Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA digital health market has experienced rapid growth, valued at over USD ~ billion based on a recent historical assessment. This growth is driven by technological advancements in telemedicine, electronic health records (EHR), mobile health applications, and wearable devices. The rise in healthcare costs, aging populations, and an increased focus on patient outcomes have further accelerated market demand. The healthcare sector’s shift towards digital solutions, backed by favorable regulations and increasing consumer demand for remote healthcare services, continues to drive the market’s expansion.

The market is primarily dominated by major healthcare hubs such as California, New York, and Texas. These regions have seen significant investments in healthcare infrastructure, digital health innovation, and healthcare provider adoption. States like California have been at the forefront of embracing telemedicine solutions, while New York and Texas focus on healthcare digitization across urban and rural areas. The innovation ecosystem in these areas has attracted a growing number of technology providers, health startups, and government support, propelling their dominance in the digital health space.

Market Segmentation

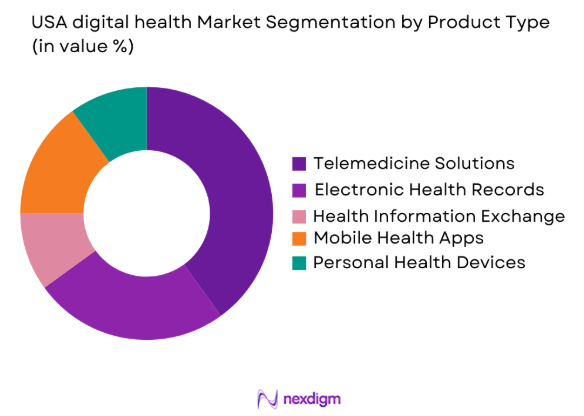

By Product Type

The USA digital health market is segmented by product type into telemedicine solutions, electronic health records (EHR), health information exchange (HIE) systems, mobile health apps, and personal health devices. Recently, telemedicine solutions have dominated the market share, driven by the increased adoption of remote healthcare services, regulatory support, and consumer demand for at-home consultations. This shift has been accelerated by the COVID-19 pandemic and the resulting need for digital health solutions. Telemedicine’s convenience, cost-effectiveness, and ability to improve access to care, especially in rural areas, have further cemented its market dominance.

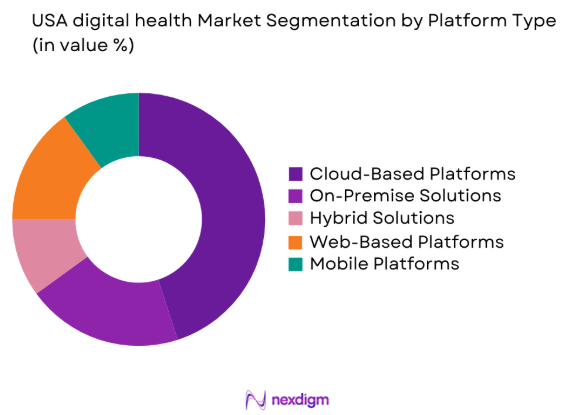

By Platform Type

The USA digital health market is segmented by platform type into cloud-based platforms, on-premise solutions, hybrid solutions, web-based platforms, and mobile platforms. Cloud-based platforms have a dominant share, mainly due to their scalability, cost-effectiveness, and ease of integration into existing healthcare IT systems. The cloud allows healthcare providers to offer remote monitoring, improve data sharing, and enhance interoperability across the healthcare ecosystem, making it the most preferred platform type for healthcare institutions and consumers alike.

Competitive Landscape

The competitive landscape of the USA digital health market is highly fragmented, with several major players consolidating their positions by acquiring smaller startups, forming strategic partnerships, and expanding their product portfolios. Major players like Cerner, McKesson, and Philips dominate the market, focusing on telemedicine, EHR solutions, and integrated health platforms. The influence of these players is shaping the market by setting standards for interoperability, data security, and user adoption, while encouraging innovation through R&D investments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Cerner Corporation | 1979 | North Kansas City, MO | ~ | ~ | ~ | ~ | ~ |

| McKesson Corporation | 1833 | Irving, TX | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, NL | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

| Teladoc Health | 2002 | Purchase, NY | ~ | ~ | ~ | ~ | ~ |

USA digital health Market Analysis

Growth Drivers

Increased Adoption of Telemedicine

The rapid expansion of telemedicine is fueled by increasing demand for accessible, affordable healthcare, particularly in rural and underserved regions. Patients and healthcare providers are adopting virtual consultations as a convenient and efficient alternative to traditional in-person visits. The growth of telehealth infrastructure, supported by government initiatives, policy incentives, and insurance reimbursements, is further driving market adoption. The COVID-19 pandemic accelerated the uptake of telemedicine, highlighting its critical role in maintaining care continuity. As healthcare systems continue to integrate telemedicine into routine workflows, including remote monitoring and virtual consultations, the USA digital health market is expected to sustain robust growth and broader technology adoption.

Technological Advancements in Digital Health Solutions

Ongoing technological innovation is driving substantial growth in the USA digital health market. Advancements in artificial intelligence (AI), machine learning, and cloud computing are enabling more advanced telemedicine platforms, improving data analytics, and optimizing clinical workflows. AI-powered tools for diagnostics, predictive analytics, and personalized treatment planning are increasingly adopted across healthcare settings, enhancing efficiency and patient care. Simultaneously, wearable health devices, including smartwatches and fitness trackers, are playing a critical role in continuous health monitoring, delivering real-time insights that support early interventions, improve outcomes, and help manage healthcare costs. These technological developments are shaping a more connected and data-driven healthcare ecosystem.

Market Challenges

Data Privacy and Security Concerns

A key challenge in the USA digital health market is safeguarding sensitive patient data amid the growing reliance on digital platforms. The proliferation of telemedicine, electronic health records, and connected devices has heightened exposure to data breaches, hacking, and cyber-attacks. Healthcare organizations are required to comply with stringent regulations, including HIPAA, to ensure secure storage, transmission, and handling of patient information. The complexity of these regulatory requirements, coupled with rapidly evolving technology, makes maintaining compliance increasingly difficult for providers. Concerns over data privacy, combined with the rising frequency and sophistication of cybersecurity threats, could slow adoption rates and limit market growth, highlighting the need for robust security strategies and continuous risk management.

Integration and Interoperability Issues

Despite notable advancements in digital health solutions, interoperability between healthcare systems remains a significant challenge in the USA digital health market. Providers frequently use multiple platforms for electronic health records, telemedicine, and health information exchange, resulting in fragmented care and operational inefficiencies. The inability of these disparate systems to communicate effectively restricts seamless data sharing, delays clinical decision-making, and can negatively impact patient outcomes. Integrating digital health technologies into existing healthcare infrastructures, especially in rural and underserved areas, poses additional obstacles due to limited technical resources and infrastructure gaps. Addressing these interoperability and integration issues is essential to fully realizing the potential of digital health solutions and supporting continued market growth.

Opportunities

Expansion of Wearable Health Technology

The rising demand for wearable health devices, including fitness trackers, smartwatches, and biosensors, offers considerable opportunities in the USA digital health market. These devices enable individuals to continuously monitor health metrics, track vital signs, and manage chronic conditions such as diabetes, hypertension, and cardiovascular issues. Integration of wearables with telemedicine platforms enhances remote patient monitoring, enabling healthcare providers to deliver timely interventions and personalized care. As consumers become increasingly health-conscious and proactive about managing their well-being, adoption of wearable health technology continues to accelerate. This trend is further supported by advancements in sensor technology, improved data analytics, and the growing preference for connected healthcare solutions, driving substantial market expansion.

Government Support and Funding for Digital Health Solutions

The U.S. government has been proactively promoting the adoption of digital health technologies through various grants, funding programs, and policy reforms. Initiatives such as the Medicare and Medicaid Services (CMS) Innovation Center encourage healthcare providers to implement electronic health records and telemedicine solutions, while enhancing access to healthcare in underserved regions. Ongoing efforts to digitize healthcare systems, supported by regulatory incentives and reimbursement programs, are creating a favorable environment for market expansion. These policies not only drive technological adoption among providers but also stimulate innovation among technology companies. Consequently, both healthcare organizations and digital health solution providers are positioned to benefit from government-backed initiatives fostering nationwide digital healthcare integration.

Future Outlook

Over the next five years, the USA digital health market is expected to experience continued growth driven by technological innovations, increased demand for remote healthcare solutions, and regulatory support. Advancements in artificial intelligence, wearable health technology, and telemedicine will continue to shape the landscape. Additionally, government initiatives aimed at improving healthcare accessibility and reducing costs will further drive market expansion. As digital health adoption becomes more mainstream, healthcare providers will increasingly integrate digital solutions into their operations, leading to enhanced patient care and operational efficiencies.

Major Players

- Cerner Corporation

- McKesson Corporation

- Philips Healthcare

- Medtronic

- Teladoc Health

- GE Healthcare

- Allscripts Healthcare Solutions

- IBM Watson Health

- Oracle Health Sciences

- Johnson & Johnson Medical Device

- Siemens Healthineers

- Athenahealth

- Zebra Medical Vision

- Accenture

- Health Catalyst

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Digital health technology companies

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Hospitals and clinics

Research Methodology

Step 1: Identification of Key Variables

Identification of key market variables such as product types, platform types, and regulatory factors that influence the digital health market.

Step 2: Market Analysis and Construction

Collection and analysis of both primary and secondary data to construct a clear picture of the market landscape, including market size, trends, and growth drivers.

Step 3: Hypothesis Validation and Expert Consultation

Validation of findings through expert consultations, including interviews with industry professionals, healthcare providers, and technology companies.

Step 4: Research Synthesis and Final Output

Synthesis of the data and expert insights to deliver a comprehensive market report, providing actionable recommendations and forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Adoption of Telemedicine

Rising Healthcare Costs and Demand for Cost-Effective Solutions

Government Initiatives and Funding for Digital Health - Market Challenges

Data Privacy and Security Concerns

High Initial Investment for Healthcare Providers

Regulatory Compliance and Integration Challenges - Market Opportunities

Growth in Wearable Health Technology

Emerging Markets Adoption of Digital Health Solutions

Artificial Intelligence and Machine Learning Integration in Healthcare - Trends

Growth in Remote Patient Monitoring

AI-driven Diagnostics and Treatment Solutions

Integration of IoT in Healthcare - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine Solutions

Electronic Health Records (EHR)

Health Information Exchange (HIE) Systems

Mobile Health (mHealth) Apps

Personal Health Devices - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Solutions

Hybrid Solutions

Web-based Platforms

Mobile Platforms - By Fitment Type (In Value%)

Hospital Fitment

Clinic Fitment

Home Healthcare Fitment

Corporate Wellness Fitment

Telemedicine Fitment - By End User Segment (In Value%)

Healthcare Providers

Healthcare Payers

Patients

Pharmaceutical Companies

Government Agencies - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Procurement Platforms

Third-Party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Regulatory Compliance, Data Security, User Adoption Rates, Integration Complexity, Market Growth Rate)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cerner Corporation

Allscripts Healthcare Solutions

McKesson Corporation

Siemens Healthineers

GE Healthcare

Philips Healthcare

Medtronic

IBM Watson Health

Oracle Health Sciences

Johnson & Johnson Medical Devices

Fujifilm Healthcare

Athenahealth

Zebra Medical Vision

Teladoc Health

Dexcom

- Increasing Demand from Healthcare Providers for Digital Solutions

- Government Focus on Expanding Digital Health Access

- Patients’ Growing Acceptance of Telemedicine

- Rise in Healthcare Technology Adoption by Payers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now