Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Edge Computing market reached approximately USD ~ billion based on a recent historical assessment, supported by accelerating enterprise digitalization and expanding deployment of distributed IT infrastructure. Demand is driven by low latency processing requirements across autonomous systems, industrial IoT, smart retail, and real time analytics workloads. Telecom edge nodes, private 5G networks, and on premise micro data centers are expanding rapidly, enabling localized computing architectures that reduce bandwidth dependence and improve application responsiveness.

Major metropolitan technology corridors such as Silicon Valley, Seattle, Austin, and Northern Virginia dominate deployment due to dense hyperscale cloud presence, advanced telecom infrastructure, and enterprise innovation ecosystems. Industrial hubs across Midwest manufacturing clusters and logistics intensive regions also exhibit strong adoption, driven by automation and connected operations.

Market Segmentation

By Product Type

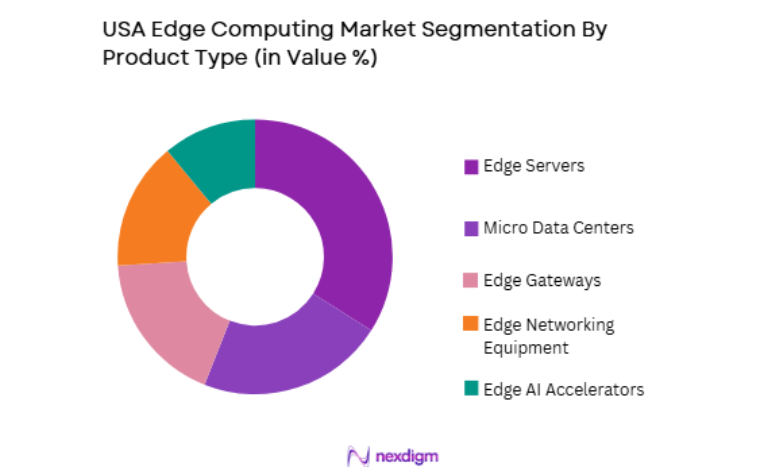

USA Edge Computing market is segmented by product type into edge servers, edge gateways, micro data centers, edge AI accelerators, and edge networking equipment. Recently, edge servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprise workloads migrating from centralized cloud to distributed architectures require high performance compute nodes at network peripheries. Edge servers enable containerized applications, virtualization, and AI inference processing locally, supporting industrial automation, smart surveillance, and real time analytics. Telecom operators deploying multi access edge computing nodes rely heavily on ruggedized edge servers integrated into base stations and aggregation sites. Hyperscale providers also standardize edge server platforms to extend cloud services closer to users.

By End Use Industry

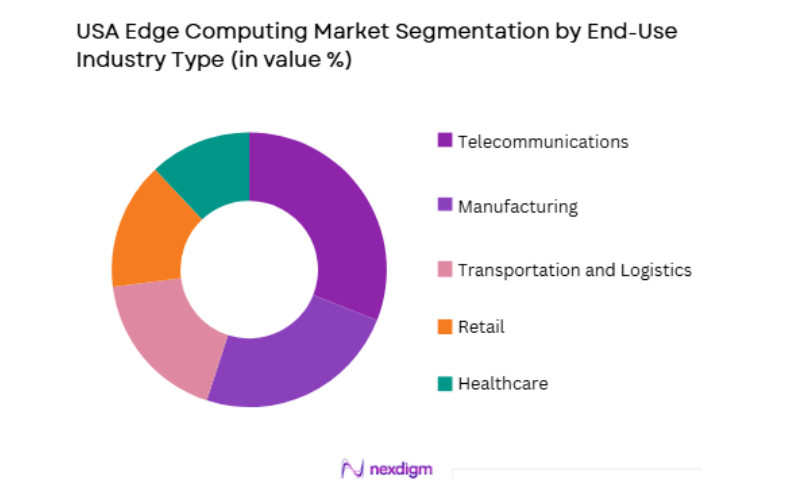

USA Edge Computing market is segmented by end use industry into manufacturing, telecommunications, healthcare, retail, and transportation and logistics. Recently, telecommunications has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecom operators deploy edge nodes to enable low latency services such as private 5G, content delivery, and network function virtualization. Multi access edge computing architectures embedded within radio access networks allow localized processing for connected devices and applications. Increasing mobile data traffic, streaming demand, and enterprise connectivity solutions drive telecom investment in distributed compute infrastructure. Telecom providers also partner with hyperscale cloud firms to deliver edge cloud services, further expanding deployment scale. Their ownership of network infrastructure and proximity to users positions telecom as the largest adopter.

Competitive Landscape

The USA Edge Computing market exhibits moderate consolidation with major technology conglomerates and telecom infrastructure providers shaping deployment ecosystems. Hyperscale cloud vendors, semiconductor firms, and network equipment manufacturers collaborate through integrated edge platforms combining compute, connectivity, and software orchestration. Telecom operators extend infrastructure reach, while hardware specialists provide ruggedized edge devices.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Model |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Cisco Systems | 1984 | San Jose, USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | Round Rock, USA | ~ | ~ | ~ | ~ | ~ |

| HPE | 1939 | Houston, USA | ~ | ~ | ~ | ~ | ~ |

USA Edge Computing Market Analysis

Growth Drivers

Latency Critical Industrial and Autonomous Applications Expansion

Proliferation of latency sensitive applications across autonomous mobility, industrial automation, and immersive media is accelerating localized compute deployment near data sources to meet stringent responsiveness, reliability, and bandwidth efficiency requirements. Manufacturing automation systems increasingly depend on deterministic processing for robotics coordination, predictive maintenance analytics, and machine vision inspection workloads requiring millisecond decision latency unattainable through centralized cloud architectures. Autonomous vehicles, drones, and connected transportation platforms generate continuous sensor streams demanding edge processing to ensure safety critical decision making without network dependency risks. Real time augmented reality and immersive collaboration applications in enterprise training and design workflows require local rendering and data synchronization to maintain user experience fidelity. Edge computing architectures reduce backhaul traffic and operational costs by filtering, aggregating, and analyzing data locally before selective cloud transmission. Telecom operators deploying private 5G networks integrate edge compute nodes to support industrial IoT and mission critical communications use cases. Defense and public safety sectors adopt edge analytics for surveillance, situational awareness, and secure operations in disconnected environments.

Telecom Edge Cloud and 5G Infrastructure Integration

Nationwide deployment of 5G networks and telecom edge cloud platforms is accelerating distributed computing adoption by embedding compute resources directly within radio and aggregation network layers across metropolitan and enterprise connectivity environments. Telecom providers integrate multi access edge computing nodes at base stations and central offices to deliver localized application hosting and network function virtualization capabilities. Partnerships between telecom operators and hyperscale cloud firms enable hybrid edge cloud services extending public cloud platforms closer to enterprise and consumer endpoints. Increasing mobile data traffic and bandwidth intensive applications such as streaming, gaming, and IoT connectivity require localized processing to maintain quality of service. Private 5G deployments in manufacturing, ports, and campuses rely on on site edge compute infrastructure for deterministic connectivity and analytics workloads.

Market Challenges

Fragmented Edge Architecture Standards and Interoperability Constraints

Diverse hardware platforms, software frameworks, and orchestration environments across vendors create interoperability challenges that complicate deployment, integration, and lifecycle management of distributed edge computing infrastructure across heterogeneous enterprise and telecom environments. Lack of standardized interfaces between edge devices, cloud platforms, and network systems increases integration costs and deployment timelines for organizations adopting multi vendor edge ecosystems. Edge workloads often require compatibility across containers, virtualization layers, and proprietary device operating systems, limiting seamless portability between platforms. Industrial environments with legacy operational technology systems further complicate integration with modern edge computing architectures and protocols. Telecom edge platforms, enterprise edge nodes, and hyperscale edge clouds frequently employ distinct management stacks, reducing unified orchestration efficiency.

Distributed Infrastructure Security and Data Governance Complexity

Edge computing environments expand the attack surface by distributing compute and data processing across numerous geographically dispersed nodes, creating heightened cybersecurity risks and governance challenges compared with centralized data center architectures. Edge nodes often operate in remote or uncontrolled physical environments such as factories, telecom towers, and transportation hubs, increasing vulnerability to tampering and unauthorized access. Local data processing introduces regulatory and compliance complexities regarding data sovereignty, privacy, and auditability across jurisdictions and industries. Resource constrained edge devices may lack robust security monitoring and patch management capabilities compared with centralized systems. Managing identity, encryption, and secure communications across thousands of distributed endpoints requires advanced orchestration and lifecycle controls.

Opportunities

AI Inference Acceleration at the Edge for Real Time Intelligence

Rapid growth of artificial intelligence inference workloads across industrial automation, smart cities, healthcare diagnostics, and autonomous systems creates strong demand for localized edge computing platforms capable of executing machine learning models directly at data generation points. Edge AI enables immediate analytics and decision making without reliance on cloud connectivity, supporting safety critical and latency sensitive applications. Semiconductor advances in low power AI accelerators and GPUs optimized for edge deployment enhance processing efficiency within constrained environments. Enterprises adopt edge AI for predictive maintenance, quality inspection, and anomaly detection across distributed operations. Smart infrastructure systems deploy edge intelligence for traffic management, surveillance analytics, and environmental monitoring.

Private Edge Infrastructure in Industrial and Sovereign Environments

Growing demand for data sovereignty, operational control, and ultra reliable connectivity is driving enterprises and governments to deploy private edge computing infrastructure within industrial campuses, defense installations, and critical national infrastructure environments across the United States. Manufacturing plants implement on premise edge data centers integrated with private 5G networks to support automation and analytics while retaining data locally. Energy utilities deploy edge compute for grid monitoring, predictive maintenance, and remote asset management across geographically distributed operations. Defense and aerospace sectors require secure disconnected edge environments for mission critical analytics and situational awareness. Government smart infrastructure projects deploy localized computing for traffic, surveillance, and emergency systems independent of public cloud reliance.

Future Outlook

The USA Edge Computing market is expected to expand steadily over the next five years as distributed digital infrastructure becomes integral to industrial automation, telecom evolution, and artificial intelligence deployment. Integration of edge with 5G, AI accelerators, and hybrid cloud platforms will accelerate enterprise adoption. Regulatory emphasis on data sovereignty and infrastructure resilience will support localized computing investment. Demand from manufacturing, transportation, healthcare, and defense sectors will sustain growth as latency sensitive applications proliferate across connected environments.

Major Players

- Amazon Web Services

- Microsoft

- Cisco Systems

- Dell Technologies

- Hewlett Packard Enterprise

- NVIDIA

- Intel

- IBM

- Google

- AT&T

- Verizon

- Juniper Networks

- Nokia

- Schneider Electric

- Siemens

Key Target Audience

- Telecom network operators

- Manufacturing enterprises

- Transportation and logistics operators

- Healthcare system providers

- Retail chains

- Energy and utilities companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key supply and demand variables across technology adoption, telecom infrastructure deployment, industrial automation trends, and enterprise digitalization patterns were identified. Product architectures, deployment models, and regional infrastructure concentration were mapped to understand structural drivers influencing USA Edge Computing market dynamics.

Step 2: Market Analysis and Construction

Technology ecosystem mapping combined vendor offerings, deployment architectures, and industry adoption patterns to construct market segmentation and competitive structure. Supply chain roles across semiconductor, hardware, software, and telecom integration layers were analyzed to estimate market distribution and value capture.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with edge infrastructure vendors, telecom engineers, industrial automation specialists, and enterprise IT architects. Technical feasibility, deployment constraints, and adoption timelines were assessed to refine USA Edge Computing market assumptions and structural insights.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized into a coherent market framework covering segmentation, competitive positioning, growth drivers, and adoption outlook. Cross industry technology convergence and infrastructure evolution patterns were incorporated to produce the final USA Edge Computing market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Low latency requirements for real time analytics and automation

5G expansion enabling distributed compute at network edges

Rising AI inference workloads deployed closer to data sources - Market Challenges

Interoperability issues across heterogeneous edge hardware and software

Security and patch management complexity across distributed sites

Power, cooling, and site readiness constraints for remote deployments - Market Opportunities

Private 5G plus edge bundles for factories, ports, and campuses

Edge AI optimization for video analytics in retail and public safety

Energy efficient edge infrastructure upgrades for distributed facilities - Trends

Growth of micro data centers and modular edge pods

Adoption of Kubernetes based edge orchestration and fleet management

Shift toward purpose built AI inference appliances at the edge - Government regulations

FCC spectrum and 5G deployment compliance requirements

NIST cybersecurity frameworks and supply chain risk management guidance

State privacy laws influencing edge data collection and processing practices - SWOT analysis

- Porters Five forces

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

- By System Type (In Value%)

Edge Compute Servers and Micro Data Centers

Industrial Edge Gateways and Controllers

Edge AI Accelerators and Inference Appliances

Edge Storage Nodes and Caching Systems

Edge Networking and SD WAN Edge Devices - By Platform Type (In Value%)

Telco Multi Access Edge Computing Platforms

Cloud Provider Edge Zones and Outposts

Enterprise Private Edge Platforms

Edge Colocation and Distributed Data Centers

Industrial OT Edge Platforms and SCADA Edge Stacks - By Fitment Type (In Value%)

Greenfield Edge Site Deployments

Brownfield Retrofit at Existing Facilities

Embedded Edge in Equipment and Machines

Portable and Containerized Edge Units

Hybrid Edge Integration with Central Cloud - By End User Segment (In Value%)

Manufacturing and Industrial Automation

Retail and Smart Stores

Healthcare and Connected Care

- Market Share Analysis

- Cross Comparison Parameters (Edge hardware portfolio breadth, Edge orchestration and management stack, Telco and 5G integration capability, Security and zero trust features, Deployment footprint and partner ecosystem)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dell Technologies

Hewlett Packard Enterprise

Cisco Systems

NVIDIA

Intel

AMD

IBM

Microsoft

Amazon Web Services

Google

VMware

Red Hat

Equinix

Vertiv

Schneider Electric

- Factories prioritize deterministic latency, ruggedization, and OT IT interoperability

- Retail deployments focus on in store video analytics, loss prevention, and personalization

- Healthcare use cases emphasize privacy controls, uptime, and edge enabled diagnostics

- Transportation users demand roadside and hub edge resilience with remote management

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now