~ million, reflecting sustained adoption of embedded and cloud-native vehicle software platforms across consumer and commercial vehicles. Market maturity is shaped by accelerating software-defined vehicle architectures, increasing integration of telematics, infotainment, and OTA capabilities, and expanding data-driven services. Platform deployments span OEM-native systems, middleware layers, and hybrid smartphone-integrated environments, with ongoing investments in cybersecurity, cloud orchestration, and lifecycle management enhancing platform robustness and scalability.

Adoption is concentrated across California, Texas, Michigan, and Washington, supported by dense automotive R&D clusters, cloud infrastructure availability, and advanced connectivity corridors. Urban hubs such as Silicon Valley, Detroit, Austin, and Seattle host mature developer ecosystems and deep OEM–technology partnerships. High penetration of 5G corridors, smart city pilots, and fleet digitization programs strengthen demand concentration, while supportive federal and state-level digital transportation policies accelerate platform deployment across consumer, commercial, and public-sector mobility ecosystems.

Market Segmentation

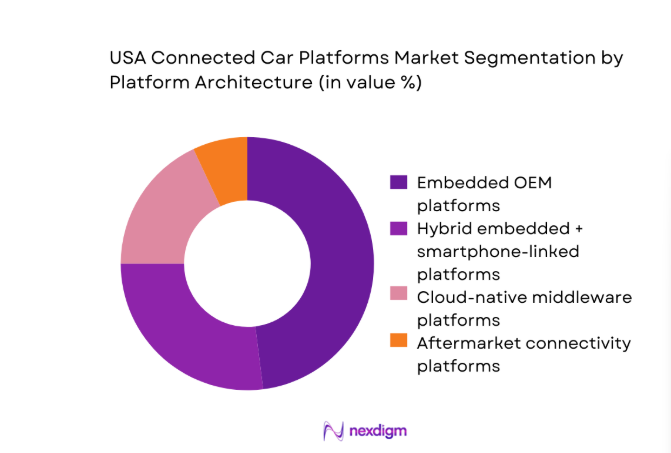

By Platform Architecture

Embedded OEM platforms dominate due to deeper integration with vehicle operating systems, enabling centralized compute, OTA updates, and secure data orchestration across infotainment, ADAS, and telematics. Hybrid platforms retain relevance in mid-range vehicles through smartphone integration, while cloud-native middleware gains traction among OEMs seeking scalable service orchestration and third-party app ecosystems. Aftermarket platforms remain niche, driven by legacy fleet retrofits and small operator digitization. Platform choice is increasingly influenced by cybersecurity certification requirements, long-term software support commitments, and compatibility with software-defined vehicle roadmaps. OEMs prioritize architectures that enable subscription services, lifecycle updates, and modular feature activation to improve customer engagement and post-sale monetization.

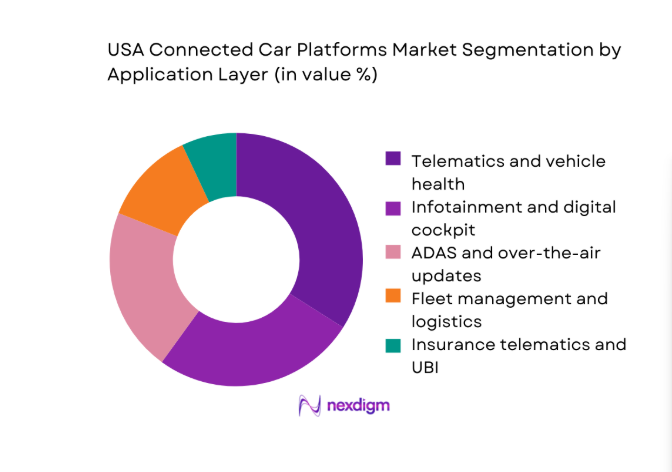

By Application Layer

Telematics and vehicle health lead adoption due to compliance-driven fleet monitoring and predictive maintenance needs. Infotainment and digital cockpit layers expand with demand for personalized in-car experiences and app ecosystems. ADAS and OTA platforms grow as software-defined vehicle strategies scale, enabling remote updates and safety feature activation. Fleet management applications gain momentum across logistics and public fleets, while insurance telematics platforms benefit from usage-based policy models and regulatory acceptance. Application-layer investments increasingly target data interoperability, edge analytics, and AI-driven insights to support real-time decision-making and service monetization across mobility ecosystems.

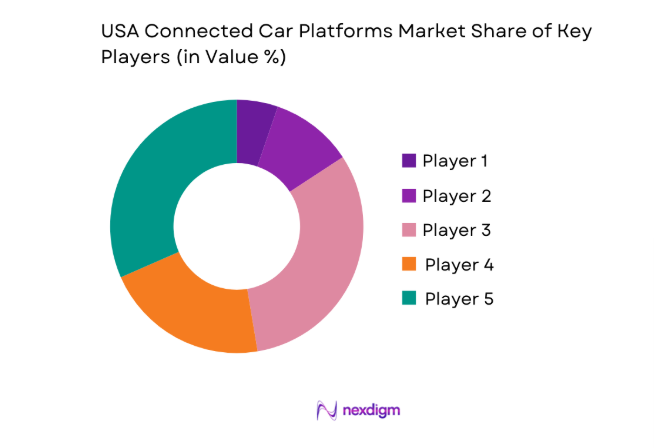

Competitive Landscape

The competitive environment features vertically integrated OEM platforms alongside technology providers delivering cloud orchestration, connectivity management, and software lifecycle tools. Platform competition centers on ecosystem depth, security certifications, and scalability across vehicle programs, with partnerships shaping go-to-market strength and developer adoption.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| General Motors | 1908 | Detroit, MI | ~ | ~ | ~ | ~ | ~ | ~ |

| Ford Motor Company | 1903 | Dearborn, MI | ~ | ~ | ~ | ~ | ~ | ~ |

| Tesla | 2003 | Austin, TX | ~ | ~ | ~ | ~ | ~ | ~ |

| Bosch | 1886 | Stuttgart, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Qualcomm | 1985 | San Diego, CA | ~ | ~ | ~ | ~ | ~ | ~ |

USA Connected Car Platforms Market Analysis

Growth Drivers

Rising OEM mandates for embedded connectivity as standard

Automakers increasingly standardize embedded connectivity to support safety, diagnostics, and software updates across new vehicle programs. In 2023, federal vehicle safety reporting logged 412 software-related recall actions, driving platform integration to enable remote remediation. State transport agencies recorded 64 connected corridor pilots supporting data exchange with vehicles. The National Highway Traffic Safety Administration documented 9 cybersecurity advisories linked to in-vehicle networks during 2024. Manufacturing plants in Michigan and Texas commissioned 18 new software validation labs in 2022–2024 to support embedded platform testing. These indicators reinforce mandatory platform inclusion across model lines to manage lifecycle updates and compliance requirements nationwide.

5G rollout enabling low-latency services and OTA capabilities

Telecom infrastructure expansion strengthens connected vehicle platform performance by enabling low-latency data exchange and continuous software delivery. In 2023, the Federal Communications Commission authorized 6,200 new 5G small cell permits along urban mobility corridors. The Department of Transportation logged 1,140 roadside units upgraded for vehicle-to-network interoperability during 2024. Average urban network latency benchmarks published by federal labs fell to 19 milliseconds in 2022 and 17 milliseconds in 2024. State smart corridor programs expanded to 27 metropolitan routes by 2025, enabling reliable OTA updates and real-time telemetry. These infrastructure indicators directly support platform reliability and advanced service deployment nationwide.

Challenges

Fragmented OEM platform stacks and interoperability issues

Divergent software stacks across automakers hinder cross-platform interoperability and ecosystem scalability. In 2022, federal interoperability pilots recorded 14 incompatible data schemas across connected vehicle platforms. The National Institute of Standards and Technology cataloged 31 automotive interface specifications in active use during 2023, complicating standardization. State smart mobility pilots reported 86 integration defects during multi-OEM trials in 2024. Certification audits across 22 production lines identified 57 deviations from common API profiles between 2022 and 2025. These institutional indicators reflect persistent fragmentation that slows multi-vehicle service deployment, increases integration overhead, and constrains third-party developer participation across connected car platforms nationwide.

High cybersecurity and data privacy compliance costs

Compliance with evolving cybersecurity and privacy mandates elevates implementation burdens for connected platforms. In 2023, federal agencies issued 11 new automotive cybersecurity advisories affecting in-vehicle data handling. The Cybersecurity and Infrastructure Security Agency logged 248 reported vulnerabilities in automotive software components during 2024. State privacy enforcement actions related to connected services reached 39 cases between 2022 and 2025. Certification programs expanded to 7 distinct automotive cybersecurity frameworks across this period. Regulatory audits across 41 production programs required remediation timelines under 120 days, straining engineering resources and delaying feature rollouts, thereby increasing operational friction for platform deployments nationwide.

Opportunities

Expansion of paid digital services and feature-on-demand models

Connected platforms enable feature activation and subscription services through software controls embedded at manufacture. In 2023, the Department of Commerce reported 23 software export approvals linked to automotive digital services toolchains. State consumer protection agencies recorded 112 filings related to in-vehicle digital service disclosures in 2024, clarifying monetization frameworks. Federal digital identity standards published in 2022 facilitated secure in-car account provisioning across 9 pilot programs. Vehicle software update events logged by transport authorities exceeded 3.2 million OTA transactions across public fleet pilots in 2025, validating scalable service activation pathways that support diversified revenue streams without physical retrofits.

Growth of insurance telematics and usage-based insurance platforms

Usage-based insurance integration benefits from connected platform telemetry and regulatory acceptance. State insurance departments approved 41 new telematics programs between 2022 and 2024. The National Association of Insurance Commissioners issued 6 model guidelines on connected data governance in 2023, standardizing insurer access frameworks. Public fleet trials across 14 municipalities recorded 28 million miles of telematics-enabled driving logs during 2024, supporting actuarial modeling. Federal privacy audits documented 19 compliant consent mechanisms adopted by insurers in 2025. These institutional indicators support scalable integration of insurance services within connected platforms, enabling data-driven underwriting and driver engagement services.

Future Outlook

The market outlook through 2030 reflects steady integration of software-defined vehicle architectures across new models, expanding OTA capabilities, and deeper convergence of infotainment, ADAS, and telematics. Policy support for smart corridors and cybersecurity standards will shape platform design priorities. Partnerships across OEMs, cloud providers, and telecom operators will accelerate service ecosystems, while data governance frameworks strengthen consumer trust and long-term adoption.

Major Players

- General Motors

- Ford Motor Company

- Stellantis

- Tesla

- Amazon Web Services

- Microsoft

- Qualcomm

- Bosch

- Continental

- Harman International

- Verizon

- AT&T

- BlackBerry QNX

- TomTom

Key Target Audience

- Automotive OEM digital platforms and software divisions

- Tier-1 automotive electronics and middleware suppliers

- Cloud infrastructure and edge computing providers

- Telecom operators and connectivity service providers

- Fleet operators and logistics service providers

- Mobility service and shared transportation operators

- Investments and venture capital firms

- Government and regulatory bodies including the U.S. Department of Transportation and Federal Communications Commission

Research Methodology

Step 1: Identification of Key Variables

Key platform architecture types, connectivity layers, application modules, cybersecurity requirements, and lifecycle update pathways were defined. Regulatory mandates, infrastructure readiness, and institutional interoperability standards were mapped to platform deployment contexts. Demand drivers across consumer, fleet, and public-sector use cases were delineated to scope analytical variables.

Step 2: Market Analysis and Construction

Platform adoption pathways were constructed using OEM program disclosures, federal corridor deployments, and state smart mobility initiatives. Application-layer penetration was analyzed across telematics, infotainment, ADAS, and OTA functions. Ecosystem linkages between OEMs, connectivity providers, and cloud orchestration layers were synthesized to build market structure logic.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on platform convergence, cybersecurity compliance burdens, and OTA scalability were validated through consultations with automotive software architects, transport agency technologists, and infrastructure program managers. Institutional benchmarks and standards documentation were used to test feasibility across regulatory and operational constraints.

Step 4: Research Synthesis and Final Output

Findings were consolidated into a coherent market narrative linking platform architectures, application layers, and policy frameworks. Cross-validation ensured internal consistency across ecosystem dynamics, deployment readiness, and future trajectory assumptions. Insights were refined to ensure consulting-grade clarity and actionable relevance.

- Executive Summary

- Research Methodology (Market Definitions and platform scope, OEM telematics platform mapping and deployment audits, Tier-1 and platform vendor revenue triangulation, Connected vehicle parc and activation rate modeling, Primary interviews with OEMs and fleet platform teams, Regulatory and spectrum policy impact assessment)

- Definition and Scope

- Market evolution

- Usage pathways across consumer, fleet, and mobility services

- Ecosystem structure across OEMs, Tier-1s, cloud and connectivity partners

- Supply chain and channel structure for embedded and hybrid platforms

- Regulatory environment

- Growth Drivers

Rising OEM mandates for embedded connectivity as standard

5G rollout enabling low-latency services and OTA capabilities

Growing adoption of software-defined vehicles

Fleet digitization and compliance-driven telematics demand

Monetization of in-vehicle data and subscription services

Partnerships between OEMs and hyperscale cloud providers - Challenges

Fragmented OEM platform stacks and interoperability issues

High cybersecurity and data privacy compliance costs

Long automotive product development cycles

Uncertain ROI on consumer subscription services

Network coverage gaps for advanced services

Complex integration with legacy vehicle architectures - Opportunities

Expansion of paid digital services and feature-on-demand models

Growth of insurance telematics and usage-based insurance platforms

Vehicle-to-everything enablement for smart city integration

Edge computing and AI-driven predictive maintenance services

Data monetization partnerships with mobility and retail ecosystems

Retrofit platforms for legacy fleet vehicles - Trends

Shift toward centralized vehicle operating systems

Standardization around cloud-native automotive middleware

Integration of generative AI in in-car assistants

Increased use of digital twins for vehicle lifecycle management

Open API ecosystems for third-party app developers

Convergence of infotainment and ADAS compute platforms - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Active Platforms, 2019–2024

- By Average Selling Price, 2019–2024

- By Platform Architecture (in Value %)

Embedded OEM platforms

Hybrid embedded + smartphone-linked platforms

Cloud-native middleware platforms

Aftermarket connectivity platforms - By Connectivity Technology (in Value %)

4G LTE

5G NR

Satellite connectivity

DSRC / C-V2X integration layers - By Vehicle Type (in Value %)

Passenger vehicles

Light commercial vehicles

Heavy commercial vehicles

Off-highway and specialty vehicles - By Application Layer (in Value %)

Telematics and vehicle health

Infotainment and digital cockpit

ADAS and over-the-air updates

Fleet management and logistics

Insurance telematics and UBI - By End User (in Value %)

Retail consumers

Commercial fleets

Mobility service providers

Government and municipal fleets - By Distribution Channel (in Value %)

OEM direct

Tier-1 integrators

Cloud and platform providers

Aftermarket solution providers

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Platform scalability, OEM partnerships footprint, Cloud integration depth, OTA and lifecycle management capabilities, Security and compliance certifications, Data monetization toolkits, Developer ecosystem maturity, Total cost of ownership)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

General Motors

Ford Motor Company

Stellantis

Tesla

Google

Amazon Web Services

Microsoft

Qualcomm

Bosch

Continental

Harman International

Verizon

AT&T

BlackBerry QNX

TomTom

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Active Platforms, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now