Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Door Panels market current size stands at around USD ~ million, reflecting steady demand from OEM interior programs, model refresh cycles, and compliance-driven material upgrades across passenger and commercial platforms. The market is shaped by evolving interior safety standards, durability requirements, and consumer preferences for soft-touch surfaces and integrated controls. Supply chains remain sensitive to resin availability and specialty textile inputs, while sustainability targets continue to influence material selection and component architecture across vehicle programs.

Demand concentration is strongest in Midwest and Southeast manufacturing corridors anchored by major assembly plants and Tier-1 clusters. Design engineering hubs in Michigan and California drive early-stage validation and tooling decisions, while logistics nodes in Texas and Ohio support just-in-time delivery to assembly lines. Policy environments emphasizing interior emissions compliance and recycled content adoption accelerate ecosystem maturity, reinforcing localized supplier networks and tooling investments near OEM footprints.

Market Segmentation

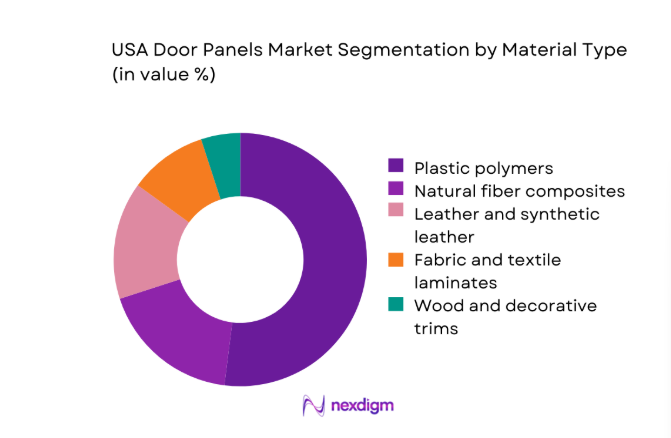

By Material Type

Polymer-based door panels dominate due to manufacturability, surface finish consistency, and compatibility with lightweighting targets. Polypropylene blends and engineered plastics enable rapid tooling changes aligned with model refresh cycles, while natural fiber composites are gaining traction for sustainability credentials and acoustic damping. Premium trims using leather, synthetic leather, and textile laminates remain concentrated in higher trim levels, driven by perceived quality and tactile differentiation. Wood and decorative trims persist in limited luxury applications where aesthetic differentiation justifies higher complexity in lamination and finishing processes. Material selection increasingly reflects regulatory thresholds for interior emissions and OEM recycled-content mandates.

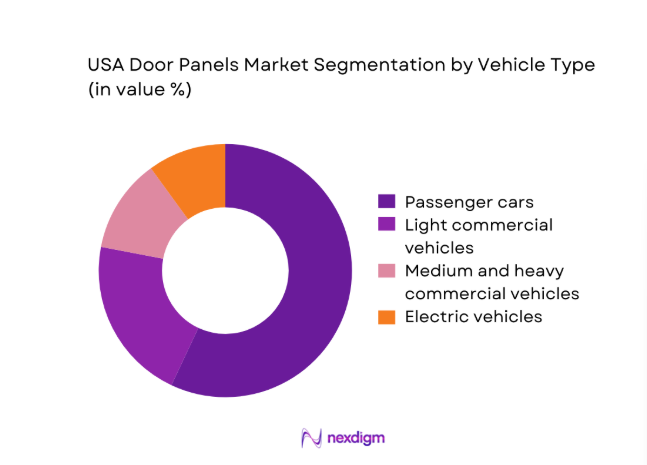

By Vehicle Type

Passenger cars lead adoption due to higher feature density, frequent trim-level differentiation, and shorter refresh cycles that favor interior redesign. Light commercial vehicles increasingly adopt upgraded door trims to improve driver comfort and fleet branding, while medium and heavy commercial vehicles prioritize durability and easy-clean surfaces over aesthetics. Electric vehicles exhibit distinct requirements, including lightweight substrates and integrated ambient lighting to support cabin differentiation. Vehicle-type segmentation is shaped by production planning, platform modularity, and interior packaging constraints, with OEMs standardizing door architectures across platforms to control tooling complexity and ensure cross-program component reuse.

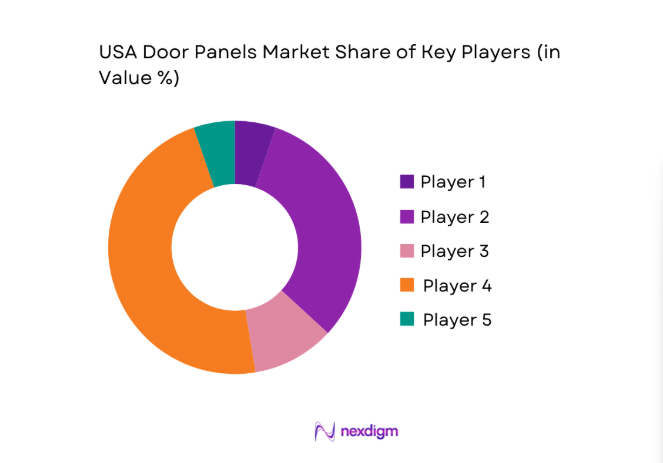

Competitive Landscape

The competitive environment is characterized by Tier-1 suppliers with vertically integrated tooling, materials engineering, and proximity to OEM assembly plants. Differentiation centers on surface finishing capabilities, lightweight substrates, sustainability compliance, and program management reliability across multi-plant footprints.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Adient | 2016 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ | ~ |

| Lear Corporation | 1917 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Faurecia | 1997 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Grupo Antolin | 1950 | Spain | ~ | ~ | ~ | ~ | ~ | ~ |

USA Door Panels Market Analysis

Growth Drivers

Rising vehicle production and model refresh cycles in the US

Assembly activity across Michigan, Ohio, Kentucky, Tennessee, Alabama, and Texas expanded through 2023 and 2024 as new model introductions increased tooling changeovers. Federal safety updates issued in 2022 and 2023 elevated interior impact requirements, prompting door panel redesigns across multiple platforms. Port throughput volumes at Los Angeles and Long Beach recovered in 2023, stabilizing inbound resin flows. Rail carload counts serving Midwest assembly corridors increased in 2024, improving just in time deliveries. State incentives supported retooling projects at three manufacturing sites in 2023, accelerating platform refresh cycles and driving consistent program launches across compact, midsize, and utility segments.

Growing demand for premium interiors and soft-touch surfaces

Consumer preference shifts toward comfort and perceived quality intensified in 2023 and 2024, reflected in trim-level proliferation across domestic assembly programs. Interior option packages expanded across five major assembly plants, increasing SKU counts for stitched door trims and padded substrates. National highway safety testing updates in 2022 emphasized interior contact surfaces, accelerating adoption of energy absorbing foams. Warranty claims related to hard plastic scuffing declined in 2024 following material upgrades. Dealer feedback loops indicated higher attachment rates for premium interior packages across new vehicle launches in 2023, reinforcing OEM commitments to tactile differentiation within standardized door architectures.

Challenges

Volatility in polymer and resin prices

Resin supply volatility persisted across 2023 and 2024 as hurricane disruptions affected Gulf Coast petrochemical operations and maintenance outages constrained output. Import lead times from East Asia fluctuated through 2023 due to port congestion, complicating production planning for thermoplastic substrates. Rail transport bottlenecks in early 2024 extended delivery windows to Midwest plants, increasing line changeover risks. Inventory buffers expanded at two Tier 1 facilities during 2024 to mitigate supply gaps. Environmental compliance audits in 2022 introduced additional qualification steps for alternative resins, slowing substitution cycles and raising operational complexity for multi plant manufacturing networks.

High tooling and retooling costs for new vehicle platforms

Platform consolidation accelerated across 2023 and 2024, requiring new molds for modular door architectures. Tool steel lead times extended in 2023 due to capacity constraints among North American toolmakers, delaying validation cycles. State level safety certifications introduced in 2022 mandated additional impact testing for interior components, extending tooling qualification timelines. Workforce shortages in skilled machining persisted through 2024, reducing throughput at tooling facilities. OEM change management protocols introduced in 2024 increased revision counts per program, complicating freeze dates and raising risks of late stage rework for door panel assemblies across multiple assembly locations.

Opportunities

Integration of sustainable and recycled material content

Regulatory guidance on recycled content thresholds expanded in 2022 and 2023, prompting OEM procurement teams to specify minimum recycled polymer content in interior components. Municipal recycling capacity in California and Michigan increased in 2024, improving feedstock availability for compounded resins. Federal grants issued in 2023 supported pilot lines for bio composite processing at two supplier sites. Lifecycle assessment frameworks adopted by three state agencies in 2024 elevated preference for low emission interior materials. These shifts create pathways for suppliers to qualify recycled substrates across multiple platforms while aligning with OEM sustainability scorecards and supplier performance audits.

Growth in EV-specific interior redesigns and flat-floor architectures

EV assembly programs expanded across Tennessee and Texas in 2023 and 2024, introducing flat floor layouts that alter door panel geometry and packaging. Federal charging corridor investments in 2022 supported regional EV adoption, increasing OEM focus on differentiated interiors. Cabin acoustic requirements intensified for EVs in 2023 due to lower powertrain noise, elevating demand for damping layers within door trims. Thermal insulation standards issued in 2024 for battery adjacent structures influenced material layering in door panels near sill interfaces, opening opportunities for advanced composites and integrated insulation solutions across new EV platforms.

Future Outlook

The market outlook through 2030 reflects continued OEM emphasis on modular interior architectures, sustainability compliance, and differentiation for electrified platforms. Localization of tooling and material compounding is expected to deepen near assembly clusters. Regulatory evolution on interior emissions and recycled content will shape material choices, while digital validation and faster refresh cycles will compress development timelines across vehicle programs.

Major Players

- Adient

- Magna International

- Lear Corporation

- Faurecia

- Grupo Antolin

- Toyota Boshoku

- Yanfeng Automotive Interiors

- Hyundai Mobis

- TS Tech

- IAC Group

- Plastic Omnium

- Brose Fahrzeugteile

- Motherson Group

- SAS Autosystemtechnik

- Tachi-S

Key Target Audience

- Passenger vehicle OEM interior engineering teams

- Commercial vehicle OEM procurement divisions

- Tier-1 automotive interior system integrators

- Tier-2 material compounders and laminate suppliers

- Automotive tooling and mold manufacturing firms

- Investments and venture capital firms

- U.S. Department of Transportation and Environmental Protection Agency

- State motor vehicle regulatory agencies

Research Methodology

Step 1: Identification of Key Variables

Core variables were defined across material systems, door architectures, manufacturing processes, and compliance thresholds. Program cadence, tooling cycles, and localization factors were mapped to assembly footprints. Regulatory requirements for interior emissions and recycled content were incorporated as design constraints.

Step 2: Market Analysis and Construction

Demand drivers were constructed from assembly plant activity, platform refresh cadence, and interior content density. Supply factors included material availability, tooling capacity, and logistics reliability. Scenario frames reflected platform consolidation and electrification impacts on door panel design complexity.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were validated through structured consultations with OEM interior engineers, supplier operations leads, and compliance specialists. Validation focused on material substitution feasibility, tooling lead times, and production readiness across multi-plant programs.

Step 4: Research Synthesis and Final Output

Findings were synthesized into market narratives aligned with regulatory evolution, platform strategies, and manufacturing constraints. Cross-functional insights were consolidated to ensure consistency across segmentation, competitive dynamics, and forward-looking assessments.

- Executive Summary

- Research Methodology (Market Definitions and door panel architecture taxonomy, OEM and Tier-1 procurement interviews, teardown and material composition analysis, production capacity and tooling audits, trade flow and tariff mapping, regulatory standards review, pricing and cost-curve benchmarking)

- Definition and Scope

- Market evolution

- Usage and functional pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising vehicle production and model refresh cycles in the US

Growing demand for premium interiors and soft-touch surfaces

Lightweighting initiatives to improve fuel efficiency and EV range

OEM push for recycled and bio-based interior materials

Advancements in tooling and surface finishing technologies

Customization and trim differentiation for brand identity - Challenges

Volatility in polymer and resin prices

High tooling and retooling costs for new vehicle platforms

Supply chain disruptions for specialty fabrics and resins

Stringent VOC and interior emissions compliance costs

Pressure on margins from OEM price-down programs

Quality and durability issues under extreme temperature cycles - Opportunities

Integration of sustainable and recycled material content

Growth in EV-specific interior redesigns and flat-floor architectures

Smart surfaces with ambient lighting and haptic controls

Localization of Tier-1 production to reduce logistics risk

Aftermarket premium trim upgrades and personalization

Adoption of digital twins for tooling and design optimization - Trends

Shift toward soft-touch, stitched, and premium surface finishes

Increased use of recycled plastics and natural fiber composites

Modular door panel architectures for platform sharing

Ambient lighting and integrated controls within door trims

Design simplification to reduce part counts and weight

Nearshoring of component manufacturing in North America - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Material Type (in Value %)

Plastic polymers

Natural fiber composites

Leather and synthetic leather

Fabric and textile laminates

Wood and decorative trims - By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Medium and heavy commercial vehicles

Electric vehicles - By Panel Configuration (in Value %)

Front door panels

Rear door panels

Sliding door panels

Tailgate and liftgate trims - By Manufacturing Process (in Value %)

Injection molding

Thermoforming

Compression molding

Foam-in-place and lamination - By Sales Channel (in Value %)

OEM fitment

Aftermarket replacement

Dealer accessories

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (manufacturing footprint, material portfolio depth, OEM relationships, tooling and engineering capability, cost competitiveness, sustainability compliance, innovation pipeline, delivery reliability)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Adient

Magna International

Lear Corporation

Faurecia

Grupo Antolin

Toyota Boshoku

Yanfeng Automotive Interiors

Hyundai Mobis

TS Tech

IAC Group

Plastic Omnium

Brose Fahrzeugteile

Motherson Group

SAS Autosystemtechnik

Tachi-S

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now